Opinion Leader | Luo Zhiheng

abstract

For a long time, all sectors of society have regarded the deficit ratio of 3% as the warning line of fiscal discipline, and the deficit ratio of 3% as a sign of fiscal positivity. However, in fact, China's actual deficit rate has already exceeded 3%, and one line or one data can not be a sign of fiscal discipline. Strict fiscal discipline depends on a sound financial management system and incentive accountability system, rather than a data of the desperate need. The EU and the United States, the birthplace of the deficit rate of 3%, also broke 3% during the economic downturn. If the deficit ratio is kept at 3% and the combination of fiscal policies of "deficit control+special debt expansion" is adopted, it will not only restrict the fiscal enthusiasm in the future, but also lead to hidden dangers of special debt and local debt risks, which is not conducive to promoting China's economy from debt and investment driven to innovation and consumption driven, and it is difficult to reflect the enthusiasm of fiscal policies, It is not conducive to stabilizing and boosting market expectations. Therefore, it is necessary to emancipate the mind, play the role of fiscal policy realistically, and let the limited financial funds play a greater role.

China's official deficit rate has been stable at or below 3% for a long time, but major international financial institutions will make amendments to it. From 2020 to 2022, China's official deficit ratio will be 3.6%, 3.2% and 2.8% respectively, while the narrow caliber of IMF estimates will be 9.7%, 6.0% and 7.5% respectively. In fact, after considering the use of carry over balances, budget stability adjustment funds and special debts, the actual deficit rate has indeed exceeded 3%, reaching 10.9%, 6.9% and 7.7% respectively in 2020-2022; After taking into account the debt financing of quasi fiscal activities, the broad fiscal deficit rate is higher. On the one hand, in order to maintain the stability of the official deficit rate, on the other hand, countercyclical adjustment requires a certain amount of fiscal expenditure, so in recent years, the new special debt has expanded year by year. However, the reserve of high-quality projects is insufficient, the project income is gradually reduced, and there are various problems in the use of special bonds, such as project packaging, investment direction non-compliance, illegal misappropriation, and idle funds. The special bonds have gradually evolved into de facto "general bonds", and the repayment of principal and interest of special bonds in some regions is facing certain difficulties, which will increase the risk of local debt.

To sum up, from the perspective of innovating macro-control methods and boosting market confidence, It is necessary to shift from "deficit control+special debt expansion" to "deficit expansion+special debt control", which is conducive to promoting economic growth from debt and investment driven to innovation and consumption driven; From the perspective of optimizing the government debt structure and preventing and resolving risks, It is necessary to increase the proportion of national debt, reduce the proportion of local debt, increase the proportion of general debt, and reduce the proportion of special debt. The deficit ratio will break three when it breaks three, making room for the slowdown or pressure drop of the scale of special debt.

Risk tip: economic recovery is not as expected

text

1、 China's official deficit rate is stable, but the actual deficit rate has already exceeded 3%. International financial institutions have adjusted China's deficit rate

China's stable public finance deficit ratio can no longer reflect the real situation. The actual deficit ratio has already exceeded 3%. Considering the debt financing of quasi fiscal activities, the broad fiscal deficit ratio has even exceeded 10%. The deficit ratio has four dimensions:

First, the official deficit rate, which is stable at or below 3%, only reflects the most narrow sense of the general public budget deficit rate. The deficit rate used by the Ministry of Finance of China only involves the deficit of general public budget in the four budgets, excluding government fund budget, state-owned capital operation budget and social insurance fund budget. The implementation deficit rate of 3% is an accounting result. It is mainly through the budget stability adjustment fund and the balance account carried forward over the years to make the implementation deficit equal to the budget deficit. As a result of adjustment, this indicator has been stable at 3% and below all year round. In 2022, after the transfer of funds from the national finance and the use of the balance carried forward of 2.47 trillion yuan, the final deficit will be 3.37 trillion yuan, 2.8% of the deficit rate, which is equal to the budget deficit and the target deficit rate. This indicator can no longer reflect the actual gap between fiscal revenue and expenditure. Whether the controversial deficit rate should exceed 3% is the indicator.

