Article/Cheng Shi, columnist of Sina Financial Opinion Leader (WeChat official account kopleader)

Asset performance in developed markets is expected to shift. The European stock market may continue to be depressed, while the US stock market is expected to bid farewell to the bull market and enter a period of adjustment with repeated oscillations. The US dollar index is expected to gradually turn into a downward channel, and non US dollar safe haven assets such as yen and gold are expected to have greater appreciation potential.

"The number of heavenly ways is opposite, and prosperity will decline." In 2019, constrained by the hesitation of global recovery and the impact of the resurgence of the crisis, the recovery power of developed markets is expected to decline and deteriorate gradually. Among them, the US economy is expected to enter the first half of the cycle inflection point in 2019. With trade friction as the center, policy uncertainty may become the primary risk to the US economy. The European economy will face multiple shocks from geopolitical risks, and the real threat of regional integration retrogression will rise again, which may drag Europe back to the old state of weak recovery. In comparison, thanks to the stable internal and external environment, Japan's economy is expected to slow down slightly, but it is likely to show comparative advantages. In general, with the United States, Europe and Japan as the leading forces, the developed markets are expected to show a sharp feature of slowing economic growth, slowing inflation, rising risk centers and prudent policies in 2019. Affected by this, asset performance in developed markets is expected to shift. The European stock market may continue to be depressed, while the US stock market is expected to bid farewell to the bull market and enter a period of adjustment with repeated oscillations. The US dollar index is expected to gradually turn into a downward channel, and non US dollar safe haven assets such as yen and gold are expected to have greater appreciation potential.

American Economy: Towards the Turning Point of the Cycle

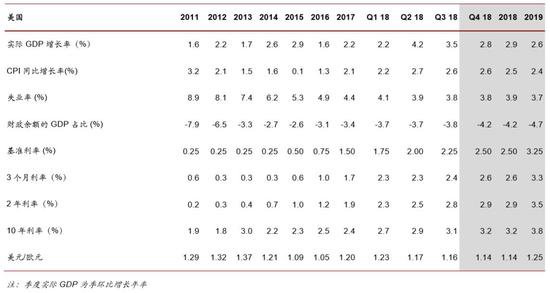

In terms of growth, the US economic cycle has reached an inflection point. In 2019, as the policy costs of trade frictions accelerate to appear, the fiscal stimulus effect of the early deficit gradually subsides, and the Federal Reserve steadily normalizes its monetary policy, the growth rate of the U.S. economy will move past the stage high and fall back on the relatively slow long-term growth channel. Specifically, this change has two characteristics. First, from the perspective of timing, 2019 is expected to start the first half of the turning point of the US cycle. Since June 2018, the short-term and long-term leading indicators of the US economy have diverged significantly. Indicators leading for 1-2 quarters (based on the average working hours, consumer expectations and other indicators) hover around the historical peak. However, the indicators leading 3-6 quarters (based on new private building permits, real estate prices and other indicators) have continued to decline. In view of this, the super expected performance of the US economy since the second and third quarters of 2018 will continue to the first half of 2019 in the short term, and will strongly support the Federal Reserve to complete the gradual interest rate increase. However, from the second half of 2019, the growth rate of the U.S. economy will gradually show weakness, and gradually decline, indicating that the turning point of the cycle is approaching. 2019 and 2020 will respectively constitute the first and second half of the turning point of this round of the US cycle. Second, from the perspective of growth rate, the first half of the turning point will be "decelerating without stalling". As stated in our previous research, since 2017, "large-scale tax cuts+accelerated interest rate hikes" have constituted the "two foot model" of the US supply side reform by taking advantage of the policy window period of the US economic stimulus, effectively correcting the distortion of the economic structure caused by long-term monetary easing. Thanks to this, since 2018, the labor productivity and total factor productivity of the United States have achieved a strong boost. At the same time, the number of quarterly new enterprises has hit a new high since 2004, consolidating the long-term development momentum. Therefore, although the growth rate of the U.S. economy will approach the long-term level in 2019, the growth is still stable, and the actual growth rate for the whole year is expected to be 2.6%.

