Opinion leaders | Luo Zhiheng, Fang Kun

1、 Policy resolution: the interest rate will be increased by 75bp in July, and the rate of scale reduction will be doubled in September

This interest meeting decided to raise the interest rate by 75bp, and the speed of reducing the interest rate remained unchanged, which was in line with market expectations. With regard to interest rate increase, this meeting raised the interest rate by 75bp to 2.25% - 2.50%, and the policy interest rate has reached the peak of the interest rate increase cycle in 2018. As for the scale reduction, the current rate of scale reduction remains unchanged, with a monthly reduction of US $47.5 billion in US debt and MBS. In September, the scale reduction was accelerated to a monthly reduction of US $95 billion in US debt and MBS.

Before this meeting, June data showed that inflation was off anchor "breaking 9", and the unemployment rate was at a historical low. Both core data supported hawkish interest rate hikes. The market was worried about raising interest rates to 100bp. There are two reasons why the Federal Reserve chose 75bp to avoid a larger interest rate increase.

First, recession expectations are accumulating, and the economy is weakening or it is difficult to resist faster interest rate hikes. Although there was no inflection point in the inflation and unemployment rate data, the economic data of PMI and other more subdivisions in June weakened, and the market's recession expectations were constantly strengthened. According to the Atlanta Federal Reserve's GDP now model, the real GDP of the United States in Q2 2022 will show negative growth for two consecutive quarters, with an annualized rate of - 1.2%, which has met the basic conditions for the NBER to identify economic recession. The US economy is facing the risk of a technical recession. The Federal Reserve pursues a soft landing, and recession for inflation is not the desired outcome of the Federal Reserve.

The second is to maintain the credibility of the Federal Reserve and avoid faster interest rate hikes exacerbating market panic. Keep consistent with the interest rate forward-looking guidance of the last meeting. Under the intertwined uncertainty of global inflation, supply bottlenecks, geopolitical conflicts and other factors, the Federal Reserve acted on an opportunistic basis and dynamically adjusted its policies. At the press conference of the interest meeting in June, Powell gave two options: 50bp and 75bp. If the interest rate is increased by a larger margin, the market expectation will be confused, or a broader market turbulence will be triggered.

2、 Conference statement: the economy is weak and inflation is difficult to solve

The keynote of the statement at this meeting was neutral, which not only recognized the signs of economic slowdown, but also emphasized that continued high inflation led to continued interest rate hikes of 75bp and the reduction of the table as planned.

On the economy, the statement first responds to the market's concerns about the economy. The first sentence of the statement made it clear that the recent consumption expenditure and production indicators have been softened, which is consistent with the current market recession expectations, corresponding to the weakening of the U.S. personal consumption expenditure on a month on month basis, and the negative growth of the U.S. industrial output index on a month on month basis in June. Although acknowledging the economic slowdown, the Federal Reserve does not seem to give up the hope of soft landing. The current strong job market is the bottom line of the Federal Reserve.

With regard to inflation, the upward pressure on food prices is particularly mentioned. The statement changed the term of the Russia Ukraine conflict from "Russia's invasion of Ukraine" to "Russia's war against Ukraine", reflecting that the geopolitical conflict may last longer and may continue to drive up inflation. In the inflation statement, the statement added the "food" factor, because food is related to people's livelihood, and restoring price stability is also the political task of the Federal Reserve. In June, the CPI of the United States hit a new high of 9.1% year on year, and there was widespread pressure to raise prices in all sub items. The Federal Reserve also had no choice but to continue to raise interest rates significantly. The food CPI was 10.4% year on year, driving the overall CPI 1.4 percentage points year on year.

As for table reduction, it was added that the rate of table reduction would be increased in September as planned. According to the established plan, the current scale reduction is still in the transition period of three months, and the rate of scale reduction from June to August is to reduce US debt and MBS holdings of US $47.5 billion every month. In the policy implementation part of the July meeting, the Federal Reserve added that in September, it began to speed up to reduce its holdings by $95 billion a month, including $60 billion in US Treasuries and $35 billion in MBS.

With regard to voting, the statement of this meeting was unanimously adopted. This is consistent with the statements of the voting committees before the silence period of this meeting. Even the most hawkish voting committee did not choose to raise interest rates by a higher margin. Barr, the newly appointed Federal Reserve's vice chairman of supervision in July, also voted to raise interest rates by 75bp.

