Opinion Leader | Liu Xiaoshu

Recently, with the release of the 2023 annual report and the first quarter report of 2024, the continued decline of the net interest margin of commercial banks, especially state-owned commercial banks, has aroused widespread concern in the market.

Taking state-owned banks as an example, since 2022, the net interest margin in a single quarter has continued to decline significantly. After falling below 2% for the first time in the first quarter of 2022, it has almost plummeted all the way; By the fourth quarter of 2023, the net interest margin of state-owned banks in a single quarter had fallen below 1.5%. The Measures for the Implementation of Qualified Prudential Assessment (2023 Revision) issued by the self-discipline mechanism of pricing according to market interest rates on April 10, 2023, has broken the 1.8% warning line.

Will the net interest margin continue to decline? When will the decline stop?

To answer this question, we need to find out why the net interest margin continues to decline.

1、 The continuous decline of asset side interest rate is the direct reason for the narrowing of net interest margin

Net interest margin refers to the ratio of net interest income to average interest bearing assets, which is used to measure the profitability of interest bearing assets of banks. It is one of the core efficiency indicators of banks.

Through the disassembly of the net interest margin, it is found that the cost of the liability side is basically stable, and the continuous narrowing of the net interest margin is mainly due to the drag of the asset side.

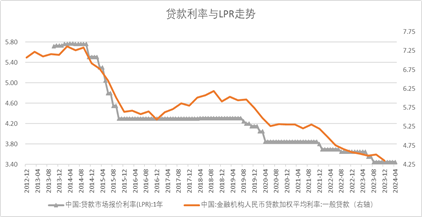

Since 2021, the interest payment rate of listed banks has been characterized by rigidity, and has risen slightly overall except for maintaining basic stability. Therefore, the continuous narrowing of the net interest margin is mainly due to the decline of the asset side interest rate, especially the loan interest rate.

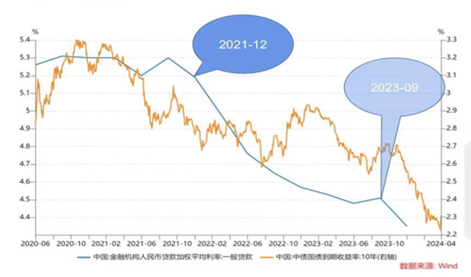

By comparing the trend of weighted average interest rate of general loans, we can find that the loan interest rate has basically remained stable for one and a half years before the end of 2021; After entering 2022, the loan interest rate has dropped sharply, from 5.2% to 4.5% in September 2023, with a decline of 70bp; although the decline of the loan interest rate in the third quarter of 2023 has slightly eased and reversed, after September 2023, the decline of the loan interest rate reappeared and accelerated, with a decline of 16bp in just one quarter. By the end of 2023, the general loan interest rate had dropped to 4.35%.

In addition to the credit interest rate, the interest rate in the financial market also declined significantly. As can be seen from the figure above, the yield curve of 10-year treasury bonds and the downward trend of general loan interest rate showed a certain synchronization: the fluctuation of treasury bond yield declined from December 2021 to September 2023, and the downward trend of treasury bond yield further accelerated from September 2023 to April 2024, with a decline of about 50BP in just a few months.

So what determines the trend of interest rates?

2、 The trend decline of return on capital is the fundamental reason for the narrowing of the current round of net interest margin

We often hear various arguments such as "there is a large space for China to cut interest rates this year", "there is still room for interest rate reduction" and "there is still a large space for monetary policy to cut interest rates and interest rates". This reflects the central bank's determinism of loan interest rates. That is, when the central bank adjusts the LPR, commercial banks will adjust their loan interest rates accordingly according to the monetary policy of the central bank, and then enterprises and individuals will adjust their investment and consumption behavior according to the loan interest rates of commercial banks.

Indeed, the data shows that there is a significant correlation between the central bank's policy interest rate LPR and the weighted average interest rate of general loans. It seems that the central bank has played a huge role in lending rates.

Therefore, in the view of interest rate central bank determinists, the trend of the net interest margin of commercial banks is determined by the central bank. For example, some analysts believe that "the main reason for the decline of interest margin is the multiple cuts of LPR". The special column article "Reasonably view the profit level of China's commercial banks" in the Report on the Implementation of China's Monetary Policy in the Second Quarter of 2023 proposed that commercial banks should maintain reasonable profit and net interest margin to maintain stable operations and prevent financial risks, which is also conducive to enhancing the sustainability of commercial banks in supporting the real economy. It is also believed by the central bank determinists that the future trend of net interest margin depends on the central bank.

In fact, this is all wrong.

It is not the central bank that determines the trend of interest rates, but the return on capital.

The essence of interest rate is the return on capital of the real economy. Schumpeter wrote in the Theory of Business Cycle Cycle that profit is the source of interest, that is, in essence, the rate of return on capital determines the demand of enterprises for loans, and also determines the level of loan interest rates that enterprises can accept. Businessmen will calculate how much expected return can be brought by investment, and how much capital cost is used for investment. Only when it is compared to gain or loss, will they decide whether to invest or not. Therefore, the most important variable supporting the level of lending interest rate is the return on capital.

