Article/Lu Ping, columnist of Sina Financial Opinion Leader

The traditional industry represented by steel can usher in the improvement of industry fundamentals for a period of time after the implementation of the policy of improving industry concentration. However, due to the lack of strong logic such as brand barriers, price difference between ex factory price and wholesale price of industrial standard products, the traditional industry with strong cycle after the harvest of "M&A dividend" still faces cyclical fluctuations in performance, and the trend of enterprises in the industry will usher in differentiation after the end of "M&A dividend".

Summary:

In the past five years, the supply of products has exceeded the demand and the industry concentration has improved because Guizhou Moutai Represented by the main logic of the liquor industry performance and share price flying together. In the next five years, under the goal of transformation and upgrading of the traditional industry and carbon peak, the production restriction policy and merger and reorganization policy of the traditional industry will continue to ferment. It seems that the logic similar to the liquor industry will reappear in the traditional industry. Taking the steel industry as the representative of the traditional industry, this paper analyzes and compares the liquor and steel industries from the aspects of demand, supply and industry concentration. We believe that the traditional industry represented by steel can usher in the improvement of industry fundamentals in a period of time after the implementation of the policy to improve industry concentration. However, due to the lack of strong logic such as brand barriers, price difference between ex factory price and wholesale price of industrial standard products, the traditional industry with strong cycle after the harvest of "M&A dividend" still faces cyclical fluctuations in performance, and the trend of enterprises in the industry will usher in differentiation after the end of "M&A dividend".

Demand: In terms of total demand, influenced by the rise of the middle class, the liquor industry's short-term demand is stable and long-term growth is expected. However, due to the impact of urbanization entering the middle and later stages and the declining growth rate of infrastructure investment, the short-term demand of the steel industry is stable, and the long-term trend is downward. As far as the periodicity of demand is concerned, the demand of the liquor industry is cyclical, but the cycle is long, and the performance periodicity is weaker due to the price difference between the factory price and the wholesale price. The steel industry is highly cyclical and the performance cycle fluctuates greatly.

Supply: The price of upstream raw materials in the liquor industry has little impact. The liquor supply is completely regulated by the enterprise plan and has little elasticity. The output of the whole industry is gradually shrinking and the periodicity is weak. The supply of steel industry is greatly affected by demand, and the bargaining power of upstream raw materials is weak. The steel output is in a slow rise trend in the short term, but it is expected to gradually weaken under the production restriction policy in the future.

Industry competition pattern: In recent years, the industry concentration of the liquor industry has increased rapidly, and the competitive advantages and brand barriers of high-end liquor have been continuously strengthened. However, compared with foreign countries, the industry concentration still has much room for improvement. Although the policies to improve the concentration of the steel industry have been released successively, the concentration of the steel industry is still low and has not increased significantly in recent years, but the future trend is expected to be upward.

1、 Liquor industry

As a long-term high-quality race track, the main growth logic of the liquor industry is: first, it is driven by volume, and the rigid demand that can pass through the cycle and the limited capacity lead to supply and demand mismatch. The amount of supply determines the height of performance. Second, it is driven by price. Brand barriers and investment values give rise to the pricing power of enterprises. With the upgrading of industrial structure, the industry accelerates its differentiation in the stock market, The high-end Maotai flavor liquor represented by Moutai has made a breakthrough, and the secondary high-end liquor enjoying industrial dividends has quickly caught up.

1. Demand analysis

1) Mass consumption demand: vigorous growth, rigid stability

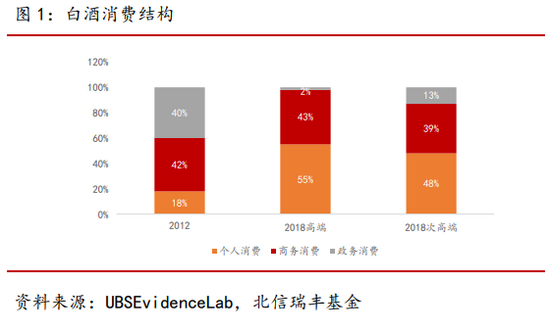

After in-depth adjustment from 2013 to 2014, the proportion of public consumption has increased significantly, while government consumption has shrunk rapidly. In 2018, government consumption accounted for only 2% of high-end liquor, and personal consumption has exceeded 55%. The liquor consumption structure has changed from government consumption to business consumption and public consumption.