3、 Answer to the reporter: Suggest that the pace of interest rate increase will slow down and strive to achieve a soft landing of the economy

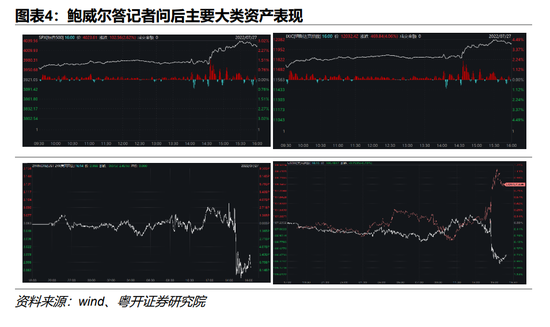

Powell's speech released a dove signal, and the market risk appetite increased, This is reflected in the strength of both stocks and bonds, and the weakness of the US dollar. The US stock market continued to expand its gains after the press conference. The S&P 500 index and the Nasdaq index closed up 2.61% and 4.06% respectively. The two-year interest rate of US bonds fell by up to 8bp, the US dollar index fell by 0.70%, and the gold price rebounded by 0.86%.

The weak economy superimposes on the tightening and overweight, and the interest rate increase may be slowed down in the future. Powell's opening remarks were basically consistent with the conference statement. Powell first pointed out that some recent economic indicators in the United States have been weak, including a sharp slowdown in the growth of consumer spending, weakening real estate demand, and declining private enterprise investment. However, when Powell changed his subject, the labor market was still strong, which showed that the total demand was still stable, intended to deny recession, and there was still room for a soft landing in the future. With regard to inflation, he reiterated that inflation was too high. Although the price of commodities had fallen recently, the earlier surge had pushed up prices and increased inflationary pressure. The path of subsequent interest rate increases will depend on the future data and economic prospects, and decisions will still be made from meeting to meeting. Powell also hinted in particular that with the continued tightening of monetary policy, the pace of interest rate increase may eventually slow down, which made the market think that it is more dove like.

About the path of interest rate increase. First, the 75bp interest rate hike is radical enough. The first question for reporters is whether there is any discussion about the interest rate increase rate higher than 75bp. Powell pointed out that the 75bp interest rate increase this time is an appropriate range after considering the current data. If inflation becomes more disappointing, the interest rate increase will be more radical. Considering that the CPI hit a new high in June, it is enough for the Federal Reserve to choose to raise the interest rate by 75bp, which means that 75bp is the largest single interest rate increase in this cycle.

Second, there is no forward-looking guidance for subsequent interest rate hikes. The reporter's second question is about the path of subsequent interest rate hikes. First of all, Powell explained that the current level of neutral interest rates has reached, and the pace of interest rate increases is very fast. The economy and inflation have not yet fully reflected the effect of interest rate increases. The implication is that the current interest rate is not a restrictive level, and further interest rate increases are needed to reduce inflation this year. Secondly, Powell refused to give a clear interest rate guidance. He only said vaguely that September might be an unconventional large increase. This may reserve the possibility of 75bp, but the subsequent inflation rate may fall back. The Federal Reserve does not need to raise interest rates so aggressively, so it is more likely to raise interest rates by 50bp.

Third, there is no final conclusion on when to cut interest rates. Another reporter asked what conditions need to be met for future interest rate cuts. Powell pointed to employment, saying that at present, the number of new jobs has slowed down significantly. At present, the demand of the labor market is cooling, but the supply has not improved, and the labor participation rate has not further increased. The unemployment rate may rise in the future when the labor market recovers the balance between supply and demand. This means that the unemployment rate has risen significantly, or it is a necessary condition for the Federal Reserve to cut interest rates.

About reducing tables, reducing tables is on the right track. Powell said that the effect of the scale reduction was good, and the scale reduction plan was basically on track. According to the model, it will take 2-2.5 years for the Federal Reserve's assets and liabilities to reach equilibrium.

As for the economy, there is no economic recession at present. Journalists are also generally concerned about how the Federal Reserve views the risk of economic recession. First of all, Powell declared that there is no recession, and recession means that more industries have been shrinking for several months. The work of the Federal Reserve is not to define recession, but to choose the right tools according to economic data to achieve the goal of price stability and employment stability. Secondly, Powell predicted that the demand for housing and investment in the GDP sub item in the second quarter would slow down. The current strong labor market may call into question the negative growth of GDP data.

Regarding policy, the Federal Reserve is still committed to a soft landing. Powell stressed that price stability is the cornerstone of economic growth. He will avoid recession in the process of raising interest rates and try not to make mistakes. At present, the space for interest rate increase has been narrowed, and may be further narrowed. The goal of the Federal Reserve is still a soft landing. The way to achieve a soft landing is to reduce labor market demand, but it will not lead to a sharp rise in the unemployment rate. It is necessary to slow down economic growth and wait for the gap between supply and demand to close, which will be lower than the potential economic growth for a period of time. This process may include a period of low growth and weak labor market. Below trend growth may be a necessary condition for reducing inflation.

