Opinion Leader Ren Zeping

Introduction

Real estate is the largest pillar industry of the national economy, which is related to economic recovery, livelihood employment and financial risks. We must make a soft landing and avoid a hard landing. China is currently at a critical stage of the transformation of new and old driving forces. If the real estate is stable, the economy will be stable, employment will be stable, and finance will be stable. At present, the relationship between supply and demand in the real estate market has undergone major changes. What is the future situation?

We made Ten predictions of China's real estate:

1. The era of real estate development came to an end, and the era of housing stock dominated. The inflection point of the long cycle of the population of 20-50 year old main house buyers appeared. "Real estate looks at population in the long run, land in the medium run and finance in the short run".

2. Land finance is facing transformation. Land finance accounts for 30% of local financial resources. The problem of local debt is prominent and needs to be resolved urgently, so as to promote the transformation to tax finance and equity finance.

3. The real estate market is facing adjustment and differentiation. Adjustment is to digest the previous high housing prices, high inventory and high leverage. Differentiation is that the market of population flowing into and out of cities will be significantly differentiated.

4. The population migrates to the urban agglomeration in the metropolitan area, and the population in the northeast, northwest, and low-energy cities is facing continuous outflow pressure. In the future, the United States, Japan, and South Korea will have population agglomeration in the second half of urbanization.

5. The soft landing of the real estate market, to a large extent, affects the smooth shifting of China's economic growth. It is crucial for the employment of tens of millions of people, dozens of upstream and downstream industrial chains, and the security of financial credit, which accounts for nearly a quarter of the total, in the next 2-3 years. It is inadvertent that the global economic history shows that real estate is the mother of the cycle, with ten crises and nine real estate crises.

6. It is a general trend to relax restrictive measures such as purchase restrictions, loan restrictions and price restrictions. These are tightening measures introduced during the overheated period of the real estate market. The situation has changed. The real estate market has shifted from preventing overheating to preventing overheating. It is necessary to accelerate the cancellation of restrictive measures and promote the soft landing of the real estate market. We can consider continuing to cut interest rates significantly and establishing a housing bank to purchase developers' inventory for security housing. The top priority is to restart market confidence.

7. The reshuffle of the real estate industry is a general trend. Most of the real estate enterprises will disappear or be merged and restructured. We will increase efforts to support high-quality real estate enterprises to restructure the industry, and the survival of the fittest is an inevitable experience for all industries to develop into a mature stage.

8. Real estate sales and investment will gradually slow down, and it is expected to bottom out in the next two years or so. The future housing market will be mainly supported by the demand for improvement, urban renewal, and affordable housing.

9. The three major projects are the main support for real estate investment in 2024, and the funds are mainly from the central government. It can be considered to set up a housing bank to purchase developers' inventory for security housing. After obtaining funds, developers will give priority to security housing, which will help to prevent uncompleted tailings, waste of land resources and resolve financial risks.

10. Urban agglomeration strategy, linking people with land, financial stability, rent and purchase are the fundamental measures to realize the healthy development of the balance between supply and demand in the real estate market, change the perception, and comply with the economic law.

catalog

1 Prediction 1: The era of real estate development ends and the era of stock comes to an end

2 Forecast II: Land finance will transform to tax finance and equity finance

3 Forecast 3: The real estate market is facing adjustment and differentiation

4 Prediction 4: Population Clustering towards Metropolitan Cities

5 Prediction 5: Soft landing of real estate is related to the smooth shift of China's economy

6 Prediction 6: Relaxing restrictions on purchase, loan and price is the future trend

7 Prediction 7: The shuffle of the real estate industry is the general trend

8 Prediction 8: Real estate sales and investment bottoming is imminent

9 Prediction 9: Three major projects are the main support for real estate investment in 2024

10 Prediction 10: Urban agglomeration strategy, people land linkage, financial stability, rent and purchase simultaneously

text

1 Prediction 1: The era of real estate development ends and the era of stock comes to an end

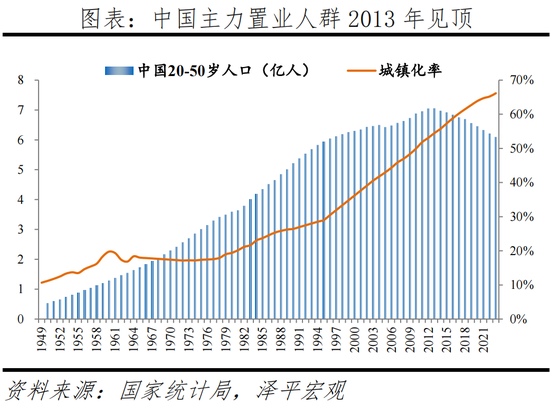

The era of real estate development ended and the era of stock housing dominated. At present, the inflection point of the long cycle of the population of the main 20-50 year old house buyers has emerged, with the urbanization rate reaching 66% and the household ratio exceeding 1.09. "Real estate looks at population in the long run, land in the medium run and finance in the short run".

