Opinion leaders | Yu Yongding, Zhang Yi

Recently, the discussion on the direct purchase of treasury bonds by the People's Bank of China in the primary market has again become a hot topic in the market and academia. This kind of discussion is very necessary. As long as the two sides of the debate are not preconceived and listen modestly to disagreeable opinions, they should be able to reach agreement on the basis of logic and facts.

There are three main reasons against the PBOC's direct purchase of government bonds in the primary market: first, under the existing legal framework, the PBOC cannot purchase government bonds in the primary market to finance fiscal deficits, which is the bottom line; Second, the essence of the central bank's direct purchase of government bonds in the primary market is "monetization of fiscal deficits". It is difficult to ensure that the financial authorities will not indulge in borrowing money directly from the central bank in the future. "Monetization of fiscal deficit" will damage the government's credit and eventually lead to inflation out of control; Third, China's macro-economy has not yet reached the point where the central bank needs to directly purchase government bonds in the primary market. China's savings rate is high, and the public's demand for national debt is still strong. The issuance of national debt by conventional methods can provide financing for the fiscal deficit without crowding out effect.

The view of supporting the People's Bank of China to directly purchase government bonds in the primary market is mainly based on two points: first, the current economic pressure is high, and we should attach great importance to the impact of the economic downturn. Due to the huge number of government bonds to be issued (even more than the original plan), conventional government bond financing is very likely to produce crowding out effect, inhibit private investment, and is not conducive to economic growth; Second, in the context of insufficient aggregate demand, monetization of fiscal deficits will not lead to runaway inflation as long as it can exit in time.

This paper does not intend to comprehensively comment on the discussion of fiscal deficit financing, because some of the views have gone beyond the scope of economics, while others are hypothetical questions that can only be answered by practice. This article only talks about the possibility, advantages and disadvantages of different financing methods in China.

Three ways of deficit financing

Deficit financing can be divided into three ways: one is national debt financing, that is, the Ministry of Finance issues national debt to the public through primary market dealers (mainly commercial banks in China); The other is monetary financing (commonly known as "monetization of fiscal deficit"), that is, the Ministry of Finance directly borrows money from the Central Bank; The third is the way that the market is currently buzzing: the Ministry of Finance issues treasury bonds to the public through primary market dealers, while the Central Bank purchases the same amount of treasury bonds from the public through open market operations. The third method is called "Chinese QE" by some scholars. This paper will analyze the different effects of national debt financing and currency financing on the money supply, and explain that quantity breadth is actually money financing, but it is not equal to money financing. For the convenience of analysis, suppose that the government issues 100 units of national debt,

Scenario 1: National debt financing

The Ministry of Finance issues treasury bonds to the public through commercial banks. The Ministry of Finance will increase 100 units of liabilities (national debt) while increasing 100 units of assets (cash or/demand deposits, hereinafter referred to as "central bank deposits"). Under the financing of national debt, the increased central bank deposits in the central bank's liabilities (the Ministry of Finance will first deposit the obtained funds into the special account opened by the central bank - the treasury account) will be offset by the decrease of the currency in circulation or reserves. The central bank's balance sheet will not expand.

If commercial banks use their own funds to purchase national debt. There should be two main possibilities. First, commercial banks reduced their holdings of other assets by 100 units (in the simplest case, cash on hand) and increased their holdings of treasury bonds by 100 units. The asset structure of commercial banks has changed, but the asset scale has not changed. The reduction of other assets by commercial banks means that commercial banks withdraw 100 units of currency from circulation and then inject 100 units of currency back into circulation by purchasing government bonds (first, it becomes the deposit of the Ministry of Finance in the Central Bank). The total amount of money has not changed in the above process.

Second, commercial banks use excess reserves to purchase 100 units of national debt; The asset structure of commercial banks has changed, but the total amount has not changed. The changes in the assets and liabilities of the Ministry of Finance are still as follows: the liabilities increase by 100 units of national debt, and the assets increase by 100 units of central bank deposits. The debt structure of the central bank has changed: 100 units of excess reserves have become 100 units of deposits of the Ministry of Finance. The base currency of the central bank's liabilities remained unchanged. However, the liquidity of excess reserves and central bank deposits is different. We cannot rule out the possibility that this form of treasury bond financing will generate inflationary pressure.