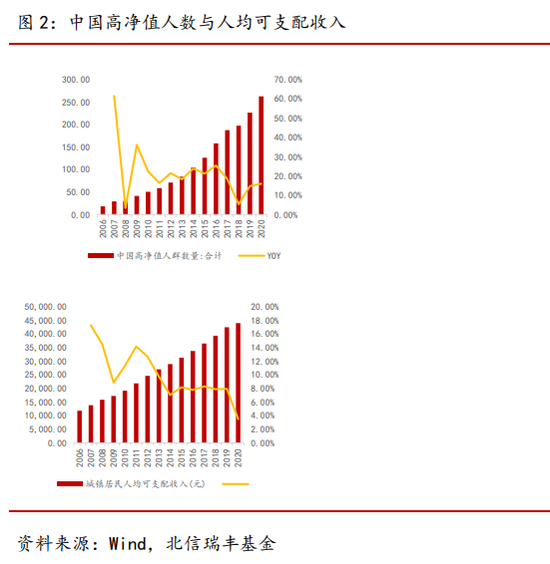

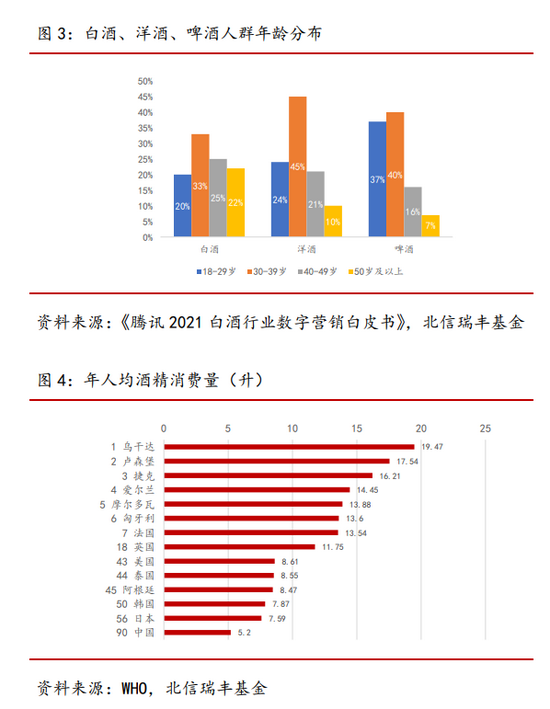

The rise of the middle class is expected to increase in the future. Liquor frequently appears in residents' ordinary festival family feast, which is bound to bring a huge increase in alcohol consumption. From 2006 to 2020, the number of high net worth people increased from 181000 to 2.62 million, with an average annual growth rate of 19.5%. The per capita disposable income of urban residents increased from 11800 yuan to 43800 yuan, with an average annual growth rate of 9.14%. In 2020, China's annual per capita alcohol consumption was 5.2 liters, ranking only 90th in the world, and Uganda's annual per capita alcohol consumption was up to 19.47 liters, which still has much room for improvement.

The demand is rigid, and the demand elasticity above the secondary high-end is small. As a mass consumer product, liquor demand itself has a certain rigidity, and the periodicity is not strong. From the perspective of product structure, with the improvement of consumption awareness and the influence of social circles, Chinese residents gradually show a consumption upgrading trend of "drinking less and drinking better". TMI data shows that in 2020, on average, 44% of consumers will drink higher quality liquor than the previous year, and the number of secondary and super high-end consumers will increase by 49% and 66% respectively. Secondary high-end and above liquors are irreplaceable due to their high brand barriers. Although the price fluctuates greatly, the demand is still strong, further weakening the periodicity of mass consumption.

2) Business and investment demand: strongly related to the economy, but with a long cycle

Considering China's long-standing liquor culture, liquor has been endowed with special social and gift consumption attributes. On the one hand, the business activities and wealth effects brought about by changes in fixed asset investment and liquidity will directly drive liquor consumption. On the other hand, when the industry boom and inflation are high, high-end liquor with hard currency attributes will also induce dealers and hot money to hoard goods. And different from other flavor types, the taste and flavor of Maotai flavor liquor are significantly related to the storage time after brewing, so it has the investment attributes of hoarding, collection and inflation prevention.

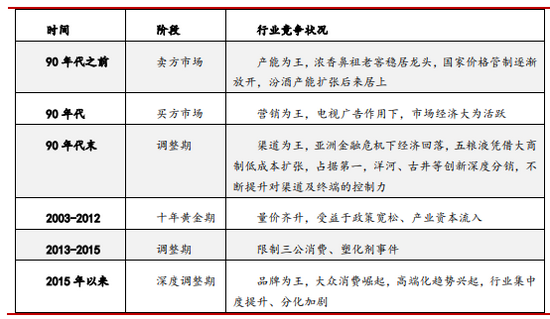

Business and investment demand are easily affected by economic operation and policies, but the cycle lasts for a long time. Since the reform and opening up, the liquor industry has mainly experienced two adjustments in 1989-1992 and 1998-2003, and then started a golden decade of development. Since the restriction of "three public consumption" and the plasticizer event in the second half of 2012, the liquor industry has entered a deep adjustment period again. This adjustment is long and large.

Table 1: Historical review of liquor industry

Source: Public information, Beixin Ruifeng Fund

Source: Public information, Beixin Ruifeng Fund 2. Supply analysis

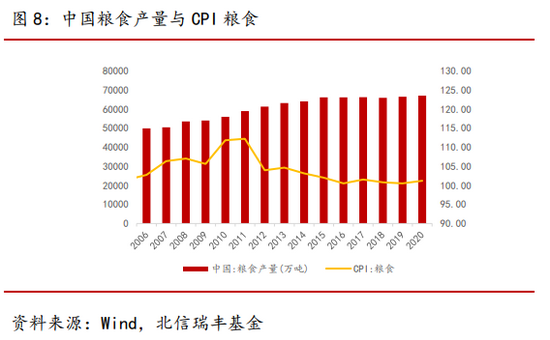

Upstream raw materials: China's liquor is a relatively closed market, which is mainly self-sufficient in China. The proportion of imports and exports is extremely low, less than 1%. In 2020, China's liquor export volume was 14.246 million liters, while the import volume was only 2.778 million liters. However, the domestic liquor output and sales volume were 7.407 million liters. At the same time, as a major agricultural country, China's grain supply was basically stable, In recent years, under the control of national policies, the price of grain has not fluctuated much. At present, the cost of raw materials and packaging accounts for a low proportion of the revenue of finished wine, about 5.2% and 6.3%.

Downstream dealers: Since the liquor market pricing was launched in 1988, the liquor sales channel model has evolved several times, and now it has developed a large business system dominated by mainstream dealers( Wuliangye )Deep distribution mode dominated by manufacturers( Gujing Gong wine Yanghe) and small dealer system (Moutai), as well as the cooperation mode jointly led by manufacturers and dealers( Luzhou Laojiao , drunkard).

In recent years, the sales system of the liquor industry has been evolving towards deep distribution and flattening. Manufacturers have constantly carried out drastic channel reforms, and have implemented product division, channel division, and region division for dealers with too large sales range. The sales revenue of the top five dealers has declined, but since 18 years, with the increase of the proportion of direct sales mode, The second level dealer was upgraded to the first level dealer, and the dealer concentration showed an upward trend again.

