Article/Sina Financial Opinion Leader Columnist Lian Ping, Deng Zhichao, etc

From January to February 2021, economic growth will continue to recover. Influenced by the base in 2020, many economic data are rare. Through these exaggerated data, we can still observe the basic situation of the current economic operation, and on this basis, we can conduct a rational and prudent analysis of the future, and put forward relevant policy recommendations.

1. The impact of international economy on China's economy cannot be ignored

At present, the world economy is on the way to recovery, global demand is picking up significantly, and the external environment of China's economy is undergoing positive changes. However, the unsynchronized vaccination between China and major economies, the unsynchronized monetary policy, and the deterioration of global financial market expectations caused by high US bond yields may all have an impact on China's economy that cannot be ignored.

two thousand and twenty-one Since, China's vaccination rate has been slower than that of major economies in the world, which may bring about the risk of delayed opening up. According to the data of the British Economist magazine, as of the middle of February, the proportion of vaccinated people in China was only 3%, far lower than 17% in the United States, and also lower than that in Israel, the United Kingdom, the European Union and other economies. The Economist Intelligence Unit predicts that, at the current rate, China's vaccination rate will reach the target of 60% at least by the end of 2022, at least one year later than that of the country with the fastest vaccination rate. If the vaccination rate of major economies in the world reaches the level of group immunity, economies can open up to each other, but China's low vaccination rate is not enough to support opening up, which may inhibit the international cycle of China's economy for a period of time. Since March, the vaccination rate in China has accelerated significantly.

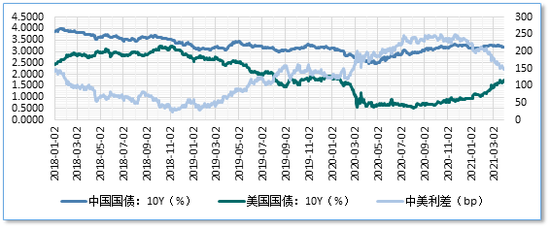

At present, monetary policies at home and abroad are not synchronized. Monetary policies in major economies around the world continue to be implemented in a wide range, and domestic monetary policies are stable and return to normal, thus forming a "capital flow pressure gap" at home and abroad. In the fourth quarter of 2020, China's direct investment surplus was US $56.5 billion, and its securities investment surplus was US $54.2 billion. In the future, external capital will continue to flow into China from direct investment and securities investment. In particular, the capital inflow under securities investment is characterized by short-term, high-frequency and strong impact, which may lead to increased exchange rate fluctuations. The continuous inflow of capital is likely to increase the vulnerability of the financial market. If the reversal of capital flows is triggered at a certain point in the future, financial risks will be triggered. At present, the yield of US Treasuries has increased significantly, and the yield difference between the 10-year treasury bonds of China and the US has narrowed to about 150 BP. With the recovery of the U.S. economy and the implementation of Biden's 1.9 trillion yuan stimulus plan, the U.S. bond yield may be high, or it may be further upward, and the interest rate gap between China and the United States will narrow accordingly. Therefore, it is not ruled out that a certain point may trigger a rapid return of capital under securities investment.

High US bond yields depress global asset valuations, and promote the transmission of financial risk expectations to China. As the issuer of the currency of the world's largest economy, the Federal Reserve has assumed the function of "global central bank" to a certain extent. At present, the implementation of large-scale fiscal stimulus policies and quantitative easing and low interest rate policies in the United States will weaken the stability of the dollar value in the long run, making global investors suspicious of holding dollar assets, especially U.S. bonds, and the demand for U.S. bonds will decline. At the same time, the United States also issued treasury bonds on a large scale, resulting in an oversupply of treasury bonds. The United States has an incentive to increase the yield of treasury bonds to attract investors. In order to control the risk of financial institutions, the Federal Reserve resumed the policy of supplementing leverage ratio, which led commercial banks to sell US bonds periodically, and the yield of US bonds continued to rise. The US bond yield is the pricing basis of global financial assets. The Shanghai Branch of the US bond yield will lower the global asset valuation, forming the expectation of valuation decline and causing financial market turbulence. Under the condition that the openness of China's financial market continues to expand, this expectation of valuation decline may quickly be transmitted to the domestic financial market, thereby reducing risk appetite, triggering pessimistic expectations and bringing about market instability.