4、 After the hawkish peak of the Federal Reserve, it may face a slowdown in the pace of interest rate increase, the realization of recession expectations, and the switching of asset price style

Before this meeting, the market was concerned about whether the Federal Reserve's judgment on the inflation trend and the risk of economic recession in the second half of the year would adjust the range and pace of subsequent interest rate increases, thus affecting whether the price trend of major categories of assets would switch.

After this meeting, the path of the Federal Reserve to increase interest rates gradually became clear, which was reflected in "two peaks". First, the peak rate of hawkish tightening in this round of interest rate increase cycle was probably in July. It is expected that the amplitude and rhythm of the subsequent interest rate increase will slow down, along the path of 50bp in September, 25bp in November and 25bp in December. Second, the peak of this interest rate increase cycle may appear in December. It is expected that the interest rate increase will be basically completed by the end of this year. Next year, the Federal Reserve will adjust its monetary policy stance according to the degree of economic recession. If the degree of economic recession next year exceeds expectations, the Federal Reserve may start to cut interest rates.

1. Slowing inflation margin and weak economic indicators point to the peak of hawks

After the 75bp interest rate increase in July, the most hawkish period of the Federal Reserve will pass. In view of the slowing inflation margin and signs of weak economic growth, the Federal Reserve is expected to be more cautious when raising interest rates in September, and the rate of interest rate increase will probably slow to 50bp.

On the one hand, the period of maximum inflation pressure has passed. Recently, the international food price and energy price have both experienced a correction. In terms of food, there are also hopes of easing international food trade, agriculture products Prices generally fell. On July 22, representatives of Turkey, Russia, Ukraine and the United Nations reached an agreement on the export of agricultural products from Black Sea ports, which eased the bottleneck of grain export in Ukraine. In terms of energy, the recession expectation has depressed the international crude oil demand, but the supply has not yet appeared a new bottleneck. Since June, the international crude oil futures prices have fallen sharply. Affected by this, on July 25, the domestic retail gasoline and diesel prices in the United States fell by 13% and 9% respectively from a relatively high level. It is expected that the US energy CPI inflation in July will marginally ease. In the second half of the year, with the base moving up, the US CPI will slow down year on year, and the period of maximum inflation pressure has passed, which has left room for the Federal Reserve to adjust the pace of interest rate increase.

On the other hand, because the leading indicators of the economy have shown signs of recession, the risk of recession is approaching the peak of the corresponding interest rate increase cycle.

First, PMI indicators have weakened significantly. In June, the US ISM manufacturing PMI fell below the historical hub, while the new order index fell below the boom and bust line for the first time since the outbreak in 2020. In July, Markit US service industry PMI fell below the boom and bust line for the first time since the outbreak in 2020.

Second, the spread between 10-year and three-month maturities of US debt is about to be inverted. The upside down of bond term spread has always been an effective leading indicator to predict economic recession. According to the research of the San Francisco Federal Reserve, compared with other term spread indicators, the 10y-3m spread has a stronger ability to predict economic recession. Since the 75bp interest rate increase in June, the short-term interest rate has continued to rise, and the 10y-3m term interest margin of US bonds has narrowed rapidly from 1.6% to less than 0.3%. The Federal Reserve may press the "pause button" to raise interest rates when the 10y-3m interest rate spread of US Treasuries is about to hang upside down.

Third, the cost of physical financing rose and credit spreads widened. Real enterprise financing not only needs to bear the rising risk-free interest rate, but also faces a widening credit spread. Since the first interest rate increase in March this year, the credit spreads of US investment grade (BBB) corporate bonds and high-yield bonds have expanded by 29bp and 113bp respectively. With the rapid increase of interest rates by the Federal Reserve, the credit spreads expand rapidly, and the financing conditions of enterprises deteriorate significantly, which will lead to the contraction of enterprise investment.

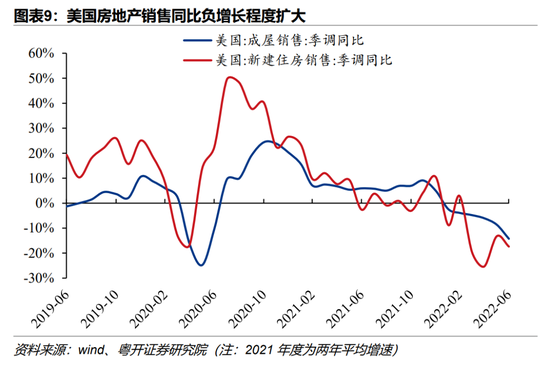

Fourth, the sales of interest rate sensitive properties declined significantly. After the Federal Reserve raised interest rates, interest rates soared, mortgage demand fell sharply, and sales of second-hand and new houses fell. In June, the sales data of second-hand houses in the United States hit a low point since June 2020, while the sales of new houses also fell sharply by 8% month on month. According to the statistics of the American Association of Realtors, the number of existing housing contracts signed in the United States in June fell by 20% compared with the same period last year, and the average interest rate of 30-year mortgage contracts exceeded 6%.