From the perspective of demand, in terms of population, the number of Chinese 20-50 year old main real estate buyers peaked in 2013. By the end of 2023, the urbanization rate of the permanent population will reach 66.16%, and the urban permanent population will increase by 11.96 million compared with the end of last year. International experience shows that the development of urbanization is similar to a slightly flattened "S-shaped" curve, and China is currently at the end of the decelerating stage of rapid development (30% - 70%). According to our prediction, China's urbanization rate will reach about 78.6% by 2040, corresponding to 1.05 billion urban population, an increase of about 150 million over 2020.

In terms of supply, the number of urban housing units in China will increase from about 31 million to 360 million from 1978 to 2022, and the household ratio will increase from 0.8 to 1.09 。 Compared with 1.17 and 1.16 in the United States and Japan, 1.03 and 1.02 in Germany and the United Kingdom, domestic housing supply is from shortage to overall balance.

In general, the population aged 20-50 in China peaked in 2013, and the peak demand has passed. The housing stock ratio of nearly 1.1 and the construction of a new development model of real estate have accelerated, marking that China's real estate market has bid farewell to the high growth stage.

2 Forecast II: Land finance will transform to tax finance and equity finance

Land finance is facing transformation. Land finance accounts for 30% of local financial resources. The problem of local debt is prominent and needs to be resolved urgently, so as to promote the transformation to tax finance and equity finance.

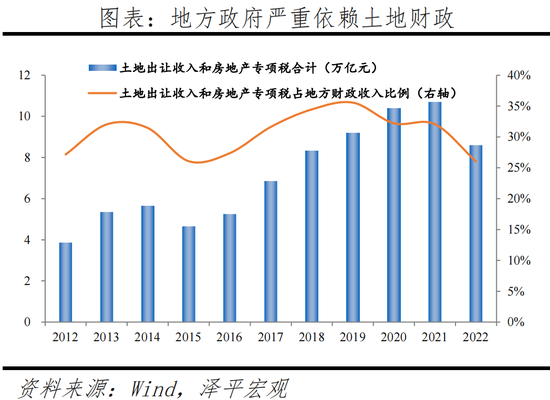

In the design of land finance system, local governments rely on land finance, and the direct taxation of real estate and the income from land transfer contribute significantly. In 2022, the total income from land transfer and special real estate tax will account for 26.0% of the local fiscal revenue, and the land price will account for about 50% of the house price. Affected by the economic downturn cycle in the past two years, the local government's land fiscal space has continued to shrink. In 2023, the revenue from the transfer of state-owned land use rights will be 5.8 trillion yuan, falling below the 6 trillion mark, down 13.2% year on year, 2.9 trillion yuan less than the peak of 8.7 trillion yuan in 2021.

From a macro perspective, In 2022, the total revenue of local governments related to real estate will be 8.6 trillion yuan, including 6.7 trillion yuan from state-owned land transfer fees, and 1.9 trillion yuan from taxes of five real estate specific categories. From 2012 to 2019, the total income from land transfer and special tax on real estate increased from 27.1% to 35.6% of local fiscal revenue, and then decreased to 26.0% in 2022. In 2022, the income from land transfer and special tax on real estate will account for 63.4% of the sales of commercial housing.

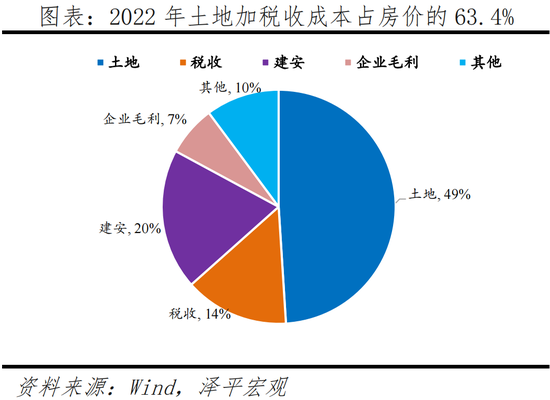

From the perspective of mid city, 11 cities including Beijing, Shanghai, Guangzhou, Shenzhen, Hangzhou and Tianjin were selected for the calculation of house price composition. In 2022, the land cost will account for 49.0% of the house price, the tax cost will account for 14.4%, the construction and installation cost will account for 19.5%, the gross income of enterprises will be 7.0%, and the land cost plus tax cost will account for about 50% of the house price. After regressing the growth rate of housing prices from 2014 to 2022 to the growth rate of land prices, it is found that for every one percentage point increase in land prices, housing prices will increase by 0.2 percentage points, and the rise in land costs has a strong explanatory power for the rise in housing prices.