Second, the actual deficit rate. The actual deficit rate has exceeded 3% for eight consecutive years after considering the use of carry over balances, budget stability adjustment funds and special bonds. The use of the balance carried forward over the years and the budget stability adjustment fund is equivalent to financing the expenditure of the year. The scale of local government special bonds has gradually expanded. The new scale of special bonds in 2022 is equivalent to 108% of the official deficit (national debt+local government general bonds), and it will reach 98% in 2023. In essence, it is still financing for government expenditure. Therefore, the actual deficit is based on the official deficit, plus the used carry over balance, budget stability adjustment fund and special debt. This indicator has exceeded 3% in 2015, reaching 3.6%, and will reach 7.7% in 2022. Compared with the official deficit rate, the actual deficit rate can better reflect the enthusiasm of China's fiscal policy and the policy cycle, showing an obvious negative correlation with GDP growth, and the characteristics of countercyclical adjustment are obvious. The current cognition of "controlling the deficit rate within 3%" is essentially still the balanced budget concept of emphasizing the balance of fiscal revenue and expenditure and controlling the deficit rate, which is not conducive to playing the role of countercyclical regulation, and is also inconsistent with the actual function of finance under the market economy; The perception that "a deficit rate of less than 3% is compliance with fiscal discipline" is also relatively narrow. Fiscal discipline depends not on any line or certain data, but on a sound financial management system and incentive accountability mechanism.

The third is the IMF's global comparable deficit ratio. Since the main content of China's government fund budget is land transfer revenue, in order to facilitate global comparability, the IMF excludes the revenue and expenditure of land transfer, and adds up the revenue and expenditure differences of the four government accounts to build a narrow deficit ratio in IMF caliber, which includes public fiscal deficits, carry forward balances, adjustment funds, revenue and expenditure differences of government funds excluding land transfer revenue, special bonds, and social security funds. From 2020 to 2022, China's deficit ratio will be 9.7%, 6.0% and 7.5% respectively, which is in the middle level of the world. In 2022, China will be higher than the United Kingdom (6.3%), the United States (5.5%), France (4.9%) and Germany (2.6%), but lower than India (9.6%) and Japan (7.8%). Relatively speaking, China's finance is both positive and leaves room for future fiscal sustainability.

Fourth, the IMF's broad deficit ratio. China's broad deficit ratio will reach 16.8% in 2022, which is obviously high. The caliber includes local government financing platforms, government guidance funds, railway bonds, PSL, policy financial bonds, special construction bonds and other quasi financial activities. The broad deficit ratio calculated by IMF in 2020-2022 is 18.4%, 13.8% and 16.8% respectively.

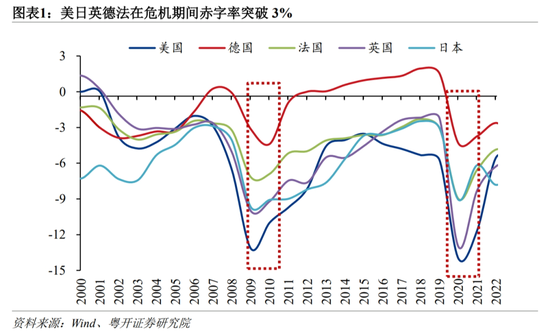

2、 From the perspective of international experience, economies such as Britain, Germany, France and Japan have decisively broken through the 3% constraint during the economic downturn

(1) As the warning line of deficit rate, 3% is derived from the provisions of the Mayo, lacking theoretical and scientific basis. It has been 30 years since then, and the global situation has changed greatly

The so-called deficit rate should not exceed 3%, which is derived from the Maastricht Treaty, which came into force in 1993 in the EU. The threshold for member states to join the EU includes: the deficit rate should be less than 3% and the debt rate should be less than 60%. This fiscal discipline aims to support a strong euro. After Germany's proposal to control the deficit rate at 1% was rejected, countries set a warning line of 3% through political negotiations rather than scientific measurement.