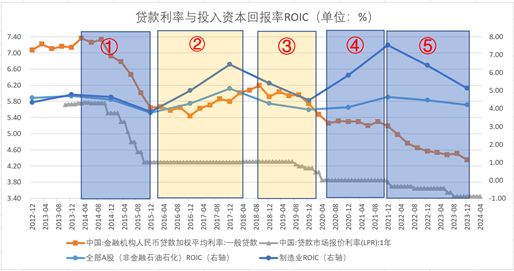

Return on invested capital ROIC is the rate of return earned by all invested capital in production and operation activities, regardless of whether such invested capital is called debt or equity. Compared with ROE, ROIC removes the impact of different financing structures on profitability. When we compare the weighted average interest rate of ROIC and general loans of all A-share non-financial petroleum and petrochemical enterprises, we find that the trend of loan interest rate and ROIC is more consistent than the policy interest rate. This consistency is not only reflected in normal periods, such as the ① - ③ and ⑤ stages in the figure below, especially in the ② and ③ stages. Although the policy interest rate has hardly moved, both the loan interest rate and ROIC have experienced an inverted U-shaped trend; In a special period, such as stage ④, the epidemic period, despite the implementation of the loose monetary policy, the loan interest rate is still strong, almost unchanged during the period. On the surface, the policy interest rate remains unchanged, but in fact, it is inseparable from the fact that ROIC is in the rising period during this period.

So, how to understand the correlation between policy interest rate and loan interest rate? In fact, the central bank is more likely to adjust the cost of capital to the return on capital determined by fundamentals through monetary policy, operating along the economic situation rather than against it. To put it bluntly, it is to adjust the interest rate passively to adapt to the change of return on capital. Of course, as Howard Marx of Oaktree Capital said, the central bank's decision-makers, like you and me, are ordinary people who are not smarter than the market. They also make occasional mistakes in decision-making, such as lagging behind in cutting interest rates or not cutting interest rates when it is time to cut or not raising interest rates when it is time to raise interest rates.

Returning to the problem that the net interest margin of commercial banks has narrowed significantly since 2022, it is still the sharp decline in the return on capital of the real economy that has led to the decline of asset side interest rates, as shown in the figure below. In other words, the decline in the return on capital is the fundamental reason for the narrowing of the current round of net interest margin.

3、 Overproduction intensifies the narrowing of the current round of net interest margin

If the decline in the return on capital led to the decline in interest rates, then overproduction exacerbated the decline in interest rates.

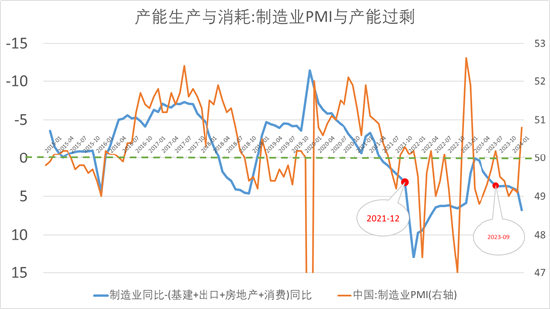

Manufacturing industry represents capacity production, and infrastructure, exports, real estate and consumption represent capacity consumption. Therefore, surplus production, that is, the difference between the growth rate of manufacturing investment and the total growth rate of exports, real estate and infrastructure, to a certain extent, measures the degree of overproduction in the economy. Before 2022, the opposite number of production surplus is highly coordinated with the short cycle trend of the economy represented by new manufacturing PMI orders. It fluctuates around 0, and each cycle span is 3-4 years. Therefore, the cyclical accumulation phase of production surplus meets the public expectations, and the market reaction is relatively calm. However, from the time of entering 2022, the surplus of production will continue to be in a positive range, that is, the surplus of production will continue to accumulate, that is, the problem of "overproduction" will intensify, and the non cyclical accumulation stage of surplus of production will exceed the market expectations, thus causing market shock. It is worth noting that the accumulation speed of production surplus behind the two key nodes of loan interest rate mentioned above, December 2021 and September 2023, is accelerated. The loan interest rate is highly related to the surplus production, which further confirms that the surplus production will aggravate the downward trend of the loan interest rate. China's bond market is mainly an inter-bank market, and the diving effect of credit fund prices is obviously transmitted to market interest rates.

It can be observed that the long-term market interest rate also experienced large fluctuations with the continuous downward trend of the loan interest rate. Since the fourth quarter of 2023, the yield to maturity of 10-year treasury bonds has experienced a significant downward trend. With no obvious adjustment of monetary policy, it is rare for long-term interest rates to decline so sharply in the past decade.

The credit interest rate and market interest rate accelerated to fall under the impact of overproduction, further exacerbating the decline of net interest margin.

4、 Next trend of net interest margin of commercial banks

The improvement of the net interest margin is nothing more than two ends. The asset side improves the yield of interest bearing assets, and the liability side reduces the cost of interest bearing liabilities.

How to get the return on assets? In the short term, it depends on the degree of relief of overproduction, and depends on the degree of consumption of trade in, investment in equipment renewal and other efforts to digest the surplus; Long term depends on the improvement of return on capital, and depends on the cultivation and development progress of new quality productivity in the process of conversion of new and old drivers.

Is it possible to reduce the debt side interest payment rate? In recent years, the cost of debt has remained basically stable and increased slightly. In the short term, there is room for improvement in the cost of liabilities. For example, since the last month, banks have accelerated their withdrawal from the shelves of high interest deposit taking tools, and the three major deposit taking tools, namely, manual interest supplement, call deposits, and medium - and long-term certificates of deposit, have been gradually restricted. In short, debt cost control has become one of the core competitiveness of commercial banks to improve net interest margin.

(The author introduces: Tsinghua University Doctor of Science, Xiamen University Doctor of Economics, Director of China Chief Economist Forum, Chief Economist of Bank of Qingdao)