With the economic growth turning to an inflection point, American inflation will also leave the peak and turn to a downward trend. However, because the economic growth is "decelerating without stalling", and this round of economic summit has led to a strong rise in wage growth, coupled with imported inflation caused by trade friction, the downward range of inflation in 2019 is expected to be less than the decline of economic growth, and the year-on-year growth rate of CPI for the whole year is expected to be 2.4%.

At the policy level, Trump and the Federal Reserve moved to the "crossroads". In 2019, two potential policy changes will constitute the biggest uncertainty of the US economic trend. For the Trump administration, the "crossroads" lie in the subsequent impact of the mid-term elections. In terms of fiscal policy, as the Democratic Party regains control of the House of Representatives, it will have a real constraint on the Trump government, so the possibility of further tax cuts and infrastructure construction is significantly reduced. In terms of trade policy, in the short term, Trump's extreme anti globalization measures have been initially restricted by the backbite of protectionism. On November 1, the heads of state of China and the United States held an "ice breaking call". On November 8, President Xi Jinping met with former Secretary of State Henry Kissinger of the United States. As a result, China US relations have shown signs of easing, and further warming in the future is worth looking forward to. However, in the long run, it has become the consensus of the two parties of the United States to curb China's rise and maintain the advantage of the United States in leading the world. Once the domestic contradiction intensifies sharply, the possibility that the Trump administration will join hands with the Democratic Party to worsen the trade conflict cannot be ruled out. On the whole, China US economic and trade relations are expected to present a pattern of "short-term pressure easing and long-term game continuation". The possibility of partial de integration between China and the United States is high, but the probability of full de integration is very low; It is possible to carry out a normalized policy game, but the probability of starting a comprehensive cold war is very small. For the Federal Reserve, the "crossroads" lie in the policy mix transformation in the middle of 2019. By the middle of 2019, the target range of the Federal Reserve's policy interest rate will reach the long-term neutral level (3%), and the space for interest rate increase will be narrowed. Therefore, if the U.S. economy remains stable after entering the turning point of the cycle, the Federal Reserve is expected to change from "fast rate increase+slow contraction table" to "slow rate increase+fast contraction table", so as to moderately restore the steepness of the yield curve.

However, as a latecomer in the internal policy game, the choice of the Federal Reserve still needs to refer to the Trump government's initiatives, so the following three potential policy combinations are formed, which have different impacts on growth, risk and inflation. First, subject to the negative impact of trade frictions, the Trump government will no longer increase trade frictions, and the Federal Reserve will switch to "slow interest rate increase+rapid contraction" as scheduled. The U.S. economy has "slowed down without stalling" in the short term, inflation has declined steadily, long-term economic growth has remained steady, and financial risks have been gradually cleared in continuous adjustment. At present, this situation is the most likely, and it is also the benchmark scenario we predict. Second, the escalation of trade frictions and the rising risk of the "economic iron curtain" will have a serious impact on the economic and financial stability of the United States. The Federal Reserve will be forced to suspend the normalization of monetary policy, and the long-term and short-term growth of the United States economy will be damaged, which may lead to the "stagflation" dilemma. Third, trade frictions are escalating. However, due to the time lag of negative impact, the Federal Reserve still switches to "slow interest rate increase+rapid contraction table" as scheduled, which will lead to the growth of long-term interest rate of US debt exceeding the market's capacity, resulting in a new round of economic and financial systemic risks.

At the risk level, market sentiment has entered a fragile and sensitive stage. As the US economic cycle moves towards an inflection point, the uncertainty caused by overlapping the "crossroads" of policies will lead to a highly sensitive and fragile mood of US investors in 2019, which will frequently switch between excessive pessimism and excessive optimism. Moreover, the current high valuation level of risky assets such as US stocks and high-yield bonds has not yet fully "Price In" both for economic downside risks and policy uncertainties. Affected by this, in 2019, the price of risk assets in the United States is expected to enter a continuous and repeated period of oscillation and adjustment, and the market volatility is expected to continue the long-term upward trend. It is expected that the long VIX index, gold and other non US dollar hedge assets will produce relatively certain returns. In addition, due to the continuous oscillation of the US market and the large probability of the Federal Reserve slowing down the pace of interest rate increase, the dollar index is expected to fall easily in 2019 but not rise, and the numerical center is expected to decline significantly. On the whole, the 10-year US bond yield will be the vane of the US market risk in 2019, which deserves close attention.

