Article/Lu Ping, columnist of Sina Financial Opinion Leader

In the future, in the case of long-term bottom grinding of pig prices, the leading enterprises are expected to obtain periodic excess profits in the downward cycle by reducing costs and improving efficiency. At the same time, after some small and medium-sized farmers accelerate clearing out of the industry due to serious losses and capital chain rupture, they will follow the trend to supplement capacity vacancies and further increase market share, It is suggested to continue to pay attention to the realization degree of cost improvement of leading enterprises.

Summary:

A complete pig cycle lasts for 3-4 years, and the core concern is the change of breeding sows. Since 2006, China has experienced three complete pig cycles.

The first round: July 2006 February 2010. The outbreak of "blue ear disease" in the summer of 2006 led to a decrease in the stock of reproducible sows and a shortage of market supply. From July 2006 to March 2008, pig prices rose. Since then, the epidemic has been controlled and the pig price has entered a downward cycle. In June 2009, the government started the frozen meat storage work to cover the pig price and release the bottom signal.

The second round: from February 2010 to April 2014. The outbreak of "foot and mouth disease" in February 2010 accelerated the pig price to reach the bottom, which fell to 9.70 yuan/kg in June 2010. Since then, a new round of rebound has begun, with a cyclical high point in September 2011. Since then, the market has entered the stage of eliminating the production capacity of sows again, and the pig price has entered the downward channel.

The third round: from April 2014 to May 2018. In April 2014, the pig price rebounded from the bottom. Since 2015, environmental protection policies have become stricter, and pig prices have continued to rebound to the peak in June 2016, breaking 21.2 yuan/kg. Since then, the pig price in 2017 has been in a downward phase. Until May 2018, the pig price has dropped to 10 yuan/kg.

The fourth round that has not been completed: the outbreak of "African swine fever" in August 2018 became a catalytic factor at the turning point of the new cycle. At the end of October 2019, it broke the 40 yuan/kg mark, almost twice the high point of the previous cycle. In 2020, the domestic pig market will still maintain the situation of supply exceeding demand, and the price of pigs will fluctuate at a high level. Later, thanks to the continuous introduction of policies to support the resumption of pig production in various regions, the national pig production capacity will accelerate recovery. Since January 2021, the domestic pig price has fallen rapidly. When we see that "the pig price is more than three months lower than the average cost of the industry", "the price of eliminated sows has continued to fall", and "the price of binary sows has fallen below 1000 yuan/head" in the industry, the bottom inflection point of the cycle may come. The downward phase of the pig cycle may be extended to 2023. In the future, in the case of long-term bottom grinding of pig prices, the leading enterprises are expected to obtain periodic excess profits in the downward cycle by reducing costs and improving efficiency. At the same time, after some small and medium-sized farmers accelerate clearing out of the industry due to serious losses and capital chain rupture, they will follow the trend to supplement capacity vacancies and further increase market share, It is suggested to continue to pay attention to the realization degree of cost improvement of leading enterprises.

1、 3-4 year pig cycle regression

1. Pig cycle

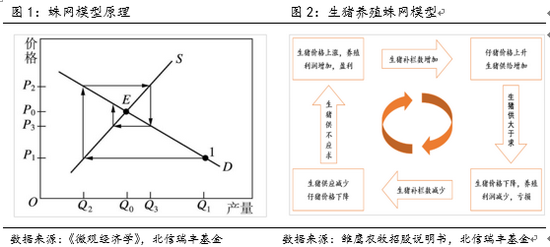

China's pig breeding perfectly fits the cobweb model. The cobweb model is a model that describes the interaction between demand, supply and price of goods in a continuous period of change in a perfectly competitive market. According to the cobweb model, the current demand depends on the current price, but the current supply depends on the price of the previous period, so it is easy to lead to a phased imbalance between supply and demand. The rise in pig prices has led farmers to form positive expectations for the future. Their action to supplement the fence will lead to an increase in the supply of live pigs in the next period, while the elasticity of demand for pork is relatively small. The excess supply of pork in the next period will lead to a decline in the price of pork in the current period. At this time, the loss expectations of farmers urge them to eliminate sows to reduce the supply in the next period, which will increase the price of live pigs in the next period. The supply and demand relationship of pigs fluctuates so repeatedly to form a "pig cycle".

