Article/Lu Ping, columnist of Sina Financial Opinion Leader

Will the supply side reform under "carbon peak and carbon neutrality" boost economic growth? It can be seen from the cases of the United States and Japan, two developed countries, that in the face of internal and external problems, the supply side reform has successfully achieved national economic transformation and take-off again.

Summary:

In September 2020, China proposed to "strive to reach the peak of carbon dioxide emissions by 2030, and strive to achieve the goal of carbon neutrality by 2060. Will the supply side reform under" carbon peak and carbon neutrality "boost economic growth? It can be seen from the cases of the United States and Japan, two developed countries, that in the face of internal and external problems, the supply side reform has successfully achieved national economic transformation and take-off again.

The United States: supply side reform effectively controls inflation and achieves economic recovery. In November 1981, the year-on-year growth rate of CPI was 4.64%, far lower than the growth rate of 11.46% in April 1981. Since November 1981, the year-on-year growth rate of CPI has remained in single digits, falling back to 2.6% by August 1983. From the end of 1982, the US economy began to recover, and GDP continued to grow. In 1984, the GDP growth rate in Q1 reached 8.58%; The unemployment rate also began to decline at the end of 1982 and remained at a low level until the end of 1989.

Japan: In the 1970s, the oil crisis led to the phenomenon of high prices, rising unemployment, and business closure in Japan. Japan implements reform from the supply side: reduce costs, encourage innovation, reduce business volume, and vigorously ease overcapacity. The volume reduction operation has significantly enhanced the international competitiveness of Japan's manufacturing industry. From the second half of the 1970s to the 1980s, electronics, automobile and other industries replaced the original steel, petrochemical and other industries and became the leading industries leading Japan's economic growth. Japan's industrial structure has gradually shifted from the original labor-intensive and resource intensive to knowledge and technology intensive. Before the 1973 oil crisis: refused to slow down, stimulated to increase leverage, and the stock market fell deeply after the bubble; After the 1973 oil crisis, the supply side reform was implemented, supplemented by a neutral and tight monetary policy. The risk-free interest rate dropped significantly, and the stock market was bullish after the successful speed change.

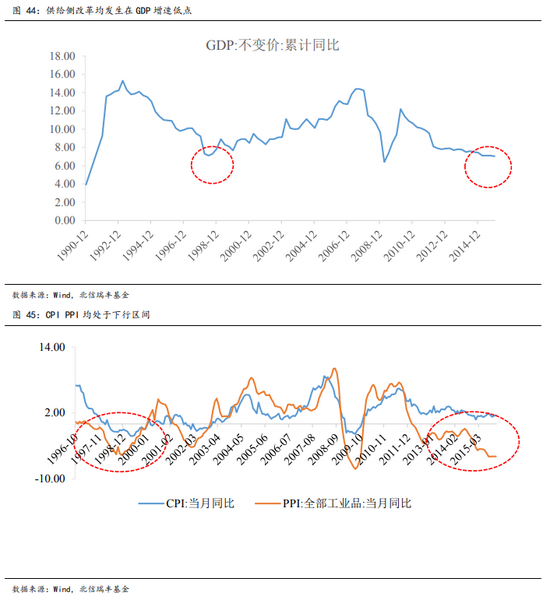

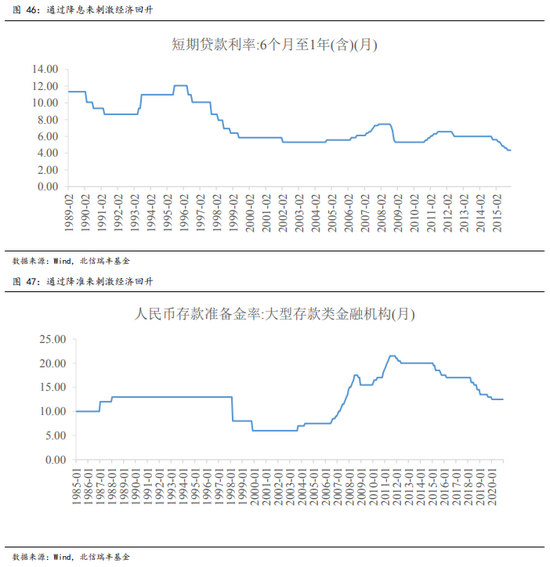

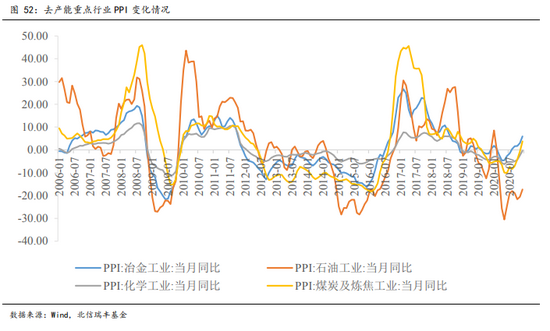

China: Two previous supply side reforms - the supply side reforms around 1998 and 2015. In terms of timing, 1998 and 2015 corresponded to a downward period of GDP growth, with a growth rate of 7.66% in the fourth quarter of 1999 and 7.04% in the fourth quarter of 2015. CPI and PPI both showed a downward trend, with prices falling and industrial deflation, and PPI performance was relatively low in both periods. In addition, the capacity utilization rate of some industries is low, the overcapacity is serious, and the profits of enterprises are down. In 1998, the textile industry was the main industry, and in 2015, the traditional industries such as coal and steel were the main industries. In terms of monetary policy, the central bank stimulated the economic recovery by cutting interest rates and reserve requirements in both periods.

