Opinion leaders | Li Xunlei, Ma Jun

Since this year, the market's expectations of the path of the Federal Reserve's interest rate increase have been roller coaster. The employment market has strengthened beyond expectations, inflation has declined as scheduled, and the liquidity crisis in the banking industry has erupted. Has the Federal Reserve's interest rate increase come to an end? Will the existing monetary policy objectives be modified? Will interest rate hikes stop in March and beyond? This article is based on this analysis 。

Main points

The employment trend is generally optimistic, and the unemployment rate is difficult to reach a high point within the year 。 The labor force participation rate is still 0.8% lower than that before the epidemic. At present, the change caused by demographic changes is about 0.7 percentage points, which is the main reason for the decline of the current labor force participation rate. No collapse of labor demand The excessive attention to the layoff tide overestimated the degree of demand decline. On the whole, the size of the president is still smaller than the number of employees, and the vacancy level is still high. The gap between supply and demand is still high At present, the US labor market is still in short supply. The labor market is dominated by supply 。 The supply is dominant in the existing labor market, and the labor force flows into the market to fill the job gap. This has also led to a hot job market, although the economic environment is still declining, Indicators such as short-term unemployment rate are difficult to rise rapidly. We expect that the unemployment rate will only rise moderately in the year, and it will be difficult to climb to a high of 6%. At the same time, in view of the passivity and lag of labor market indicators such as the unemployment rate, we should pay less attention to employment indicators in the near future 。

In the medium term, inflation is difficult to return to the pre epidemic level 。 Inflation fell smoothly, only slowing down in January this year. However, before the weight adjustment, the year-on-year growth rate of CPI was 6.2%, which was in line with the market expectation at that time. Only core inflation "resists tenaciously" 。 From the perspective of the contribution of year-on-year CPI growth in the United States, the energy and food sub items continued to fall after peaking in the middle of last year. Concerns about the growth of energy and food items can be ignored, and we should focus on the core inflation which fell slowly. Core commodities are temporarily unimpeded 。 The overall contribution of core commodities to year-on-year CPI growth fell from a high 2.6% to 0.2%. However, the leading indicator Mannheim Price Index of used cars, its main sub item, has been positive month on month for two consecutive months, We need to be alert to the future rise of commodity inflation 。 data display Housing inflation resilience is far higher than expected, and it is expected that housing will ease in the second half of the year 。 The growth rate of non farm hourly wage is still far higher than the pre epidemic average, which may become the final resilience of support services. We believe that as inflation gradually falls back to a low level, its resilience may become prominent. At the same time, considering the possible "endogenous" impact of rent and other services, it may be difficult for the medium-term inflation to return to the pre epidemic level and remain above 3% 。

The liquidity crisis of regional banks may also spread. As the range and speed of this round of interest rate increase is rare, it will inevitably lead to "accidents". Silicon Valley Bank (SVB) announced bankruptcy on March 10. On March 12, the Federal Reserve, the Ministry of Finance, FDIC and other departments worked together to stabilize market sentiment temporarily, However, the solution can solve the symptoms but not the root causes. The UK pension crisis and the collapse of Silicon Valley banks are essentially confidence problems caused by the lack of liquidity due to mismatched asset durations 。 Recently, Credit Suisse also experienced a thunderstorm, causing the market to worry about its liquidity. We believe that the vulnerability of the global financial system will be further revealed in the future, and various small crises may occur more frequently or even evolve into global financial crises 。 Considering that its resilience will gradually emerge after inflation falls back, and that the vulnerability of the global financial market has become increasingly prominent in the near future, the Federal Reserve may take precautions, Re mention the old issue of inflation target modification to strive for space for policy change 。

It's hard to say that the interest rate increase cycle is over, and it is generally judged that the interest rate increase in March is 25 basis points 。 But the wise choice of the Federal Reserve should be to suspend interest rate increase in March. The weight of factors affecting interest rate increase should be: risk>inflation>employment 。 It is unlikely that the Federal Reserve will stop raising or lowering interest rates. Small crises can be solved only through quantitative tools of targeted liquidity. Under the benchmark scenario, the Federal Reserve may raise interest rates by 25 basis points in March and May respectively, and then end the process of interest rate increase. In addition to the benchmark situation, attention should be paid to the diffusive financial crisis and the adjustment of the Federal Reserve's policy objectives. Once the two types of events occur, the Federal Reserve's interest rate increase cycle will end as soon as possible 。

