Article/Ren Zeping, Luo Zhiheng, Gan Yuan, Sun Wanying and other columnists of Sina Financial Opinion Leader Column (WeChat official account kopleader)

Recently, financial deleveraging is turning into stable leverage. We judge that in the future, monetary finance will be structurally relaxed, and counter cyclical adjustment will be strengthened. While increasing the supply of basic currency, structural financial regulation will be relaxed to increase the ability of credit derivatives to support the real economy.

event

In October, the added value of industries above designated size was 5.9% year on year, the previous value was 5.8%; The total retail sales of consumer goods in October were 8.6% year on year, up from 9.2%; Fixed asset investment from January to October was 5.7% year on year, 5.4% from the previous year; In October, the urban unemployment rate was 4.9%, the previous value was 4.9%. In October, the social financing scale increased by 728.8 billion yuan, expected to be 1.3 trillion yuan, with the previous value of 2.21 trillion yuan; M2 money supply is 8% year on year, expected to be 8.4%, the previous value is 8.3%; New RMB loans reached 697 billion yuan, expected to reach 904.5 billion yuan, up from 1380 billion yuan.

catalog

1. Core view: the economy has bottomed out twice and the policy has begun to break the ice

2. The effect of credit easing policy has not yet appeared, and the financing situation is still tight

3. Industrial production is still low, cars are sluggish, and high-end manufacturing such as communication and electronics is growing rapidly

4. The growth rate of fixed asset investment rose slightly but remained sluggish, mainly supported by manufacturing investment. The low M2 level and the downward trend of social finance indicate that investment growth is difficult to rise in the short term

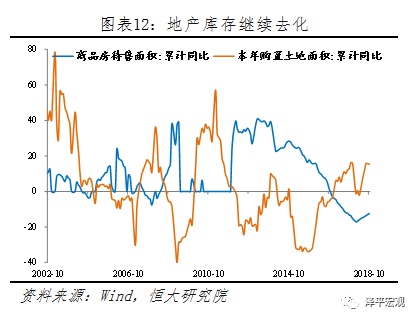

5. Investment in real estate sales fell back, financing situation remained tight, and real estate enterprises accelerated pre-sale collection

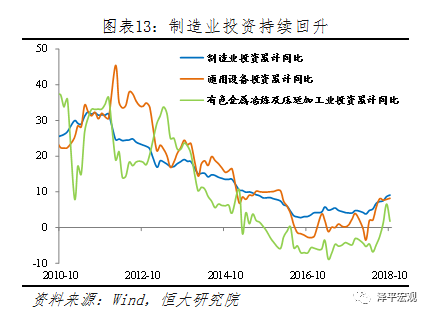

6. Manufacturing investment is at a new high in the past three years, and the production capacity is verified in a fresh cycle, but the downstream private enterprises are squeezed

7. The growth rate of infrastructure investment rebounded at the bottom, and the rebound was supported by "stabilizing investment" and "reinforcing weakness" in the future, but the range was limited

8. Low consumption, upgrade and demotion reflect social stratification, declining liquidity and downward pressure on the economy

9. Both imports and exports rose sharply on a year-on-year basis, and exports may decline significantly after the "scramble for exports" effect disappears

10. The Sino US trade friction has moved from confrontation to relaxation in the short term, but it is still severe in the long term. The best response is reform and opening up

11. CPI rose moderately and PPI continued to fall

12. PMI of manufacturing industry dropped to a new low in two years, and new orders, especially new export orders, declined significantly, showing the impact of trade friction

text

1. Core view: the economy has bottomed out twice and the policy has begun to break the ice

In the second half of 2015, we judged that China's economy was close to the bottom and "L-shaped economy"; in early 2017, we judged that the capacity was cleared "in the new cycle"; in early 2018, we proposed "the top of the financial cycle".

At present, China's economy is in the superposition of six major cycles: the world economy is in a new round of growth cycle, but may gradually peak and fall back, the financing situation is tight at the top of the financial cycle, the bottom of the new production capacity cycle, the middle of the real estate cycle regulation, the destocking cycle and the new political cycle.