What are the similarities and differences between China's carbon neutrality and the previous supply side reform? Different from the supply side reform that only focuses on the economic field, carbon neutrality is an important measure to cope with climate change and achieve sustainable human development. It is intended to profoundly change the economic and industrial development and energy structure, and is a self revolution of production and lifestyle. It not only means the restriction of carbon emissions, but also means the restriction of the total consumption of fossil energy. By 2050, China will realize that non fossil energy accounts for more than half of the total energy consumption and build a civilized energy consumption society. Compared with most developed countries, it takes about 50 years to reach the peak of carbon to reach the middle of carbon harmony, while China has only 30 years, which is more time intensive and heavy task. We believe that the carbon emission reduction route of the whole industrial chain to achieve carbon neutrality in 2060 can be summarized into three dimensions: energy sector, terminal sector and environmental protection sector. Energy sector: should undertake the historical mission of clean energy and promote the transformation and adjustment of energy structure. Terminal sector: industrial structure upgrading should be carried out from two aspects of "energy conservation" and "emission reduction". In the short term, the supply side reform will be carried out mainly by limiting production to reduce production from the source. In the medium and long term, it is still necessary to save energy and improve efficiency through new process exploration, the use of clean energy such as electrification, and the establishment of a green circular economy, so as to reduce energy or resource consumption per unit output. Environmental protection department: through the establishment of a sound carbon emission monitoring and trading system, the energy sector and the "high carbon" industrial sector can effectively ensure emission reduction, while accelerating the construction of a green and low-carbon circular economy, and realizing the recycling of downstream resources, including the secondary use of scrap steel, plastics, scrap non-ferrous metals and other raw materials.

1、 Can supply side reform boost the economy? - Take the US and Japan supply side reform as an example

In September 2020, China proposed to "strive to reach the peak of carbon dioxide emissions by 2030, and strive to achieve the goal of carbon neutrality by 2060. Will the supply side reform under" carbon peak and carbon neutrality "boost economic growth? It can be seen from the cases of the United States and Japan, two developed countries, that in the face of internal and external problems, the supply side reform has successfully achieved national economic transformation and take-off again.

1. The supply side reform of the United States realizes the re emergence of the economy

1) The background of US supply side reform is stagflation

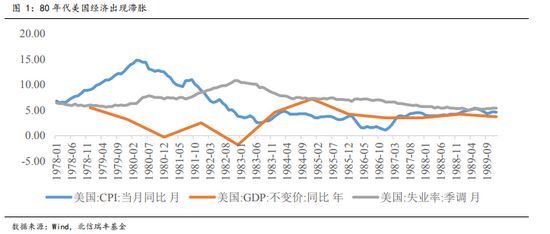

The supply side reform of the United States is to deal with "stagflation". After World War II, the US government continued to increase social welfare spending and strengthen economic regulation to curb various market failures such as monopoly and negative externalities. As a result, the government relied excessively on stimulus policies and the economy stagnated. On the one hand, inflation continued to rise, with CPI rising from 6.4% in February 1978 to 14.4% in June 1980; On the other hand, the U.S. economic growth rate continued to decline. In 1980, the U.S. GDP was only - 0.2% year on year, and the unemployment rate was as high as 7.18%, even 10.8% in 1982, deeply trapped in the "stagflation" quagmire.

Secondly, there are structural problems in the US economy: in the context of the rise of Japan and Western Europe, the competitiveness of domestic goods in the US has declined and there has been a relative overcapacity; The high income tax of individuals and enterprises has inhibited private sector investment and production; The government has excessive interference in the regulation of economy and price, and the efficiency of enterprise operation is low.

2) Reagan Economics: Tax Reduction, Deregulation and Monetary Tightness

From 1981 to 1989, the Reagan government carried out reforms based on the above issues, including tax cuts, reduction of social welfare, deregulation of some industries, and promotion of market-oriented reform of interest rates. Among them, tax cuts, deregulation and tight money are the essence of Reagan economics.

First, reduce taxes. The proportion of individual income tax in GDP decreased from 9.1% in 1981 to 7.6% in 1984; Reduce the tax burden on enterprises. From 1981 to 1990, the proportion of enterprise income tax in GDP remained below 2%.

Second, deregulation. The Reagan administration relaxed regulation mainly in the following aspects: relax the implementation of the antitrust law, encourage enterprises to compete reasonably; Deregulation of oil and gasoline prices; Deregulation of the automobile industry; Reduce intervention in labor market prices; Remove institutional barriers through legislation to support the development of small and medium-sized enterprises; Encourage enterprise innovation and successfully promote the transformation of industrial structure. Through the above measures, prices have been significantly reduced, social welfare has been improved, and economic vitality has been effectively enhanced.

Third, reduce inflation and adopt tight monetary policy. Reduce the growth rate of money supply and increase the discount rate, so as to keep the interest rate at a high level and reduce the inflation rate. In November 1981, the year-on-year growth rate of CPI was 4.64%, far lower than the growth rate of 11.46% in April 1981. Since November 1981, the year-on-year growth rate of CPI has remained in single digits, falling back to 2.6% by August 1983.

3) Supply side reform effectively controls inflation and realizes economic recovery

Maintain low inflation rate with high interest rate and effectively control inflation

The Reagan Administration adopted the idea of the monetarist school to reduce the growth rate of money supply and increase the discount rate, so as to keep the interest rate at a high level and thus reduce the inflation rate. Since 1980, the real interest rate in the United States has basically remained at a high level of 6% - 8%. The high interest rate has played a certain role in curbing inflation. The CPI has decreased from 13.5% in 1980 to 6.2% in 1982, and has remained below 5% since then; PPI also dropped from 14.1% in 1980 to 2% in 1982, and then basically remained below 6%.

Realize economic recovery and growth in the late period of reform

The economy is still in recession in the early stage. The government increased savings, investment and production by cutting tax rates, but higher interest rates inhibited investment and offset the incentive effect of tax cuts on investment. Therefore, in the early stage of reform, the United States was still in crisis and recession. From 1981 to 1982, the US industrial production index continued to decline from August 1981 until 1982Q4; The unemployment rate also rose from 6.3% in January 1980 to 10.8%; GDP dropped sharply from 1981Q3 to the bottom of -2.56% in 1982Q3.

Later economic recovery and growth. Since the end of 1982, the US economy has begun to recover and its GDP has continued to grow. In Q1 of 1984, the GDP growth rate reached 8.58%; The unemployment rate also began to decline at the end of 1982 and remained at a low level until the end of 1989; The industrial production index began to rise steadily in February 1983 and reached 68.3 in December 1989, an increase of 29.8% over the beginning of 1983.