Figure: Yields of 10-year treasury bonds in China and the United States

Source: Wind, Zhixin Investment Research Institute

2. Imbalance and emerging problems in economic recovery

From the year-on-year data, the data of January to February 2021 currently released can be roughly divided into two categories according to their relative strength. One is relatively strong, including two aspects: first, the export growth rate is quite high, and the average value of two years is also relatively high; Second, the growth of added value of industries above designated size. It averaged 8.1% in two years. The weak ones are investment and consumption, that is, domestic demand. The two-year average growth rate of fixed asset investment is only 1.7%, and the two-year average growth rate of consumption is 3.2%. Among them, the average investment in manufacturing and infrastructure construction for two years is negative. This means that the current positive growth of investment is mainly driven by real estate investment, and the growth rate of real estate investment will reach 7% in 2020. It can be seen that several components of the growth rate of fixed asset investment are obviously unbalanced. This means that in the future, if the growth of investment in infrastructure and manufacturing cannot be improved, and the growth of real estate investment cannot maintain a relatively stable and rapid growth in the future, there may be downward pressure on the growth of investment.

The growth of industrial added value was very strong, but the growth rate of domestic consumption picked up slowly, and the growth rate of domestic investment was not high, which showed that the world economy had formed a great demand for China's supply. This is probably the main reason for the continuous good performance of industrial added value in the recent period. It can be seen that the two types of strong trend data mainly benefit from the dependence of foreign demand on China's exports.

From the chain comparison operation data, it seems that some fields are weak and unstable. The industrial added value grew month on month, once reaching 1.89% in April 2020, and then continued to decline, reaching 0.69% in February 2021. The month on month growth of investment also continued to slow, reaching 4.5% in March 2020 and 2.43% in February 2021. Consumption is not only weak, but also fluctuates greatly on a month on month basis. Objectively speaking, the fluctuation of consumption growth rate is not surprising, because consumption is the most or the most affected by the epidemic. Consumption was unstable at one stage, mainly due to the impact of external imported cases, and some local outbreaks were rebounding. For example, there were repeated outbreaks in January, and consumption in January showed a negative growth of 1.4% month on month.

At present, there are three emerging issues that need attention. First, the production side seems to be weaker than in previous years. The manufacturing PMI in February was relatively weak compared with previous years. In the nine years from 2011 to 2019, the manufacturing PMI production index in the month of the Spring Festival in eight years was lower than the previous value, with an average decline of 0.86. The manufacturing PMI production index in February 2021 decreased by 1.6 from the previous month, significantly exceeding the average of 0.86. Before the data was released, the market generally expected that the industrial production in February 2021 would be stronger than that in the Spring Festival in previous years due to the "local New Year" initiative, but the actual situation failed. First, the rise in the price of raw materials will somewhat suppress the willingness of small and medium-sized enterprises in the middle and lower reaches to produce. In mid February, the PMI of small and medium-sized enterprises fell 1.8 and 1.1 month on month respectively. Second, the proportion of enterprises reflecting high labor costs and insufficient labor supply in February was 36.2% and 18.3% respectively, both recent highs. The manufacturing PMI employee index fell from 48.4 to 48.1, the lowest level since March 2020. Third, the eve of the New Year coincided with the rebound of the epidemic in many parts of the country, which increased concerns about whether there would be a large-scale rebound in the country and affected the normal development of production activities.

Secondly, domestic demand seems to have slowed down. In February 2021, compared with January, the index of new orders reflecting the domestic demand of the manufacturing industry declined from 52.3 to 51.5, a decrease of 0.8. In the nine years from 2011 to 2019, the manufacturing PMI new order index in the month of the Spring Festival decreased by 0.47 on average compared with the previous value. It can be seen that the decline of the index in February 2021 exceeded the seasonal average level. The import quantity of bulk commodities in February also showed signs of slowing down, or it was related to the recent rise in the price of bulk commodities, more hoarding in the previous months and the recent decline in production demand.