On March 5, 2024, the Government Work Report deployed the key work in 2024, and mentioned that "we should make overall plans to resolve and stabilize the development of local debt risks, further implement a package of debt programs, properly resolve the risk of existing debt, and strictly prevent the risk of new debt", and "plan a new round of financial and tax system reform". To resolve local implicit debt, we need to deepen reform and handle the relationship between the central and local governments, between the government and the market, and between the government and finance.

Fiscal and tax reform is an inevitable choice in the medium and long term. It is necessary to promote the transformation of land finance to tax finance and equity finance. In the long run, on the one hand, we should promote land finance transformation, strengthen the development of new infrastructure, new energy and other industrial construction, and cultivate local industrial highlands; On the other hand, from the land finance to the equity finance, some local governments have already got rid of the dependence on real estate and built local characteristic industrial clusters. For example, Anhui is accelerating the construction of emerging industry clusters represented by information technology, new energy and new materials, and Changzhou is building a "new energy city" on a large scale, incubating enterprises through equity investment and broadening financial revenue channels.

3 Forecast 3: The real estate market is facing adjustment and differentiation

The real estate market is facing adjustment and differentiation. Adjustment is to digest the previous high housing prices, high inventory and high leverage. Differentiation is that the market of population flowing into and out of cities will be significantly differentiated

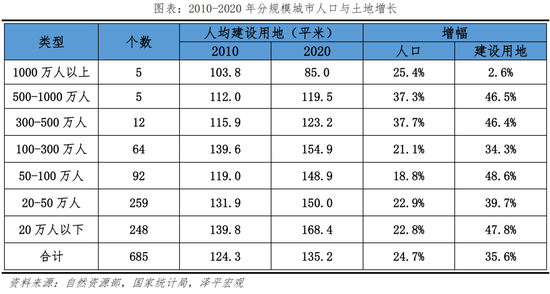

The current situation of China's real estate market needs to be adjusted urgently: the separation of people and land, supply and demand mismatch lead to high prices in the first and second tier, high inventory in the third and fourth tier, and the high leverage and high turnover model of real estate enterprises before the "three red lines" is prominent. The separation of people and land is mainly due to the long-term tendency of "controlling the size of large cities and actively developing small and medium-sized cities" in China's urbanization strategy, which deviates from the trend of population migration. In terms of scale, the urban population of cities with more than 10 million people increased by 25.4% from 2010 to 2020, but the land supply only increased by 2.6%; Urban population under 200000 grew by 22.8%, and land supply increased by 47.8%. In terms of real estate enterprises, compared with international mature real estate enterprises, the leverage ratio of Chinese real estate enterprises is generally high. At the end of 2022, the asset liability ratio of China's real estate industry reached 79.1%, slightly down from 80.7% in 2020, but still at a high level. The average asset liability ratio of American real estate enterprises was 39.1%, which was at a low level.

In recent years, the Central Economic Work Conference and others emphasized that the real estate industry should explore new development models. In the development path to mature real estate market, China's future real estate transformation will focus on the following aspects: 1) Establishment “ People, housing, land and money are the new mechanism of linkage; 2) Improve the basic system of the whole life cycle of housing from development and construction to maintenance and use; 3) We will carry out the construction of "three major projects", including affordable housing, urban village renovation, and public infrastructure for both emergency and emergency use; 4) We will accelerate efforts to solve the housing problems of new citizens, young people, and migrant workers, and work hard to build good houses; 5) Explore the new connotation of the real estate industry, explore the "light and heavy" mode of "development and construction+space services" for real estate enterprises, and build a new track in the field of urban and rural housing construction.

4 Prediction 4: Population Clustering towards Metropolitan Cities

The population migrates to the urban agglomeration in the metropolitan area, and the population in the northeast, northwest, and low-energy cities is facing continuous outflow pressure. In the future, the United States, Japan, and South Korea will have population agglomeration in the second half of urbanization.