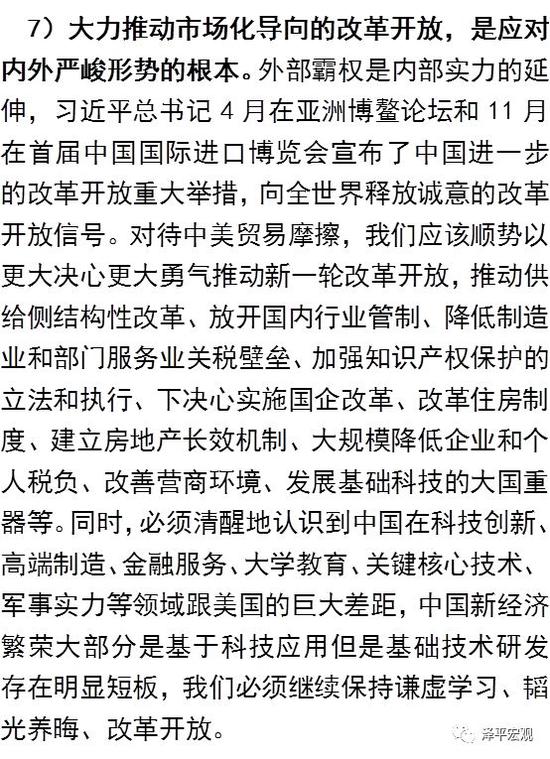

In the face of the impact of internal and external factors such as the Federal Reserve's interest rate increase, Sino US trade friction, fiscal consolidation, financial deleveraging, and real estate regulation, the economic situation is facing accelerated decline from the second half of 2018 to 2019, and it is expected that the second bottom will be reached in the middle of 2019. Monetary, financial and taxation policies should be shifted to strengthening counter cyclical regulation, providing a stable macro environment for long-term supply side structural reform, and supporting the real economy and capital market. The Politburo meeting stressed for the first time that "downward pressure on the economy has increased", deployed six "stabilities" to solve the difficulties of private enterprises and SMEs, and the Central Bank, the Banking and Insurance Regulatory Commission, the Securities Regulatory Commission, the Ministry of Finance, the Ministry of Justice and other departments introduced rescue measures. In the long run, the most fundamental thing is to actively promote reform and opening up, show confidence in opening up, open up new investment opportunities, and boost enterprise confidence.

From the economic and financial data in October, we can see the nine characteristics and trends of the macro-economy:

1、 The strong cycle of the US dollar superimposes global trade friction, and the global market, including the US stock market, is turbulent. We believe that the US economy has peaked at a high level and is about to enter stagflation, but the fundamentals are still healthy, the leverage ratio is generally controllable, and the Trump boom is about to end rather than collapse. The impact of trade frictions on the United States is beginning to show. The recent slowdown of the United States economy and the sharp decline of the stock market may make the Trump government calm down and return to the negotiating table. The Federal Reserve's interest rate increase, the strengthening of the US dollar, Trump's tax cuts and global trade frictions have led to the accelerated return of capital to the United States. Countries, especially emerging markets, have seen their exchange rates depreciate and their stock markets fall. Turkey and Argentina have seen their exchange rates collapse successively, facing difficulties similar to those in Southeast Asia in 1998: asset price bubbles, high foreign debt, and high inflation.