2. Japan's reform in the growth shift period in the 1970s to achieve stable economic growth

1) Reform background: Japan's economy has entered into a period of gear shifting and deceleration from high-speed growth

Since the 1970s, Japan's economy has entered a stable growth stage from a period of rapid growth.

Japan's economy caught up at a high speed from 1951 to 1973, with an average economic growth rate of about 10%. After the shift of growth rate, the economic growth rate from 1974 to 1991 was about 5%, belonging to the stage of medium growth. The reasons why Japan is faced with the shift of economic growth and power upgrading are as follows: First, the long cycle of Japanese real estate appeared around 1969; Second, the Japanese Lewis inflection point appeared in the late 1960s. With the sharp reduction of rural transferable surplus labor force and the widespread popularity of durable consumer goods, the basic conditions supporting rapid economic growth have changed.

With the "stagflation" caused by the oil crisis and the increasingly serious environmental pollution, Japan's economy has to embark on the road of transformation

In the 1970s, the oil crisis led to high prices, rising unemployment, business failures and other phenomena in Japan. In 1974, Japan's economy experienced the first post-war negative growth. With the arrival of Lewis turning point and the dual impact of the Japanese government's "national income doubling plan" at the same time, labor costs rose rapidly, and enterprises were overwhelmed; Japan's high-speed growth period is realized by a large amount of energy input and extensive management. Rapid industrialization has caused energy consumption and increasingly serious environmental pollution. National discontent is rising, and Japan's growth model of high energy consumption and high pollution is unpopular.

2) Implement reform from the supply side: reduce costs and encourage innovation

"Reduce the volume of operation" to reduce energy consumption, interest and labor costs

Save energy consumption. Under the impact of the oil crisis, the competitiveness of Japan's high energy consumption industries has been greatly reduced. The Japanese government, through administrative guidance and various restrictive measures, has guided enterprises with poor efficiency to shut down and switch, significantly reducing the production capacity of these industries.

Reduce interest burden. After the outbreak of the oil crisis, Japanese enterprises' own capital ratio was not high and the interest burden was heavy. Through the implementation of "volume reduction operation", the self owned capital ratio of Japanese enterprises has increased significantly. In addition, the interest burden of enterprises has been effectively reduced due to the continuous reduction of Japanese interest rates over the same period.

Reduce labor costs. After the arrival of the Lewis turning point, the labor cost rose significantly. The enterprise adjusted the number of employees by firing temporary workers, controlling the employment of regular employees, and no longer adding new people after female employees left, so as to reduce labor costs.

The government guides the upgrading of industrial structure, vigorously relieves overcapacity and supports the development of emerging industries.

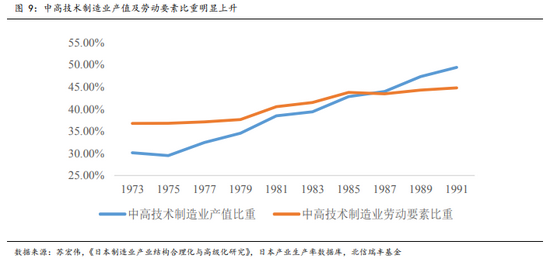

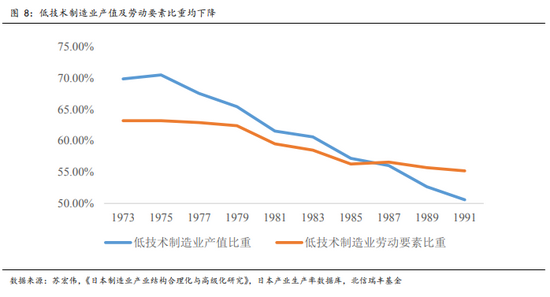

We will vigorously ease overcapacity. The outbreak of the oil crisis has severely impacted Japan's economy, which is heavily dependent on energy, especially the high-tech manufacturing industry with high energy consumption, declining industries and increased overcapacity. In 1978, the Japanese government enacted laws to actively adjust and relieve declining industries and overcapacity. In 1976-1991, the proportion of output value of low tech manufacturing industry decreased by 1% - 3% annually. By 1991, the proportion of output value of low tech manufacturing industry in Japan was 50.59%, 19.27% lower than that in 1973. During the same period, with the major adjustment of industrial structure, the proportion of labor factors in low tech manufacturing industry decreased by 8.02%.

Support the development of emerging industries. The Japanese government encourages and fosters the development of new knowledge and technology intensive industries, provides subsidies for the development of cutting-edge technologies, and implements preferential policies in tax and finance. The proportion of output value of medium and high-tech manufacturing industry increased by 1% - 3% in 1976-1991. In 1991, the proportion of output value of medium and high-tech manufacturing industry in Japan was 49.41%, an increase of 19.17% compared with 1973, and the proportion of labor factors increased by 8.02%.

3) Reform achievements: industrial upgrading was smoothly achieved, and the economy and stock market took off

Japan has grown into a manufacturing power, and its industrial structure has been successfully optimized and upgraded

"Volume reduction" has significantly enhanced the international competitiveness of Japan's manufacturing industry. By the early 1980s, Japan had become the country with the highest energy efficiency among major economies. From the second half of the 1970s to the 1980s, electronics, automobile and other industries replaced the original steel, petrochemical and other industries and became the leading industries leading Japan's economic growth. Japan's industrial structure has gradually shifted from the original labor-intensive and resource intensive to knowledge and technology intensive.

"Stable growth" of economy

Through this reform, Japan successfully completed the shift from high speed to stable growth. The average growth rate of Japan's economy remained at about 4% from 1975 to 1985. During this period, Japan's economic growth in major developed countries was still relatively fast.

1974-1981 The stock market went out of the bull market after the successful speed change

Before the 1973 oil crisis, Japan refused to slow down, stimulated leverage, and the risk-free interest rate reached more than 10%. The stock market fell deeply after the bubble; After the 1973 oil crisis, the supply side reform was implemented, supplemented by a neutral and tight monetary policy. The risk-free interest rate dropped significantly, and the stock market was bullish after the successful speed change.

2、 What industries did the last round of domestic supply side reform focus on? How to change it?

