Wenwu Chaoming Macro Team

Wu Chaoming (Vice President of Caixin Research Institute, Chief Economist of Caixin Securities) Hu Wenyan Chen Ran

text

Since late February, the spread of COVID-19 overseas has accelerated, the international financial market has adjusted significantly, and the market's concern about the financial crisis has risen sharply. The market has different views on whether the global financial crisis has occurred. Some believe that a global financial crisis has occurred, and others judge that a financial crisis has not yet occurred. For example, on March 22, the leadership of the Central Bank said that "it is too early to conclude that the world has entered a financial crisis", and pointed out that "the international financial crisis usually has three basic characteristics: first, whether there is a cross market and continuous panic decline in the international financial market; second, whether there are a large number of financial institutions, especially systemically important financial institutions, have failed. The third is to see whether the operation of the global real economy has been seriously damaged ".

In addition to observing capital market price signals, panic and other indicators, how to understand the operating mechanism behind the crisis may be more critical and profound in judging whether a financial crisis will occur. Based on the understanding that the nature of the epidemic public health crisis is different from that of the financial crisis, and that the essence of the financial crisis is the passive and rapid contraction of the balance sheets of enterprises, households and financial institutions, this paper believes that major economies in the world, especially the United States, have built "three firewalls" for enterprises, households and financial institutions, leading to the "financial accelerator" of the financial crisis The mechanism and the "wealth effect" mechanism have been temporarily frozen, and the financial crisis is safe in the short term.

However, if the epidemic prevention and control time is too long, and the economic indicators continue to deteriorate after the real economy has been "shocked" for too long, it will easily break the "three firewalls". Under the role of the "financial accelerator" and the "wealth effect" mechanism, the financial crisis will occur, and the financial and real economy will fall into a vicious circle. Therefore, the global top priority is to effectively prevent and control the epidemic.

1、 There are some early signs of financial crisis

From the perspective of asset prices, credit spreads, dollar liquidity, short-term economic growth and other indicators in the financial market, there have been some crisis signals.

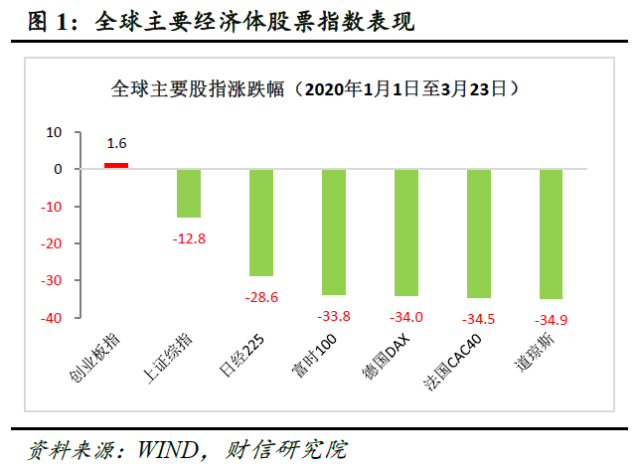

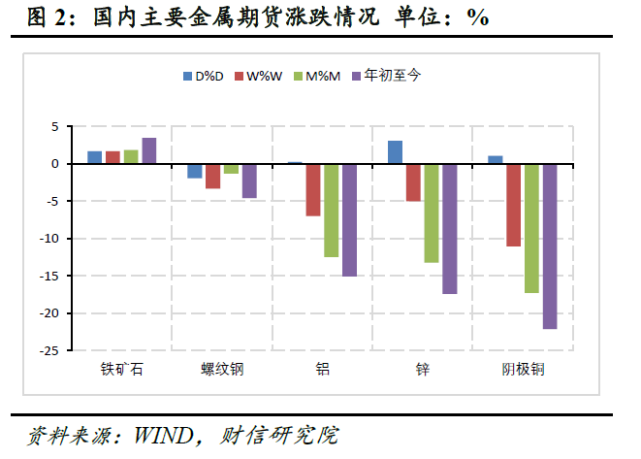

First, asset prices in the financial market continued to fall unexpectedly. Since mid to late February 2020, the US stock market has experienced four "circuit breakers" in a row, breaking the historical record. As of March 23, the stock indexes of the US, Europe, South Korea and some emerging market economies have all declined by more than 30% this year (see Figure 1); At the same time, the price of crude oil dropped by more than 50% and the price of copper, zinc and other metals dropped by about 20% during the year (see Figure 2). From historical experience, the huge decline of stock markets and bulk commodities is one of the important characteristics during the crisis.