Employment: Unemployment rate is hard to reach a high point within the year

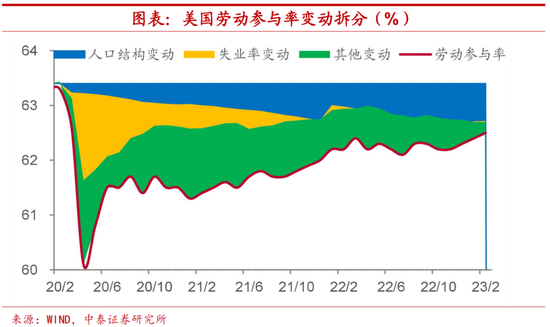

The labor force participation rate is still 0.8% lower than that before the epidemic 。 We divide the changes in the labor participation rate into three parts: permanent changes due to demographic changes, temporary decline in the labor participation rate due to drastic changes in the unemployment rate, and other reasons not including these two. Through calculation, we found that At present, the change caused by demographic changes is about 0.7 percentage points, which is the main reason for the decline of the current labor participation rate 。 This part measures the change in the total labor participation rate due to the change in the number of people of all ages when the labor participation rate of all ages remains unchanged. The supply shock brought by Xinguan has pushed the gap between supply and demand in the labor market to a new high 。

But the labor demand has not collapsed 。 Since the middle of last year, several industries led by the Internet in the United States have witnessed a wave of layoffs. Through statistics on the information that American enterprises have announced more than 100 layoffs in a single time since 2022, we found that the layoff craze reached a climax in January this year. By March 2023, the number of presidents had exceeded 180000. According to this information, some institutions had judged that the demand of the job market had stalled, We think that excessive attention to the layoff trend overestimates the degree of demand decline 。 one side The trend of layoffs is mainly concentrated in the information service and financial industries, and large-scale layoffs in a wider range of industries have not been observed yet. on the other hand The financial industry and information service industry responded earlier to the economic downturn, leading other industries. On the whole, the size of the president is still smaller than the number of employees, and the vacancy level is still high 。

The gap between supply and demand is still high 。 By calculating the difference between the number of job vacancies and the number of unemployed in the employment market, we can find that the supply and demand gap only fluctuated slightly during the layoff tide, but still remained at a high level. In January 2023, the difference will rise to 5.13 million, significantly higher than the pre epidemic level. This shows that at present, the labor market in the United States is still in short supply.

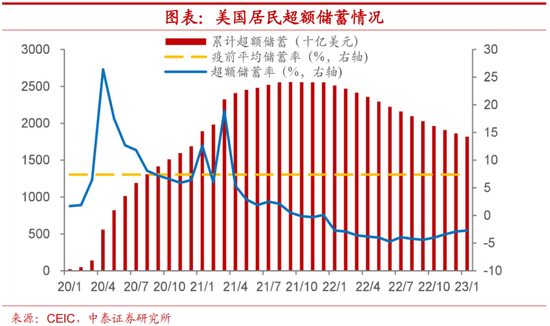

The labor market is dominated by supply 。 The US economic recession is approaching, and the employment index should show signs of cooling, but it is still not weak. In terms of demand In January, the number of job vacancies recorded 10.82 million, more than 3.8 million more than before the epidemic. The demand remained strong, and it was difficult to weaken in the short term. In terms of supply Due to the influence of income trend, the excess savings of residents continued to decline after the recession of financial subsidies. Under the expectation of economic recession, the labor supply rose. The unemployment rate in February was still at a historical low, recording 3.6%. We believe that in the existing labor market Supply occupies a strong position The labor force poured into the market to fill the job gap. This has also led to the fact that although the economic environment is still declining, the employment market is hot, and short-term unemployment rate and other indicators are difficult to rise rapidly 。

