Opinion Leader | Guan Tao

In recent days, the exchange rate of Japanese yen, Korean won, Indian rupee and other Asian currencies against the US dollar has hit a new low in recent years or even decades. For a while, the talk of "Asian financial crisis" or "Asian currency defense war" became very popular. However, the sharp devaluation of Asian currencies in this round is mainly due to the re pricing of the Federal Reserve's tightening expectations and the external impact of the strengthening of the dollar index, which is quite different from the Asian financial crisis caused by internal vulnerabilities such as the imbalance of current account payments, the heavy burden of foreign debt, and the inflexible exchange rate mechanism more than 20 years ago. In the context of the continued differentiation of monetary policy with the Federal Reserve, probably the Asian region will only show monetary pressure. In the case of the general increase of exchange rate flexibility, even the currency crisis will not count, let alone the derivative debt and banking crisis.

US PCE inflation rebounded in the first quarter, triggering the withdrawal of market interest rate cut expectations

On April 25, the United States released its first quarter economic data. In the quarter, the real GDP of the United States grew at an annualized rate of 1.6%, much lower than the 2.4% expected by the market, and also lower than 3.4% in the previous quarter, the lowest since the third quarter of 2022, indicating that the growth momentum of the United States economy slowed down. However, the first quarter is usually the trough of the US economic growth in the whole year, and it is too early to draw the conclusion that the US economy is stagnant from the single quarter data. In fact, the real GDP of the United States in the current quarter increased by 2.97% year-on-year, 1.25 percentage points higher than that in the same period of the previous year, and only 0.17 percentage points lower than that in the same period of the previous year (see Figure 1).

What surprised the market even more was the US personal consumption expenditure (PCE) inflation data. In the quarter, the month on month annualized rate of PCE increased by 3.4%, the previous value was 1.8%, the largest increase in a year; The core PCE excluding food and energy increased by 3.7%, the previous value was 2.0% (see Figure 2). This triggered the market's concern about sustained inflation, which, together with the consumer price index (CPI) inflation data for March released on April 10, confirmed the bumpy road of the "last mile" of anti inflation.

After the data was released, the yield of US treasury bonds rose and the stock market was shocked. In the intraday trading, the yield of two-year and 10-year US bonds rose above 5% and 4.7% respectively, closing at 4.96% and 4.70%, 7 and 5 basis points higher than the previous day; The three major indexes of US stocks all fell by more than 1%, and the decline in the tail market converged to less than 1%. The market's expectation of the Federal Reserve's interest rate cut has cooled again. According to the "Federal Reserve Observation Tool" of the Chicago Board of Trade (CME), the probability of the Federal Reserve starting to cut interest rates in September is 45%, the probability of only cutting interest rates once in the year is 40%, and the probability of cutting interest rates twice is 29%. On the same day, the US dollar index recovered part of the decline in Asian trading hours and still closed below 106, 105.56, down 0.23% from the previous day.

On April 26, the US released the PCE inflation data for March. In the same month, PCE increased by 2.7% year on year, the expected value was 2.6%, the previous value was 2.5%, and the month on month growth was 0.3%, which was in line with the expectation and kept the same as the previous value; Core PCE grew 2.8% year on year, with an expected value of 2.7%, the previous value of 2.8%, and a month on month growth of 0.3%, which was in line with the expectation and unchanged. After the release of the data, the US stock market jumped, and the three major indexes closed higher, of which the S&P 500 Index and the Nasdaq Composite Index recovered their losses of the previous day; The yield of two-year US bonds was flat with that of the previous day, and the yield of 10-year US bonds declined by 3 basis points to 4.67%. At the same time, traders increased their bets that the Federal Reserve will cut interest rates for the first time in September, with a probability of 65%, slightly higher than 60% before the data release. However, the market generally believes that inflation in the United States may have bottomed out, which is easy to rise but difficult to fall in the future. On the same day, the dollar index returned to 106 and closed at 106.09, up 0.49% from the previous day.

Asian currencies continue to be under pressure due to the revaluation of the Fed's tightening stance

Last year, the market's expectation of the US economic recession was falsified. Throughout the year, inflation in the United States continued to fall and unemployment rate recovered moderately, but the economic growth jumped from 1.9% to 2.5%, which was a "no landing" state. The market did not wait for the Federal Reserve to cut interest rates. Although the Federal Reserve only raised interest rates four times last year by 100 basis points and has suspended interest rate increases since September 2023, it still maintained its restrictive monetary policy stance.

At the end of last year, the market generally expected a "soft landing" of the US economy in 2024. At the last interest rate meeting, the Federal Reserve also said that it could not see the possibility of economic recession in the United States, suggesting that the interest rate increase was close to the end. In 2024, the growth of the United States economy would slow down, and it would consider cutting interest rates three times a year. However, this year, the market consensus has been hit again. At the beginning of the new year, the market repriced the tightening stance of the Federal Reserve due to the impact of the inflation data in the first three months that continued to exceed expectations. In April (as of April 26, the same below), the yield of two-year and 10-year U.S. bonds rose 37 and 47 basis points respectively from the end of last month, and the dollar index rose 1.5%; Since this year, the yield of two-year and 10-year US bonds has risen 73 and 79 basis points respectively, and the US dollar index has risen 4.6%. Against this background, the Mexican peso, which has been strong since the current round of Fed tightening cycle, fell 3.6% against the US dollar in April (see Figure 3).

