Article/Shu Shi, columnist of Sina Financial Opinion Leader (WeChat official account kopleader)

Some real estate agents reported that in the past month, rents in both commercial buildings and residential rental markets have stagnated or even decreased to varying degrees. Perhaps this is another sign that the property market has intensified its downward trend.

The author once wrote in August this year that Hong Kong real estate is gradually entering a sensitive moment. On the one hand, the unit price of buildings has repeatedly hit new highs, and on the other hand, the bargaining space of second-hand property market has gradually increased, with frequent large price reductions and unloading; What's more, the transaction price in some areas has begun to be lower than the bank's valuation, reflecting that the owners are willing to sell the property at a lower price than the market price.

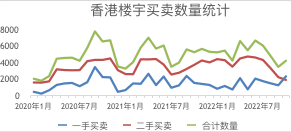

But in less than three months, the real estate situation in Hong Kong has changed from "sensitive" to "critical". According to the economic report of the third quarter of 2018 released by the Hong Kong government, the transaction volume of the residential property market has dropped from 18900 in the second quarter by about 24% to 14413 in the third quarter, of which the transaction volume of second-hand buildings has dropped from 13933 in the last quarter to 9918.

Further comparison with the data of the Rating and Valuation Department shows that the number of building transactions in October 2018 has dropped by 58% compared with May 2018, while the monthly transaction amount has dropped by 56%!

From the perspective of unofficial indicators, the Centa City Leading Index (CCL), which reflects the trend of second-hand property prices in Hong Kong, recently reported 180.4 points, down 1.28% weekly, the largest weekly decline since March 2016 (two and a half years). The latest index reflects the situation from October 22 to 28, which is also the fourth week after the interest rate hike of local banks in Hong Kong. So far, the CCL index has fallen for seven consecutive weeks, falling 3.3% in total. In particular, in the past three weeks, the eight sub indexes of CCL have fallen twice, which shows that the decline of second-hand property prices has turned sharply.

In just a few months, what is the reason for the sharp changes in Hong Kong's real estate market? From all aspects of analysis, Hong Kong real estate is currently facing the following danger signals:

First, Hong Kong's macro-economy is slowing down gradually. According to the statistics released by the Hong Kong SAR government in mid November, the GDP in the third quarter of 2018 grew by 2.9% on an annual basis, further slowing down compared with 3.5% in the second quarter. The annual economic growth forecast was adjusted to 3.2% from the estimated 3-4% in the previous quarter.

The main reason for the economic slowdown is the impact of trade frictions. Ou Xixiong, an economic adviser to the Hong Kong government, pointed out that the impact of trade frictions on Hong Kong's economy has gradually emerged. If trade frictions continue to deteriorate, they will have a greater indirect impact on Hong Kong's financial stability and trade climate. He believes that it is difficult to predict whether Hong Kong's economic growth in the fourth quarter will continue to be affected by the above factors.

According to Ou Xixiong's explanation, the first round of tariff increase measures only affected 1.4% of Hong Kong's exports, so the overall export performance in the third quarter was still good. However, after the United States announced in September that it would impose additional tariffs on Chinese goods worth 200 billion dollars, Hong Kong's export performance in the fourth quarter had been affected. If the tax rate increased to 25% in 2019, it would have a greater impact on exports. On the other hand, the inflation pressure in Hong Kong is rising continuously. The Hong Kong government has raised its basic inflation forecast for the whole year from 2.5% to 2.7%.

In the market, many market analysts have lowered Hong Kong's macroeconomic forecasts. ING Bank lowered its economic forecast for Hong Kong for the second time this year, lowering the GDP of the fourth quarter from 2.8% to 2.2%, and the annual forecast from 3.6% to 3.3%.

If the macro-economy continues to slow down and inflation continues to rise, it will further erode private consumption capacity, weaken the wealth effect and affect the willingness of citizens to invest in real estate.

Secondly, the volatility of Hong Kong's capital market has increased, affecting consumer sentiment. According to the analysis of the Hong Kong government, the fluctuation of the financial market and the significant decline of Hong Kong shares since the second quarter will further hit consumption.

After the stock market goes down, Hong Kong's housing and parking prices usually face a decline, which has been confirmed many times in past experience. According to some brokers, when the property price rises, many owners will carry out two or even three click financing for cash out, and some of the funds will be invested in the stock market, and once the stock market falls a lot, these owners will have to consider buying houses as soon as possible.

On the other hand, nearly half of Hong Kong people are engaged in financial related industries. If the stock market does not work, unemployment may soon come. In this case, the transactions of buying buildings and parking spaces will certainly decrease. Just imagine, who would be interested in buying a house to collect rent or buying a car as a substitute when their jobs are going to be lost? Don't buy a car. Taking the subway is more physical; As for the purchase of a house, we should put it aside first - in case of unemployment, we will face the risk of mortgage foreclosure.

Third, and the most important signal is that recently the owner's bidding has stopped forging ahead, and the market has frequently heard cases of price cuts to clinch deals. In the Taikoo City area of Lanchou House Estate on Hong Kong Island, some real estate agents disclosed that many owners of second-hand buildings began to voluntarily reduce prices by 5% - 20% in order to get funds to change houses as soon as possible. After the financial tsunami in 2008, the maximum decline of residential buildings in Taikoo City was about 20%.