2019, the US economy moves towards a cyclical inflection point

Source: Bloomberg, IMF and our forecast

Source: Bloomberg, IMF and our forecast European economy: meet the challenge of populism again

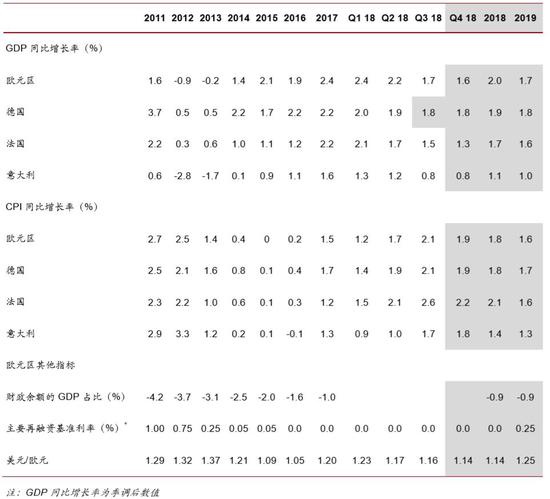

In terms of growth, Europe's recovery has returned to the old weak state. In 2019, subject to three major factors, the euro zone economy will bid farewell to the good times of 2017-2018 and return to the old state of relatively weak recovery. First, the demand side stimulus effect accelerated to decline. With 2018 as the turning point, the output gap in the euro area has changed from negative to positive. So far, the marginal stimulus effect of the loose policy on the economy will tend to be weak. Second, structural reform is difficult to sustain. For the aging European economy, labor is the most important resource element. Thanks to a series of labor market reforms in EU member states from 2008 to 2014, labor mobility and productivity in Europe rose rapidly from 2014 to 2017, laying the foundation for this round of economic recovery. However, in 2017-2018, when the recovery was strong, the subsequent structural reform failed to achieve a major breakthrough, which led to the decline of labor productivity from 2017Q4, weakening the recovery potential. Third, the external pressure gradually increased. With the cost of global trade friction accelerating in 2019, the European economy, which is highly dependent on trade, will be greatly hit. According to the IMF's latest forecast, the current account balance of the euro area will fall to the lowest point since 2015 in 2019. The uncertainty of trade prospects has been reflected in current expectations. Since the beginning of 2018, the euro area consumer confidence index and Sentix investment confidence index have both crossed the peak and entered a downward channel. Overall, the real economic growth rate of the euro area is expected to fall back to 1.7% in 2019. While economic growth is weak again, the weak rise of labor productivity will make it difficult to sustain the rapid growth of current wages. Therefore, in 2019, the inflation level in the euro area is expected to gradually decline, and the year-on-year growth rate of CPI is expected to decline to 1.6%.

At the policy level, the European policy space is narrowing. Faced with various internal and external challenges, Europe does not have sufficient policy space to reverse the sluggish economic growth. From the perspective of unified monetary policy, since the normalization of monetary policy of the Federal Reserve will not stop in 2019, the ECB is expected to continue to tighten monetary easing marginally. However, in view of the weak economic growth, the European Central Bank's prudent attitude is expected to be further strengthened. The first interest rate increase will delay the approximate rate to the fourth quarter of 2019, so as to continue the low interest rate state and support economic growth. From the perspective of decentralized fiscal policies, there is a clear mismatch in the capacity and willingness of countries in the euro area. As a pillar country in Europe, although Germany has abundant fiscal surplus, its output gap has closed. Under the crisis of declining domestic support rate, the Merkel government is difficult to carry out large-scale fiscal stimulus and exchange the welfare of its own people (high inflation) for the recovery of the European economy. However, as the third strongest in the euro area, Italy's economy has lagged behind in its recovery during the decade of crisis, and there is still a significant output gap and fiscal stimulus space. However, because the growth rate of the budget target exceeds the EU regulations, it falls into a fierce game with the EU, which may not fully release the effectiveness of the policy. From the perspective of structural reform, in 2019, with the geopolitical pressure in the Middle East and the inflow of refugees, together with the rise of internal populist forces, the deepening reform of the euro area integration, especially the construction of financial capacity, is expected to remain stalled, making it difficult to repair the long-term growth potential of the European economy in a timely manner.