From the perspective of international experience, population migration can be divided into two stages: from rural to urban migration, to obvious migration to urban agglomeration in the middle and later stages of urbanization. Internationally, the population migration in the United States has two characteristics: first, at the regional level, it has gathered from the rust 8 states dominated by traditional industries to the west and south coasts dominated by energy, modern manufacturing and modern service industries. Second, at the urban and rural level, the population obviously converges to the metropolitan area in the middle and later stages of urbanization. Japan's population continues to gather in the metropolitan area along with the industry, but in about 1973, it changed from "three poles" of the Tokyo circle, Osaka circle and Nagoya circle to "one pole" of the Tokyo circle. (Please refer to the in-depth report "Zeping Macro", "New Trends of China's Population Migration", "Six Imbalances and Countermeasures in China's Real Estate Market", "China's Urban Talent Attraction Ranking 2023")

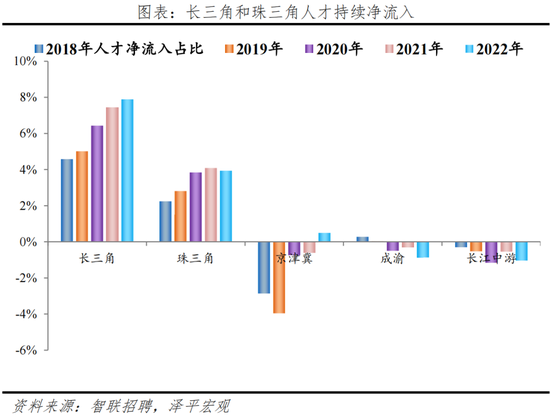

The overall trend of population flow in China is that the population is further clustered in economically developed regions and metropolises, and the differentiation is increasing. The first and second tier population continue to flow in but the growth rate is slowing, and the third and fourth tier cities continue to net outflow. Metropolitan area The population converges to the metropolitan area, but the differentiation is increasing. At the level of urban agglomeration, the population further converges to core cities. It is estimated that in the future, about 80% of China's new urban population will be distributed in 19 urban agglomerations, of which about 60% will be distributed in the Yangtze River Delta, Pearl River Delta and other seven urban agglomerations. As the population continues to differentiate, the difference in real estate investment potential will continue to emerge.

Regional level From 2010 to 2020, the proportion of population in the east increased by 2.15 percentage points, while that in the middle decreased by 0.79 percentage points, that in the west increased by 0.22 percentage points, and that in the northeast decreased by 1.20 percentage points. In 2020, the population in the eastern, central, western and northeastern regions will account for 39.93%, 25.83%, 27.12% and 6.98% respectively.

At the provincial level, the six provinces with shrinking population are all located in the north. People follow the industry and go higher. In 2020, the population of Guangdong and Shandong provinces will exceed 100 million, 126 million and 102 million respectively, accounting for 16.1% of the whole country. Nine provinces including Henan, Jiangsu and Sichuan have a population of 50 million to 100 million, 17 provinces including Yunnan, Jiangxi, Liaoning, Fujian and Shaanxi have a population of 10 million to 50 million, and Ningxia, Qinghai and Tibet have a population of less than 10 million. In the past 10 years, the population of Gansu, Inner Mongolia, Shanxi, Liaoning, Jilin, Heilongjiang and other six provinces has shrunk, reducing 555000, 657000, 796000, 1155000, 3379000 and 6464000 respectively. All of them are located in the north, and people vote with their feet and head to the south. (Please refer to the "Zeping Macro" in-depth report New Trends of Population Migration in China Etc.)

5 Prediction 5: Soft landing of real estate is related to the smooth shift of China's economy

The soft landing of the real estate market, to a large extent, affects the smooth shifting of China's economic growth. It is crucial for the employment of tens of millions of people, dozens of upstream and downstream industrial chains, and the security of financial credit, which accounts for nearly a quarter of the total, in the next 2-3 years. It is inadvertent that the global economic history shows that real estate is the mother of the cycle, with ten crises and nine real estate crises.

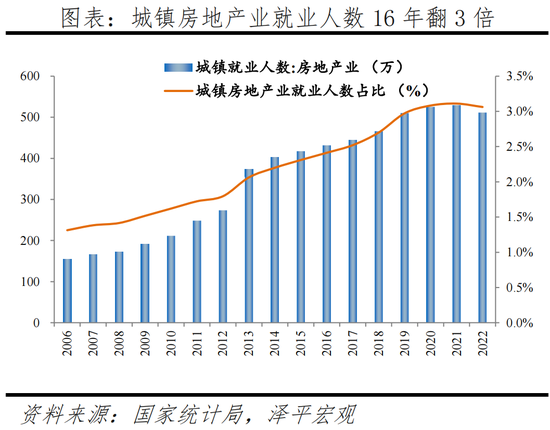

Real estate industry solves the massive employment of China's real economy 。 Although the real estate industry is facing major adjustments in the past two years, the number of property practitioners is growing against the trend. It is estimated that the number of real estate practitioners in China will reach 13 million by 2023, which is three times larger than that in 2004. From 2004 to 2018, the number of employees in China's real estate industry increased from 3.96 million to 12.64 million, and it is estimated that the number of employees in China's real estate industry will reach 13 million by 2023. The rapid development of China's real estate industry in history has provided a large number of employment opportunities for the society. According to the latest fourth national economic census in China, among the real estate practitioners in 2018, 50%, 29%, 13% and 6% of them are property management, real estate development and operation, real estate intermediary services and real estate leasing. We expect that the above proportion will be adjusted to 65%, 17%, 11% and 6% in 2023.