2) Manufacturer

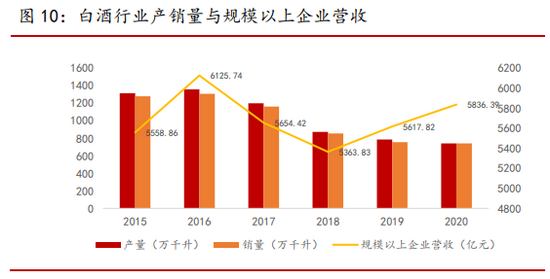

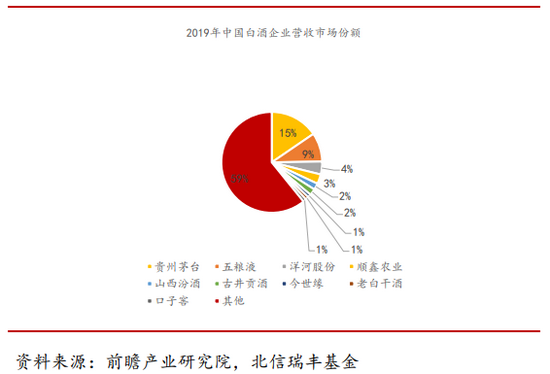

Market scale: According to the data of the National Bureau of Statistics, the number of liquor enterprises in China is about 1000 at present, and the output is 7 million kiloliters. The output and sales of liquor enterprises show an obvious downward trend, but the revenue of enterprises above the designated size has increased rather than decreased, reaching 583.6 billion yuan in 2020. The future growth is expected, which can be seen in nearly three years. The improvement of industry performance is mainly driven by price.

Source: Prospective Industry Research Institute, Beixin Ruifeng Fund

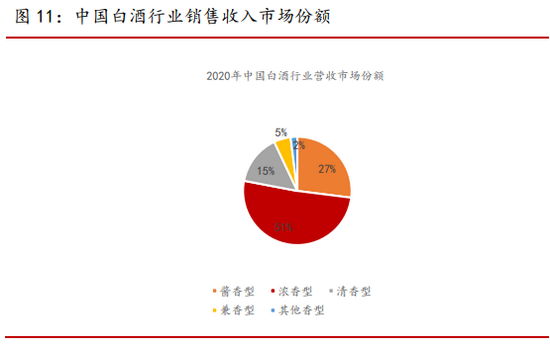

Source: Prospective Industry Research Institute, Beixin Ruifeng Fund From the perspective of market segmentation, Luzhou flavor liquor is the track with the highest market share in the liquor industry at present, accounting for 51% of the revenue in 2020, and Maotai flavor liquor and Qingxiang liquor rank second and third, accounting for 27% and 15% respectively. Maotai flavor liquor has the characteristics of small quantity and high price due to its complex process and high brand barriers, and there is a gap between Maotai and Maotai, Maotai alone accounts for 15% of the market, and the market share of Maotai in Maotai liquor is more than 63% (the market scale is more than 130 billion yuan), and more than 90% in the old wine market (the market scale is about 50 billion yuan); However, Luzhou flavor liquor has a large number of enterprises and a reasonable price belt distribution, presenting a situation of monopoly competition. Fragrant wine emphasizes the cost performance of commodities, has certain health care functions, and has cultivated its differentiated competitive advantage. Due to the low brewing threshold, it is close to complete competition.

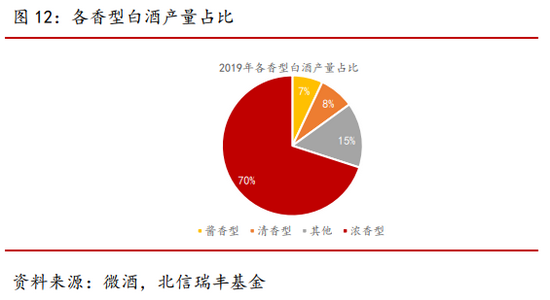

Enterprise production capacity: in 2019, the production of Luzhou flavor liquor accounted for 70% of the production structure of all flavor liquors, while the production capacity of Maotai flavor liquor was only 7%, which has a certain scarcity, which can be mainly attributed to: (1) production cycle constraints. Maotai flavor liquor requires at least 5 years from feeding to leaving the factory, while the production of Luzhou flavor liquor and Qingxiang liquor requires only 3 and 2 years respectively; (2) The yield rate of high-quality wine is limited. The longer the cellar is, the higher the yield rate of high-quality wine is. The excellent wine rate of Luzhou Laojiao cellars over 10 years is only 1% to 2%, 20% for those over 30 years, and 40% for those over 50 years; (3) The production area is limited. For example, the production of Maotai liquor is limited to 15 square kilometers of Maotai town, and the maximum production capacity is about 100000 tons.

Competition pattern: the brand concentration has increased, and the high-end trend is obvious. At present, the concentration of China's liquor industry is increasing year by year, but the proportion of CR5 is still low, only 34% in 2019. In 2018, the global liquor industry, the CR5 of South Korea, the United States, and Japan has reached 91%, 51%, and 48%, compared with China, there is still much room for improvement. At the same time, the industry differentiation has intensified. Although the overall production and sales have shrunk, the leading enterprises have continued to raise prices. From 2016 to 2019, the number of enterprises above the designated size in the liquor industry has decreased by 30.42%, which has improved the overall profitability of the industry.

3. Specific case: the rise of Guizhou Moutai

1) The first stage (2008-2012): establish category competition with the help of Maotai flavor liquor marketing

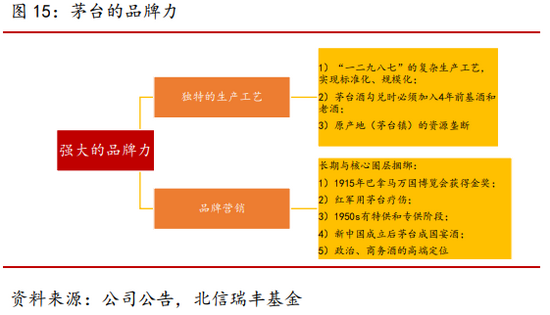

The state-owned Moutai Distillery was established in 1952, and Guizhou Moutai Liquor Co., Ltd. was established in 1999. Maotai has been known as "national liquor", "diplomatic liquor" and "export liquor" for a long time through brand marketing, which is tied to the core circle. At the same time, it pioneered the concept of liquor flavor, distinguishing Maotai liquor with Maotai flavor from other brands of liquor, and realizing the transformation from brand competition to category competition. According to Hurun brand ranking in 2020, Guizhou Moutai won the first place for the third time in a row with a brand value of 1040 billion yuan.