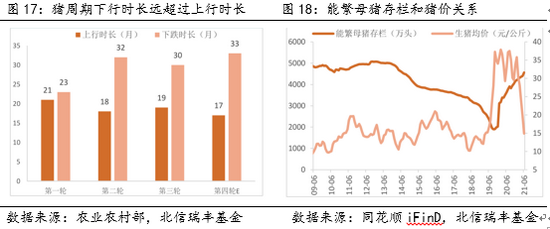

A complete pig cycle lasts for 3-4 years, and the core concern is the change of breeding sows. The ability to breed sows in the pig cycle is the core productivity. It will take about 14 months from the supplement of sows to the sale of live pigs. The changes in the stock of sows will affect the sale of commercial pigs in the next 14 months or so. If the farmers are in a long-term loss state, or affected by the epidemic situation and other factors, the stock of breeding sows will be reduced, which will lead to the shortage of live pigs 14 months later, leading to the peak of pig prices. The production time of live pigs determines that its cycle law is different from that of general industrial products, and it is difficult to be affected by short-term policies to cause greater price fluctuations.

2. Go back to the pig cycle in history

Since 2006, China has experienced three complete pig cycles.

The first round: July 2006 February 2010. The outbreak of "blue ear disease" in the summer of 2006 led to a decrease in the number of reproducible sows on hand and a shortage of market supply. From July 2006 to March 2008, the pig price rose, reaching a cyclical high in March 2008, and the pig price exceeded 17.45 yuan/kg. Since then, the epidemic situation has been controlled, production capacity has recovered, pig stocks have continued to rise, and pig prices have entered a downward cycle. After the Spring Festival in 2009, the pig price continued to decline. In June 2009, the government started the frozen meat storage work to cover the pig price, releasing the bottom signal.

The second round: from February 2010 to April 2014. The outbreak of "foot and mouth disease" in February 2010 accelerated the bottom of pig prices, which fell to 9.70 yuan/kg in June 2010. Since then, a new round of rebound has begun. In September 2011, there was a cyclical peak, and pig prices rose to 19.92 yuan/kg, up 105.4%. Since then, the market has once again entered the stage of eliminating the production capacity of sows, and the pig price has entered the downward channel.

The third round: from April 2014 to May 2018. Influenced by the low pig price in 2013-14, the pig breeding industry suffered a total loss, and farmers were more willing to eliminate sows, which accelerated the elimination of breeding sows. In April 2014, the pig price bottomed out and rebounded. Since 2015, the environmental protection policy has become stricter, the prohibition, restriction and removal of pig breeding in various regions have been strengthened, the threshold for pig breeding has been raised, and small and medium-sized farms have accelerated their withdrawal from the industry. The pig price has continued to rebound to the peak in June 2016, breaking through 21.2 yuan/kg. Since then, the pig price in 2017 has been in a downward phase. Until May 2018, the pig price has dropped to 10 yuan/kg.

3. A new round of pig cycle has reached the bottom of profitability

African swine fever is rampant, and a new round of pig cycle has set a new record. In August 2018, the outbreak of "African swine fever" became a catalytic factor at the inflection point of the new cycle. The panic selling of farmers led to the continuous decline of pig prices and accelerated the reduction of production capacity. Due to the greater impact of African swine fever on sows, the number of breeding sows on hand has continued to decline at an accelerated rate since the outbreak, reaching the lowest point of 19.13 million in September 2019. The pig production capacity has been severely damaged. The impact of this non epidemic situation (not zoonosis) on consumption demand is relatively small, and the gap between market supply and demand continues to emerge, In this round of pig cycle, the pig price rose all the way to a record high, breaking the 40 yuan/kg mark at the end of October 2019, almost twice the peak of the previous cycle, and the prosperity of the new round of pig cycle was better than any previous cycle.