2. When will the peak of interest rate increase cycle come?

With the Federal Reserve's unconditional interest rate increase and its full efforts to fight against inflation, recession has become a highly probable event, and the hope of achieving a soft landing is slim. First, the interest rate increase was so large that the leading economic indicators weakened significantly. Second, the fast pace of interest rate increases led to the rapid tightening of financial conditions and the rapid decline of prosperity of interest rate sensitive sectors, which exposed the recession risk intensively. The US economic recession may be unavoidable. As the Federal Reserve raises interest rates to a neutral rate, it may have four side effects: weak real estate sales, rebound of unemployment rate, poor investment in manufacturing industry, and low consumption of residents. In particular, the suppression of interest rate increases on the investment side may appear faster.

The market is expected to reach the peak of the current interest rate increase cycle in December this year, and the interest rate reduction cycle may start in the first half of next year. In the first quarter of this year, the GDP of the United States experienced a technical recession due to the drag of inventory and net exports. However, consumer consumption and private investment still had momentum, and the substantive recession has not yet occurred. As the risk of future recession approaches, the Federal Reserve may cut interest rates in 2023. According to the IMF New World According to the economic outlook report, the year-on-year forecast of the real GDP of the United States in 2023 has been lowered to 1.0%, which is even lower than the growth rate of the euro zone in the energy crisis. The expectation of the federal funds rate futures market shows that the expected policy interest rate of the Federal Reserve in the first half of 2023 has generally fallen since more than a month ago.

3. How will asset prices be affected?

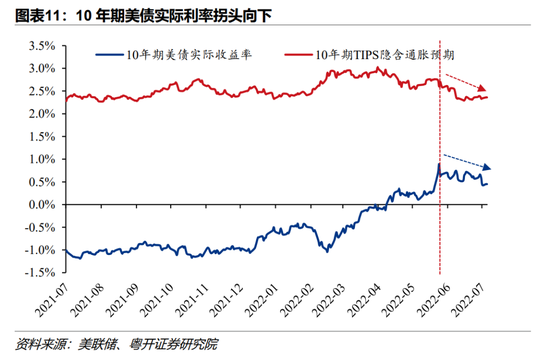

For the US bond interest rate, the 10-year interest rate center is down. Recently, the long-term and short-term interest rates of US Treasuries have become more upside down, mainly due to the obvious decline in long-term interest rates. However, after splitting down, the fall of long-term interest rates is mainly driven by the downward trend of real interest rates, and inflation expectations are still strong. Next, the recession expectation gradually materializes, and the real interest rate may still have room for correction, which makes the long-term interest rate may still have downward space.

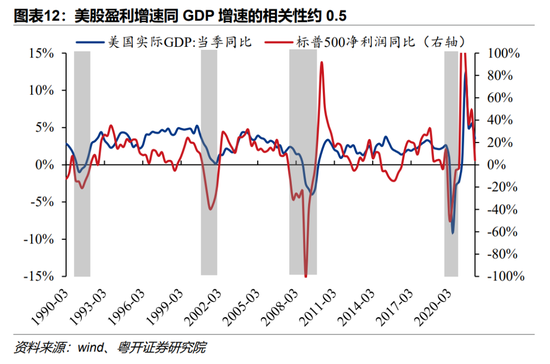

For US stocks, there is much room for growth stocks to rebound. From the perspective of the change of tightening rhythm, as the tightening rhythm of the Federal Reserve slows down, the US stock market may usher in a wave of valuation repair market, and growth stocks with large adjustments in the previous period will have a rebound opportunity. From the perspective of earnings expectations, the current earnings of US stocks have been in a slowdown trend. If the economic recession occurs at the end of this year and the beginning of next year, the earnings expectations will further decline, which will limit the height of the rebound of US stocks.

For the dollar index, it still remains high and volatile, and there may still be room for the central sector to rise. The factor supporting the strong US dollar in the second half of the year is the difference between economic growth and financial risks in the US and Europe. The European Central Bank has been significantly constrained by the increased stagflation of the energy crisis and the high debt restricting the monetary space. Although the new policy tool TPI (transmission protection tool) was announced in July, the debt in the euro area is high, economic growth is weak, and the idea of division prevails. After the European Central Bank raised interest rates by 50bp, the debt repayment pressure of Italy and other marginal countries in southern Europe has led to an increase in the risk of the European debt crisis, which will continue to suppress the euro, thus supporting the dollar to maintain a high level of operation.

(The author of this article introduces: Vice President of Yuekai Securities Research Institute, Chief Macro Researcher, Certified Public Accountant, Doctor of Finance of China Academy of Financial Sciences, and the third best macroeconomic analyst of New Fortune (team). Research direction: macroeconomic, fiscal theory and policy.)