In fact, the vast majority of assets of Chinese commercial banks are loans and advances, followed by financial investment, and then the central bank reserves. The proportion of national debt held by commercial banks in total assets is generally not too high (local special debt may be more). Therefore, the main target of the Chinese government to sell treasury bonds is the general public. As a primary dealer, commercial banks act as underwriters to a large extent when purchasing government bonds. According to the source of residents' funds, treasury bond financing can be divided into two situations: the first situation is that residents use cash to purchase treasury bonds, and the cash held by residents is converted into deposits of the Ministry of Finance in the Central Bank. Commercial banks only charge commissions, and their balance sheets will not change. The total liabilities of the central bank remain unchanged, but the structure has changed: the cash held by the original residents has become the deposits of the Ministry of Finance. Due to the close liquidity of cash and deposits of the Ministry of Finance, there should be no inflationary pressure.

In the second case, residents withdraw deposits from commercial banks to purchase government bonds. In this case, the assets and liabilities of commercial banks will decrease equally. But in other respects, it is no different from the first case.

In a word, national debt financing will not lead to the expansion of the central bank's balance sheet and increase of the base currency, so it will not lead to the increase of the money supply and the rise of inflation pressure. However, the treasury bond financing may lead to the rise of the treasury bond yield and the overall economic yield curve, resulting in "crowding out effect" on non-governmental investment.

Chart 1 Balance sheet changes of the Ministry of Finance and commercial banks under treasury bond financing operation

Data source: produced by the author

Note: For the sake of brevity, the two cases of commercial banks purchasing government bonds on behalf of the public will not be tabulated.

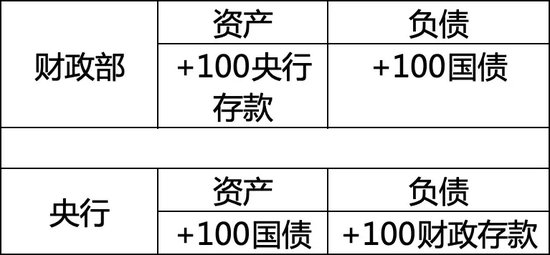

Scenario 2: Monetary financing

The change in the balance sheet of the Ministry of Finance is the same as that in Scenario I. The assets of the central bank increased by 100 units of national debt, and the liabilities increased by 100 units of deposits of the Ministry of Finance - the increase of deposits of the Ministry of Finance in the central bank. The Ministry of Finance will not keep money in the central bank for a long time. Once the finance "uses up" the money, other forms of money in circulation will increase accordingly. The biggest difference between monetary financing and national debt financing is that monetary financing causes the central bank to expand its balance sheet (assets and liabilities increase simultaneously); National debt financing does not lead to the expansion of the central bank. The result of money financing is that the money supply increases as much as the fiscal deficit. Monetary financing will not produce crowding out effect, but it will lead to inflation with a high probability. In principle, there is no need for commercial banks to intervene and the public to participate in the process of monetary financing.

Chart 2 Balance sheet changes of central bank and central bank under monetary financing operation

Data source: produced by the author

Note: The central bank deposit and financial deposit are the same fund.

Scenario 3: National debt financing+open market operation

The standard definition of open market operation is that the central bank buys and sells government securities in the open market. Open market operation itself is a monetary policy tool, and the central bank purchases and sells government bonds in the open market to implement monetary policy. Even if the government does not issue new government bonds, the central bank should conduct open market operations at any time to buy and sell government bonds to achieve the monetary policy goal of maintaining growth and stabilizing prices. Under normal circumstances, the open market operation buys and sells the existing stock of national debt rather than the new flow of national debt, so it has nothing to do with fiscal policy. However, open market operation can also directly cooperate with the government in implementing the expansionary fiscal policy of expanding the deficit.

It should be noted that the open market operation of the People's Bank of China is very different from that of the West in terms of objectives and tools. In particular, there have been a series of changes in the financial instruments bought and sold by the People's Bank of China in the open market operation. For a considerable period of time, it was to sell central bank bills (central bank bills) to hedge the impact of the increase in foreign exchange reserves on the base currency. After 2015, it was mainly the central bank that provided loans to commercial banks through reverse repo (commercial banks provided securities as collateral, which should also include government bonds). Because the role of China's treasury bond trading in open market operation is relatively limited. Therefore, the following discussion on treasury bond financing+open market operation is mainly based on the situation of the United States.