The two "four trillion" economic stimulus plans launched by China after the 2008 financial crisis were mainly invested in infrastructure fields such as "railway, highway and infrastructure", which led to the rapid expansion of industries such as steel, cement, coal and flat glass. When China's economy recovered from the crisis and the macroeconomic stimulus policy gradually withdrew, the problem of overcapacity in these industries gradually emerged, product prices were depressed, and the industry suffered extensive losses. In 2015, the central government put forward the 15 word policy of "capacity reduction, inventory reduction, leverage reduction, cost reduction and weakness remedy" (referred to as "three reductions, one reduction and one supplement"). It aims to eliminate the backward production capacity of cement, flat glass and other industries, and focus on reducing the excess capacity of steel, coal and other industries. The policy goal of improving the industry's prosperity degree was achieved by expanding effective supply through strategies such as closing, stopping and turning around, with remarkable results.

1. Before reform, overcapacity industries were in deep trouble

"Supply side" means that the main contradiction of economic operation is on the supply side. The Ministry of Industry and Information Technology announced that the list of backward and overcapacity enterprises eliminated in the industrial industry was mainly concentrated in steel, cement, electrolytic aluminum and other industries. The "overcapacity" of these industries is reflected in the low capacity utilization rate and poor profitability of the industry. The loss of member enterprises of China Steel Association reached 50.5% in 2015; The total profits of 90 large coal enterprises (69.4% of the national output) in the first 11 months of 2015, according to the statistics of China Coal Association, fell 90.7% year on year. Therefore, the steel and coal industries have become the first industries to be given "quantitative indicators" for capacity reduction. In February 2016, the State Council issued the Opinions on Solving Excess Capacity in the Iron and Steel Industry and Realizing Difficult Development, and the Opinions on Solving Excess Capacity in the Coal Industry and Realizing Difficult Development. The two documents proposed that it would take five years to reduce crude steel production capacity by 100 million tons to 150 million tons; It will take 3-5 years to withdraw about 500 million tons of coal capacity and reduce and restructure about 500 million tons of coal capacity.

2. Optimize the supply structure and promote the benign development of the industry

The essence of "supply side reform" is to reduce inefficient supply, improve output efficiency, promote product price recovery and maintain the benign development of the industry under the condition of insufficient demand. From the results, the "supply side" reform has achieved the expected goals. After the "supply side" reform, the number of enterprises in industries with overcapacity such as iron and steel dropped significantly, the growth rate of fixed asset investment rose steadily, product prices also gradually rebounded, the overall profitability of the industry gradually increased, and the asset liability ratio continued to decline.

1) Eliminate backward production capacity and improve industry concentration

From the change of production capacity before and after the "supply side" reform, the production capacity of cement, crude steel and steel has decreased continuously since 2016, of which crude steel has the largest decline, reaching 9% in 2018; However, the production capacity of flat glass and electrolytic aluminum did not decline, but the growth slowed down.

The elimination of inefficient production capacity has made the capacity utilization rate of the whole industry rise steadily. From the second quarter of 2016 to the fourth quarter of 2019, the capacity utilization rate of coal mining and washing industry, ferrous metal and rolling industry increased by 13% (from 58.4% to 71.5%) and 7% (from 72.3% to 79.5%) respectively.

According to the data of the Ministry of Industry and Information Technology of the People's Republic of China, by the end of 2018, the ceiling index of 140 million to 150 million tons of steel capacity has been completed, so the capacity of the steel and cement industries began to expand. The corresponding fixed asset investment has accelerated significantly since 2019.

Under the policy of "close, close and turn", small enterprises continue to withdraw from the market. Adjust and optimize the supply structure to reduce ineffective supply. The number of enterprises in the ferrous metal smelting and rolling industry and the ferrous metal mining industry decreased sharply from 10071 and 3128 at the end of 2015 to 5138 and 1528 at the end of 2018, respectively, with a decrease of nearly 50%. The industrial concentration of some industries has significantly improved. For example, the market concentration of the top ten cement enterprises has increased from 40% in 2010 to 57% in 2016.

2) The situation of oversupply has been significantly improved

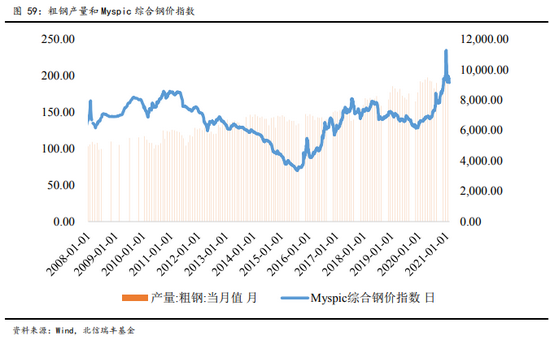

According to the data of the Ministry of Industry and Information Technology of the People's Republic of China, by the end of 2018, the ceiling index of 140 million to 150 million tons of steel capacity reduction set in the "13th Five Year Plan" has been completed ahead of schedule. Subsequently, the steel industry began to pick up production capacity in 2018. The "supply side" reform has significantly improved the situation of oversupply in the steel industry. The part of steel output exceeding the demand reached 0.99 trillion tons in 2015, and dropped to only 0.33 trillion tons by 2020.

3) The profitability of the industry has been significantly enhanced

After the supply side reform, the sales profit margin of ferrous metal smelting and rolling processing industry increased significantly. Since 2016, the industry's sales profit margin has gradually increased from the low point (0.29%) in February 2016 to more than 6% in 2018, close to the historical highest level in 2004; The asset liability ratio also decreased from 68% to 60.5% in 2020.

3. The recovery of "demand side" is also the key to the improvement of industry prosperity

The demand side is also the key to the success of the above-mentioned "supply side" reform. Going out of the "downturn" area on the demand side is the basis for improving the existing efficient production capacity. After 2015, the investment growth rate of the real estate industry gradually recovered, and the year-on-year growth rate of the completed investment in real estate development rebounded to more than 7%. The recovery of downstream demand has played a supporting role in improving the prosperity of steel, cement and other industries.

