Opinion Leader | Peng Wensheng

For China at the current stage, it is necessary to pay attention to the debt repayment of the enterprise sector and local governments, which includes both the risk of default and the debtor's forced austerity in order to repay the debt, thus exerting downward pressure on the total demand. At present, China is in the downward phase of the financial cycle, and the endogenous demand momentum is insufficient. Different from the downward trend of the US financial cycle originating from the demand side, China is a typical trigger of the capital supply side, which requires the subsequent counter cyclical adjustment policies to be adapted. In addition, insufficient effective demand and the "decentralization" of the global industrial chain also have a negative impact on alleviating debt pressure.

In the debt risk resolution phase, risk appetite declined and the demand for safe assets increased, but the supply of safe assets endogenous in economic activities faced downward pressure. M2 (bank deposits) is the main part of the safety assets of Chinese residents and enterprise sectors. The recent weak demand for credit has led to a decline in M2 growth. In order to deal with the problem of insufficient effective demand on the entity side and weak risk appetite on the financial side, the key to macro countercyclical adjustment lies in fiscal expansion 。

China can think about debt resolution from the two dimensions of increment and stock. In terms of debt increment, the central government can appropriately increase the debt. The government debt is the asset of contemporary people, which increases the net assets of enterprises and households, thus helping to deleverage enterprises and households; In terms of stock, debt restructuring oriented by extension and interest reduction reduces the current debt service burden.

The different tools and transmission channels of macro policies are subject to different degrees of market constraints. The promotion of demand increase by reducing interest rates may be constrained by the exchange rate. The speed and extent of risk premium decline are affected by the macro environment, including the debt resolution process itself, geopolitical and other factors. In short, under the current situation, Central government debt is the most exogenous and counter cyclical, and is the most effective tool to deal with insufficient aggregate demand and resolve debt risks 。

——Peng Wensheng, member of China Finance 40 Forum (CF40), CICC Chief Economist, Head of Research Department, President of CICC Research Institute

This article is the keynote speech delivered by the author at the 2024 · Financial 40 Annual Conference and Closed door Seminar "Towards a Financial Power" Parallel Forum Session I and CF40 Quarterly Report on Macro Policy "How to Balance Debt Growth and Debt Risk" on April 20, 2024, which is released under the authorization of the author. This article only represents the author's personal views, not the positions of CF40 and the author's organization.

With regard to the debt problem and its risks, we need to first clarify the types of debt we are currently concerned about. For China at this stage, we pay more attention to the debts of non-governmental and physical sectors, especially the debts accumulated by local urban investment enterprises in the course of operation and related problems. In theory, local governments and their subordinate urban investment enterprises have the credit attribute of government departments, but in reality their financing conditions have the characteristics of private sector debt, and they are not really official debtors.

One kind of debt risk refers to default risk, which may cause losses to the financial system, or even financial crisis. The other means that the debtor is forced to tighten expenditure in order to repay the debt without debt default, thus exerting downward pressure on the total demand and increasing the pressure on debt repayment. From these two perspectives, economic downward pressure and debt risk are mutually reinforcing.

Any debt is accompanied by corresponding claims, so debt and assets are corresponding. In recent years, "balance sheet recession" has become a popular word, which can help us understand the debt problem vividly, but it describes a result more than the reason behind it. Only by understanding the causes of the balance sheet from prosperity to recession can we have a complete judgment of the policy situation, which is also a key motivation to look at the debt problem from the perspective of the financial cycle 。

The financial cycle refers to the medium - and long-term trend of changes in real estate prices and credit. Essentially, it refers to changes in assets and liabilities. The former refers to real estate, while the latter refers to debt related to real estate. Real estate is the most common collateral for credit. The two complement and promote each other, bringing about pro cyclical finance. When the real estate industry is in prosperity, credit expansion promotes the rise of house prices, which means that the value of its collateral rises, both of which lead to spiral procyclicality. However, this characteristic also means that once the financial cycle turns, the downward trend will last for a long time, and there will be greater resistance to re reversal in the short term.

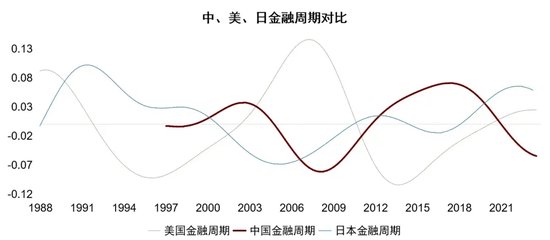

Compared with the latest estimates of the financial cycles in China, the United States and Japan, the upward curve represents credit expansion and rising house prices. It can be seen that China is currently in the downward phase, while the United States and Japan are on the upward side. Japan seems to have downward signs recently. This is partly one of the endogenous reasons for the current downward pressure on China's economy, that is, the negative impact of the real estate debt contraction on the economy.