Unemployment rate is no longer sensitive, and it is hard to see a peak within the year 。 Under the background of demand cushion and supply dominated labor market, it is difficult to rapidly raise the level of unemployment rate due to the falling demand caused by the economic downturn. The work paper of St. Louis Federal Reserve also explains this phenomenon. The author divides job vacancies into employment and unemployed workers. The recent decline of job vacancies for employed workers has little impact on the unemployment rate. We expect that the unemployment rate will only rise moderately this year, and it will be difficult to climb to a high of 6%. At the same time, in view of the passivity and lag of labor market indicators such as the unemployment rate, we should pay less attention to employment indicators in the near future 。

Inflation: difficult to return to the pre epidemic level in the medium term

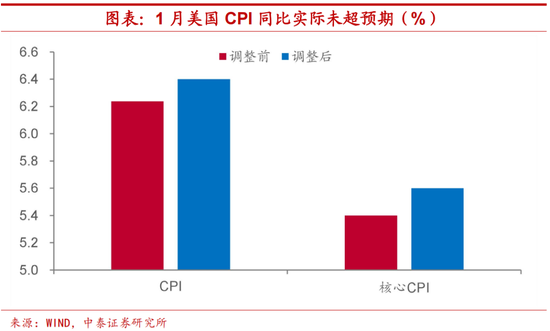

Inflation fell smoothly 。 The year-on-year growth rate of US CPI has accelerated since September last year, and slowed down only in January this year. But the CPI data in January exceeded expectations, not the deterioration of actual inflation, Weight adjustment of main cause statistics details 。 After restoring the weight of major adjustment items, we found that the year-on-year growth rate of CPI before adjustment was 6.2%, which was in line with the market expectation at that time. This shows that the inflation decline is still smooth in the near future, and there is no need to worry too much 。

Only core inflation "resists tenaciously" 。 From the perspective of the contribution of year-on-year CPI growth in the United States, the energy and food sub items continued to fall after peaking in the middle of last year. The growth of the energy sub items was mainly linked to the growth of crude oil prices. In the context of economic downturn in major economies around the world, the oil price was unlikely to rise significantly, and the food sub items, fertilizer and bulk commodities agriculture products There is a certain correlation between prices, and the upward possibility is also small. We believe that concerns about the growth rate of energy and food items can be ignored, and we should pay attention to the core inflation that has fallen slowly 。

Core commodities are temporarily unimpeded 。 Observing the contribution of the core inflation sub item to CPI, we can find that the contribution of core commodities has peaked since February last year, driven by the decline of second-hand car prices, and the overall contribution to the year-on-year growth of CPI fell from a high 2.6% to 0.2%. However, the leading indicator Mannheim Price Index of used cars, its main sub item, has been positive month on month for two consecutive months, We need to be alert to the future rise of commodity inflation 。

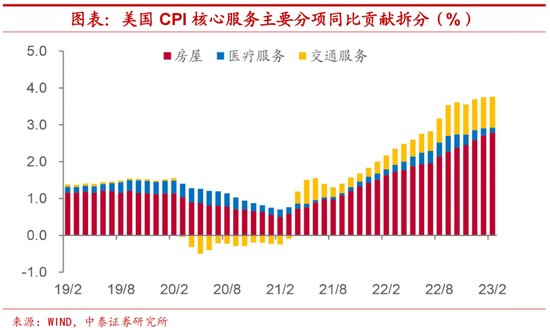

Housing is difficult to solve in the short term 。 The growth contribution of core service items has continued to rise since August 2021, without showing a decline. The contribution of housing items measuring rent is dominated and continues to rise. The relevant leading indicators such as house prices and zillow point to the housing inflation should have peaked at the beginning of the year, but the data shows that inflation resilience is far beyond expectations, and housing is expected to ease in the second half of the year. We believe that housing inflation is still resilient, and it is hard to be optimistic in the short term 。