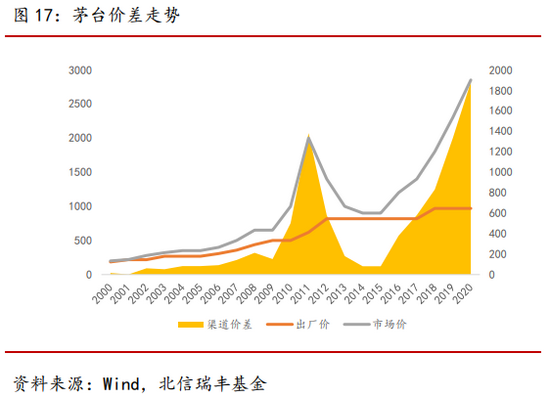

After the four trillion yuan stimulus policy, demand surged. Moutai focused on the precise consumption system of politics and commerce, quickly established a leading position, and took the initiative to raise prices. In 2008, the factory price of Feitian Moutai was adjusted to 439 yuan, which was the opposite of Wuliangye's five year old factory price. In 2012, the factory price of Moutai was increased to 619 yuan. Due to limited supply, dealers Consumers and hot money bought and stocked up in advance, and the first batch price reached 1700 yuan when it was the craziest. The dealer price difference of each bottle of Maotai liquor was up to 1000 yuan, and the retail price was 2300 yuan, gradually entering the super high-end price belt. At present, the product matrix includes (1) high-end Maotai liquor: aged liquor (6k-7w), commemorative liquor (5k-1.6w), boutique liquor (8k), zodiac liquor (4k), ordinary liquor (3k) and low-grade liquor (1k), (2) middle and low-end liquor series: one song, three maotai and four sauces, with prices mainly ranging from 300-500 yuan.

2) The second stage (2012-2014): exchange price for volume to quickly seize the market

After the event of restricting Sangong consumption and plasticizer, facing the rapidly shrinking demand for liquor, Moutai has always adhered to the ex factory price of 819 and maintained its brand image through stable prices. At the same time, the profit of dealers was increased through the development of non-standard liquor. In 2013 and 2014, the distribution right was released twice to expand sales, and the first price of Moutai liquor was lowered to try to seize the market. Since the price of Moutai hit an astonishing 1700 yuan in 2012, and then went down all the way to around 850 yuan, the price cut was far more than that of other liquor companies, attracting consumers to buy. As a result, the sales volume of Moutai liquor doubled in the three years from 2012 to 2014. The rapid price reduction has released the brand potential accumulated previously. Maotai Liquor has rapidly completed the transformation from government affairs to business and personal customers, and its channels have expanded from about 1900 at the end of 2011 to more than 2700 in 2015. However, at this time, the profitability of dealers has declined sharply, and the policy of price reduction and volume expansion can no longer be continued. At the same time, the financial attribute of Moutai has been gradually explored, and then it began to embark on the luxury like route of rapid price increase.

In contrast, in February 2013, Wuliangye "bucked the trend" and increased the ex factory price of Puwu by 10%, but the ex factory price was inversely linked to the approved price, which seriously damaged the interests of dealers and impeded sales. Although it was significantly reduced in 2014, the brand image was greatly weakened as a result.

3) The third stage (2015-2016): the demand for supply reform is weak, and the quantity and price are controlled

Since November 2014, the Maotai rating has been at a low level. The company announced that "no sales increase, no new dealers increase, and no factory price reduction in 2015" to stabilize the price. In 2016, Maotai changed the delivery rhythm from quarterly delivery to monthly delivery, reducing the one-time market entry (limited delivery). In 2017, Maotai's official caliber "guaranteed channel profit of 200 yuan", and Maotai realized the gradual rise of terminal price through volume control.

4) The fourth stage (2017-2018): both volume and price rise, channel price difference bubble

17 years ago, the revenue growth of Moutai was mainly driven by the increase of sales volume, and since then, it has been mainly driven by the increase of price. Since the beginning of 2018, the channel profit rate of Moutai has been more than 80%, and the price is seriously distorted. At this stage, Moutai tried to solve the contradiction between supply and demand by vigorously increasing prices and volume. In 2017, the ex factory price of Moutai rose to 969 yuan, and in 2018, the suggested retail price rose from 1299 yuan/bottle to 1499 yuan/bottle, and the market price has reached 1800 yuan/bottle. At the same time, the number of dealers will be greatly reduced, the proportion of direct sales of supermarkets and e-commerce will be expanded, and the channel price difference will be managed.

5) The fifth stage (since 2019): price orientation, upgrading of product and channel structure

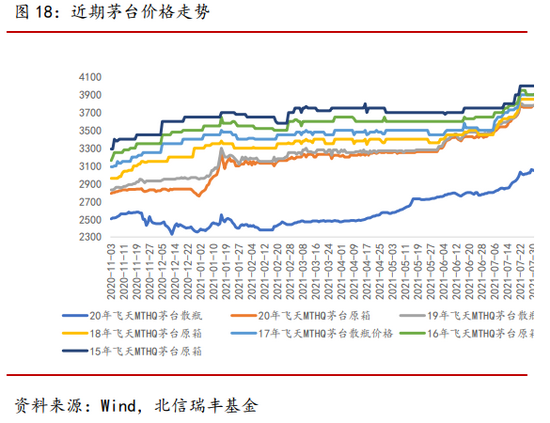

Since 2019, the "sauce wine craze" has become a hot trend in the industry. With the resumption of production and economic recovery, the Maotai rating has been rising all the way, constantly breaking the price ceiling. By the end of 2020, it will be stable around 2800 yuan, with a maximum increase of nearly 900 yuan in 2020.