Figure 1 Comparison of financial cycles between China, the United States and Japan

It is worth noting that not all financial cycle downturns are associated with economic recession and financial crisis, and the specific causes behind the downturns need to be explored in depth. For example, at the beginning of the 21st century, China's control over credit was actually tight. At that time, the financial cycle showed a downward trend, but the overall economic situation in China was optimistic over the same period. This is because at that time, the People's Bank of China's foreign exchange accounts increased and the monetary expansion was fast. For a period of time, half of M2 growth was related to the increase of foreign exchange accounts.

In most cases, the foreign exchange account is brought by the trade surplus, representing the increase in the net assets of non-governmental sectors such as enterprises and households. This was one reason why China's economy performed better even though it faced a downward financial cycle at that time. Different from the beginning of this century, the current downward trend of China's financial cycle is mainly manifested in the simultaneous contraction of credit and real estate 。

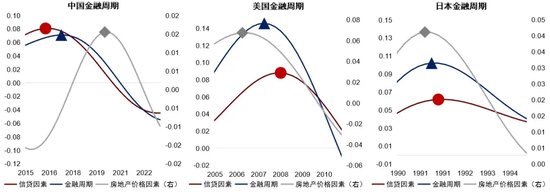

The reasons that drive the financial cycle downward have important implications for policy choices. Compared with the driving factors of the downward financial cycle in China, the United States and Japan, the downward financial cycle is driven by the typical policy of the United States, which starts with monetary tightening and works from the demand side. From 2004 to 2006, the Federal Reserve raised interest rates, American house prices peaked in 2006, and the financial crisis and credit crunch occurred in 2008. China is triggered by the supply side of funds. Starting from the strengthening of supervision and credit tightening at the 2017 National Financial Work Conference, housing prices will peak in 2021.

It seems that the result of the downward financial cycle in both China and the United States is the decline of housing prices and credit crunch, but the meaning of policy choices may be different: starting from the demand side and interest rates, the subsequent countercyclical adjustment is also based on monetary easing as the main carrier, for example, the decline in interest rates helps households and business sectors cope with the pro cyclicality of the decline in real estate and debt, However, financial supervision was strengthened after the crisis. That is to say, the financial regulation in the United States is pro cyclical, which requires that the counter cyclical monetary policy should be relaxed particularly, and the short-term interest rate should be reduced to zero.

Starting from the supply side and credit supervision, the subsequent countercyclical adjustment naturally starts from the supply side, which means that supervision is countercyclical. The countercyclical regulation helps to reduce the intensity of countercyclical monetary adjustment, which may be one of the reasons why China's monetary interest rate has not dropped so much.

However, such policy mix also faces challenges. Supply side (regulatory) policies are more structural and often targeted at specific industries, such as real estate. The promotion of total expansion may not be effective in the short term. For example, the deregulation of real estate credit is relaxed, but because of the strong pro cyclical nature of the real estate downturn, the boosting effect of the deregulation is relatively limited. Therefore, the pro cyclical nature of the downward trend of the current financial cycle deserves attention, and needs the cooperation of demand side policies to help counter cyclical adjustment. One of the aggregate policies on the demand side is the reduction of interest rates, which reduces the debt repayment burden, but also faces the problem of lack of pro cyclical endogenous momentum, Finance is truly exogenous and the most effective counter cyclical adjustment tool 。

Figure 2 Relationship between US Japan financial cycle, credit factors and real estate price factors

Weak demand increases pressure on debt repayment

In addition to the pro cyclical nature of finance, the debt problem is also affected by the overall economic situation. At present, China's economy is facing the problem of insufficient effective demand, which increases the pressure on debt repayment. The shortage of effective demand transcends short cycle fluctuations and has a cross cycle nature.

From the perspective of its causes, the lack of demand in China is certainly affected by the downward financial cycle, in addition to the "scar effect" brought by the COVID-19 epidemic. Compared with the United States, China's fiscal expansion during the epidemic was relatively limited, so the private sector was more affected.

Another reason for China's insufficient demand is the impact of global industrial chain adjustment. In the past Sino US trade cooperation model, on the margin, China produced and the United States consumed. At present, the United States is promoting "decentralization", which means that China is facing the pressure of insufficient demand and deflation, while the United States is facing the pressure of insufficient supply and inflation.

The difference in internal demand between China and the United States is reflected externally in the change of exchange rate, that is, the depreciation of the real exchange rate of RMB and the appreciation of the real exchange rate of the dollar. Considering that the RMB real effective exchange rate has not depreciated against a basket of currencies recently, the difference in the performance of the real exchange rate between China and the United States is not only caused by the change of the nominal exchange rate, but also reflects the difference in the inflation trend between the two countries.