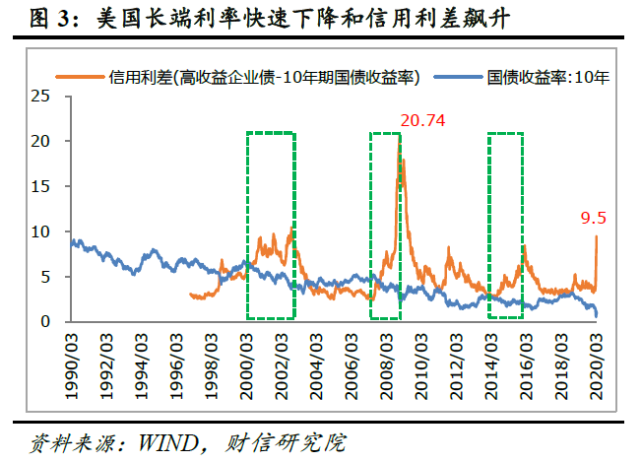

Second, the long-term interest rate dropped sharply, and the credit spread soared to the crisis level. On March 16, on the basis of an emergency interest rate cut of 50BP at the beginning of the month, the Federal Reserve cut the interest rate by another 100BP, directly reducing the federal benchmark interest rate to 0-0.25%, which drove the yield of the U.S. 10-year treasury bond to 0.54% for a time, with the largest drop of more than 130BP in the year. On the contrary, the interest rate of high-yield corporate bonds in the United States has soared, and the credit spread represented by the difference between its yield and that of 10-year government bonds has risen to 9.5% (see Figure 3), which is comparable to the level during the crisis in history. This shows that market risk appetite has declined sharply, investors are pessimistic about economic growth expectations, and they are willing to reduce investment in high-risk assets.

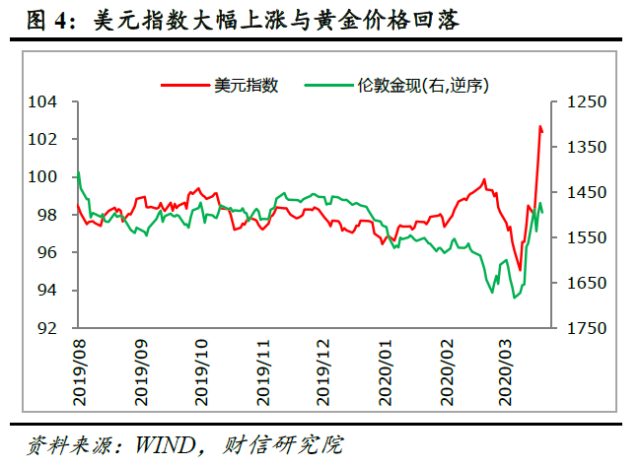

Third, there was a global "dollar shortage", and gold and other safe haven assets were also sold off. Influenced by the spread of COVID-19, the downward pressure on the US economy has continued to increase. However, since mid March, the US dollar index has run counter to the fundamentals, rising by about 8% and breaking through the 100 threshold (see Figure 4). This reflects that the turmoil in the financial market may have triggered concerns about US dollar liquidity. In order to respond to the impact of the financial market and effectively adjust the balance sheet, and at the same time prevent the risk of shrinking overseas US dollar supply caused by the reduction of the US trade deficit in the future, investors' demand for US dollars has increased significantly, pushing up the US dollar index. For this reason, investors are even willing to sell gold and other safe haven assets in exchange for dollars. For example, the maximum retreat of London gold price since the high point on March 9 has been close to 15% (see Figure 4).