Third, the slowdown in external demand seems to be more obvious. Generally, the sales activities of enterprises in the Spring Festival will decrease, and the PMI external demand index will fall seasonally. In February 2021, the PMI index of new export orders in the manufacturing industry fell from 50.2 to 48.8 below the boom and bust line. In the same period, the index of new export orders of non manufacturing PMI fell from 48.0 to 45.7, returning to the level in the third quarter of last year. Both declines are not small. However, the expectations of manufacturing enterprises are still relatively positive. The expected production activity index of manufacturing export enterprises in February was 60.8, still in a high boom range, indicating that most manufacturing export enterprises are still optimistic about the recent situation. At present, the above three aspects are just a preliminary problem. Whether they can become a trend is still difficult to make a conclusion and needs further observation.

3. The pressure and hidden worries of economic operation cannot be ignored

In view of the improvement of the global epidemic, the economic recovery and the further release of domestic demand, the overall trend of economic operation throughout the year is optimistic, but it is still necessary to carefully see the problems, pressures and hidden worries.

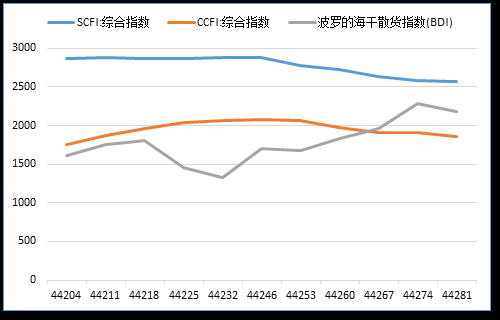

Since the second half of 2020, the strong global demand for Chinese manufacturing products may be transferred or replaced to some extent. It is a highly probable event that the world economy will recover as a whole in the coming quarters. Under the stimulus of fiscal and monetary policies, the economic growth of the United States will show a good performance in the second half of the year or next year. The expansion of demand in the United States will also stimulate the economic recovery of the EU, ASEAN and other important economies. The improvement of the global economy will usually boost China's exports, but in 2020, there is a logical anomaly. In the process of rapid recession of the world economy, China's exports not only did not shrink, but increased significantly, mainly because the overall global demand contracted faster than the supply capacity. At this time, China's comprehensive and powerful industrial system played a role. With the improvement of the epidemic situation and the recovery of global supply capacity, the world's demand for Chinese industrial products may shift or be replaced to some extent. In March 2021, the BDI index reflecting global trade rose significantly, while the SCFI and CCFI indexes reflecting domestic exports declined significantly. This will affect the growth of China's exports in the second half of the year, which may lead to the existence of the abnormal phenomenon that China's exports do not grow synchronously when the world economy recovers as a whole, thus putting some pressure on the manufacturing industry.

Figure: SCFI and CCFI indexes

Source: Wind, Zhixin Investment Research Institute

At present and in the future, manufacturing and export industries are under the pressure of rising costs. First, it is affected by the appreciation of the RMB. The relevant data of the past two decades clearly draw a conclusion that after the appreciation of the RMB reached 8% or more within six months to one year in two or three quarters, China's export growth rate declined, because the appreciation made the cost of China's export products rise significantly. From May 2020 to January 2021, the appreciation of RMB against the US dollar will be about 9%, which will weaken the competitiveness of export enterprises and bring pressure on China's exports after the second half of the year. The second is that the labor cost of manufacturing industry is rising very fast. From the third quarter of 2020 to the beginning of 2021, the labor cost in coastal areas such as the Pearl River Delta and Yangtze River Delta cities has risen significantly. Typical of Ningbo, about 50% of its output value is related to exports. The huge demand of the international market makes it difficult to find a job in the local market. Many business owners have raised the salary standards for recruitment, and many enterprises have increased their wages by 50% - 100%. Wages are rigid, and it is very unlikely to return to the original place once they are pushed up. The labor cost of major coastal export industries has risen significantly, which will bring rising pressure on the cost side of China's exports.