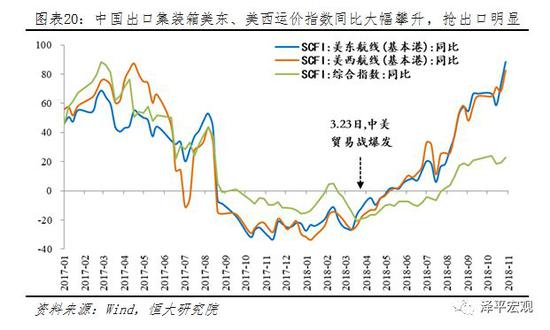

2、 Against the background of the global economic marginal slowdown and continued trade friction, China's export growth has continued to grow at a high rate, with obvious export competition effect. The index of new orders has hit a 33 month low, and subsequent exports are expected to decline significantly. First, Shanghai's comprehensive index of export container freight rates was relatively stable (22.9% year-on-year at the end of October), but the prices of the West America and East America routes rose sharply to 80% and 77% year-on-year, resulting in tight shipping between China and the United States. Second, the export delivery value has risen significantly for four consecutive months, including the export delivery value of computer communication electronic equipment, which has continued to rise since June. Third, the global economic margin has slowed down. The global manufacturing PMI has declined for six consecutive months, at a low point since November 2016. The BDI index has declined after peaking at the beginning of August. The export growth of Japan and South Korea has turned negative, but China's export has risen against the trend, and the export growth to the United States has remained above 11% for six consecutive months. Fourth, PMI's new export orders hit a 33 month low, which will put a great downward pressure on exports in the future.

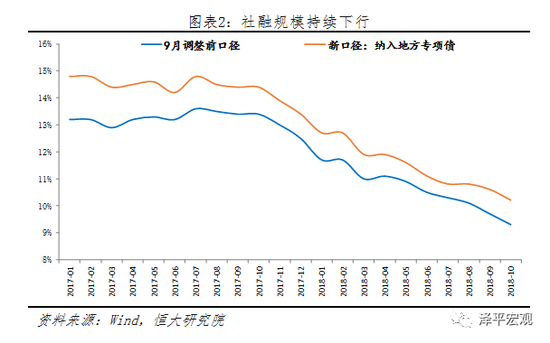

3、 Domestic, As the financial cycle entered the second half, the financial deleveraging in the early stage and liquidity ebbed. From January to October this year, the scale of social finance was 16.1 trillion yuan, 2.8 trillion yuan less than the same period last year, Off balance sheet financing continued to shrink, monetary policy transmission was blocked, banks were "reluctant to lend", private enterprises and small and medium-sized enterprises were difficult to finance, M2 was at a historical low, the loan structure deteriorated, enterprises' medium and long-term loans declined significantly, and short-term bill financing increased significantly. Recent financial deleveraging is turning into stabilizing leverage We judge that in the future, monetary and finance will be structurally relaxed and counter cyclical regulation will be strengthened. While increasing the supply of basic currency, financial regulation will be structurally relaxed to increase the ability of credit derivatives to support the real economy.

4、 The growth rate of fixed asset investment rose slightly but remained at a low level, which was mainly supported by the manufacturing industry. Affected by financial deleveraging, fiscal consolidation and real estate regulation, it was difficult to recover significantly in the later period. The growth rate of infrastructure investment hit the bottom and rebounded, supported by the availability of special debt funds and accelerated fiscal expenditure (The issuance of 1.35 trillion yuan of special bonds was basically completed by October, and the fiscal expenditure in October was 8.2%). Later, under the role of "stabilizing investment" and "reinforcing weakness", it continued to rebound, but the extent was not large. The meeting of the Political Bureau and the executive meeting of the State Council in July demanded that fiscal policies be more active and play a greater role in restructuring and expanding domestic demand; At the meeting of the Political Bureau at the end of October, the six stabilities were put forward again; On October 31, the Office of the State Council issued the Guiding Opinions on Maintaining the Strength of Shortcomings in the Field of Infrastructure, which proposed that efforts should be made to complement the weaknesses in the fields of railways, roads, water transport, airports, water conservancy, energy, agriculture and rural areas, ecological environmental protection, public services, urban and rural infrastructure, shantytown reconstruction and other fields, and accelerate the promotion of major projects that have been included in the plan. With the completion of the cleaning up of the non compliant projects in the early stage, the implementation of the compliant projects has been accelerated, and the special bond funds continue to be used. The State Council requires that the projects under construction should not be blindly withdrawn, and the rebound of infrastructure investment is expected to continue.