First, treasury bond financing means that the Ministry of Finance sells treasury bonds to primary dealers (mainly commercial banks in China) in the primary market to finance fiscal deficits. The general public can purchase government bonds from primary dealers in the secondary market. National debt financing does not increase the money supply, but may lead to an increase in interest rates. At the same time, the central bank carries out open market operations to buy government bonds in the open market (to simplify the analysis, it is assumed that the central bank buys the same amount of government bonds as the newly added government bonds). The result of treasury bond financing+open market operation is that the total amount of treasury bonds in the assets of commercial banks has not changed: although commercial banks bought 100 units of "new" treasury bonds from the Ministry of Finance, 100 units of "old" treasury bonds were bought by the Central Bank. The 100 units of assets (other creditor's rights or self owned funds, etc.) decreased when commercial banks purchased national bonds were replaced by the 100 units of reserves increased at the central bank. The newly added assets of the central bank are 100 units of national debt purchased from commercial banks, and the newly added liabilities are 100 units of reserves deposited by commercial banks in the central bank.

Under the mode of treasury bond financing+open market operation, the assets and liabilities of commercial banks change, but the total amount remains unchanged. The 100 units of new treasury bonds issued by the Ministry of Finance bypassed commercial banks and were eventually held by the Central Bank. The new assets of the Central Bank are 100 units of national debt, and the new liabilities are 100 units of reserves. The central bank expanded its balance sheet and increased its base currency. The pressure of raising interest rates caused by treasury bond financing by the Ministry of Finance was offset by open market operations. Since we assume that the central bank's open market operation is due to insufficient liquidity in the money market, commercial banks do not have a large amount of excess reserves. Therefore, excess reserves are not included in the assets of commercial banks in Table 3.

Chart 3 Balance sheet changes of various institutions under treasury bond financing+open market operation

Data source: produced by the author

Note: The central bank deposit and financial deposit are the same fund.

According to Bernanke, the monetary financing in case 2 and the "treasury bond financing+open market operation" in case 3 are essentially the same. In his famous speech on helicopter dropping money in 2002, he clearly pointed out that "financing tax reduction through currency creation is equivalent to treasury bond financing and the open market operation of the Federal Reserve in the bond market." However, the author believes that there are still some differences between the two. Monetary financing increases the financial deposits in the central bank's balance sheet. The Ministry of Finance will "spend money" in the shortest possible time. The financial deposit is highly liquid, belonging to M0 or M1. However, as a result of "treasury bond financing+open market operation", the increased liabilities of the central bank are reserves and base currency. The reserve cannot be directly used to purchase goods and services. The increase of reserves means the increase of the loan capacity of commercial banks. However, in the case of insufficient effective demand or deflation, because banks are reluctant to lend and residents and enterprises are reluctant to borrow, the increase of reserves may not immediately lead to the increase of broad money and may not immediately lead to inflation pressure.

It can be seen that the quantitative easing associated with deficit financing is not the same as the open market operation as a pure monetary policy tool. It cannot be said that quantitative easing is just a large-scale open market operation.

The Experience and Lessons of American Leniency

After the subprime crisis broke out, the US Federal Reserve not only bought government bonds, but also bought private financial assets, such as MBS (mortgage-backed loans). At the initial stage, the main purpose of the US Federal Reserve's policy of volume easing was to stabilize the prices of financial assets such as MBS and prevent the collapse of financial asset prices from leading to the bankruptcy of a large number of "systematic" financial institutions. Another important purpose of implementing the policy of volume expansion is to lower the yield of national debt, "rush" funds from the national debt market to the stock market, raise the stock price, stimulate consumption and investment through the wealth effect generated by the rising stock price, and thus stabilize economic growth. As a means of financial financing, quantitative easing occurred later in the subprime crisis. After the financial market has basically stabilized, the main policy goal of the US government has shifted to stimulating economic growth and preventing recession. In 2009, the US fiscal deficit rose from 459 billion US dollars in 2008 to 1.4 trillion US dollars. While the US government is engaged in deficit finance and issuing new treasury bonds, the Federal Reserve has purchased a large number of treasury bonds (including a considerable amount of outstanding treasury bonds) from the open market, effectively curbing the rise of treasury bond yields and eliminating the crowding out effect.