Last year, Japan's economy grew 1.9%, 0.9 percentage points faster than the previous year. However, because the Bank of Japan stuck to the control of the yield curve (YCC), the negative interest margin between Japan and the United States further widened, making the yen the only currency among the six basket currencies in the Intercontinental Exchange (ICE) dollar index to fall against the dollar for three consecutive years. In 2021 and 2022, the negative interest margin of 10-year US bond yield increased by 50 and 153 basis points month on month, respectively, and the yen fell 10.3% and 12.2% against the US dollar, respectively. Last year, the negative interest rate spread of the 10-year US bond yield rose 68 basis points month on month, and the yen exchange rate fell 7.0% (see Figure 4). Affected by this, last year, Japan's economy grew and Germany's economy declined, but Japan fell one place in the world economic rankings, and Germany ranked ahead of Japan.

After CPI inflation exceeded the target of 2% for 24 consecutive months, at the interest meeting on March 19 this year, the Bank of Japan finally withdrew from the eight year old era of negative interest rates and abandoned YCC control, but said that the next step of tightening would be prudent, and generally maintain the stance of monetary easing. In the case of high US bond yields and further upward movement driven by the Fed's tightening expectations, the negative interest margin between Japan and the US continues to be at a high level. On the same day, the yen exchange rate fell below 150 again, and since then it has kept breaking the lowest record since 1990 (see Figure 4).

Although officials of the Ministry of Finance and the Central Bank of Japan have recently warned about the depreciation of the yen for many times, even the finance ministers of the United States, Japan and South Korea issued a joint statement during the annual spring meeting of the International Monetary Fund (IMF) and the World Bank on April 17, saying they were worried about the recent depreciation of the Korean won and the yen, and agreed to cooperate closely on the development of the foreign exchange market. However, "just talk without practice", the market did not see the official entry of Japan, and the yen exchange rate continued to decline all the way.

At the interest rate meeting on April 26, the Bank of Japan kept the interest rate unchanged, and predicted that the price risk in fiscal year 2024 would be upward and the growth risk would be downward, and the loose financial environment would continue. After the announcement of the resolution, the market stopped waiting and the yen exchange rate fell below 156, 157 and 158 in one day, closing at 158.33, a new low for 34 years. In April, the daily average 10-year US bond yield negative interest margin was 369 basis points, up 24 basis points month on month (see Figure 4).

Over the same period, other Asian currencies fell one after another, becoming victims of the Federal Reserve's most aggressive tightening cycle in the past 40 years. As of April 26, the exchange rates of the Malaysian ringgit, the Vietnamese rupee and the Indian rupee against the US dollar had all hit new lows since the data was available, the Taiwan New Taiwan Dollar and the Indonesian rupee had respectively hit new lows since May 2016 and April 2020, and the Korean won, the Thai baht and the Philippine peso had all hit new lows since November 2022. Since this year, the exchange rates of Japanese yen, Thai baht, Korean won, Taiwan New Taiwan Dollar, Indonesian rupee, Philippine peso and Malaysian ringgit against the US dollar have fallen by 10.9%, 7.6%, 6.3%, 5.8%, 4.8%, 4.0% and 3.9% respectively (see Figure 5); The Singapore dollar and the yuan fell 3.1% and 2.1% respectively, both hitting new lows since November 2023.

Asian currencies may continue to weaken, but they are not worried about the financial crisis

At the interest rate meeting in November 2022, Federal Reserve Chairman Powell once divided the Fed's tightening into three stages: the first stage, how fast to raise interest rates; In the second stage, how high is the terminal interest rate; In the third stage, how long are the restrictive policy positions. Now it seems that even though the Fed's tightening has gone through the second stage, it has not yet gone out of the third stage.

At the interest meeting on March 20 this year, the Federal Reserve significantly revised the forecast value of US economic growth in 2024 from 1.4% to 2.1%; The IMF changed on April 16 New World In the economic outlook, the forecast value of US economic growth in 2024 will be significantly revised up from 2.1% to 2.7%. Both forecasts are far higher than the Federal Reserve's estimate of 1.8% potential economic growth in the United States.

In view of the rising probability that the US economy will not land, the market gradually turns to the expectation that the Federal Reserve will cut interest rates later and less. At present, the time for the first interest rate cut by the Federal Reserve in the year has been postponed from the beginning of the year to the end of the year, and the number of interest rate cuts throughout the year has also decreased from five or six times to one or two times. On April 16, Powell said that due to the lack of progress in the fall of inflation, it may be appropriate for high interest rates to play a role in a longer period of time. On April 18, New York Federal Reserve Chairman Williams "released the eagle" and will consider raising interest rates if necessary, although this is not a benchmark situation.