The newly started housing area has recovered from 2015, and the difference between the newly started housing area and the completed housing area has gradually expanded, indicating that the demand for steel, cement, glass and other commodities caused by building demand has a more solid foundation.

The "coal flying and dancing" since 2021 is mainly due to the mismatch between global supply and demand, and the gradual repair of global demand. However, the production capacity of some resource countries with severe epidemics has not fully recovered. The bottleneck problem of upstream raw material supply is prominent, and the impact of carbon neutrality and production restriction is superimposed. The overall change in the supply and demand structure has pushed up the price of bulk commodities, which is not exactly the same as the capacity cut in 2015-16.

The global industrial demand is expected to peak within two months. At the same time, with the improvement of the epidemic situation, the production capacity of resource countries will be gradually restored. At that time, the prices of black, nonferrous and other bulk commodities will fall, while crude oil will be relatively late. While domestic demand has weakened, there is pressure on prices of steel, coal and other products to rise.

3、 When will the supply side reform be carried out? Will it cause high inflation?

1. Supply side reform in the United States

Time point selection of US supply side reform

The two oil crises in the 1970s drove the oil price to continue to soar. In 1974 (the first oil crisis), the price of crude oil exceeded US $10/barrel for the first time; In 1979-1980 (the second oil crisis), the price of crude oil reached as high as 39 dollars/barrel, and the soaring price of oil led to the surge of coal production capacity in the United States.

The capacity utilization rate of the durable goods manufacturing industry in the United States has declined significantly. In the face of foreign competition, the competitiveness of domestic goods has declined, and overcapacity has emerged. In addition, since the 1970s, the growth rate of the population of working age in the United States has declined, from 1.9% in 1971 to 0.7% in 1980.

The inflation rate in the United States began to rise gradually from the middle and late 1960s, and has evolved into stagflation in the 1970s. In June 1980, the core CPI was as high as 13.5%, and in November 1982, the unemployment rate was as high as 10.8%. During this period, the government initiated supply side reform.

The US supply side reform did not cause inflation

The capacity reduction of traditional industries in the United States has triggered short-term structural inflation, but it has not triggered overall high inflation. The prices of coal and other mining products have risen sharply due to the contraction of output, but the duration is not long. CPI dropped from 13.5% in 1980 to 6.2% in 1982. PPI dropped from 14.1% in 1980 to 2% in 1982.

Deregulation measures and encouragement of competition have made relevant industries achieve "cost reduction and efficiency increase", which is also one of the factors that weaken high inflation. According to the estimate in President Reagan's Economic Legacy: Great Expansion by the Senate in 2000, after the deregulation measures were implemented in some industries in the 1980s, the prices of these industries showed a straight downward trend in 10 years, saving consumers billions of dollars every year.

From the demand side, the baby boom in 46-64 pushed the global demand surge in the 1970s to marginal improvement; The decline in the proportion of middle class income in the United States and the decline in consumption capacity also eased the contradiction between supply and demand to a large extent. In addition, in the early 1980s, the government maintained low inflation with high interest rates and raised the discount rate. Tight monetary policy played a significant role in curbing inflation.

2. Supply side reform in Japan

Japan carried out two rounds of supply side structural reform in the 1970s and after entering the 21st century.

Supply side reform in the 1970s

In the 1970s, the Japanese economy was faced with a shift in growth. From high economic growth to medium growth in 1974-1991.

Under the impact of the oil crisis, "stagflation" occurred. The first oil crisis had a huge impact on Japan, whose dependence on oil imports was as high as 98%. The year-on-year growth rate of CPI rose from 3.9% in September 1972 to 24.9% in February of the next year. In order to control inflation, the sharp tightening of fiscal and monetary policies led to negative economic growth in 1974.

In addition, Japan's labor costs are rising rapidly. The labor force has shifted from surplus to shortage, and the labor cost has risen rapidly. Against this background, with the oil crisis as the turning point, Japan started the supply side reform of capacity reduction and industrial adjustment.

The supply side reform in the 1970s did not cause inflation

The appreciation of the yen curbed the risk of inflation. In the process of capacity reduction in Japan from 1975 to 1985, although the prices of minerals, steel, oil and coal products continued to rise, the prices of various commodities declined significantly after 1985. From the perspective of time nodes, the signing of the Plaza Agreement in 1985 made the yen appreciate significantly, thereby curbing imported inflation and reducing the risk of price escalation under the supply side reform.

The supply side reform may be conducive to restraining inflation in the long run. In the 1980s, Japan's total factor productivity continued to rise. In the late reform period, the upstream industry achieved "cost reduction" and the downstream industry achieved "efficiency increase". The long-term force of technological innovation may offset part of the earlier increase in prices in the following decade.

From the demand side, global demand slowed down, and there was no risk of imported inflation in Japan in the 1980s. The baby boom in 46-64 pushed the global demand surge in the 1970s to marginal improvement, and the natural population growth rate has declined year by year since 1974. In addition, Japan completed the industrial upgrading in the 1970s, the economic growth slowed down, domestic demand slowed down, and there was no endogenous inflation risk.

Supply side reform at the beginning of the 21st century

From the late 1980s to the early 1990s, Japan's economy continued to boom, but a large number of funds poured into the stock market and the real estate market, resulting in bubbles. In 1991, the "bubble economy" burst, and the economic growth rate dropped to about 1% per year, which was in a long-term depression.

During the "bubble economy" period, Japan's high non-performing debt triggered a financial crisis. Some banks have been unable to reach the required capital adequacy ratio. The bankruptcy of financial institutions has caused great shock to the financial market. In addition, Japan's aging population has become increasingly severe, which has brought a series of adverse effects, such as insufficient labor supply, weak growth of consumption demand, etc. Against this background, Japan implemented "structural reform" in April 2001.

At the beginning of the 21st century, the supply side reform did not significantly increase Japan's economy and did not cause inflation

Japan's "structural reform" has achieved some results, but the results are limited because its market-oriented reform still needs to be deepened, and the reform of the aging population has not made enough progress. The Japanese economy grew slowly, and the stock market stopped falling and rebounded. From February 2002 to February 2008, the Japanese economy realized a 73 month boom recovery. The actual growth rate of this boom is not high, with an average growth rate of less than 2%, but it has improved compared with the average growth rate of 1% in the 1990s.