The 1997 Stability and Growth Pact of the EU further defined the rules for fiscal policy coordination, the conditions for implementing excessive fiscal deficits, the punitive measures for excessive deficits, and the establishment of an early warning mechanism to monitor the development of countries' financial conditions, so as to ensure that a basic fiscal balance or a slight surplus will be achieved in the medium term (from 1997 to 2004). The "excessive deficit procedure" requires the offending member states to pay non interest deposits accounting for 0.5% of their GDP. If the fiscal deficit situation does not improve in the next two years, this deposit will be turned into a fine. However, after the establishment of the European Central Bank, the monetary policy of the euro area has been unified, and countries can only rely on a single fiscal policy to regulate their economies. Low growth and high welfare in some countries will inevitably lead to high deficit rates and debts. The deficit rate of 3% has become a soft constraint, and even if member countries violate it, they have failed to implement penalties.

(2) From the perspective of the fiscal practice of the EU and other major countries, 3% is not an absolute red line, and it is normal for the counter cyclical adjustment to exceed 3% in some years

In 1995 and 1996, the deficit ratio of the EU had exceeded 3%, reaching 7.2% and 4.2% respectively. When encountering the international financial crisis, the EU deficit ratio decisively broke through 3% again, 6.7%, 6.4%, 4.5%, 4.3% and 3.3% respectively from 2009 to 2013, all breaking through 3%, in order to achieve the goal of promoting economic recovery as soon as possible. The United States, Japan, Germany, France and Britain all exceeded 3% during the financial crisis, while BRICS countries such as India exceeded 5% all the year round. When encountering the century epidemic, the deficit rates of the United States, Britain, Germany, France and Japan will reach 14.0%, 13.0%, 4.3%, 9.0% and 9.1% respectively in 2020. It can be seen from this that the European and American economies have already abandoned the 3% warning line standard and taken more pragmatic measures. When the economy encounters a major crisis and downward impact, they decisively break through the constraint of the deficit rate of 3%.

3、 If we continue to insist on controlling the deficit ratio at 3% , adopt "deficit control" + The policy combination of expanding special debt will produce a series of consequences

(1) Limited deficit ratio leads to insufficient fiscal enthusiasm, and the effect of fiscal countercyclical adjustment cannot be brought into play

Since the deficit scale is equal to the product of the deficit ratio and nominal GDP, the growth of nominal GDP has its objectivity, so a deficit ratio of about 3% limits the deficit scale. At present, China's economy continues to recover as a whole, but there is still a process to recover to the pre epidemic track. The foundation for recovery is still not solid. The problems of insufficient macro aggregate demand and weak confidence of micro entities have not been fundamentally solved. The size of the constrained deficit is difficult to meet the risks and challenges of the other side, which may lead to constraints in the performance of the government's functions and difficulties in financial operation at all levels. In the context of the downward trend of land transfer income, the phenomenon of local governments' public service supply interruption and wage suspension often occurs in some areas.

(2) Under the premise that the deficit ratio constrains the deficit scale, the special debt has to undertake the important function of countercyclical adjustment through the expansion of special debt, but with the decline of project income, special debt has created a series of problems, becoming a new source of risk

First, there are various problems in the use of special bonds, such as project packaging, investment direction non-compliance, illegal appropriation, and idle funds. In June 2023, the National Audit Office found that 20 regions "packaged" projects into a balance between income and financing scale through false reporting of project income, underestimation of cost, etc., and issued 19.821 billion yuan of special bonds. Five regions have illegally invested 5.003 billion yuan in prohibited fields such as landscape engineering and commercial projects; Illegal appropriation of 15.798 billion yuan in 47 regions; Five regions falsely reported the expenditure progress of 33 special bond projects. By the end of 2022, 6.027 billion yuan had been left unused.