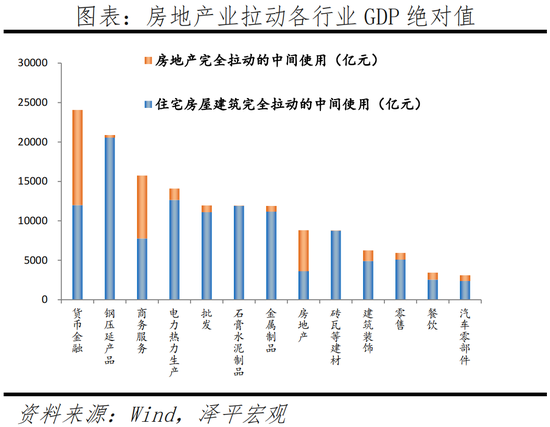

Real estate drives the output value of dozens of upstream and downstream industrial chains. Through investment and consumption, real estate not only directly drives the manufacturing sectors such as building materials, furniture and wholesale related to housing, but also significantly drives the tertiary industries such as finance and business services. According to the latest input-output table of the National Bureau of Statistics for 2020, we estimate that the broad sense of the real estate industry will completely pull the upstream and downstream industrial chains to GDP of 10.0 trillion yuan, and directly pull the upstream and downstream industrial chains to GDP of 2.4 trillion yuan. In terms of industries, the GDP added value of monetary finance, retail, steel calendering and gypsum cement driven by the broad real estate industry ranked first, with 810.7 billion yuan, 423 billion yuan, 352.7 billion yuan and 282 billion yuan respectively. The GDP of ceramic products, building materials such as bricks and tiles, and gypsum cement fully driven by real estate accounted for 51.2%, 50.9%, and 47.1% of the total GDP of the industry.

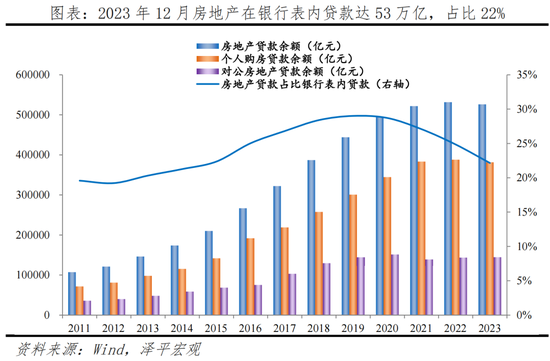

In December 2023, the credit balance of real estate banks will reach 53 trillion, accounting for 22.2% of the stock. It is characterized by large volume, peak proportion and slow growth. The occupation of bank credit by real estate is reflected in public real estate loans and personal housing mortgage loans. Overall, as of December 2023, the balance of bank credit occupied by real estate reached 52.6 trillion, accounting for 22.2% of bank loans, 6.7 percentage points lower than the peak period in 2019. In terms of structure, the loan for public real estate development was 1.44 billion yuan, and the loan for personal housing was 3.81 billion yuan, which peaked in 2018 and 2020 respectively. With the introduction of the policy of "three red lines" and "two concentration of loans", the loan fell back to 6.1% and 16.1% respectively in December 2023.

6 Prediction 6: Relaxing restrictions on purchase, loan and price is the future trend

It is a general trend to relax restrictive measures such as purchase restrictions, loan restrictions and price restrictions. These are tightening measures introduced during the overheated period of the real estate market. The situation has changed. The real estate market has shifted from preventing overheating to preventing supercooling. It is necessary to accelerate the cancellation of restrictive measures and promote the soft landing of the real estate market.

In the context of major changes in the supply and demand relationship of the real estate market in China, the introduction of the optimization policy of the core city property market is very important for stabilizing the property market and the economy. At present, the real estate has entered the stage from "anti overheating" to "anti supercooling". From the perspective of sales, investment and other indicators, the real estate market has been out of tune. There is still much room for urbanization, improvement and urban renewal in the future. The focus is to promote soft landing and launch new models. As the mother of the cycle, real estate stability leads to economic stability.