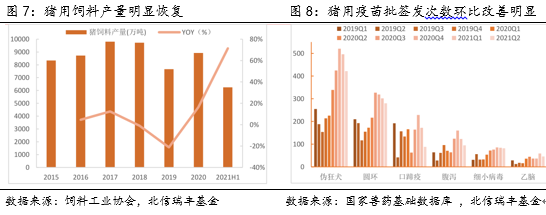

Non plague prevention and control has entered normalization, and pig reproduction has accelerated. With the remarkable achievements in the prevention and control of swine plague in Africa, the stock of domestic reproducible sows has rebounded from the bottom in October 2019, but it will take about 14 months from the supplement of reproducible sows to the sale of live pigs. In addition to the impact of the new domestic epidemic in 2020 on the resumption of production and the impact of sporadic outbreaks of non plague, the domestic pig market will still remain in short supply in 2020, The price of pigs fluctuated at a high level of 30-35 yuan/kg, which benefited from the continuous introduction of policies to support the resumption of pig production in various regions and the accelerated recovery of pig production capacity nationwide. According to the statistics of the National Bureau of Statistics, 45.64 million sows can be bred nationwide by the end of June 2021, equivalent to 102% by the end of 2017; The pig population was 439 million, up to 99.4% at the end of 2017. On the other hand, the comprehensive recovery of pig production capacity can also be verified through the substantial growth of pig feed production and the continuous improvement of the number of pig vaccine batches issued month on month.

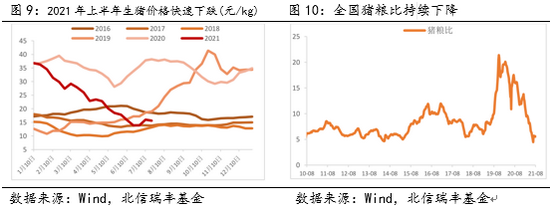

Pig prices fell, feed rose, and pig breeding profits were squeezed in both directions. From the second half of 2019 to the end of 2020, pig breeding will maintain a high degree of scenery, and the profit of self breeding and self breeding mode will be maintained at more than 1500 yuan/head for a long time; The outsourcing piglet fattening model also has a considerable long-term benefit. Since 2021, with the faster than expected recovery of pig production capacity and the growth of replacement consumption of poultry meat, the tight supply and demand of pork in the market has been eased, the pig price has entered a downward range, the superimposed feed cost has been rising, and the pig breeding income has been gradually compressed. In June, the pig price fell below the cost line of self breeding and self rearing, and the loss of self breeding and self rearing of pigs once exceeded 500 yuan/head; The fattening mode of purchased piglets entered the loss stage at the end of February, and the loss reached 1500 yuan/head at the end of June. The national average pig grain price fell to 4.90:1 in June, entering the first level warning range of excessive decline, and the central and local governments started to collect and store frozen meat to cover the pig price.

2、 The current market supply is sufficient, and the bottom of the cycle has not yet formed