Judging from the path of increasing the price of Moutai ton, this stage is mainly due to the optimization of product and channel structure. The ex factory price of Moutai has been stable for a long time since 2017. Due to the unhealthy trend of the Central Commission for Discipline Inspection to increase the price of high-end liquor, Moutai has been unable to raise the price for a long time. In 2020, under the influence of the epidemic, the sales of Moutai liquor declined, and the income growth was entirely contributed by the increase in ton price, which was mainly contributed by the direct marketing channels. At the same time, the growth rate of liquor series has increased rapidly, with a compound growth rate of 65% in 16-19. Due to the spillover of brand effect and the continuous implementation of the strategy of controlling quantity and price, the price of liquor series has increased from about 100-200 yuan in 2011 to 300-500 yuan. At the same time, around the 2021 Spring Festival, Moutai launched multiple channel price control policies, and the mandatory 100% unpacking policy was still strictly implemented, effectively combating the market chaos of dealers hoarding Moutai in boxes.

2、 Steel industry

1. Demand analysis of steel industry

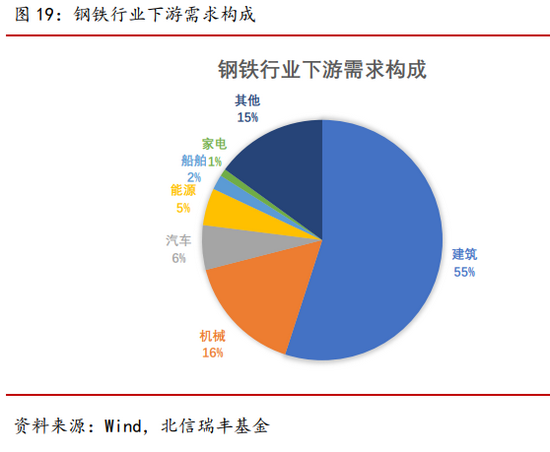

1) Composition of requirements

2) Future demand trend analysis

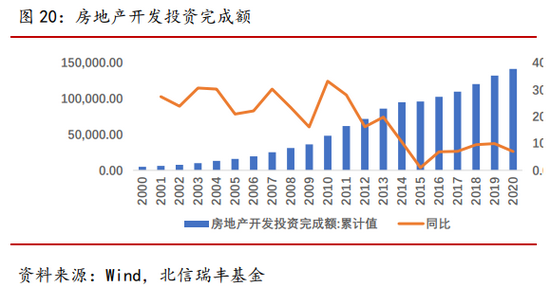

First, look at the needs of the construction industry and machinery industry. The demand of the construction industry is mainly related to infrastructure investment and real estate investment. The demand of the machinery industry is closely related to the growth of the construction industry. For this part of demand, our judgment is that it is more likely to shrink in the future. As far as infrastructure investment is concerned, the year-on-year growth rate of infrastructure investment has a very obvious correlation with the increase of urbanization rate. As China gradually enters the middle and late stage of urbanization, the growth rate of urbanization will continue to slow down, which will also lead to the slowdown of China's infrastructure investment growth. As far as real estate is concerned, from 2001 to 2020, the year-on-year growth rate of the completed investment in real estate development in China has declined. In the future, it is expected that the growth rate of investment in real estate development will further slow down under the positioning of "housing is not speculation".

Then look at the demand of the automobile industry. Data shows that from 2014 to 2020, the year-on-year growth rate of China's automobile sales showed a downward trend. Among them, there will be negative growth from 2017 to 2020. Recently, the heat of new energy vehicles is high, and the demand for some plates remains high. However, the development of new energy vehicles is only a substitute for traditional fuel vehicles, so it cannot bring about an increase in overall demand for the steel industry.

2. Supply analysis of steel industry

1) Supply status of steel industry

From the perspective of blast furnace operating rate, from 2012 to 2021, China's blast furnace operating rate continued to decline, and supply showed a tightening trend.

From 2013 to 2020, China's crude steel output showed a slow growth, and the growth rate fluctuated significantly, with obvious cyclical changes.

On the whole, since the era of high growth of domestic infrastructure construction, real estate investment and automobile sales has passed, and with the deep contradictions of high global debt, rich poor differentiation, and aging population, there is greater certainty that steel demand will shrink in the long run.

2) Supply concentration of steel industry

From 2009 to 2020, the proportion of the output of key enterprises in the national crude steel output showed a fluctuating downward trend, and the problem of low industry concentration was not significantly improved.

3) Analysis of future supply trend

Recently, the state has issued steel production restriction policies for many times to resolve the overcapacity of the steel industry and help achieve the goal of carbon neutrality. The carbon reduction path of the steel industry includes: directly reducing output, eliminating backward and overcapacity, and improving industry concentration. On January 26, 2021, the spokesman of the Ministry of Industry and Information Technology said that in 2021, the steel production would decline year on year.

However, from the data side, China's crude steel production capacity basically maintained a slow growth trend from 2013 to 2020, and the production restriction logic remained on the policy expectation, which has not yet been fulfilled. Even if the logic is fulfilled and the steel supply drops, the steel enterprises may not benefit from it. On the one hand, this is just a price increase in exchange for volume reduction, which leads to a discount for the improvement effect of price increase on profitability, which is obviously different from the logic of the simultaneous increase in the volume and price of high-end liquor. On the other hand, production restriction can only weaken the cyclical fluctuation of steel supply, but cannot be completely eliminated. This has also led to the difficulty for steel enterprises to achieve steady growth in performance. For high-end liquor represented by Moutai, even though the demand for liquor also fluctuates periodically, due to the large interest margin between the ex factory price and the wholesale price for a long time, when the ex factory price is far lower than the wholesale price, liquor enterprises can steadily increase the price of their products, thus achieving a long-term stable growth of performance.