From the experience of the United States, because the banking system is unwilling to lend, the money supply has not increased with the increase of reserves, so the price growth has been significantly lower than the inflation target of 2% in the past decade. When the economy was in a state of deflation, the expansion of the Federal Reserve's balance sheet and the surge of reserves caused by volume easing did not lead to inflation.

On the whole, the Federal Reserve's volume easing policy is very successful. However, the implementation of any policy must seize the opportunity and discretion. In March 2020, due to the outbreak of the epidemic, the sharp decline of the stock market and the "crazy" expansion of the Federal Reserve, the assets of the Federal Reserve rose sharply from about $4 trillion to more than $8 trillion in a few months. At the same time, the US government has also sharply expanded its fiscal deficit. In 2020, the ratio of the US fiscal deficit to GDP (gross domestic product) rose from 4.6% in 2019 to 15%, so that Summers denounced the US government for implementing an unprecedented irresponsible fiscal policy.

After 2021, the inflation rate in the United States has risen all the way, reaching 9.1% in June 2022. Although to a large extent (especially before 2022), the inflation in the United States is caused by supply side shocks such as supply chain disruption caused by the epidemic. But the excessive expansion of the Federal Reserve is also to blame. However, after more than ten years of implementation, how to withdraw from the broad range is still a problem.

China's current choice

In the last section of this article, we repeatedly tried to explain that monetary financing is not a red line that is absolutely impossible to touch, nor is the fiscal deficit absolutely impossible to monetize. We should not place too much trust in textbook rhetoric out of theoretical purity.

Similarly, we should not advocate that China should follow suit just because the United States and other developed countries have monetized monetary financing and fiscal deficits. Everything should be based on the actual situation in China. All policy considerations should be based on the principle of "being not only above, not only academic, but also practical".

As mentioned above, the Chinese government and academia have two main concerns about monetary financing. One is the fear that the loss of fiscal discipline after the monetization of deficits will eventually lead to the loss of credit of the government and the central bank; Second, we are worried that monetary financing may lead to increased inflationary pressure and further expansion of asset price bubbles.

The above concerns are reasonable. During the normal operation of the economy, observing fiscal discipline is conducive to maintaining the credibility of the government and the central bank, and maintaining people's confidence in legal currency. However, in the stage of economic contraction, if the counter cyclical adjustment policy is not adopted to restrain the rapid decline of the economy, the credit of the government and the central bank will be impossible to talk about. At present, "insufficient aggregate demand is a prominent contradiction facing the current economic operation". Although the CPI (Consumer Price Index) in February turned positive year on year, it is still necessary for the government to adopt expansionary fiscal and monetary policies to stimulate growth, without worrying too much about the rise of future inflation.

According to the government work report, in 2024, the budget deficit will be 4.06 trillion yuan, and the broad fiscal deficit will be 11.1 trillion yuan. The central government has planned to issue 4.06 trillion yuan of general treasury bonds and 1 trillion yuan of ultra long-term special treasury bonds; Local governments plan to issue 3.9 trillion yuan of special bonds. For such a large fiscal deficit, the first consideration should be debt financing. In fact, judging from the current situation, the public is quite enthusiastic about purchasing national debt. It seems that there will be no problem that the interest rate of national debt has to be raised (or the yield of national debt has to be raised) in order to issue national debt. However, according to our preliminary estimate, if the consumption growth is not ideal, the growth rate of real estate investment continues to decline significantly, and the growth of net exports is difficult to provide significant support for economic growth, then unless the government reduces the economic growth target of 5%, the government must significantly increase support for infrastructure investment. In this case, the government needs to significantly increase the issuance of government bonds, and the Ministry of Finance and the Central Bank need to strengthen cooperation to try to implement the Chinese style of volume easing.

The main goal of fiscal policy is to make up for the lack of effective demand through the increase of government expenditure. The main direction of fiscal expenditure should be infrastructure investment. Secondly, fiscal expenditure can also be used to improve and increase the provision of public services and promote residents' consumption.