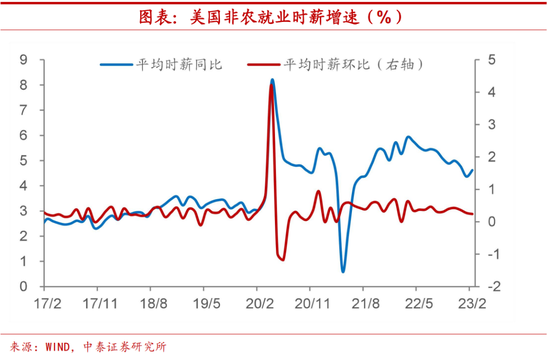

Low inflation is hard to return to before the epidemic 。 In addition to rent, the inflation related to wage growth, which made Powell's biggest headache, more stubborn. The growth rate of non farm hourly wage to measure wages was still far higher than the pre epidemic average, This may become the final toughness of supporting service items 。 We believe that As inflation gradually falls back to a low level, its resilience may become prominent. At the same time, considering the possible "endogenous" impact of rent and other services, the medium-term inflation low point may be difficult to return to the pre epidemic level, and remain above 3%.

How long can the interest rate increase last?

The range and speed of this round of interest rate increase is rare 。 from Rate increase range In just one year, the Federal Reserve has raised interest rates by 4.5%, far higher than the historical level. from Rate increase rhythm From the perspective of the initial pace of interest rate increase, the single interest rate increase gradually increased from 25 bp to 75 bp, and four consecutive interest rate increases at the 75 bp level, a record. Historically, the Federal Reserve may have a financial crisis at the late stage of each cycle of interest rate increase, and this cycle may not end happily.

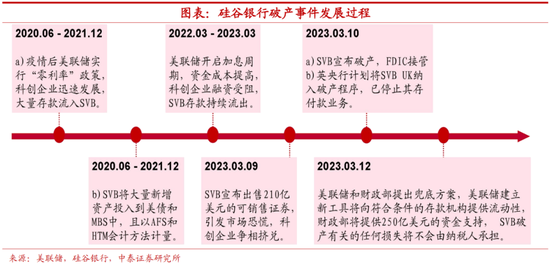

Silicon Valley Bank is just the beginning 。 Recently, the bankruptcy of Silicon Valley Bank (SVB) has attracted market attention. Before that, there had been the UK pension crisis and FTX bankruptcy. SVB went bankrupt because the Federal Reserve implemented the zero interest policy at the beginning of the epidemic, science and technology innovation companies developed rapidly, and SVB absorbed a large amount of funds. however As the Federal Reserve continues to raise interest rates, SVB's portfolio potential losses continue to expand In addition, the financing of scientific and technological innovation enterprises is blocked, the operation is difficult, and the deposits continue to flow out. SVB's debt side spending pressure increases sharply. In order to raise funds, SVB announced the sale of all its marketable securities of $21 billion and sought to raise $2.25 billion through the sale of common shares and preferred shares. As a result, the market panicked, and SVB ran to withdraw funds. On March 10, SVB officially declared bankruptcy and was taken over by the Federal Deposit Insurance Corporation (FDIC).

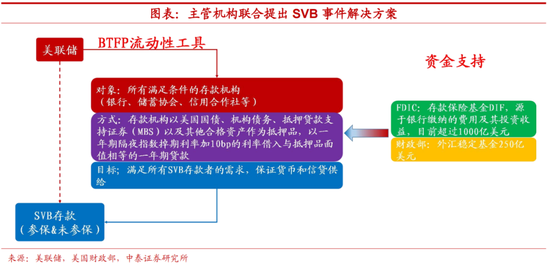

Solution does not cure the root cause 。 On March 12 local time, the Federal Reserve, the Ministry of Finance and the FDIC issued a joint statement that the Federal Reserve established the BTFP liquidity tool to provide one-year loans to all eligible depository institutions as liquidity turnover, and the FDIC and the Ministry of Finance provided financial support so that all SVB deposits could be preserved. The UK pension crisis and the collapse of Silicon Valley banks were jointly caused by a number of wrong decisions, and the existing asset duration mismatch caused the confidence problem of insufficient liquidity; There are also problems of improper management and moral problems. This time, many departments worked together to stabilize the market sentiment temporarily, but the action was not decisive enough, and it was only a temporary measure, not a permanent cure.