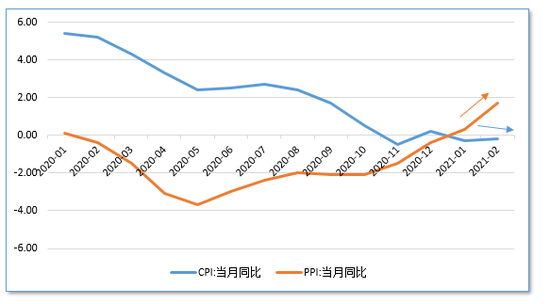

At present, the pressure of imported inflation is increasing, which may squeeze the operation of midstream and downstream industries. This domestic PPI uplink shows typical input characteristics. Since the fourth quarter of 2020, the prices of international bulk commodities represented by oil, copper and other major industrial raw materials have risen significantly. The acceleration of vaccination in major countries and regions, the implementation of Biden's US $1.9 trillion poverty alleviation policy, and the preparation of the subsequent US $3 trillion stimulus policy may push overseas demand into a significant expansion range in the future, which will further strengthen the expectation of international commodity price rise in the short term and continue to push the PPI to reach more than 6% in the second quarter. However, CPI declined slowly due to the downward trend of the pig cycle and the previous base. At present, it has fallen into the negative range, and may rise in the future fluctuations. The annual CPI may hover between 1% and 2%. The expansion of the PPI-CPI inverse scissors difference indicates that inflation transmission in the upstream and downstream industrial chains is not smooth. In the case of weak aggregate demand, the continuous rise of PPI is likely to erode the profits of related enterprises in the middle and downstream of the industrial chain. This situation was manifested during the supply side reform and the implementation of the "three removal, one reduction and one compensation" policy in 2016-2017. In the future, downstream industries may bear considerable operating pressure, and most of them are private economies and small and medium-sized enterprises, which should be paid attention to.

Figure: CPI and PPI trend

Source: Wind, Zhixin Investment Research Institute

Under the new policy environment, real estate may be under downward pressure. Since last year, real estate has been the main positive factor in stimulating fixed asset investment. However, in 2021, real estate investment may slow down due to a series of factors. Demand side policies such as purchase restriction, loan restriction and price restriction, which are further implemented in first tier cities and some second tier cities, will affect the enthusiasm of future real estate enterprise investment. Under the policy framework of three red lines and mortgage loan regulation, real estate financing will also slow down in the future. Although the relevant policies introduced since 2020 will not fundamentally change the situation of real estate finance, they will have some impact more or less. This will slow down the growth of bank real estate development loans, but is unlikely to significantly shrink the real estate credit financing. At present, developers' loans account for only 6% - 7% of the total bank loans. The growth rate of mortgage loans has risen rapidly in the past few years. Through prudential supervision in the past two years, the growth rate has also declined significantly, and is moving towards a relatively stable and reasonable growth. Controlled demand and financial slowdown will bring some pressure on the growth of real estate investment in 2021, which may be slightly lower than that in 2020. Under the joint force of the comprehensive demand control policy with significantly increased efforts, the market transaction may also slow down in the next stage, so that the role in stimulating consumption will be relatively weaker than in 2020. If the growth rate of real estate investment and transaction slows down in 2021, domestic demand will bear some pressure. As mentioned above, real estate will be an important support for domestic demand growth in 2020.