3. Cost analysis of steel industry

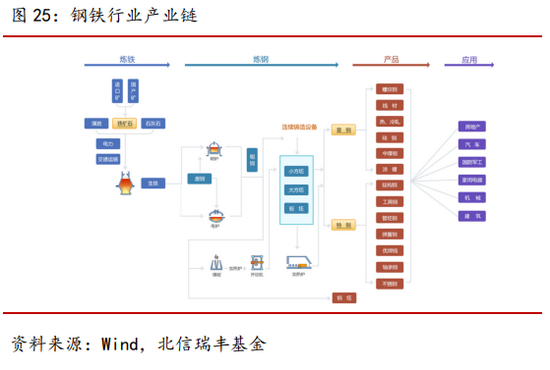

1) Basic production process

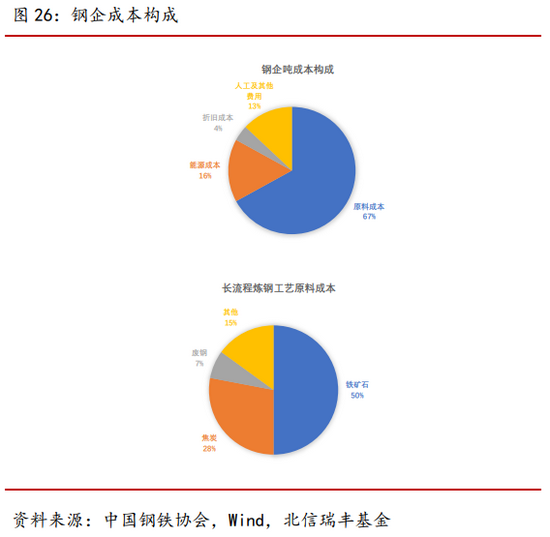

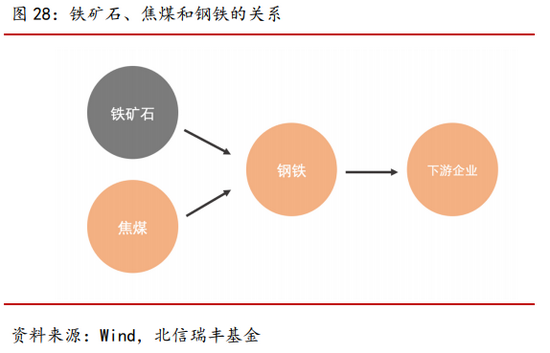

The raw materials for steel production mainly include iron ore, scrap steel and coking coal. The production process of steelmaking is divided into long and short processes, and different processes have their own advantages and disadvantages. The cost of the long process steelmaking process is low, but the carbon emission is large and the pollution is serious. Short process steelmaking has small carbon emissions and is easier to carry out personalized production, but the cost is high, which will squeeze profits. At present, the output of long process steelmaking in China accounts for about 90%, and that of short process steelmaking accounts for about 10%. Because long process steelmaking accounts for a large proportion, the steel cost is mainly calculated by the long process steelmaking process. The cost of raw materials is the most important part in the long process steelmaking technology. We can analyze the current situation of iron ore and coke, the two main parts of raw material cost.

2) Iron ore

The iron ore supply of the steel industry mainly comes from domestic iron ore and imported iron ore, and the proportion of the two remains around 1:4. The import of iron ore mainly comes from Australia. The cost of domestic iron ore mining is usually high, and the quality is poor, leading to the domestic iron ore price is often higher than the import iron ore price.

Although China is the largest iron ore importer, it has no advantage in pricing. On the one hand, the concentration of China's steel industry is low, the demand is scattered, and the cooperation between enterprises is insufficient in the price negotiation process when importing iron ore. On the other hand, there is a monopoly pattern in the iron ore market. The world's four major iron ore suppliers account for 44% of the world's output of ore, which determines that they can control the price of iron ore while the demander can only passively accept it.

The weak bargaining power over upstream enterprises has become an important reason for the low profit rate of China's steel enterprises. Comparing the performance of the world's three largest mines and China's three largest steel enterprises in 2019, it is not difficult to find that the profit rate of China's steel enterprises is significantly lower than that of the three largest mines, and most of the profits in the industrial chain are taken away by mines.

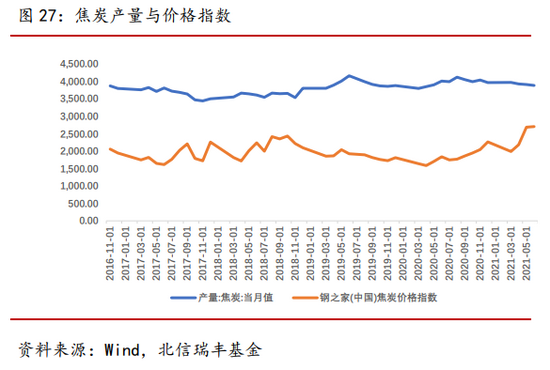

3) Coke

Most iron and steel enterprises in China have their own coking equipment, and the self-sufficiency rate of coke is usually high, which can basically meet their own production needs. At present, most of the coking coal required by China's iron and steel enterprises for coking comes from China. The iron and steel enterprises usually adopt long-term agreements, and the group purchases centrally. Some enterprises will also invest in relevant upstream enterprises to ensure the stability of raw material supply. The coking coal industry chain is also relatively dispersed, and import substitution is relatively easy, so the bargaining power is relatively weak. In the context of the recent policy of restricting the import of coking coal, the bargaining power of the domestic coking coal industry has increased, and the price of coking coal has risen, which has enabled more profits in the steel industry chain to concentrate on the coking coal industry.

Similar to coking coal industry, similar logic is happening in steel enterprises. Due to the low self-sufficiency rate of the iron ore industry and the obvious oligopoly pattern, China needs to use a large amount of foreign exchange to import a large amount of iron ore at a high price all the year round. This has damaged the interests of coking coal, steel and downstream enterprises related to China's economic interests in the industrial chain, and has left China's industrial chain at the low end of the value chain all the year round. At present, the steel industry has introduced a series of measures to improve industrial concentration and limit production, which is also expected to improve the bargaining power and industrial chain position of the steel industry.

4. Analysis on Concentration of Iron and Steel Industry

1) Current situation of steel industry concentration

At present, the concentration of China's steel industry is low. Data shows that in 2020, the CR10 of China's steel industry will be about 22%, far below the level of developed countries such as the United States, and the industry competition pattern needs to be improved.