The banking crisis continues 。 On Tuesday, the annual report disclosed by Credit Suisse announced that its financial reporting procedures for 2022 and 2021 had "major defects". Credit Suisse had a net loss of 7.3 billion Swiss francs in 2022, and a large number of deposits and net assets flowed out in the fourth quarter, Cause the market to worry about its liquidity 。 The Swiss Central Bank and the Financial Market Supervisory Authority (FINMA) issued a joint statement saying that Credit Suisse meets the capital and liquidity requirements for systemically important banks. If necessary, The central bank will provide liquidity support to Credit Suisse 。 We believe that the vulnerability of the global financial system will be further revealed in the future, and various small crises may occur more frequently or even evolve into global financial crises 。

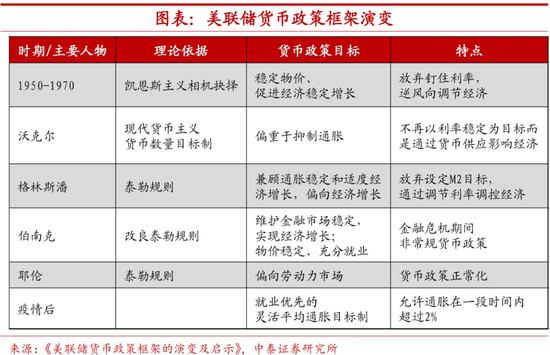

Monetary policy objectives are facing changes 。 After the outbreak of COVID-19, the Federal Reserve adjusted its monetary policy framework in August 2020 to seek a flexible average inflation targeting system with long-term stability. However, the labor market has changed greatly after the epidemic. The target policy orientation of the Federal Reserve's employment priority has increased the difficulty of fighting inflation in the United States. The labor market continues to be tense, and the inflation pressure is difficult to ease. At the end of last year, Bogsten, a famous economist at the Peterson Institute for International Economics (PIIE), a US think tank, questioned the monetary policy framework of the Federal Reserve and proposed to raise the inflation target from 2% to 4%. We believe that, in view of the resilience that will gradually emerge after inflation falls back, and the increasing vulnerability of the global financial market in the near future, the Federal Reserve may take precautions to revisit the old issue of inflation target modification, which is to strive for space for policy change 。

As for the interest rate policy of the Federal Reserve, we believe that it is unlikely to end the interest rate raising cycle 。 Considering the impact of various economic factors on the path of interest rate increase, The order of weight of factors affecting interest rate increase should be: risk>inflation>employment. Recently, the global financial market has fluctuated greatly, and small crises have emerged constantly, but the possibility of the Federal Reserve stopping raising or reducing interest rates is not very great. In the absence of a diffusive financial crisis, small crises can be solved only by targeting the quantitative tools of liquidity, without the use of interest rates, a price based tool. The UK's handling of pension storms is a precedent.

It is generally judged that the interest rate was increased by 25 basis points in March. Assuming that the regional and multipoint banking crisis is no longer spreading, the Federal Reserve may raise interest rates by 25 basis points in March and May respectively, and then end the process of raising interest rates. However, at present, the financial market has experienced severe turbulence, and American bank stocks have fallen sharply, further increasing the panic of investors and depositors. In order to stabilize expectations and avoid the liquidity crisis in the financial industry caused by the spread of panic, the Federal Reserve's wise choice should be to suspend interest rate hikes in March and make a decision after the financial situation is stable, so that the slope of the interest rate hike cycle becomes flat.

Historically, the highest point of each round of interest rate increase cycle is often prone to trigger financial risk events of different levels. This cycle of interest rate increase also has some risk points different from the past, such as the large-scale expansion of the central bank and the large-scale borrowing of the Ministry of Finance. Moreover, the rapid pace of interest rate increase and the long time of upside down of long-term and short-term treasury bond yields are relatively rare. In view of this, we believe that the Federal Reserve may change its policy objectives as described above in the future.

Second author Ma Jun: macro research assistant, Doctor of World Economics of Renmin University of China, visiting scholar of State University of New York, responsible for overseas economic and policy research.

(The author of this article introduces: Chief Economist of Zhongtai Securities.)