While the fiscal policy is leading the way, the central bank must also increase the expansion of monetary policy. The expansionary monetary policy means to cut interest rates and increase credit to enterprises and residents. By cutting interest rates and increasing credit, monetary authorities can directly stimulate consumption and investment demand. In this way, the pressure on the Ministry of Finance to expand the scale of national debt issuance in order to achieve the 5% growth target will be reduced.

Due to the problem of incentive mechanism, commercial banks have strong motivation to absorb deposits, and the deposit interest rate may be difficult to really reduce further. At present, the net interest margin of banks has fallen to the level of profit and loss equilibrium of about 1.7%, and superimposed on the uncertainty of the Federal Reserve's interest rate cut, although it is necessary for China to further cut interest rates, or even significantly cut interest rates, due to various constraints at home and abroad, the space for the central bank to further reduce policy interest rates has been compressed. At the same time, due to the lack of high-quality loan projects, commercial banks still have the problem of difficult loans. Due to lack of confidence, even if the loan interest rate is further reduced, enterprises are unwilling to borrow money rashly. For example, despite several RRR reductions, the excess reserves of Chinese commercial banks in the central bank remain at a high level. These phenomena show that under the circumstances of quasi deflation and the existence of liquidity traps, monetary policy is difficult to stimulate effective demand and promote economic growth alone.

In order to achieve the GDP growth target of 5%, further increase the expansion of fiscal policy, and issue more government bonds to finance a larger fiscal deficit, which may become the best choice later this year.

Whether the issuance of up to 9 trillion yuan of national bonds and special bonds that have been included in the plan will lead to an increase in the yield of national bonds deserves great attention. Due to concerns about income prospects, residents may maintain a high savings rate, and national debt should be the safest carrier of residents' savings. Medium and long-term treasury bonds should be sold to the general public first. If the central bank of China can actively cooperate with the issuance of national debt, at the same time or reduce the benchmark interest rate, reduce the reserve ratio, and change the incentive mechanism of banks to "pull deposits" in advance, the strong demand of residents for national debt can maintain the yield of national debt at a sufficiently low level, and the government need not worry too much about the sustainability of national debt. As a result of interest rate cuts, the RMB exchange rate may be subject to depreciation pressure. The monetary authorities do not seem to have to worry too much about the devaluation of the RMB. Depreciation is a double-edged sword. In a period of depression and low inflation, depreciation should have more advantages than disadvantages for the overall economy.

It should be noted that the central bank should further reduce all benchmark interest rates and reserve ratio, even if it does not talk about supporting the expansionary fiscal policy of the Ministry of Finance; Further expand the issuance of credit. The expansionary monetary policy not only encourages residents to increase consumption and enterprises to increase investment, but also helps prevent the liquidity of the real estate market from transforming into a debt crisis, and prevent the local debt crisis of real estate developers from transforming into a comprehensive debt crisis; It will help reduce the debt burden of local governments.

In the past, due to the different structure of assets and liabilities, the open market operation of the People's Bank of China was not mainly to buy (or sell out) government bonds, as the Federal Reserve did. For quite some time, the People's Bank of China mainly bought and sold central bank bills to hedge against changes in foreign exchange reserves; After 2015, open market operations will be carried out mainly through reverse repurchase, rediscount, credit lending, provision of structural loans, etc., to adjust the liquidity of the money market, or buy out cash bonds or buy out one-time release and shrink the base currency. It is worth noting that although large state-owned commercial banks generally have abundant funds, they hold a small amount of national debt, which accounts for about 20% of the total assets of banks. On the one hand, China's commercial banks hold relatively few government bonds, and on the other hand, the central bank's creditor's rights to the central government (long-term special government bonds) are also very limited. If China needs to implement quantity leniency, the open market operation mode of the People's Bank of China must be different from that of the United States, and its monetary and capital markets must also be different. If China needs to implement quantitative easing, many technical details need to be studied.

If the issuance of government bonds is too large and there is a sign of oversupply, the government should encourage commercial banks to purchase and hold government bonds. Under normal circumstances, after meeting the demand for credit business, commercial banks will allocate funds according to the net rate of return. Bonds held by banks include corporate bonds, general financial bonds, policy financial bonds, local government bonds and national bonds. Compared with other bonds, the yield of national debt is not high, but its liquidity is good, and it can be used as collateral to borrow short-term funds from the central bank at any time. Commercial banks are active in holding a certain amount of national debt, but that's all.