2) Increasing the concentration of the iron and steel industry will improve the operating efficiency of the industry

Recently, in order to optimize the development pattern of China's steel industry, the country has issued a series of relevant policies. In 2011, China issued the 12th Five Year Plan for the Development of the Iron and Steel Industry, which requires large steel enterprises and groups such as Baosteel and Wuhan Iron and Steel to play a leading role in accelerating the merger and reorganization of steel enterprises. In 2016, China successively issued the Guiding Opinions on Promoting the Merger, Reorganization and Disposal of Zombie Enterprises in the Steel Industry and the Plan for Adjustment and Upgrading of the Steel Industry (2016-2020), which clearly pointed out that by 2025, 60% - 70% of the domestic steel industry output will be concentrated in the top 10 steel groups. Compared with the target of 60% - 70% CR10 in 2025, China's CR10 level in 2019 is still far from the target, with a large space for improvement. The goal of 2025 will be achieved in the future, and the continuous and rapid rise of the steel industry in the next five years will become a certainty event, which will bring many benefits to the steel industry. For example, the increase of industry concentration is convenient for leading enterprises to jointly purchase raw materials, improve the bargaining power on upstream, and reduce the cost of raw material import; Through mergers, steel enterprises can obtain multiple business synergies and improve business efficiency.

Taking the merger of Wuhan and Baosteel as an example, after the merger of the two enterprises, Baosteel has gained many benefits by combining the advantageous resources of WISCO.

First, Baosteel optimized the structure of spatial layout. Baosteel combines Wuhan Qingshan Base and Guangxi Fangchenggang Base of WISCO with Baoshan Base in Shanghai, Meishan Base in Nanjing and Dongshan Base in Zhanjiang. Shanghai, Zhanjiang and Fangchenggang bases located in the Gulf region can reduce transportation costs by sea. Wuhan bases can make up for the lack of production bases in the central region, improve Baosteel's production strength in the central region and improve business efficiency.

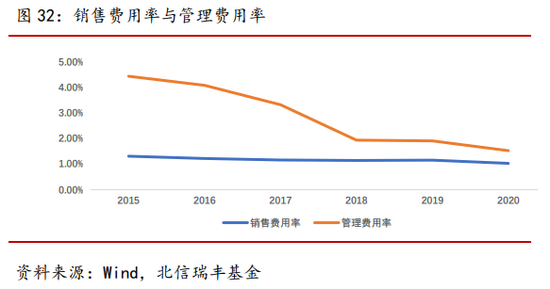

Second, Baosteel has integrated business content and shared human resources. In terms of business content, after the merger of Baosteel and WISCO, Wuhan Iron and Steel's subordinate branches, internal marketing channels and processing centers were integrated into Baosteel International, realizing the development and sharing of sales channels. In terms of human resources sharing, after 2017, all employees of WISCO were merged into Baosteel International, making Baosteel The number of production personnel increased from 21807 to 36734, and the number of technical personnel increased from 10222 to 13441, greatly improving the production and R&D capabilities. From the data point of view, after 2017, Baosteel's per capita income increased steadily, and its sales expense rate and management expense rate continued to decline.

Thirdly, the merger between Baosteel and Wuhan Iron and Steel is a horizontal merger, which expands the market share of Baosteel and facilitates the acquisition of economies of scale. This is not only conducive to reducing the fixed costs of enterprises, but also conducive to improving the bargaining power of upstream and downstream enterprises, thus improving the profitability of enterprises. From the data, after 2017, Baosteel's gross profit rate and net profit rate of sales have increased to a certain extent.

3) Comparison with the United States: with the advent of M&A era, the steel industry may usher in two stages of market

The concentration of the U.S. steel industry accelerated from 1999 to 2010, marked by the rapid rise of leading enterprises from 1999 to 2004; 2007-2010 marked by the rise of second tier leaders. This led to the rapid increase of gross and net profit rates of the steel industry from 2001 to 2007.

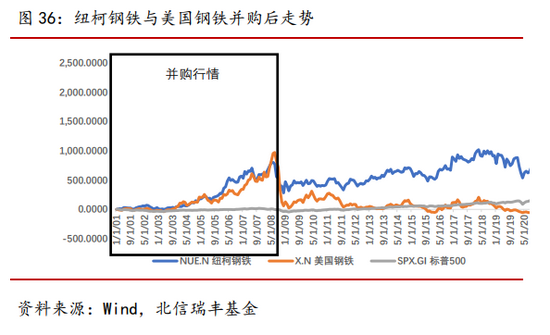

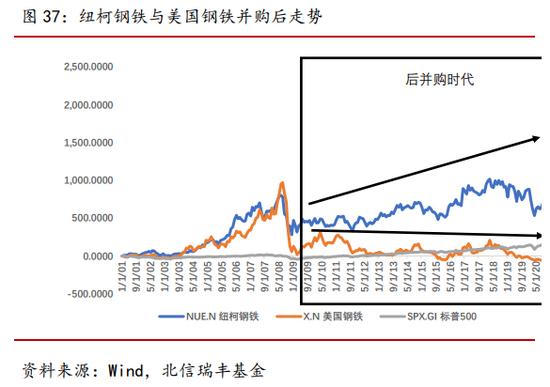

With the continuous development of steel M&A in the United States from 1999 to 2007, the operating conditions of major steel companies continued to improve, and the steel industry shares also ushered in a round of "M&A market". From 2001 to 2008, the largest cumulative growth of Nucor Steel and American Steel reached 802% and 970% respectively, while the largest cumulative growth of the S&P 500 index during the same period was only 17%.