The current property market performance is weak, so there is no need to worry about the rapid overheating of the market caused by the lifting of purchase restrictions. We can take the opportunity to completely eliminate purchase restrictions, reduce the interest rate of stock housing loans, and release reasonable housing demand. 1) The current market downturn is a good opportunity to lift purchase restrictions. In developed countries, there are no purchase restrictions for domestic residents, which are adjusted through price and tax rather than artificial administrative means. If the primary and secondary markets become active, releasing reasonable rigid demand and rigid demand, the industry can be driven to bottoming out and recovery. Further, it can promote economic growth by making more contributions to land finance and taxes. The elimination of purchase restrictions in an all-round way, in line with the trend of population flowing into the urban agglomeration in the metropolitan area, and the connection between people and land on the ground, can alleviate the historical problem of high housing prices in the first and second tier, and high inventory in the third and fourth tier. 2) We will significantly reduce the interest rate of existing housing loans, including residents and housing enterprises. Monetary policy departments will support banks to reduce debt costs through targeted reserve ratio cuts. Now the interest rate is too high, the pressure of employment and income is too great for residents to bear, and the real estate enterprises can not bear it. The stock interest rate should be significantly reduced. The first set of interest rate was reduced before, and the social response is very good. The second set of interest rate should also be reduced. This is good governance.

7 Prediction 7: The shuffle of the real estate industry is the general trend

The reshuffle of the real estate industry is a general trend. Most of the real estate enterprises will disappear or be merged and restructured. We will increase efforts to support high-quality real estate enterprises to restructure the industry, and the survival of the fittest is an inevitable experience for all industries to develop into a mature stage.

In March 2024, at the press conference of the second session of the 14th National People's Congress, the Ministry of Housing and Urban Rural Development said that "for real estate enterprises that are seriously insolvent and have lost their ability to operate, they should follow the principles of rule of law and marketization, such bankruptcy and reorganization." Under the new model, the real estate industry is being shuffled as a general trend. In the face of challenges such as the rupture of the capital chain of individual real estate enterprises and the adjustment of the real estate market, the Ministry of Housing and Urban Rural Development of China, together with relevant departments, proposed a series of policies and measures. In November 2022, the Association of Dealers proposed the "second arrow" to continue to promote and expand private enterprise bond financing support tools; In the same month, the Central Bank and the China Banking and Insurance Regulatory Commission issued 16 financial articles, providing opportunities for some real estate enterprises to go ashore and restructure their industries.

Since the rising cycle of real estate in 2015, the industry concentration will continue to increase by 2020. In 2020, the sales scale of real estate enterprises ranked top 10, 30, 50 and 100, accounting for 28.0%, 49.2%, 61.4% and 75.1% respectively. After 2021, some of the leading private real estate enterprises have defaulted on their debts and rolled over, and the real estate enterprises that have been out of danger gradually fade out of the top 100 list. The concentration of private real estate enterprises has declined, entering the shuffle stage, and the market share of the leading state-owned enterprises has increased. In addition, improved real estate enterprises comply with the trend of market demand and increase market share by virtue of high-quality products and services. As pointed out by the Minister of Housing and Urban Rural Development at the press conference of the second session of the 14th National People's Congress“ Under the new mode, the current real estate enterprises should see that in the future, they will strive for high quality, new technology and good service. Who can seize the opportunity, transform and develop, build a good house and provide good services for the masses, who can have a market, who can have development, who can have a future. ”

More efforts will be made to support high-quality real estate enterprises to restructure the industry, eliminate risks and eliminate the fittest, which will help maintain the long-term stable and healthy development of the housing market. In the medium and long term, market investors can be optimistic about the future prospects of China's economy. In February 2023, the People's Bank of China issued the Report on the Implementation of China's Monetary Policy in the Fourth Quarter of 2022, pointing out that the reasonable financing needs of the industry should be met, industry restructuring and M&A should be promoted, and the assets and liabilities of high-quality leading real estate enterprises should be improved. Credit enhancement, extension, loan renewal and other tools guarantee the cash flow of San Haosheng, rather than the insolvency of non San Haosheng. The landed real estate enterprises reorganized the whole industry, reaping 15 percentage points of future urbanization, and the rest were the king. The landed real estate enterprises were reorganized and retired from the historical stage. Big shuffle, big clearing, big differentiation, similar to the steel and coal after the supply side reform before.

8 Prediction 8: Real estate sales and investment bottoming is imminent

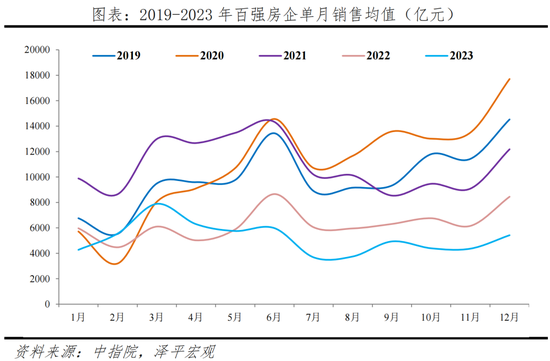

Real estate sales and investment will gradually slow down, and it is expected to bottom out in the next two years or so. The future housing market will be mainly supported by the demand for improvement, urban renewal, and affordable housing.