If further issuance of treasury bonds is needed, the rise in treasury bond yields may be more difficult to avoid. If, despite the cooperation of loose monetary policy, commercial banks are unwilling to buy more government bonds in the face of a sharp increase in new incremental government bonds, the yield curve of government bonds will inevitably move up and inhibit economic growth. At this time, the Ministry of Finance can consider "targeted issuance" or other methods to sell national debt to commercial banks. At the same time, through open market operation, the Central Bank bought the treasury bonds that had completed "one-day tour" in commercial banks. In fact, the implementation of the Chinese type of quantitative easing is that the central bank is assisting the Ministry of Finance in promoting national debt. The open market operation at this time may not be directly related to monetary policy. The basic principle of treasury bond financing+open market operation is to reduce the yield of treasury bonds as much as possible while issuing additional treasury bonds to ensure that the yield of treasury bonds is lower than the nominal interest rate.

Some people may worry that the financing method of treasury bond financing+open market operation will lead to asset price bubbles. The problem is that what we need to worry about now is the second dip of the real estate market. If monetary financing can bring about an improvement in market sentiment, provide necessary liquidity for real estate enterprises, curb asset price overshoot of real estate enterprises and enrich capital of real estate enterprises, then monetary financing is the worst choice. In order to avoid the real estate enterprises from liquidity crisis to debt crisis, which will lead to a systemic financial crisis, as guided by a series of recent policies, the government really needs to work in the assets, liabilities and capital of real estate enterprises. The same is true of local government debt. These crisis prevention and resolution measures all need financial support. In this case, the Chinese style measurement of breadth may become an unavoidable choice. There is no need to say more about the supporting effect of volume expansion on the stock market.

In a word, in an emergency period, some unconventional policies can be considered for counter cyclical adjustment of macro policies, including monetary financing in the form of broad amount. At the same time, it should be noted that monetary financing is not without costs. The worsening inflation in the United States after March 2021 is a proof. Measuring leniency is not so much a panacea as a helpless move. So far, China's first consideration should also be the regular issuance of additional treasury bonds and the open market operation aimed at increasing the liquidity of the money market and reducing the interest rate, but at the same time, it should also make ideological and technical preparations for the introduction of Chinese style quantitative easing once needed. Since we have no experience in implementing quantitative easing in the past, these preparations are also very necessary at present.

Since this year, after several RRR cuts and adjustment of money market interest rates, the short-term interest rate level of the market has declined significantly, but the long-term interest rate has declined relatively little and remained stable in the range of 2.3%. Based on the previous monetary policy practice, it is difficult for short-term liquidity easing to quickly lower the yield level of long-term bonds without adjusting the policy interest rate. If the central bank implements the Chinese style of volume expansion and purchases long-term government bonds in the secondary market, it can lower the long-term yield and effectively reduce the financing cost of the real economy.

The implementation of volume wide operation and the purchase of treasury bonds and other assets from commercial banks will increase the excess reserve on the central bank's balance sheet and expand the size of the base currency. However, as previously analyzed, under the increasing downward pressure on the economy, the role of the increase in the base currency is still difficult to transmit to the real economy. Therefore, we need not worry too much about increasing inflationary pressure for the time being. Of course, we should also be ready to withdraw from the broad range at any time.

Chart 4 Yields of government bonds with different maturities (%)

Data source: Wind database

Due to a series of characteristics of China's economy, for example, China's resident savings rate is still quite high, and the public's demand for national debt is still strong, China may not have reached the point where it needs to implement monetary financing or monetization of fiscal deficits. However, we should not rule out the possibility of adopting extraordinary measures in extraordinary times from the very beginning. "Development is the absolute principle". Only by grasping the core goal of economic growth, formulating economic policies based on China's reality and not being bound by various traditional concepts and dogmas, we will be able to find a way to maintain China's sustained economic growth and solve various contradictions and problems in the process of growth.

Source: Caijing magazine

(The author of this article introduces: member of the academic department of the Chinese Academy of Social Sciences, researcher, doctoral advisor, president of the China World Economic Association)