At the risk level, the rise of populist forces has become the primary challenge again. In 2019, the decline of economic growth will help the rise of populist forces, and promote regional risks from weak to strong, from short-term to long-term. First, in December 2018, as Merkel stepped down as the leader of the German CDU, Germany's role as a "stability anchor" in Europe will be greatly questioned. Second, the game between Italy and the EU may further escalate around the budget goal, which will trigger the EU excess deficit procedure and, under certain conditions, lead to the Italian sovereign credit crisis and the European banking crisis. Third, in March 2019, the probability of a difficult birth of the Brexit agreement is not low, and it may be forced to postpone, changing the risk of Brexit from "short-term pain" to "long-term pain". Fourth, in the European Parliament elections in May 2019, the populist political forces of all countries are expected to form a unified front for the first time and strengthen the anti regional integration forces. Fifthly, with the resignation of ECB President Draghi in November 2019, the European monetary policy and crisis rescue strategy may become uncertain. In addition, under the impact of domestic reform travails, the popular support rate of French President Makron has fallen into a low point. In 2019, it is feared that he will encounter a sharper public opinion rebound, further weakening the strength of the European solidarity and reform camp. On the whole, the 10-year bond spread between Italy and Germany will be the wind vane of European systemic risk in 2019. In combination with the above risk conditions, although the value of the euro is expected to rise in 2019 as the dollar index weakens, under the impact of many uncertainties, the range of this rise is limited, and it is expected that there will be significant fluctuations periodically. However, constrained by weak economic growth, the overall performance of the European market in 2019 is expected to fall into a long-term downturn.

In 2019, European economy meets the challenge of populism again

Source: Bloomberg, IMF and our forecast

Source: Bloomberg, IMF and our forecast Japanese economy: slow pace and quiet time

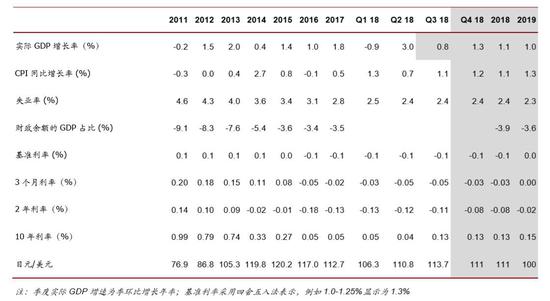

As we emphasized in previous studies, Abenomics' core is Abenomics, and the key is the reconstruction of social confidence. In 2019, with the transformation of the internal and external risk environment, the comparative advantages of the two aspects will effectively consolidate Japan's social confidence, so that the Japanese economy will become a stable and stable fixed point in the global "crisis recovery" turbulence.

First, the impact of external risks is limited. In 2019, when the global geopolitical risks are rising, Japan is expected to be isolated from all kinds of risks. In terms of trade frictions, in July 2018, Japan and the European Union reached the largest free trade agreement in history, abolishing most bilateral tariffs. In October 2018, with Abe's icebreaking visit to China, the Sino Japanese trade partnership is expected to continue to recover and work together to expand the third-party market. As a result, Japan is expected to gain the special advantage of seeking both sides and avoid the negative impact of global trade friction to the greatest extent. The IMF's latest forecast shows that the proportion of Japan's current account surplus in GDP will rise by 0.14 percentage points in 2019, which is quite different from Europe and the United States, where the current account has deteriorated. In terms of geopolitical conflicts, with the dramatic improvement of the situation on the Korean Peninsula and the continuous fermentation of the chaos in the Middle East, Japan will be far away from the forefront of the global power game in 2019, which also forms a sharp contrast with Europe and the United States, which face risks directly. From historical experience, when Japan is far away from the global risk center, the rise of global panic will enhance the risk aversion of the yen and promote its currency value to rise. Therefore, in 2019, the rise of the global risk center is expected to guide a large number of safe haven funds into the Japanese market, further enhancing the stability of the Japanese economy.