Second, the project income of the current special debt continues to decline, and the risk is gradually rising. Finally, the special debt still needs to be repaid by financial funds, becoming a de facto general debt. In actual use, special debt has problems such as single repayment source, imbalance between financing and income, and generalization of investment orientation, which does not reflect "specialty", and ultimately needs financial funds to cover the bottom, becoming a de facto "general debt". However, because the special debt is not included in the deficit, it is difficult to reflect the real risks of local governments.

Third, the local government expenditure structure and debt structure are gradually showing a trend mismatch. It is necessary to optimize the debt structure, increase the proportion of general debt and reduce the proportion of special debt. On the one hand, as the focus of China's economic development has shifted from efficiency to equity, from the first to the common prosperity, and continued to promote the equalization of basic public services, local government fiscal expenditure has shifted from infrastructure to the livelihood field, while social security, education, health care and other livelihood projects are difficult to generate revenue, which needs to be compensated by issuing local government general bonds. On the other hand, since 2018, under the impact of Sino US trade friction, COVID-19 epidemic and other shocks, the economic downward pressure has been greater, and the new special debt has expanded year by year. From 2019 to 2023, the new special debt quota will be 2.15, 3.75, 3.65, 3.65 and 3.8 trillion yuan respectively. By the end of July 2023, the balance of special debt of local governments had reached 23.16 trillion yuan, far exceeding the balance of general debt of 14.86 trillion yuan. However, at present, the number of high-quality special debt projects has decreased, and some regions have idle funds, which to some extent reflects the problem of excess supply of special debt lines.

Fourth, when the real estate entered the adjustment period, the income from land transfer dropped significantly, and the repayment of principal and interest of special debt became difficult, which became a new risk point. The special debt repayment rate of 25 provinces (the repayment of principal and interest of special debt accounts for more than 20% of the available financial resources of the government fund budget) exceeds 20%, of which the special debt repayment rate of Tianjin and Heilongjiang exceeds 100%, reaching 153.4% and 118.5% respectively. The situation of special debt repayment is severe. At the same time, the current real estate sales and investment are still on the low side. The area of real estate for sale has reached a new high since March 2016 on a year-on-year basis. The ability and willingness of real estate enterprises to acquire land have not recovered significantly, resulting in a 19.8% year-on-year decline in the revenue from the transfer of state-owned land use rights from January to September. The special debt as a numerator has risen, while the revenue of government funds as a denominator has shrunk, The risk of repayment of special debts of local governments further increased.

(3) Not conducive to driving China's economy from debt and investment driven to consumption and innovation driven

As the special debt is mainly used for investment projects, if the fiscal combination of "deficit control+special debt expansion" continues to be implemented, the economic structure will further develop towards investment or even partial ineffective investment. The newly increased scale of special bonds in the current year should be determined by the project reserves, and the number of projects that can achieve self balancing income should match the number of special bonds; When the margin of project income decreases and the number of projects that can balance themselves decreases, the new amount of special debt will naturally reduce the scale. If the special debt quota is also pushed up forcefully, it will only lead to ineffective investment and expand debt risk, and strengthen the debt and investment driven development model.

In the future, China's economy needs to achieve high-quality development, innovation driven and consumption driven. The innovation drive needs to be supported by the general public budget through tax cuts and increased subsidies, which will lead to deficits. Consumption driven needs to solve the problem of residents' consumption ability and willingness, especially in the case of insufficient confidence of residents, the issuance of consumption vouchers to low-income people is conducive to improving consumption ability; The preference of fiscal expenditure structure to public consumption fields such as medical care, education and old-age care is conducive to solving residents' worries and improving residents' consumption willingness.

(4) Not conducive to stabilizing and boosting market expectations and weakening the effect of policies

If we continue to implement the policy combination of "deficit control+special debt expansion", the market will think that the macro-control idea is still the old idea, and the market expectation will be difficult to reverse and weaken the effect of the policy. To fundamentally reverse the weak market expectations, there must be policies that go beyond the conventional and expected ones. Even if the overall scale of financial expansion remains unchanged, the market will see a different way of thinking through "increasing deficit+pressing special debt", and the new way of thinking is more realistic in facing the real deficit and risks, which makes the limited funds play a greater role.