Fourth, the domestic real economy index hit a record low, and the probability of global recession in the second and third quarters was high. From the domestic economic data in January and February, the supply side industrial added value fell by more than 10%, and the demand side consumption and investment fell by more than 20%, both of which hit a record low. In February, the manufacturing boom index PMI fell to 35.7%, lower than the lowest value of 38.8% in November 2008, indicating that the short-term impact of the epidemic on the domestic economy has actually exceeded the 2008 financial crisis. Seen from the situation abroad, the outbreak of COVID-19 in the United States and Europe is just beginning to show its impact on the economy. For example, some published data show that the manufacturing index of the Federal Reserve of Philadelphia in the United States was - 12.7% in March, down nearly 50 percentage points month on month, and the German business climate index also fell sharply in the same period. If we extrapolate the economic situation of Europe and the United States in the coming months according to the performance of China's economic data under the impact of the epidemic, it is not difficult to find that the probability of major developed economies in the world falling into recession in the second and third quarters is very high.

Does the above financial and real economy indicators with crisis signals mean that the world has entered a financial crisis or economic crisis?

2、 The essence of the financial crisis is the rapid and passive contraction of the balance sheet

The above capital market indicators frequently show the early warning of financial crisis or the signals that have occurred. However, to judge whether the current financial crisis is or not, it is not enough to rely on these signals alone, and more rigorous logical dialectics is needed. There are many reasons for the financial crisis, although the final result is mostly manifested in the collapse of the systematic financial structure, the panicky decline of asset prices in the global financial market, and the sharp decline in the growth of the real economy. The direct reason for the sharp adjustment of global stock markets this time is the spread of the epidemic in the world. Before judging whether the public health crisis will further lead to the global financial crisis, it is necessary to distinguish between the nature of the epidemic public health crisis and the financial crisis, because the impact mechanism of the two on the economy is not the same, so the results will be different. It is not appropriate to confuse the reasons for the sharp adjustment of the stock market. The devil is in the details.

(1) The nature of epidemic public health crisis is different from that of financial crisis

For the epidemic public health crisis, although the epidemic is short-term, the prevention and control of the epidemic will lead to a shock suspension of economic production activities, so its impact on the economy is short but the damage is great. During the outbreak of the epidemic, the adjustment of asset prices was not caused by problems in the balance sheets of households, enterprises, financial institutions and other sectors of the economic system. Therefore, after the epidemic, there is no need to make significant contraction and adjustment, and there is no need to go through the painful process of short-term significant deleveraging. After the "play key" is turned on, the remaining economic entities can continue their normal production and living activities.

As for the financial crisis, because the balance sheets of households, enterprises, financial institutions, governments and other sectors in the economic system have major problems, which require rapid contraction and adjustment, and face a long-term deleveraging process, the impact of the crisis on the economy is not temporary, but long-term. In addition, in the financial crisis, social production and living activities do not need shock suspension. Both supply and demand will exist, but the intensity is weakening. However, to restore demand to normal levels, the balance sheet needs to be restored to a healthy state, which takes several years.

Therefore, the impact of the epidemic public health crisis on the economy is short but large, and economic entities do not need to significantly deleverage; The impact of the financial crisis is long and far-reaching, and economic entities face a long-term deleveraging process.

(2) Two key mechanisms leading to the outbreak of financial crisis

The sharp adjustment of asset prices, such as stock and real estate prices, triggered the financial crisis mainly because of two mechanisms: the financial accelerator mechanism and the wealth effect contraction mechanism. Under the effect of these two mechanisms, enterprises, households and financial institutions quickly and passively shrink their balance sheets, leading to rapid deleveraging.

In the first financial accelerator mechanism, the sharp adjustment of asset prices will lead to a rapid reduction in the value of assets used by the enterprise sector for mortgage loans and a decline in the ability of enterprises to mortgage loans. At this time, banks will assess the credit risk of enterprises and either require enterprises to add collateral or repay loans in advance. Banks will be reluctant to lend or raise the level of loan interest rates, The balance sheet of enterprises has entered a stage of passive and rapid contraction, and the decline in investment growth has become inevitable. Under the effect of the mechanism, both enterprises and banks will face the rapid contraction of their balance sheets, the weakening and outright withdrawal of banks' financial intermediary functions, and form a negative feedback cycle of rapid reduction of real economy growth and sharp deterioration of financial risks.