1. The pork supply is abundant and the consumption demand lacks support

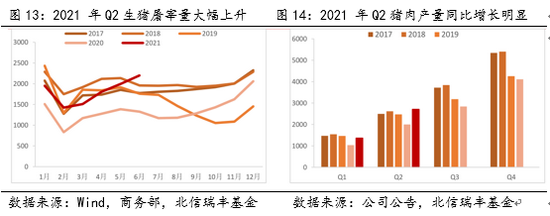

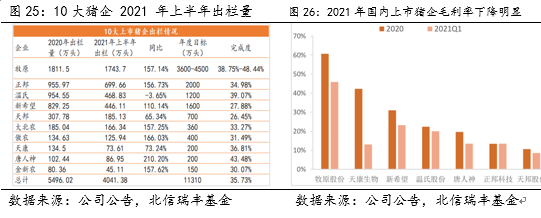

At present, the panic selling of big pigs in the market has declined significantly after they were held down, but the pork supply is still abundant. At the beginning of this year, the non pestilence in North China and the epidemic in Northeast China affected the rhythm of the resumption of live pig production. The market was generally bullish towards the mid year market, and there was an increase in the number of farmers holding down the fence and secondary fattening. The price of live pigs in the second quarter was lower than expected, which caused panic selling of large weight pigs after holding down the fence in May and June, directly leading to the market's pig slaughtering volume and pork production breaking new historical highs, Among them, in June, the pig slaughter volume of slaughtering enterprises above the national scale reached 22 million, up 66% year on year; In the second quarter, the national pork output was 13.46 million tons, up 40.2% year on year. In July, the pig marketing structure was improved. The proportion of large pigs above 150kg dropped from a high of about 25% in the middle of May to about 11% at the end of July. The supply capacity of fat pigs declined significantly New hope The average selling weight of pig enterprises has declined, but it still remains above 130kg, which is at a relatively high historical level. The market has abundant pork supply.

In the second half of the year, it is difficult for demand to be significantly boosted, and the inflection point of supply and demand has emerged. The change in consumption is gradual. In the first half of 2021, the pork trading volume of major domestic wholesale markets increased by about 56% year on year. However, restrained by the consumption supplement of poultry meat, eggs and other substitutes, combined with the COVID-19 epidemic and the weakening of seasonal demand, the pork consumption in the first half of the year was generally lower than the level in 2018, and the supply and demand in the second quarter of this year were oversupplied. In general, pork consumption in the third and fourth quarters should pick up due to the increase of household fresh sales, the promotion of school entrance banquet, and the start of school season, Mid Autumn Festival, National Day and other holidays. However, due to the recent multiple outbreaks of the COVID-19 epidemic, strict epidemic prevention and control measures have been taken in many places, which has impacted the demand for food and beverage such as college entrance banquet and group meal, and some colleges and universities have delayed the start of school or curbed campus consumption; In addition, due to the flood disaster in some provinces, the pig transportation is not smooth, resulting in local supply and demand mismatch; In addition, at present, poultry meat and imported frozen pork are in sufficient supply in the market, and the price is cheap, which will continue to restrain pork consumption. On the whole, the recovery of market demand in the third quarter was less than expected, and with the high supply of pork, the spread of the COVID-19 epidemic intensified. The market supply of pork may have crossed the inflection point of supply and demand, and will continue to oversupply for a long time.

2. The process of capacity reduction is not as expected, and the bottom of the cycle has not yet formed

The domestic pig cycle has a long decline stage. The upward duration of pig cycle is determined by the replenishment time of breeding sows and commercial pigs. In the cycle of rising pig prices, farmers are often able to quickly supplement the inventory driven by interests. When the price reaches the high point and enters the downward cycle, as long as the pig price is higher than the breeding cost, the farmers are still profitable. Superimposing the bullish expectations of most retail breeding on the future market, the market capacity is often reduced slowly, leading to the downward cycle far exceeding the upward cycle. Three rounds of pig cycle in history have verified this phenomenon.

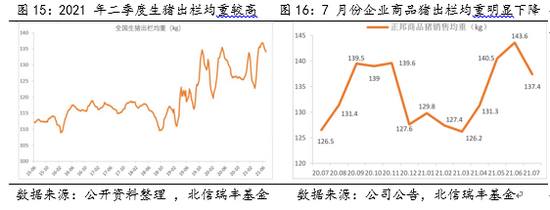

This round of pig cycle has made slow progress in capacity reduction. Unlike the historical pig cycle, this round of pig cycle peaked in October 2019, and the pig price will remain at a high level of 30-35 yuan/kg in 2020. Some free range farmers have greater profit space by virtue of cost advantages in labor, feed and other aspects. Sanyuan sows have become the consensus of many farmers, It also resulted in extremely low turnover of sows in the market in 2020. Since January this year, the domestic pig price has dropped rapidly, and the replacement of binary sows with ternary sows has continued to advance. However, the proportion of ternary sows is still as high as 20% - 30%, and it will take a long time for all of these ternary sows to be replaced with binary sows. In addition, at present, the average weight of pigs on sale is still higher than the perennial level, and the market will go through a process of de fattening pigs.