If new ideas are adopted, the local government will also be more active in the implementation, avoiding the dilemma of lack of projects but forced project approval, and the dilemma of accelerating the steady growth of issuing special bonds but facing audit accountability. At that time, we need to take precautions to strengthen the expected guidance in advance, change the narrative system and re understand the deficit.

4、 Suggestions on fiscal policy: from the income policy to the expenditure policy, from stimulating investment to expanding consumption, the deficit ratio will break three if it breaks three

First, we will further improve the efficiency of fiscal policy by focusing on the expenditure policy, supplemented by the income policy. During the economic downturn, the expenditure policy is often better than the income policy. Because the income policy of tax reduction should work through market entities, the transmission chain is long, and it is vulnerable to interference from other factors. Once the confidence of market participants is insufficient, the income side policies such as tax and fee reduction can not stimulate economic growth, but also push up the deficit and debt, and fall into the "tax and fee reduction trap". In the past, China continued to introduce tax cuts, fees, rebates and tax relief, which effectively alleviated the cash flow tension of market entities, improved the anti risk ability of enterprises, but also led to the continuous decline of macro tax burden. The macro tax burden measured by the general public budget revenue/GDP peaked in 2015, falling from 22.1% in 2015 to 16.8% in 2022, 5.3 percentage points lower than the peak in 2015, to the level equivalent to 2005. The macro tax burden measured by tax revenue/GDP peaked in 2013, falling from 18.6% in 2013 to 13.8% in 2022, which is equivalent to the level in 2001. From 2020 to 2022, the macro tax burden decreased by 0.8%, 0.2% and 1.3% respectively, with a rapid decline rate. However, large countries must ensure a certain macro-control capability to cope with various challenges, such as the fiscal transformation of economic and social risks. This requires stabilizing the macro tax burden. It is not appropriate to introduce large-scale tax and fee cuts, and promote tax and fee cuts from the "quantitative model" to the "efficiency effect model".

The second is to shift from focusing on stimulating investment to focusing on expanding investment and consumption, and promote the economy from debt and investment driven to innovation and consumption driven. China's economic development is changing from relying too much on investment and export to relying more on domestic demand, especially consumer demand. Accordingly, fiscal policy and fiscal funds should also shift from stimulating investment to expanding consumption demand. In the short term, we will increase subsidies to unemployed college students and unemployed youth, rural and urban poor groups above the minimum living standard and below the average through cash subsidies, so as to enhance young people's trust in the Party and the government, stabilize people's hearts, and enhance residents' consumption confidence and willingness. In the medium and long term, we will increase residents' income, enhance their consumption capacity, give play to the role of finance in income distribution reform, narrow the gap between rich and poor, and promote structural optimization, increase investment in public services, and promote the national income distribution pattern to favor residents, Promote the change in the structure of fiscal expenditure from material oriented to human capital investment and public consumption oriented.

Third, the realization of expanding consumer demand needs to expand the deficit, especially the central budget deficit. The deficit ratio can exceed 3%, and it is recommended to increase it to more than 4%. The macroeconomic downturn needs to strengthen counter cyclical adjustment and increase the deficit ratio. While increasing the deficit ratio, we can moderately reduce the amount of new special debt to prevent the pressure on special debt repayment from further rising. If the deficit ratio is increased from 3% to 4%, under the current economic size of China, the newly added special debt can be reduced by 1.2 to 1.3 trillion yuan. At the same time, a deficit ratio of more than 3% can send a more positive signal of fiscal policy to the international and domestic markets, which will help boost the confidence of micro entities.

(The author of this article introduces: Vice President of Yuekai Securities Research Institute, Chief Macro Researcher, Certified Public Accountant, Doctor of Finance of China Academy of Financial Sciences, and the third best macroeconomic analyst of New Fortune (team). Research direction: macroeconomic, fiscal theory and policy.)