Second, the internal policy is smooth and steady. Looking forward to 2019, unlike the increasingly fierce internal policy game in Europe and the United States, Japan's economic policies will show valuable stability and continuity. First, in September 2018, Abe was granted a three-year term of office again, which ensured that the policy framework of Abenomics would not be shaken, and was conducive to stabilizing the long-term confidence of Japanese society in structural reform, growth and inflation. Second, although the Bank of Japan may slightly adjust the scale and frequency of bond purchases in 2019, it will still maintain strong monetary easing for a long time in general, and the extremely low policy interest rate and 10-year treasury bond yield target are not expected to change. This will help hedge the reform pain caused by the consumption tax increase in October 2019, and support inflation to approach the target level. Third, thanks to the cumulative effect of early stimulus policies, Japan's nominal and real wage growth rates have both increased since the beginning of 2018, and the monthly growth rate once hit a 21 year high. The rapid growth of wages will not only help support the long-term upward trend of inflation, but also open a policy window for the implementation of structural reform. Based on the above factors, Japan's core inflation growth rate is currently at a stage high, and is expected to continue a moderate upward trend in 2019.

To sum up, Japan's economic growth is expected to decline slightly to 1.0% in 2019, but it is expected to remain stable on the whole, inflation is expected to rise moderately, and the year-on-year growth rate of CPI is expected to reach 1.3%. Based on this, in the global "crisis recovery" turbulence, the Japanese market will become an important haven for global capital, showing a significant comparative advantage. Thanks to the risk aversion, the value of the yen will also have greater room to rise. However, two risks still deserve vigilance. First, the sudden outbreak of deep adjustment in the US stock market may have a short-term spillover impact on the Japanese stock market. Second, if the yen appreciates too fast, it may cause the market to worry about the slowdown of Japanese exports.

2019, Japan's economy is slow and calm

Source: Bloomberg, IMF and our forecast

Source: Bloomberg, IMF and our forecast Developed market: developed deterioration

Looking at the overall situation, with the United States, Europe and Japan as the leading forces, the recovery power of developed markets will gradually deteriorate in 2019. While the recovery process continues, major changes in four dimensions are expected to take place.

First, the economic growth has slowed down. Farewell to the strong recovery in the previous two years, the real economic growth rate of developed markets is expected to decline slightly to 2.1% in 2019, while the inflation level will also surpass the peak in 2018, and the year-on-year growth rate of CPI is expected to decline to 2.0%. However, as the overall recovery is still on track, the employment market will continue to improve marginally, and the unemployment rate is expected to fall to 4.9%.

Second, the risk center has been improved. Under the transmission chain of "crisis recovery", Europe will become the primary target of geopolitical risks in 2019, and the black swan risks will follow throughout the year. Centered on trade frictions, the "crossroads" of policies constitute the greatest uncertainty in the US market. Japan's economy is expected to show a calm and stable comparative advantage.

Third, the policy tends to be cautious. In 2019, as the output gap turns from negative to positive and the economy slows down at the same time, countries will be more cautious about withdrawing from easing. The fiscal deficit is expected to expand moderately, monetary easing is expected to slow down, the pattern of "the United States actively tightens, Europe and Japan passively tightens" will be further consolidated, and the policy interest rate and long-term interest rate level will slightly rise.

Fourth, asset performance shift. In 2019, under the influence of various risk factors, the European stock market is expected to continue to be depressed, while the American stock market, which was long before, is expected to enter a period of adjustment with repeated oscillations. The strong trend of the US dollar index in 2018 is expected to gradually turn into a downward channel in 2019. Non dollar safe haven assets such as yen and gold are expected to have greater appreciation potential.

(The author of this article introduces: Head of ICBC International Research Department, Chief Economist. His research fields include global macro, Chinese macro and financial markets.)