At present, the bottom of the cycle is not clear. Generally, we can judge whether the pig cycle has bottomed out by combining the three indicators of "the relationship between pig price and cost", "the price of eliminated sows" and "the price of binary sows".

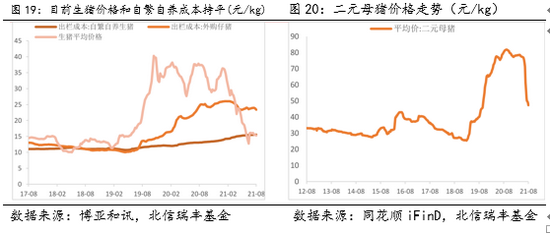

(1) The pig price is lower than the cost for more than three months. "The relationship between pig price and pig raising cost" is the key indicator to judge the bottom of the cycle. At present, there are still a large number of retail farmers in China. Generally, when the pig price has just fallen below the cost line, the retail farmers will choose to hold down the column due to their bullish sentiment towards the future market. If the pig price is below the cost line for a long time, the retail farmers will suffer serious losses and the capital chain will break, thus exiting the industry and leading to a decrease in market supply, the pig price may lead to an inflection point. Since June this year, the price of live pigs has fallen below the cost line of self breeding and self raising. However, with the expansion of industrial capacity reduction and the state's purchase and storage of frozen meat, the price of live pigs has slowly returned to 15-16 yuan/kg, which is basically the same as the average cost of the industry. Therefore, individual farmers will continue to operate based on their cost advantages in labor, feed, plant and other aspects. If we can see that the pig price falls below the cost line for more than three months, we may see a large number of individual farmers abandon the industry, and then the market supply will decline.

(2) Eliminate the price of sows and the price of binary sows. "The price of eliminated sows and dual sows" is an indicator to judge the speed and progress of capacity reduction. At present, there is still some profit space for retail breeding, and there are not many pig farms that actively eliminate sows. In the future, the price of eliminated sows will still have a large space for decline when large-scale production capacity is cut. With the acceleration of the process of replacing binary sows with ternary sows, binary sows may meet the peak or even saturation in stock. At present, the price of binary sows remains at about 1500 yuan/head, which is still at a high level compared with 2018. After the pig price continues to decline in the future, the demand for piglets will be suppressed. The average price of binary sows may continue to decline to 1000 yuan/head, indicating that farmers have suffered serious losses, Hurdle filling is in low mood.

The downward phase of this pig cycle may be extended to 2023. Although the horizontal performance of the bottom of pig price in July August this year is outstanding, there is still some distance from the real bottom of the cycle, and the key indicators are not clear. On the whole, the number of breeding sows on hand has returned to the normal level in 2017, indicating that the supply of commercial pigs will be guaranteed in the next 10-14 months. Against the background of weak consumer demand, the pig price may continue to dip to 10 yuan/kg in the next year and a half, and then linger at the bottom for a long time. The downward phase of this round of pig cycle may be extended to 2023. When we see that "the price of live pigs is lower than the average cost of the industry for more than three months", "the price of eliminated sows continues to fall", and "the price of binary sows falls below 1000 yuan/head" in the industry, the bottom inflection point of the cycle may come.

3、 The post cycle industry accelerates differentiation, and cost advantages create core competitiveness

1. The rising cost of pig raising has become the norm

The prices of corn and soybean meal remained high, and there was little room for improving feed costs. Among pig breeding costs, feed costs account for the largest proportion, about 60%; The raw material composition of fattening pig feed is about 65%, soybean meal 23% and bran 5%, so the change of pig breeding cost is mainly affected by the price fluctuation of corn and soybean meal. Since 2020, due to the tight supply and demand of domestic corn and soybean, the prices of corn and soybean meal have continued to rise, which directly led to the rising feed for fattening pigs. Since 2021, China has increased the import volume of corn and other grain substitutes, combined with the use of wheat instead of feed corn, which has eased the domestic supply pressure to a certain extent, but on the whole, the supply and demand gap of corn and soybeans remains. Since July, the prices of corn and soymeal have remained high and fluctuated, and there is little room for pig enterprises to improve feed costs.