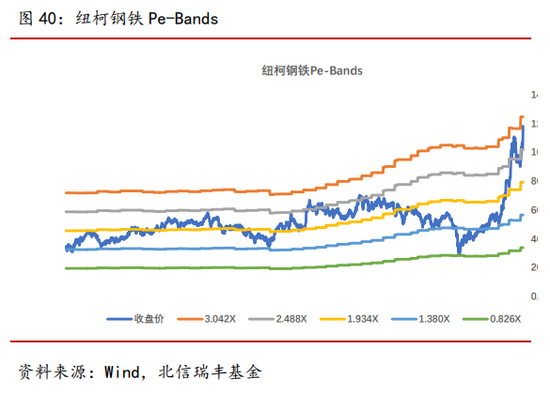

"When the tide recedes, we will know who is swimming naked." In the post M&A era, the M&A dividend gradually wears out, and the "M&A market" of the steel industry ends, and then enters the differentiation stage. As a strong cyclical industry, the improvement of industry concentration will not change the cyclical fluctuation of industry prosperity. And excellent enterprises can always go through the economic cycle, minimize the cyclical shocks of performance, achieve stable growth of performance, and thus bring stable long-term returns to investors. Taking American Steel and Newcastle Steel as examples, after their substantial withdrawal in 2008 and entering the "post merger era" of the steel industry, their stock prices have shown two different trends. Newcastle Iron and Steel continued to walk out of the slow rising market and hit a new high recently. The stock price of American steel has been falling all the way. The reason is that the outstanding management ability of Nuke Steel has ensured its steady growth of performance.

First, Newcastle Iron&Steel implements the flexible strategy of human resources to achieve flexible management of working hours. During the period of economic prosperity and industry prosperity, Nucor will extend the working hours of its employees and accelerate the pace of production as needed. In the period of economic depression and poor industry prosperity, Nucor will reduce the number of production personnel and working hours, so as to minimize the impact of the economic cycle on performance.

Second, Nucor has high operating efficiency, which has greatly saved costs. Nucor has a small number of management personnel and high efficiency. According to data, the ratio of management personnel and production personnel of Nucor is 1:300. This ratio is not only the smallest in the U.S. steel industry, but also far less than the 1:10 ratio of Baosteel Group, the leading domestic steel enterprise.

Thirdly, Nuke Steel actively implements the diversified business strategy, constantly develops a variety of products such as special steel and alloy steel, and constantly expands its production and business fields to the upstream energy, raw materials and downstream processing and sales fields, constantly cultivating new growth points of performance.

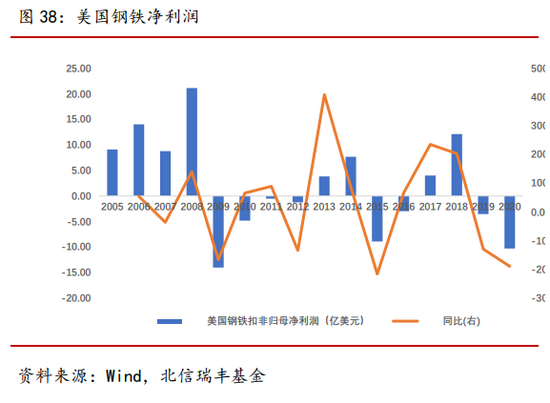

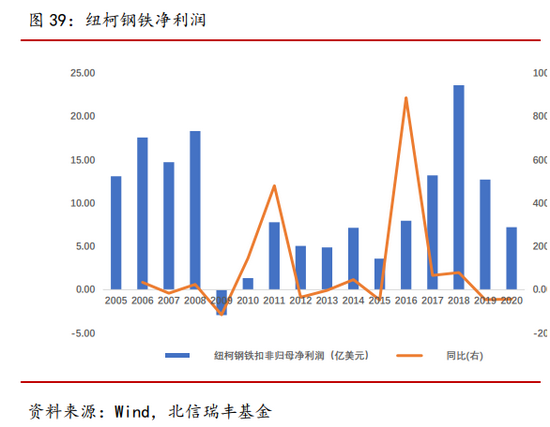

From the performance of American Steel and Nucor Steel in 2005-2020, it can be seen that the performance of both companies is subject to cyclical fluctuations due to the impact of economic cycles. However, compared with American steel, Newcastle Steel's net profit deducted from non parent company did not decline significantly in the years with poor industry prosperity, thus ensuring the fluctuation and rise of net profit deducted from non parent company, constantly improving the profit center, and becoming a strong guarantee for the rise of the valuation center.

Compared with the United States, China's steel industry may enter the stage of rapid increase in industry concentration in the next five years, bringing a round of "M&A dividend". The overall improvement of industry operation will drive the overall elevation of the steel industry's valuation center. When the industry concentration reaches a high level, the market will be differentiated. Enterprises with scientific operation and management methods, correct strategic policies, and strong cost control ability are often able to go through the boom and bust cycle of iron and steel, and finally stand out and go out of the continuous growth market.

3、 Comparison between liquor industry and steel industry

Although there are many similarities in logic between the steel industry and the liquor industry, there are essential differences between them. In terms of demand, with the increase of per capita disposable income in China, the demand of liquor industry still has a large growth space. Affected by the slowdown of urbanization and infrastructure investment in China, the demand of the steel industry is expected to decline in the long run. In addition, due to the special social, gift and investment attributes of liquor, as well as the price difference between the factory price and the wholesale price of liquor, the performance volatility of liquor industry is weak. The steel industry is greatly affected by the world economic cycle, with strong cyclicality. In terms of supply, the liquor industry is restricted by the production cycle, and the supply is greatly constrained. The steel industry is mainly affected by the environmental protection and production restriction policy, and the supply is expected to decline in the future. In terms of the industry competition pattern, the industry concentration of the liquor industry has been greatly improved at present, and the competitive advantages and brand barriers of high-end liquor have been constantly strengthened. However, the current industry concentration of the steel industry is still low. Although the relevant departments have issued the policy goal of improving the industrial concentration of the steel industry, it remains to be seen whether it can be achieved.

Therefore, we believe that if the policy goal of improving industry concentration can be fulfilled, the traditional industry represented by the steel industry will be favorable in the short term, and the fundamentals will be improved. However, because the traditional industry is dominated by industrial standard products, which are lack of differentiation, and the homogenization is very serious, the competition in the traditional industry is dominated by cost control ability. After the "M&A dividend" subsides, enterprises still face greater competitive pressure, and large cyclical fluctuations in performance are still unavoidable. It is expected that enterprises in traditional industries will face differentiation after the "M&A dividend" ends.

(About the author: Chief Economist of Beixin Ruifeng Fund)