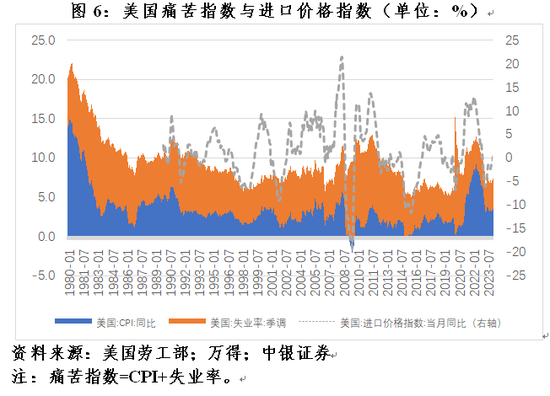

In the case that inflation has become the "obstacle" to the re-election of US President Biden, the US Treasury is not willing to cooperate with other countries to intervene in strengthening the US dollar, and the Federal Reserve will not sacrifice the independence of monetary policy for international economic policy coordination. At present, in the American misery index composed of inflation and unemployment rate, the contribution rate of unemployment rate to the misery index is slightly higher than 50%, far lower than the level of about 80% in the mid-1980s. At that time, the strong US dollar was considered to be the main cause of unemployment in the United States, which led to the Plaza Agreement requiring the revaluation of the exchange rates of the Japanese yen and the German mark. Now, the doubts about the strong US dollar from all walks of life in the United States are not strong. Of course, the topic of the return of mercantilist Trump or his return to competitive devaluation cannot be ruled out. The Federal Reserve itself is not responsible for exchange rate policy. On the contrary, a strong dollar helps reduce import costs. In order to fight inflation, the Federal Reserve may appreciate against the US dollar or be happy to see its success when there is no room to cut interest rates (see Figure 6).

Japan is not so nervous about the devaluation of the yen, but also powerless. The depreciation of the yen has indeed increased the cost of Japan's raw material imports and residents' overseas consumption, but has limited impact on Japan's overall inflation. At present, although the inflation of Japan's CPI and core CPI is higher than 2%, it has risen to around 4% at the highest level, which is less than 3% at present. On the contrary, given Japan's status as the world's largest net overseas creditor, the depreciation of the yen will increase the profits of Japan's overseas investment (see Figure 7). This is an important underlying logic for the decline of the yen and the rise of Japanese stocks. In addition, judging from the experience that the massive intervention at the end of 2022 failed to prevent the continued weakening of the yen, Japan's unilateral intervention has limited effect in the context of the polarization of Japan's and the United States' monetary policies. Other Asian countries and regions are also facing a similar situation that they cannot be independent of the Federal Reserve and can only passively bear the negative spillover effect of their policies.

It is expected that Asian currencies will still face adjustment pressure before the Federal Reserve's monetary policy turns. However, after the Asian financial crisis, the flexibility of exchange rate policies in most Asian economies has increased, and exchange rate fluctuations have become a "shock absorber" to absorb internal and external shocks, instead of passively consuming foreign exchange reserves to stabilize exchange rates. Even under the floating exchange rate arrangement, for example, the yen exchange rate has declined year after year, and the cumulative decline has already exceeded 20%, but no one said that there was a currency crisis in Japan.

On the other hand, the last Asian financial crisis was mainly caused by internal vulnerabilities such as the imbalance of current account payments, the heavy burden of foreign debt, and the rigidity of the exchange rate system. For example, Thailand, the country that started the crisis, had a large long-term current account deficit before the crisis, which was compensated by short-term foreign debt (see Figure 8). As a result, because the ability of foreign exchange reserves to repay short-term foreign debts due in the current year has declined sharply, it was finally forced to abandon the Thai baht after the currency continued to suffer attacks and the foreign exchange reserves were exhausted. This triggered the domino effect of international investors' reassessment of risks in the Asian market, which triggered the Southeast Asian currency crisis and gradually evolved into the Asian financial crisis sweeping the global emerging markets.

At present, Asian economies have generally achieved a basic balance of current account payments, increased exchange rate flexibility, moderate scale of foreign debt, and increased adaptability and tolerance to exchange rate fluctuations. Exchange rate depreciation is unlikely to trigger balance of payments (including currency crisis and debt crisis) and banking crisis (see Figure 8). Of course, it is not ruled out that some low-income, heavily indebted Asian emerging economies may "explode" under the pressure of a strong dollar, or even default on sovereign debt, but this will only be an individual crisis, and is unlikely to trigger the contagion of confidence crisis in Asia.

Currency devaluation is often called "financial crisis" and "currency defense war", reflecting the thinking pattern that appreciation is a good thing and devaluation is a bad thing formed during the period of foreign exchange shortage in the past. In fact, the exchange rate change is a "double-edged sword", with both advantages and disadvantages. Moreover, during the 2022 autumn annual meeting, the IMF once suggested that countries should maintain the flexibility of exchange rate policies to adapt to the differences in monetary policies. However, if the exchange rate changes hinder the transmission of the central bank's monetary policy (that is, affect price stability) or generate a broader range of financial stability risks, it is necessary to implement foreign exchange intervention.

(About the author of this article: Global Chief Economist of BOC Securities)