4. Macro policies highlight two themes

Since the second quarter of 2020, market institutions have generally been conservative in predicting external demand, but the actual data is much better than the predicted value; Market institutions tend to be optimistic in predicting domestic demand, while the actual data is weaker than the predicted value. This phenomenon tells us from another point of view that the good recovery of the current economic operation is largely related to the improvement of external demand. As mentioned above, if supply substitution and cost rise and other factors play a role at the same time, China's economy may face the uncertainty and instability of the new external environment after the second quarter of 2021. Although the investment in manufacturing industry will recover quickly, and the investment in infrastructure and consumption will also grow steadily, there may still be some pressure and hidden worries on domestic demand. In the future, macro policies will still seek a balance between preventing and controlling risks and maintaining economic recovery, but promoting a smooth economic recovery and consolidating it is still the primary task. Therefore, the macro policy in 2021 should highlight the two themes of return to normality and moderation and neutrality. The so-called return to normality means basically taking back the special policies in the anti epidemic stage and implementing the macro policies based on normal operation. However, conservatism and neutrality require that macro policies should not be tightened quickly and make sharp turns in the process of returning to normality, and that policy exits should have a slope to avoid obvious fluctuations in economic operation. The arrangement of deficit ratio and local government debt issuance in the 2021 government work report not only reflects the intention of returning to normal macro policies, but also reflects the relatively positive policy orientation. In order to effectively boost domestic demand and improve financial supply, the 2021 policy can actively act in the fields of real estate, consumption, tax and monetary finance, and continue to promote economic recovery growth while maintaining controllable financial risks.

Consumption is the key to expanding domestic demand and stabilizing economic growth. At present and during the 14th Five Year Plan period, we should take a multi pronged approach to improve residents' willingness and ability to consume, make the growth of residents' consumption faster than the growth of output and other demands, and increase the proportion of consumption in total demand. To achieve this goal, the key is to improve the income distribution system and raise the income level of low - and middle-income groups. We should adhere to the principle of distribution according to work and the coexistence of multiple distribution methods. We should pay equal attention to the adjustment of primary distribution and redistribution, and accelerate the formation of an olive shaped income distribution pattern with low - and middle-income groups as the main body. Increase the remuneration of workers, especially front-line workers, and increase the proportion of labor remuneration in the initial distribution. We will improve the mechanism for evaluating and distributing the contributions of market elements, and pay more attention to the market value of knowledge, technology, management and other elements. Enrich residents' investment and wealth management products, expand residents' investment channels and increase their property income. We will improve the redistribution mechanism. We will improve the individual income tax system, which combines comprehensive and classified income tax systems, and rationally adjust the distribution relationship between urban and rural areas, regions, and different groups. We will improve the general transfer payment system and increase efforts to ensure the basic livelihood of the people. We will improve the old-age insurance system and promote long-term balance of basic old-age insurance funds. We will remove the institutional and institutional barriers that affect the income growth of key groups such as new professional farmers and professional and technical personnel, and raise the minimum wage. We will further increase tax and fee reductions, reduce unnecessary costs in circulation, and reduce the burden of consumption. We will accelerate the improvement of the soft and hard environment for consumption, constantly innovate new consumption models and formats, and continue to promote consumption upgrading.

At present and in the future, the smooth operation of the real estate market is crucial. In terms of real estate policy, firstly, it is suggested to increase the land supply in some second tier cities, especially those second tier cities where the house price rises rapidly and the population flows into them more net, which can also be included in the policy scope to solve the housing problem in "big cities". By the first 10 weeks of 2021, the land supply of key second tier cities has nearly halved compared with the same period last year, while Chengdu has released only 2% of the land supply area in the same period last year, and Ningbo has only one-third of the land supply area in the same period last year, which is an important reason for the rapid growth of house prices in these regions. Second, it is suggested that the pace of the decline of housing credit growth should be gentle and should not be tightened quickly. Considering that the overheated real estate in some parts of China is a structural problem, the real estate credit policy should be more targeted and increase the control of real estate loans in first tier cities and key second tier cities. Especially in areas like Guangzhou and Shenzhen where the housing loan growth rate is fast, we can strengthen the control of local branches of commercial banks that "step on the red line" in combination with the housing loan concentration system of financial institutions, moderately delay the speed of credit delivery of housing loans, guide the growth rate of housing loans to be slightly lower than the speed of the expansion of local total credit, and alleviate the problem of local overheating of real estate. Third, it is suggested to properly expand the financing channels for real estate enterprises. In order to increase housing supply in big cities and stabilize housing prices, it is recommended to increase financing channels for long-term stable real estate enterprises, including direct and indirect financing channels, such as equity financing, bond financing, small and medium-sized bank credit, and trust funds (REITs) And other ways to alleviate the problem that the reasonable financing needs of some real estate enterprises are difficult to implement, so as to increase the supply of housing market in the first and second tier cities.