3. Supply side reform in China

Time point of China's two supply side reforms

Compared with the supply side reform around 1998 and 2015, in terms of time point selection, 1998 and 2015 correspond to a downward period of GDP growth, with the growth rate of 7.66% in the fourth quarter of 1999 and 7.04% in the fourth quarter of 2015. CPI and PPI both showed a downward trend, with prices falling and industrial deflation, and PPI performance was more sluggish in both periods. In addition, the capacity utilization rate of some industries is low, the overcapacity is serious, and the profits of enterprises are down. In 1998, the textile industry was the main industry, and in 2015, the traditional industries such as coal and steel were the main industries. In terms of monetary policy, the central bank stimulated the economic recovery by cutting interest rates and reserve requirements in both periods.

The overall economic environment of the two supply side reforms mainly has the following three differences. First, deleveraging was relatively obvious in 1998-2000, but the asset liability ratio remained high during 2015-2016. The heavy asset industry was mainly state-owned enterprises, and social responsibility made deleveraging and capacity reduction more difficult; Second, the real estate price in 2015-2016 was much higher than that in 1998-2000; Third, the exchange rate was stable in 1998-1999, and was in the process of downward recovery in 2015-2016.

Supply side reform and inflation in 1998

In 1998, the capacity reduction was mainly concentrated in the textile industry, and its price rebound had little impact on the overall inflation. The price of the textile industry bottomed out after capacity reduction. In 1999, the price recovered for the first time. The total profit of the whole industry and the profit of a single enterprise reached the highest level since 1985. However, in 2001, the production capacity of the textile industry rebounded, and the newly increased cotton spindle production capacity in that year rose rapidly from 17000 spindles per year in 1998-2000 to 470000 spindles in 2001. The profits of the whole industry fell again, the supply and demand of products worsened, product inventories piled up again, and prices fell again.

The real success of capacity reduction in the textile industry and the real trend improvement in profitability were achieved in two typical demand driven periods. From 2002 to 2003, after China's accession to the WTO, foreign demand grew. At the same time, China ushered in a golden decade of real estate, and investment growth also continued to rise; From 2009 to 2010, the government launched a "four trillion" strong stimulus to deal with the financial crisis. Under the support of demand, upstream profits rose synchronously, and the textile industry prices reached the bottom in 2002 and entered the upward range.

Supply side reform and inflation in 2015-2016

The main idea of this round of supply side reform is "three reductions, one reduction and one compensation". "Capacity reduction" and "inventory reduction" are relatively successful, especially in the coal and steel industries. At the beginning of the reform, the price of raw materials soared and PPI rose significantly. The reform significantly reduced the production capacity of the upstream industry, coupled with the impact of the monetization policy of the shed reform, and the improvement of the supply and demand relationship promoted the rise of raw material prices. At present, with the ebb of the stimulus policy, production capacity has begun to rise. PPI has dropped significantly compared with the peak in 2016, but the hub is still significantly higher than before the reform. Especially for steel, coal and other industries.

The supply side reform triggered short-term structural inflation, but did not trigger overall high inflation. Before 2015, CPI and PPI basically maintained a highly positive correlation year on year; After 2015, the trend of year-on-year CPI and PPI has become a normal. China's supply side structural reform was formally proposed at the end of 2015, that is to say, the year-on-year differentiation trend of CPI and PPI reflects the transfer process of the focus of macro-control from demand to supply side.

China's inflation performance is caused by both domestic and foreign factors. After 2016, the global inflation rate rose steadily, and China's imported inflation pressure gradually increased; The supply side reform adjusts the upstream supply and demand, although to some extent, the inflation increases drive However, due to weak domestic consumption and investment demand, it is difficult to obtain necessary demand support for the rising inflation rate.

In addition, if there is no increase in demand, the transmission of upstream price increases to the downstream will not be so smooth. This round of supply side reform focuses on the upstream industry. In the context of no systematic improvement in demand, there is an obvious feature of "one consumption and another growth" between the profits of the upstream industry and the downstream industry, rather than the transmission to the downstream.

4、 What are the similarities and differences between carbon neutrality and the previous supply side reform?

1. Supply side reform triggered by this round of carbon neutrality: comparison with 2016

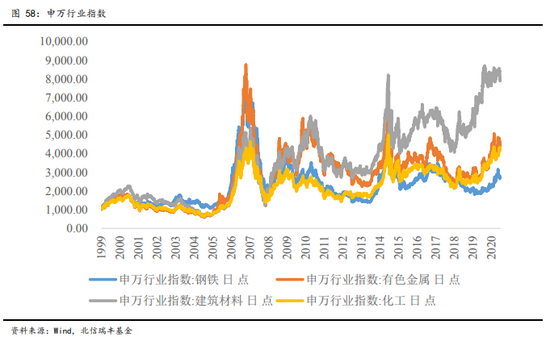

Recently, carbon neutral concept stocks have become the hot spot of market capital pursuit. Since February 2021 State Grid Yingda The carbon neutral index rose by about 15.72%, and the Shenwan Iron and Steel Index also rose by 23.22%. The carbon neutral plate rose against the trend by taking advantage of the policy dividend, pro cyclical, undervalued and other overlapping advantages, but it has declined recently. Some stocks of the carbon neutral concept have shown signs of breaking away from the fundamentals, and the trend differentiation of individual stocks within the plate has increased significantly.

Due to the need to achieve carbon peak in 2030 and carbon neutrality in 2060, it is necessary to strictly limit the new capacity of high energy consuming industries. At the beginning of 2021, the Ministry of Industry and Information Technology made a statement for many times, such as "resolutely compress the crude steel output to ensure that the crude steel output will decline year-on-year in 2021". Recently, some provinces have begun to control the capacity scale of high energy consuming industries. For example, Inner Mongolia has issued regulations since 2021, New capacity projects such as electrolytic aluminum and aluminum oxide will no longer be approved. If it is really necessary to build, capacity and energy consumption reduction and replacement must be implemented in the area. In addition, the differential electricity price policy will be implemented for eight industries of electrolytic aluminum, ferroalloy, calcium carbide, caustic soda, cement, steel, yellow phosphorus, and zinc smelting in strict accordance with national regulations. On March 19, Tangshan City issued a notice on the measures to limit production and reduce emissions of steel industry enterprises in Tangshan City, involving 23 steel enterprises in Tangshan. From March 20 to December 31, the measures to reduce emissions of 30-50% of the production limit will be implemented. According to the document, from March 20 to December 31, the total consumption of iron ore in Tangshan City may decrease by 51.59 million tons.