Comprehensively consider multiple dimensions, such as changes in macroeconomic policies, confidence restoration of real estate enterprises and residents, etc. We expect that under the neutral scenario, the overall supply and demand will still narrow slightly in both directions in 2024, and the bottoming will be completed in about two years. In 2024, the sales area of commercial housing will be - 5.3% year on year, with an absolute sales scale of about 1.06 billion square meters; The development investment in 2024 is restricted by the progress of sales and financing recovery, and is expected to be - 4.5% year-on-year, with a scale of about 11.0 trillion yuan.

In the neutral scenario, we believe that In terms of future macro-economy, economic policies will be slightly increased and slowly relaxed. The interest rate cut and reserve ratio cut in 2024 will be similar to that in 2023. The central government will maintain the same deficit rate. In 2024, the economy will maintain the current prosperity level and the residents' income will gradually stabilize. In terms of the real estate industry, the demand side regulation policy continued to be loose, the residents' willingness to purchase property was repaired, and the real estate price expectation improved slightly. The market recovered in a differentiated way. On the supply side, policies to rescue financing of real estate enterprises, such as financing "white list" and "three not lower than", have been successively implemented. The reasonable financing needs of real estate enterprises with different ownership have been basically met, the disposal of shutdown projects in some cities has been alleviated, the confidence of high-quality real estate enterprises in Sanhao has been restored, and Sanhao's acquisition of land has returned to a positive trend.

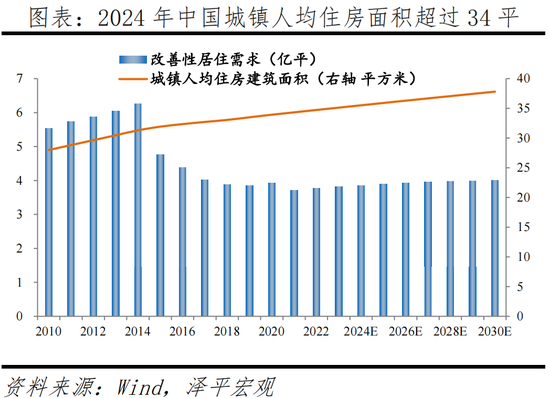

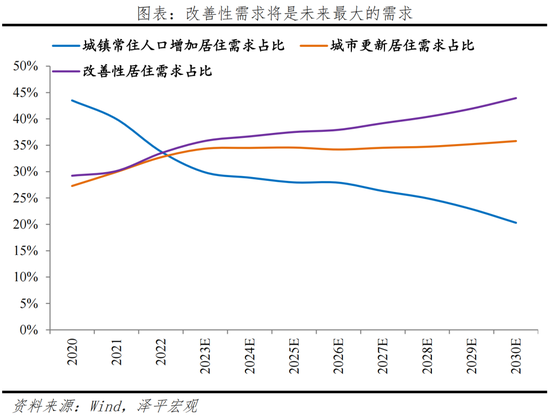

We have tracked and studied China's housing stock report series for six consecutive years, and found that the future demand of China's real estate market has declined, but there is still room for development in the medium and long term, considering the urbanization process, improving demand, urban renewal, etc. According to our estimation, the annual average new urban residential demand from 2024 to 2030 is about 1.00 billion square meters, which is lower than the average new urban residential demand of 1.13 billion square meters from 2011 to 2023, and the total residential demand in China may fall to 910 million square meters in 2030. In 2024, China's annual increase in urban residential demand will be about 1.06 billion square meters. The increase in urban permanent population (excluding changes in administrative divisions, the same later), the improvement of living conditions, and the demand for urban renewal will respectively account for 28.8%, 34.5%, and 36.7% of the total demand. In the next six years, the total amount and proportion of demand for improvement will increase year by year. It is expected that the demand will exceed the demand brought by the growth of urban permanent population and become the largest demand from 2023.

9 Prediction 9: Three major projects are the main support for real estate investment in 2024

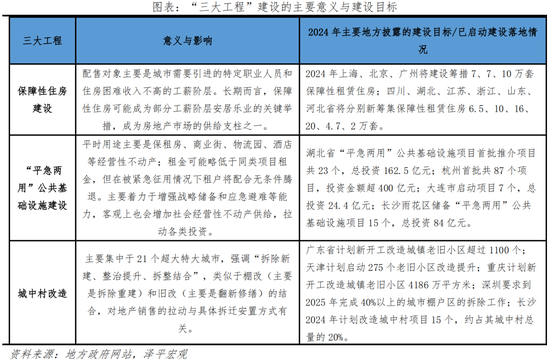

The "three major projects" are the main support for real estate investment in 2024. The capital mainly comes from the central government. We can consider setting up a housing bank to purchase developers' inventory for security housing. After obtaining funds, developers will give priority to building security, which will help prevent uncompleted tail, waste land resources and resolve financial risks.