Figure 3 Real effective exchange rate index of RMB and USD

In theory, between two open economies, when one side's demand is strong and the other side's demand is weak, it is normal for one side's exchange rate to appreciate and the other side's exchange rate to depreciate. However, China and the United States are currently facing not only economic problems, but also geopolitical factors. In the past two years, China's exports have shown an obvious trend of price decline and quantity increase. In fact, to some extent, exports have helped the United States control its domestic inflation. However, recently, European and American countries have emphasized China's overcapacity and subsidies, showing a protectionist trend. How to understand this problem and deal with the so-called overcapacity and trade protectionism in the future may also be a factor to be considered in macro policies.

Figure 4 China's export volume and price on a quarterly basis

Debt risk and safe assets

Any debt has its corresponding assets, which may be either risky assets or safe assets. In the debt risk resolution phase, the risk appetite of the residential sector declined and the demand for safe assets increased. This is because as the debt risk premium rises, market participants will pursue more safe assets, but the supply of safe assets endogenous in economic activities is facing downward pressure. If the supply of safe assets is insufficient at this time, the pro cyclical downward trend of finance may intensify.

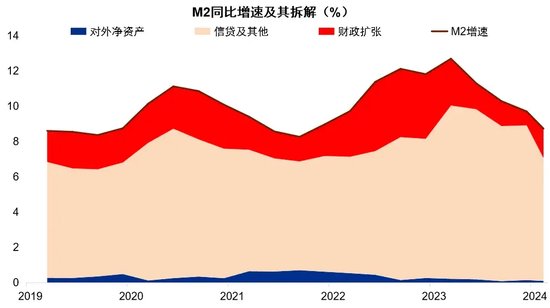

M2 (bank deposits) is the main part of the safety assets of Chinese residents and enterprises. The growth rate of M2 fell from 8.7% in February to 8.3% in March. The monetary and credit data has a strong forward-looking significance. The recent decline in M2 growth rate is worth being vigilant. The main reasons behind this are weak credit demand and lack of vitality in the economy.

Figure 5 M2 year-on-year growth rate and its disassembly (%)

In order to address the problem of insufficient effective demand on the entity side and weak risk appetite on the financial side, The key to macro counter cyclical adjustment lies in fiscal expansion 。 China is in the second half of the financial cycle, and the ideal policy choice is to promote monetary easing and fiscal easing in the case of credit crunch (or the regulatory counter cyclical adjustment effect is limited), which is also the way Japan and the United States used to deal with the downward financial cycle (including the pro cyclical nature of regulation). This policy combination requires monetary easing and fiscal expansion. If there is only the former, the effect of interest rate reduction is low and the policy effect is relatively limited.

The increase of central government debt is the key to fiscal expansion, but the problem is how to judge the appropriate level of central government debt? All debts have debtors and creditors. Debtors of central government debts are essentially the next generation of residents, while creditors are the contemporary private sector, including enterprises and families. Therefore, the increase in central government debt corresponds to the current rise in private sector net assets, which helps enterprises and households to deleverage and defuse debt risks.

Therefore, the issue of whether the central government debt level is acceptable is equivalent to whether contemporary people should overdraw the assets of the next generation, and whether we need to worry about the debt burden 30 to 40 years later. With technological progress, the answer should be no, because the economic growth brought by technological progress can effectively dilute the debt level and reduce the burden of repayment. Of course, this does not mean that government debt can expand indefinitely. If government debt grows too fast, leading to rising inflation, private sector resource allocation will be squeezed.

In short, The criterion for judging the sustainability of central government debt is not the scale of debt, but the level of inflation 。 For example, Japan's central government debt has reached 300% of GDP, but due to low inflation, it has not caused problems.

Based on the above discussion, we can think about debt risk resolution from the two dimensions of increment and stock.

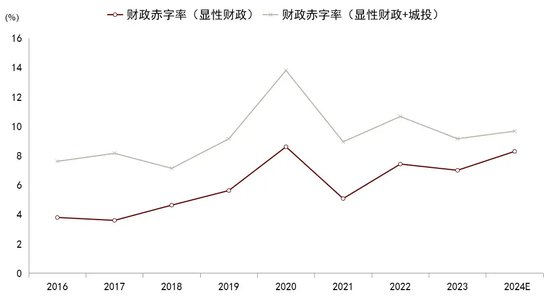

In terms of debt increase, the central government has room to increase debt 。 Recently, China's broad fiscal deficit ratio has increased only marginally, and there is still room for central government debt to help enterprises and residents reduce their debt burden. From the specific data, although this year's explicit fiscal deficit rate (including budget and government funds) has increased to a certain extent, if the implicit fiscal behavior such as urban investment is taken into account, the broad deficit rate is basically stable compared with last year.