From the perspective of the impact on the traditional cycle industry, the normalization of production restriction and emission reduction triggered by carbon neutrality is very similar to the supply side reform in 2016, which is also a supply side contraction, thus triggering a fierce response from the upstream raw material product prices and the capital market. It is believed that after the valuation adjustment, the performance of policy implementation will be realized, and the promotion of carbon neutrality may lead to a new round of "supply side reform" in the upstream cycle industry. However, there are many differences between this round of carbon neutrality and the last round of supply side reform in terms of production restriction and emission reduction:

First, this round of production restriction is a short-term stage serving the long-term goal of "carbon neutrality", which will focus on structural adjustment. In 2016, the supply side reform was mainly a policy of total volume reduction, and the effect of structural optimization was not obvious. In 2015, the four trillion yuan stimulus plan was gradually ebbing, both domestic and foreign demand was weakening, and the scale of excess capacity induced by its stimulus reached the maximum level, the industry's deficit continued to expand, and PPI continued to grow negatively. In this context, the supply side reform launched has the nature of short-term emergency policy. Essentially, it is to start from the production side and the supply side to start domestic demand and boost the economy. Therefore, many one size fits all stimulus policies have been adopted simultaneously, such as reducing reserve ratio and interest rate, reducing down payment ratio, adjusting provident fund policy, and reducing taxes and fees. At present, China's economy is in a period of high stagflation, and foreign demand is very strong, which is the main force driving economic growth. The inventory of real estate is not high under the pressure of policies. Although the prosperity of steel and other industrial sectors is low, it is affected by the rise of iron ore, coke and other cost ends, as well as the rise of global monetary easing commodity prices, Industrial products such as steel prices may still face inflationary pressure. The current economic foundation is sound, with the conditions for structural adjustment, and there is no incentive to stimulate consumption by reducing supply.

Second, the scale of capacity reduction caused by this round of production restriction is small. Since carbon neutrality is a panoramic strategy for energy, industry, construction, transportation, environmental protection and other sectors, the efforts to limit the production of traditional cycle industries will also be decentralized and weakened. At present, there is no clear schedule for capacity reduction and production restriction. In recent years, most enterprises have carried out environmental protection transformation, and the scope of enterprises affected by carbon neutrality may be further reduced. According to the calculation of Lange Iron and Steel Network, if the production reduction range of Tangshan is referred to, the reduction range of crude steel in Hebei, Henan, Shandong and Shanxi provinces is estimated to be about 70 million tons. Calculated based on the national crude steel output of 1.065 billion tons in 2020, it is equivalent to a year-on-year decrease of 6.57%, which is much smaller than the elimination of 150 million tons of steel production capacity by the supply side reform in 2016-2018, and the ban of 140 million tons of ground bar steel. Therefore, in the long run, the price of black assets is unlikely to rise in 2016, and the short-term impact should not be overestimated.

Third, it has little effect on improving enterprise profits. In terms of demand, real estate has begun to weaken under the constraints of the three red lines last year. China's economy is also gradually getting rid of the development mode of infrastructure and urban investment. In the context of unstable demand, the amplification effect of supply contraction on prices will be weakened. The transmission chain of the last round of supply side reform to upstream enterprises' profits is relatively smooth. The main reason is that high inventory and low price → enterprise losses → capacity and inventory removal → price recovery → enterprise profits improvement. At present, the price of industrial products is at a high level, and there is little room for further increase. Enterprise profits are already in the process of improvement. The active pressure reduction of production power is small, and the administrative compulsory production restriction will take inflation risks into account. For example, recently, Tangshan City held a symposium on the plan of adjusting sintering machine shutdown and production restriction for iron and steel enterprises, The meeting adjusted the emission control requirements and share of Tangshan iron and steel production enterprises, appropriately relaxed the control of ironmaking links, and lowered the 30% - 50% production limit policy to 10% - 30%.

2. "Carbon neutrality" is a long-term and comprehensive economic and energy restructuring

1) Policy intention

Different from the supply side reform that only focuses on the economic field, carbon neutrality is an important measure to cope with climate change and achieve sustainable human development. It is intended to profoundly change the economic and industrial development and energy structure, and is a self revolution of production and lifestyle.

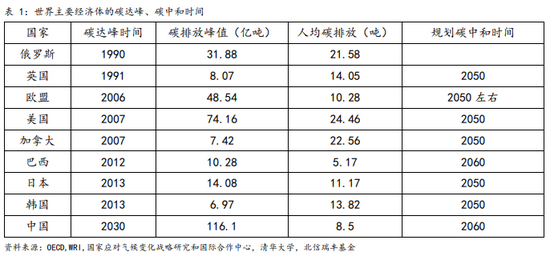

As early as 2005, China overtook the United States to become the world's largest carbon emitter. In contrast, the United States, Europe, Japan and South Korea started and transformed their industrialization earlier. Resource based countries such as Russia, Canada and Brazil have low industrial scale, so they took the lead in achieving carbon peak. While some developed countries that have achieved carbon peak have long been dissatisfied with China's growing industrial volume and carbon emissions. After taking office, Zhu Diwen publicly said that the United States would impose "carbon tariffs" on countries that do not have mandatory carbon dioxide emission reduction quotas, and implement trade protection in the name of environmental protection.