The construction of "three major projects" is poised to support real estate investment and promote stability. The construction of three major projects, including affordable housing, reconstruction of villages in cities, and public infrastructure for both emergency and emergency use, will further support market demand and investment in 2024. Among them, affordable housing, as one of the "double tracks" parallel to commercial housing in the future, is good news for real estate enterprises whether it is newly built or purchased for the purpose of affordable housing. The room ticket resettlement in coordination with the "urban village reconstruction" can expand the existing housing business, and increase the business space for housing construction and subsequent property management. The infrastructure construction of "flat and emergency" has also increased the demand for a large number of public buildings and urban space services. In cooperation with multi-channel support such as PSL's new landing, special bonds and commercial bank supporting funds, the physical workload of the "three major projects" is expected to increase in 2024, supporting market demand and investment commencement.

Establish a housing bank, which can purchase developers' land and commercial housing inventory at a suitable price through special funds to rent affordable housing, improve people's livelihood, save housing enterprises, and relieve financial pressure. Since the second half of 2021, the property enterprise capital chain has improved slowly. At the same time, the most important thing is to ensure the delivery of buildings. After the developers get the special funds, they are limited to guarantee the delivery of buildings. This can prevent uncompleted housing, and the buyers must not bear the risk of real estate adjustment. The current practice is to let the local government guarantee the delivery of buildings, but the local capacity may be relatively weak due to financial pressure. If the repayment of real estate enterprises picks up, the investment and land acquisition of real estate enterprises resume, the land finance will also resume, and the local debt pressure will be relieved. The purchased inventory of commercial housing and land used for rental housing security housing will help improve people's livelihood. If additional land is used for rental housing, it will lead to a certain degree of waste and more at one stroke.

10 Prediction 10: Urban agglomeration strategy, people land linkage, financial stability, rent and purchase simultaneously

Urban agglomeration strategy, linking people with land, financial stability, rent and purchase are the fundamental measures to realize the healthy development of the balance between supply and demand in the real estate market, change the perception, and comply with the economic law.

We put forward an industry analysis framework: "real estate looks at population in the long term, land in the medium term, and finance in the short term". If a combination of long and short measures is taken, it is expected to promote the soft landing of real estate, avoid hard landing, and contribute to China's economic recovery and employment.

According to our research on the housing system and real estate market in developed economies, combined with the current situation of China's housing system and the characteristics of its development stage, It is suggested to speed up the construction of a new real estate model with the core of urban agglomeration strategy, people land linkage, financial stability, real estate tax and rent purchase.

one )Promote the strategy of urban agglomeration in metropolitan area 。 People follow the industry and go high. The report of the 20th National Congress of the Communist Party of China pointed out that the strategy of coordinated regional development, major regional strategy, main functional area strategy and new urbanization strategy should be implemented in depth.

two )With the increase of permanent population as the core, we will reform the "people land linkage" and optimize the land supply. The new permanent population is linked to the land supply, the balance of land requisition and compensation across provinces is linked to the increase and decrease of urban and rural land use, and the principle of "the inventory reduction cycle is linked to the land supply" is strictly implemented to optimize the current land supply model.

three )Maintain long-term stability of monetary policy and real estate financial policy. Stabilizing the expectations of house buyers and supporting the demand for just needed and improved houses. Standardize the financing purpose of real estate enterprises, support the reasonable financing needs of real estate enterprises, and provide a certain time window for the real estate enterprises with problems to have the opportunity to save themselves.

four )Steadily promote the real estate tax pilot. It is a general trend for real estate tax to replace land finance. In the future, it is necessary to establish a scientific economic model to assess the impact of real estate tax on all parties. At present, the economy is at the bottom stage, and the real estate has not gone out of the predicament, so it does not have the conditions for real estate tax collection.

five )The report of the 20th National Congress of the Communist Party of China stressed that "we should accelerate the establishment of a housing system featuring multi entity supply, multi-channel security and simultaneous rent and purchase". Enriching the supply of commercial housing, rental housing, co ownership housing and other forms of supply, and forming a multi supply pattern of government, developers, rental agencies, long-term rental companies, can speed up the solution of housing difficulties for new citizens and youth groups, and promote real estate enterprises to find new long-term space in the rental business.

(About the author: economist)