In the second wealth effect mechanism, the sharp adjustment of asset prices and the decline of household sector wealth, on the one hand, lead to the decline of the mortgage capacity of the household sector, on the other hand, directly weaken the consumption capacity, which will eventually lead to the reduction of consumption expenditure, and the household sector needs to shrink and adjust its balance sheet.

In the process of the two mechanisms, the financial sector is deeply involved. The weakening of the credit capacity of enterprises and households and the deterioration of the quality of credit assets will affect the asset and liability structure of the financial sector, which is one of them; Second, financial institutions themselves also have investment in stocks, real estate and other assets. The adjustment of these asset prices will also worsen the quality of their assets and liabilities. Therefore, the financial sector will inevitably shrink its balance sheet.

To sum up, in the process of substantial asset price adjustment, enterprises, households and financial institutions will face the process of rapidly and passively shrinking their balance sheets. The short-term drastic adjustment of the balance sheet has led to the occurrence of financial crisis, which in turn has led to the tide of enterprise bankruptcy, unemployment and other phenomena in the real economy. Therefore, the essence of the financial crisis is the rapid and passive contraction of the balance sheet. As long as measures are taken to prevent or block this process of contraction, the financial crisis will not happen for the time being.

3、 All central banks have built "three firewalls" to ensure short-term crisis free

At present, in order to deal with the risks caused by the impact of the epidemic and the intensification of the turbulence in the international financial market, the central banks of the countries represented by the Federal Reserve have taken quick action. By reducing financing costs and providing unlimited liquidity, they have built "three firewalls" in financial institutions, enterprises and the residential sector, effectively avoiding the rapid and passive contraction of the balance sheets of the three entities in the short term.

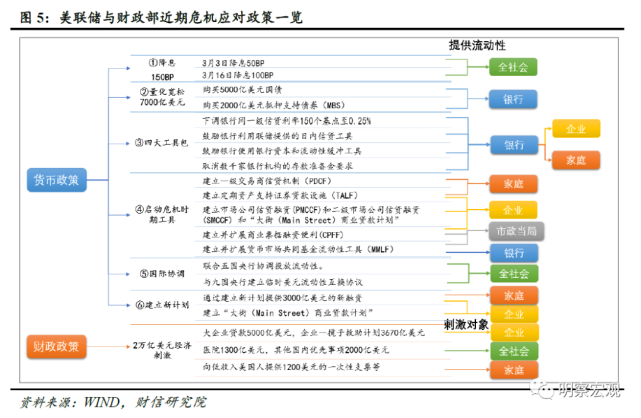

The "first firewall" is in front of financial institutions after multiple rounds of reinforcement. As the core subject of credit creation, financial institutions are the key to maintaining the stability of the financial market and supporting the real economy to overcome difficulties. The Federal Reserve seized on this point and launched the following package of crisis response plans (see Figure 5) to prevent financial intermediaries from weakening or withdrawing.

first , cut the interest rate to 0 more than expected. The Federal Reserve cut interest rates by 50 BP and 100 BP on March 3 and March 16, respectively, and directly reduced the federal funds rate to 0-0.25% to ensure that financial institutions can obtain ultra-low cost funds. secondly And announced the launch of a quantitative easing policy of about 700 billion US dollars. The Federal Reserve purchased US $500 billion of treasury bonds and US $200 billion of mortgage-backed bonds respectively to maintain sufficient liquidity within the financial system and support key market functions. third , using four toolkits. Including lowering the inter-bank primary credit rate, encouraging banks to use intra day credit tools, encouraging banks to use bank capital and liquidity buffer tools, and canceling the deposit reserve requirements of thousands of banking institutions to increase the liquidity of financial institutions. fourth , restart tools in crisis period. For example, the establishment of a primary dealer credit mechanism (PDCF) and the establishment and expansion of money market mutual fund liquidity (MMLF) will directly inject liquidity into financial institutions.