Carbon will reach its peak by 2030, and carbon will be neutral by 2060. It is estimated that China's total carbon emissions in 2030 will be 11.61 billion tons, which means not only the constraints on carbon emissions, but also the restrictions on the total consumption of fossil energy. The Strategic Plan for 2016-2030 of the Revolutionary Strategy for Energy Production and Consumption pointed out that China's total energy consumption should be controlled within 5 billion tons of standard coal by 2020; By 2030, the total energy consumption should be controlled within 6 billion tons of standard coal, and the total consumption of fossil energy should not exceed 4.5 billion tons of standard coal; By 2050, China will realize that non fossil energy accounts for more than half of the total energy consumption and build a civilized energy consumption society. Compared with most developed countries, it takes about 50 years to reach the peak of carbon to reach the middle of carbon harmony, while China has only 30 years, which is more time intensive and heavy task.

2) Action Path and Future Outlook

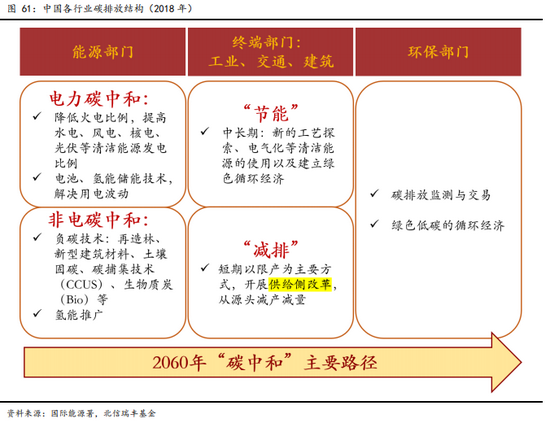

In terms of carbon emissions from energy activities used in the combustion of carbon containing energy, there are huge differences between different industries and production sectors in China. In 2018, the carbon emissions from energy activities in the power generation and heating industry accounted for 51% of the total, the carbon emissions from energy activities in the industrial sector accounted for 28%, the carbon emissions from energy activities in the transportation industry accounted for 10%, and the construction industry accounted for 4%. We believe that the carbon emission reduction route of the whole industrial chain to achieve carbon neutrality in 2060 can be summarized into three dimensions: energy sector, terminal sector and environmental protection sector:

Energy sector

We should undertake the historical mission of clean energy and promote the transformation and adjustment of energy structure.

On the one hand, carbon neutrality in electricity has been achieved. Since 2018, China's coastal provinces have begun to strictly control coal-fired power generation, but the current carbon emissions in the power sector still account for more than 30% of China's total carbon emissions. Therefore, on the supply side, it is necessary to reduce the proportion of thermal power, increase the proportion of hydropower, wind power, nuclear power, photovoltaic and other clean energy power generation, and cope with fluctuations in daytime and seasonal power demand through utility level energy storage batteries and hydrogen energy storage solutions.

On the other hand, realize carbon neutrality in the non electric field. For industries that need to burn energy, such as aviation, metal smelting, paper making, etc., non electric energy will still exist in the form of non electric energy. By 2050, China may still have 1 billion to 2 billion tons of carbon emissions, which need to be reduced through negative carbon technology, mainly including reforestation, ecological restoration, new building materials, soil carbon sequestration Carbon capture, utilization and storage (CCUS), direct air carbon capture and storage (DACCS), biomass energy carbon capture and storage (BECCS), biomass carbon (Bio), etc. can also be promoted on a large scale after the cost is reduced to achieve large-scale direct emission reduction and low-carbon utilization of fossil energy.

Terminal department

The industrial structure should be upgraded from two aspects of "energy conservation" and "emission reduction". In the short term, the supply side reform will be carried out mainly by limiting production to reduce production from the source. In the medium and long term, it is still necessary to save energy and improve efficiency through new process exploration, the use of clean energy such as electrification, and the establishment of a green circular economy, so as to reduce energy or resource consumption per unit output, To complete the transformation of energy consumption per unit GDP from the current 0.328kgce/USD to 0.119kgce/USD.

The carbon emissions of the terminal sector mainly come from the three fields of industry, construction and transportation. The energy conservation focus is to improve the level of terminal electrification rate and reduce fossil energy consumption. According to the prediction of China Energy Research Association, by 2060, the electrification rate of China's terminal sector will rise from the current 27% to 64%. The focus of emission reduction is to directly reduce the output rather than the capacity. In the last round of supply side reform, the market-oriented policy represented by differentiated electricity prices and stepped electricity prices, as well as the administrative means of checking intermediate frequency furnaces (ground bar steel) and confirming the implementation of capacity replacement, effectively promoted the elimination of backward production capacity in the steel industry, but in fact, the crude steel output kept rising in the process of supply side reform, The output of crude steel has reached new highs, which is easy to cause the imbalance between supply and demand again.

With the production of industrial products and the sales volume of fuel vehicles peaking, the demand for traditional fossil fuels will also peak. In addition, it is expected that the eight high energy consuming industries at the end of the 14th Five Year Plan will be included in the national carbon trading system, and the cost of high energy consuming enterprises with relatively backward technology may increase significantly, promoting the application of energy-saving technology and clearing out the backward capacity of the industry.

Environmental protection department

Through the establishment of a sound carbon emission monitoring and trading system, we can effectively ensure the emission reduction of energy sector and "high carbon" industrial sector, and accelerate the construction of a green and low-carbon circular economy to achieve the recycling of downstream resources, including the secondary use of scrap steel, plastics, scrap non-ferrous metals and other raw materials.

In 2011, China began to carry out local carbon trading pilot projects in seven provinces and cities, including Beijing, Tianjin, Shanghai, Chongqing, Guangdong, Hubei, and Shenzhen, and then added Fujian pilot projects. In June 2021, China will launch the national carbon emission trading market. At present, electric power enterprises have taken the lead in being included in the national carbon trading market, involving 2225 key emission units in the power generation industry. During the "14th Five Year Plan" period, seven major industries, namely petrochemical, chemical, building materials, steel, non-ferrous metals, paper making and aviation, will gradually be included in the national carbon market under the keynote of "smooth docking and smooth transition". In the medium and long term, on the one hand, enterprises included in the carbon market may be limited by emission quotas, leading to increased production costs; On the other hand, carbon emissions can also be reduced through technological transformation, and the saved quota can be sold in the carbon market to gain profits.

(About the author: Chief Economist of Beixin Ruifeng Fund)