Reform the relevant tax system and improve the willingness and ability of residents to consume. First, it is suggested to raise the threshold of individual income tax and special additional deduction standards. As mentioned in the 2021 government work report, the VAT threshold for small-scale taxpayers will be increased from 100000 yuan to 150000 yuan per month, and the income tax on the part of small and micro enterprises and individual businesses with annual taxable income less than 1 million yuan will be halved on the basis of the current preferential policies. Referring to the corresponding standards, it may be appropriate to increase the threshold of individual income tax by 1000 yuan to 6000 yuan. Special additional deductions for children's education, housing loan interest, and support for parents can also be appropriately increased according to economic growth and price factors. In comprehensive consideration, the sum of individual income tax threshold and special additional deduction standard will be increased by about 2000 yuan. This may help to improve the consumption willingness and ability of low-income groups. Second, it is suggested to refer to foreign experience and implement the policy of targeted deduction of individual income tax consumption for taxpayers who apply higher marginal tax rates. The State Administration of Taxation can formulate a set of consumption oriented deduction standards according to the personal income tax rate table, and make a quota tax return for taxpayers who apply a higher level marginal tax rate (such as 30% and above). The amount of return is determined according to the marginal tax rate. Taxpayers normally pay individual income tax in accordance with the current tax system. After the end of a natural year, they can handle the corresponding tax refund with the invoices related to consumption in that year. This will help stimulate the marginal propensity to consume of high-income people.

In order to balance the monetary policy between supporting economic growth and preventing and controlling risks, it is suggested that the prudent monetary policy should effectively implement the neutral tone. At present, the overall economy is still in the process of recovery, and the flexibility and rationality of monetary policy are crucial. It is necessary to keep the growth of money supply and social financing scale basically matching the nominal economic growth. Under the condition of maintaining reasonable and sufficient liquidity, the macro leverage ratio needs to maintain a basic stability. It is necessary to gradually return financing and liquidity operation to normal, but also to avoid a decline in financing growth. Social finance, credit and M2 can return to a level slightly higher than the average in recent years. For example, the growth rate of multiple loan balances of financial institutions can run in the range of 12.5% - 13%, the growth rate of social financing scale stock can return to the range of 11% - 12%, and the growth rate of M2 will return to the range of 8% - 9%. The interest rate of the money market remained basically stable, and the financing interest rate of the real economy continued to decrease slightly under the stable level of LPR.

It is suggested to take active and effective measures to stabilize the expectations of monetary and financial policies. At present, China's financial market is highly sensitive to monetary and financial policies, and over interpretation or even misreading of policy information is widespread. A slight disturbance may bring about the "instant face change" reversal of market operation. Under the background of unclear policy intentions and low information transparency, market players often follow their own thinking of "seeking advantages and avoiding disadvantages" to "figure out" policy intentions, and then choose corresponding behaviors. However, there is often a persistent expectation gap between "speculation" and reality, which will lead to constant volatility of the market. Market entities often fail to interpret policy information in accordance with the direction expected by the monetary authority, and the vulnerability of the financial market and its sensitivity to policy information also increase significantly. It is suggested to first clarify the monetary policy framework and communicate with the market in a timely manner; You can try to make it clear that a certain policy can be adopted when the quantitative indicators of a certain goal reach a certain range, or under what circumstances a certain policy will be implemented. This can give a clear policy signal to the market, thus helping to stabilize market expectations. The frequency of policy communication can be higher, but different communication subjects facing the market should pay attention to maintaining the consistency of policy expression.

Participants:

Lian Ping Zhixin Chief Economist of Investment and President of Research Institute

Deng Zhichao, Secretary General

Luo Huanjie, Senior Researcher

Ma Hong, Senior Researcher

Wang Hao, Senior Researcher

Researcher Dong Chengxi

(The author of this article introduces: Chief Economist and Dean of the Research Institute of Zhixin Investment, Honorary Director of the Department of Economics and Management of East China Normal University, Doctor, Professor, Doctoral Supervisor, enjoying special government subsidies from the State Council.)