The epidemic prevention and control was carried out normally, and the epidemic prevention cost of pig enterprises increased. African swine fever has a high mortality rate, strong infectivity and high possibility of recurrence, which puts forward higher requirements for the biosafety level of pig breeding enterprises. The epidemic prevention cost of enterprises is rising, which is reflected in the increase of medical expenses such as vaccines and veterinary drugs on the one hand; On the other hand, enterprises have increased investment in isolation, disinfection, drying, health monitoring and other equipment of the farm, as well as labor costs and capital depreciation. Since 2020, with the impact of COVID-19 epidemic, enterprises have taken more stringent prevention and control measures in personnel mobility, pig allocation and transportation, and to some extent, management costs have also been increased.

2. Cost advantage to build core competitiveness of leading pig enterprises

The pig price continued to decline and the industry accelerated differentiation. Benefiting from the rich profits brought by pig breeding in the past two years, listed pig enterprises grasped the industry growth trend, expanded production capacity on a large scale with strong financial strength, and quickly seized the market share. In the first half of 2021, the sales volume of the top 10 listed pig enterprises increased significantly year on year. However, after the pig price fell, the profit space of pig enterprises was severely compressed. In the context of the rising breeding costs becoming normal, large-scale capital expenditure and capacity expansion of enterprises raised production costs. When the pig price fell below the cost line and losses occurred, the sustainable and healthy operation of enterprises was limited by their capital strength and management level, and the industry would accelerate differentiation. The leading enterprises have shown strong competitiveness in epidemic prevention, cost refined control and capacity expansion by virtue of their advantages in capital, technology and talents. With the continuous release of capacity and the continuous growth of pig marketing scale, the amortization of expenses is driven by the continuous growth of production capacity, and the scale advantage is expected to further emerge.

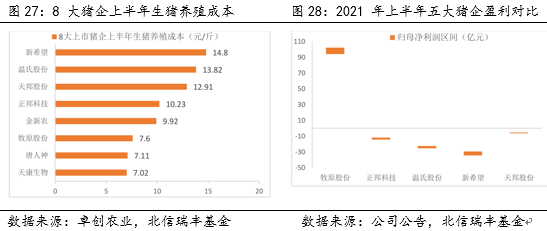

The recovery of pig prices is weak, and cost reduction and efficiency increase will become the main theme of leading enterprises. The future pig price will still hover at the bottom for a long time. Cost reduction and efficiency increase is the primary task facing the industry at present. Excellent cost control capability can build the core competitiveness of enterprises and help enterprises pass the downward cycle. At present, the price of live pigs in the market remains at 15-16 yuan/kg, leading pig enterprises Muyuan Shares The cost of Muyuan has been controlled below 16 yuan/kg, and in the investor research activity on July 26, it said that the cost target of 14 yuan/kg will be achieved in the second half of the year or in stages. Compared with other listed pig enterprises, Muyuan shares have significantly improved the cost. In the first half of the year, under the continuous decline of pig prices, it still achieved a net profit of more than 9 billion yuan (down 5.42% - 12.83% year-on-year), The performance of other pig raising enterprises dropped sharply or turned into losses year on year, especially Zhengbang Technology 、 Wynn shares And New Hope have suffered substantial losses. In the future, in the case of long-term bottom grinding of pig prices, the leading enterprises are expected to obtain periodic excess profits in the downward cycle by reducing costs and improving efficiency. At the same time, after some small and medium-sized farmers accelerate clearing out of the industry due to serious losses and capital chain rupture, they will follow the trend to supplement capacity vacancies and further increase market share, It is suggested to continue to pay attention to the realization degree of cost improvement of leading enterprises.

(About the author: Chief Economist of Beixin Ruifeng Fund)