A real estate agent of Great Wall Property believes that this is probably only the first wave, mainly due to the selling of "house changing customers". For such owners, the property they originally held has exceeded the time limit for paying "additional stamp tax", so the price reduction may be slightly larger, in order to sell as soon as possible, so that they can enter the market at this time to buy larger houses.

so-called "Additional stamp duty" It is an additional tax levied by the Hong Kong government on second-hand building transactions. It mainly refers to the ad valorem tax of 10%~20% for the property held within 3 years. The additional stamp duty does not indicate whether the seller or the buyer should bear it, but in the seller's market, it is usually borne by the buyer.

In the past, the price of second-hand buildings in Hong Kong remained high, and the "extra stamp duty" was one of the main reasons. Many second-hand owners need to face a higher amount of potential "extra stamp tax" if they want to buy a larger house after selling the old building. When the property price goes down, if the price decline can make up for the amount of the additional stamp tax, many people are willing to change their houses at this time. For example, if the house he has long admired suddenly dropped by 20%, then the house changers would rather drop their original house by 20% to cash in as soon as possible to buy the house they intend to replace. In fact, there is no place economically uneconomical, but they have changed to a more pleasant house.

When this wave of house changes ends, if the house price continues to decline, it means that the property market has entered a stage of deep adjustment.

Next, let's see if there will be a deep adjustment in Hong Kong's property market in 1997?

Although many regions in Hong Kong have reported deals with a decline of up to 20%, the CCL index has not seen a significant decline (although it has repeatedly shown signs of weakness). Therefore, many property investors are thinking that the recent 20% slump is a case, or is it likely to become a thunderstorm sweeping the Hong Kong real estate market?

Most real estate investors still believe that the situation has not deteriorated to the stage that needs deep adjustment. The reason is that the Hong Kong government has passed many stamp duty measures before, and the HKMA has been tightening the mortgage loan ratio, so the liquidity of the real estate in Hong Kong is actually quite weak. When liquidity is seriously insufficient, transaction prices tend to rise and fall sharply. If the Hong Kong government believes that the property market is in danger of major adjustment and gradually loosens the stamp duty, and the HKMA also gradually loosens the bank mortgage percentage limit after the property price declines, it may provide liquidity support for the property market, so that there will be no abnormal fluctuations in prices.

However, the above analysis ignores several important factors:

First of all, the CCL index is lagging behind and not representative enough. Hong Kong's property market transactions usually require the signing of temporary contracts, which usually take two weeks, plus one week to collect data and calculate, so it will take at least three weeks to compile the CCL index. The index is compiled based on the transactions of 100 famous small and medium-sized private housing estates in Hong Kong, not all large and medium-sized housing estates. Therefore, it may take more than three weeks for the decline of the real estate market to be reflected in the CCL index. Judging from the continuous decline of CCL in recent weeks, it is likely that the market situation has undergone a relatively large adjustment.

Secondly, the above analysis ignores the hierarchical nature of the price adjustment of Hong Kong real estate. To be specific, the rise of Hong Kong's property market is often transmitted from Hong Kong Island to Kowloon, and then to the New Territories. When the property market goes down, the housing estates in the New Territories are often the first to suffer heavy losses, and then spread to Kowloon and Hong Kong Island.

If the market still follows this pattern, the new territories property price fell by more than 10% in the past week, and the Jiahu Villa near Tianshui Wai plummeted by 15% in the 12 weeks up to October, indicating that the deep adjustment of the Hong Kong real estate market has begun.

Third, we should not be blindly optimistic about the loosening of stamp duty by the Hong Kong government. The government's economic adviser, Ou Xixiong, told the media a few days ago that the Hong Kong property market had been declining since its peak in July, but until September, the housing price was still 125% higher than the peak in 1997, while the purchasing power index (the ratio of contributions to income) of residents' real estate was still at a high of about 74% in the third quarter. He believes that the adjustment of the property market will last for a period of time and calls on the public to pay attention to the relevant risks.

Ou Xixiong's words actually released two levels of information. First, the Hong Kong government does not think that the property price adjustment is a bad thing. Second, the Hong Kong government is "happy" to continue to adjust the property price for a period of time. If so, unless there is a major adjustment in real estate, the Hong Kong government will not be in a hurry to loosen stamp duty. Therefore, real estate investors cannot hold too much hope for the Hong Kong government to rescue the market.

Finally, the impact of trade friction cannot be ignored. So far, there is no indication that the United States and China will completely resolve trade disputes in the short term. The market will not wait indefinitely for the negotiation results of both parties, because the business community will respond in advance to the upcoming tariff increase, and the financial market will also respond quickly to the relevant asset prices. The superposition effect of the two may make the price of financial assets fluctuate more sharply.

If the fluctuation of the financial market mainly affects the price of buildings, then the decline of consumption power will substantially affect the rental market, which will greatly reduce the attractiveness of Hong Kong's building investment in the case of interest rate hikes in the United States.

Some real estate agents reported that in the past month, rents in both commercial buildings and residential rental markets have stagnated or even decreased to varying degrees. Perhaps this is another sign that the property market has intensified its downward trend.

(The author of this article is an expert in Hong Kong's financial market, and the author of "The Investment Way of Chinese Hedge Fund Managers Dominating the World")