The second aspect of incremental debt is policy finance, which can be understood as a quasi fiscal behavior. At present, the proportion of real estate in new loans has dropped to about zero, but the overall credit level still shows some resilience. This is because credit is supported by policy finance in infrastructure, manufacturing, inclusive, green and other fields, and the proportion of credit invested in these fields has reached about 80% of the total new credit.

Policy finance provides funds from the supply side to help maintain a stable credit level. However, it is worth noting that these credits mainly help enterprises, and enterprise investment is not the final demand. Therefore, the expansion of policy based finance cannot effectively solve the problem of insufficient demand, which may exacerbate the so-called overcapacity problem and is difficult to drive a sustained and healthy economic recovery.

Figure 6 2016-2024E Generalized Fiscal Deficit Rate

Figure 7 Proportion of new TTM of various loans

In terms of stock, the fundamental problem of local debt is that its financing conditions are commercial while its credit conditions are governmental. This combination has brought good investment opportunities to some creditors in the past decade, but it is ultimately unsustainable. Considering the high yield enjoyed by these creditors in advance, The key to resolving the risk of existing debt lies in promoting debt restructuring 。 Debt restructuring does not mean a large-scale default, but can roll over the existing debt and reduce the interest rate to a level consistent with the government's credit. Considering the herding effect of the open market, debt restructuring can be achieved mainly through non-standard channels including credit. Such a combination will help reduce the moral hazard that may be brought about by the expansion of central government debt.

Specifically, how the central government increases debt and provides safe assets involves the question of who will expand the balance sheet of the central bank and commercial banks. Commercial banks create deposits through credit. In the context of deposit insurance and government credit guarantee for banks, deposits are also safe assets, but their risks are different from those behind the safe assets provided by the central bank.

At the beginning of the 21st century, China is facing a downward financial cycle, but the overall economy is improving. One of the important reasons behind this is that the central bank releases base currency through the purchase of foreign exchange. This is essentially a quasi fiscal behavior, which is reflected in the increase of bank deposits of enterprises and residents. From the subprime crisis in 2008 to 2017, the balance sheet scale of China's commercial banks expanded, while the central bank shrank its balance sheet in the same period. Since 2017, the expansion rate of commercial banks has slowed down significantly, while the central bank has continued to shrink its balance sheet. The overall performance is that the growth rate of China's safe asset supply has slowed down, which is also the fundamental reason for the tight overall financial environment in the same period.

From the perspective of international experience, the Federal Reserve and commercial banks in the United States have both started significant expansion of their balance sheets in 2008 and 2020, effectively matching the fiscal expansion in the same period. An important lesson of the American experience is that, In order to cooperate with the financial strength and increase the debt of the central government, the central bank can expand the balance sheet accordingly 。

Figure 8 Proportion of total assets of the People's Bank of China and total assets of commercial banks in GDP

Source: Wind, Research Department of CICC.

Note: Data as of the fourth quarter of 2023.

Figure 9 Proportion of total assets of the US central bank and commercial banks in GDP

Source: Bloomberg, Research Department of CICC.

Note: Data is as of the third quarter of 2023.

Market constraints: certainty and uncertainty

The policy options for resolving the debt problem have been mentioned above, but different tools and transmission channels of macro policies are restricted by the market to varying degrees. In the face of this downward financial cycle, China's policy path starts with deregulation to promote capital supply, and then reduces interest rates to promote endogenous demand.

Figure 10 Change of 10-year treasury bond yields in China and the United States

Source: Wind, Research Department of CICC.

Figure 11 Comparison of risk premium between US shares and A-shares

At present, the direction of interest rate reduction is relatively certain. First, from the perspective of Friedman's inflation expectations, the current real interest rate is on the high side and needs to be lowered with the yield of government bonds as the interest rate indicator. Second, from the perspective of Keynes' liquidity preference, the current real interest rate is also at a high level, taking the A-share risk premium as an indicator of interest rate.

However, there is also uncertainty behind the determined policy path. As for the former option, it may be necessary to consider the constraints on the exchange rate side to reduce interest rates to promote demand growth, A more effective measure is to boost demand through fiscal expansion and stabilize the exchange rate by boosting confidence 。

For the latter option, the speed and extent of risk premium decline are affected by debt resolution process, geopolitical situation and other factors, which also face some uncertainty. In order to deal with these factors and reduce the uncertainty of the policy effect, the policy option of reducing risk premium also needs financial support.

In short, under the current situation, Only finance, that is, central government debt, is the most exogenous and counter cyclical, which is the most effective tool to deal with insufficient demand and resolve debt risks 。

Source: China Finance 40 Forum

(About the author: Chief Economist and Head of Research Department of CICC)