The "second firewall" is steadily added to the enterprise department. The COVID-19 epidemic has led to a short-term "shock" in the economies of various countries, and many small and medium-sized enterprises have fallen into serious difficulties in their production and business activities. In order to directly and effectively save the basic stock of the enterprise subject most affected by the epidemic, reduce its losses, ease the pressure of credit contraction, and ensure that the economy can be quickly repaired after the elimination of the interference of the epidemic, the Federal Reserve will bypass financial institutions and become the "lender" of enterprises directly to deliver liquidity (see Figure 5).

one side The Federal Reserve restarted its tools in crisis period, established and expanded commercial paper financing facilities (CPFF), and provided liquidity for commercial paper issuers; Establish a Term Asset Backed Securities Loan Facility (TALF) to unconditionally provide loans to certain AAA rated ABS holders. on the other hand The Federal Reserve has set up a number of new liquidity instruments to support SME financing, such as the primary market corporate credit financing (PMCCF) for issuing new bonds and loans and the secondary market corporate credit financing (SMCCF) for providing liquidity for outstanding corporate bonds, and announced the "Main Street commercial loan project" To support eligible SME loans. It is worth noting that since the Federal Reserve cannot lend directly to enterprises and households according to the law, the Federal Reserve will provide loans to enterprises from CPFF, TALF, PMCCF and SMCCF by providing funds for special purpose vehicles (SPVs), and the Ministry of Finance will use ESF to make equity investment in SPVs.

The "third firewall" has been added to the residents' department. The impact of the epidemic superimposed on the sharp adjustment of the stock market, the income and wealth of residents were faced with great losses, and the pressure on consumption and debt repayment of residents increased, which was self-evident for the damage to the economy. To this end, the Federal Reserve restarted the crisis period tool (see Figure 5), set up the commercial paper financing facility (CPFF), and eliminated most of the risks of its inability to repay investors by extending the mature commercial paper debt of qualified issuers; Establish a term asset backed securities loan facility (TALF) to provide liquidity support for consumer loans.

After the above three layers of reinforcement, combined with the Ministry of Finance's $2 trillion financial support plan, the liquidity pressure faced by financial institutions, enterprises and the residential sector will be significantly reduced in the short term, and the pressure on balance sheet contraction will also be significantly reduced. Under the strong policy hedging, the probability of financial market crisis will also be greatly reduced.

4、 It is really necessary to prevent the occurrence of financial crisis caused by too long epidemic prevention and control

Although the macro decision-making departments of various countries have built "three firewalls" for the crisis in the short term, the economic society is a dynamic cycle system and cannot be suspended for a long time. If the overseas epidemic cannot be effectively controlled, causing economic "shock" for a long time, the difficulty of economic recovery or exponential growth, the probability of economic crisis and financial crisis will also increase greatly.

On the one hand, the epidemic prevention and control is too long, and the economy faces the risk of turning from recession to depression. At present, the epidemic situation in the United States and Europe is in an outbreak period. It is not difficult to deduce the impact of the epidemic situation on other countries according to the current losses suffered by China. It is not difficult to find that the global economy, especially the major developed economies, showed negative growth in the second and third quarters, with a high probability of falling into recession. If the epidemic prevention and control time is further prolonged, the global economy will show negative growth for consecutive quarters, and the characteristics of "three low and two high" in the economic system, namely, "low growth, low inflation, low interest rate, high leverage, and high risk", may be further amplified, and potential economic contradictions and problems may also be triggered and exposed, causing economic depression and economic crisis.

On the other hand, the long-term recession of the real economy is expected to form a negative feedback cycle with the financial market, breaking the existing "three firewalls". The current stimulus policies can alleviate the pessimistic expectations of the market in the short term, stabilize market sentiment, and maintain the stable operation of the economy and financial system, but cannot support the long-term development of the economy and financial system. If the epidemic prevention and control is delayed for too long, the real economy indicators continue to deteriorate, investors' pessimistic expectations will come back, even more panic and collapse, and the "three firewalls" will be easily broken, which will bring more heavy blows to the financial market. Under the role of the "financial accelerator" and "wealth effect" mechanism, the financial crisis will occur, Finance and the real economy fall into a vicious circle. Therefore, the urgent task is to effectively prevent and control the epidemic.