5、 The investment in real estate sales has peaked and fallen back. The high growth in the early stage is related to the delayed impact of the housing enterprises' increasing high turnover payments and the housing reform policies. Due to the tightening of financing, the first and second line price limits, the tightening of monetary resettlement for the third and fourth line shantytowns, the slowdown of residents' income growth, the rise of personal housing loan interest rates, and the land auction, the next stage of the country, especially the third and fourth line real estate sales area, will face downward pressure.

The real estate market should pay attention to two major phenomena: first, the main source of funds in place for real estate enterprises is advance collection, mortgage loans have been significantly tightened, and the financing situation is tense. The high growth rate of new construction and the low growth rate of completion reflect that real estate enterprises are accelerating pre-sale collection. From January to October, the paid in capital of real estate enterprises was 7.7% year on year, down 0.1 percentage points from January to September. Among them, domestic loans were - 5.2% year on year, personal mortgage loans were - 0.9% year on year, self raised funds were 10.8% year on year, and deposits and advance receipts were 16.3% year on year. Second, land auctions continued to increase, From January to October, there were 1139 unsold residential land auctions nationwide, including 13 unsold land auctions in first tier cities; 254 second tier cities, up 179% year on year; There were 872 land auctions in third and fourth tier cities, up 23% year on year. Land auctions are due to the great financing pressure of real estate enterprises and the increase of cities with price limits. With the attitude of the central government to resolutely curb the rise of house prices, enterprises' land acquisition behavior is more rational, and the local government has not substantially reduced the land auction price. Land auctions will lead to the decline of subsequent real estate investment, the decrease of land transfer income, and the limited source of capital for infrastructure.

6、 Manufacturing investment rose for seven consecutive months, the highest point in three years. High tech investment, such as computer, grew rapidly, and the cycle of fresh production capacity was verified.

7、 The continuous downturn in consumption and the coexistence of consumption upgrades and downgrades reflect that social stratification requires great attention. In October, the total retail sales of consumer goods grew by 8.6% in nominal terms on a year-on-year basis, 0.6 percentage points lower than that of the previous month, and the actual growth rate was 5.6%, which was the lowest since 2003. This was related to the slowdown in income growth and the delayed consumption of the "Double 11" promotion. From the perspective of structure, the consumption of new business types and upgrading types is growing rapidly. From January to October, online retail sales increased by 25.5% year on year; Cosmetics and communications increased by 11.4% and 10.4% year on year. In the long run, residents' consumption is upgraded, but in the short run, some people's consumption is degraded, liquidity ebbs, rigid debt is high, and housing rent and medical prices rise significantly, which is mainly reflected in the decline in the proportion of entertainment and cultural consumption and the concentration of middle class people, For example, people such as middle-class white-collar workers with high debt who buy houses with leverage and urban workers who rent first and second tier houses (neither property income nor financial transfer income guarantee obtained by people with similar minimum income). The gap between the rich and the poor has risen for two consecutive years, and the consumption classification characteristics between urban energy levels and high-income groups are obvious. It is necessary to promote consumption by improving national income distribution, reducing personal income tax, increasing financial investment in social security such as education and health care, reducing the gap between the rich and the poor, and increasing the supply of high-quality products such as high-end manufacturing and service industries.

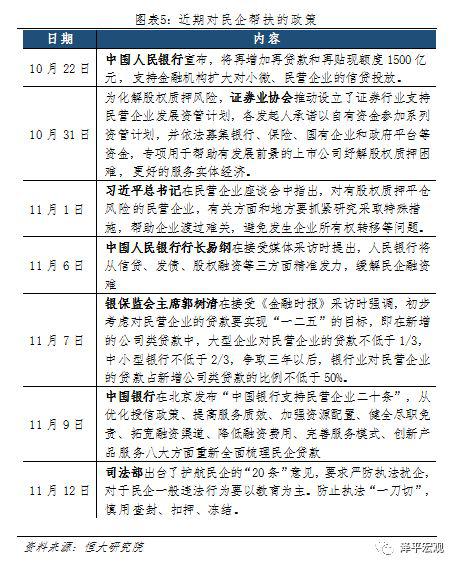

8、 The survival dilemma of private enterprises has been highly valued by the policy. It is necessary to focus on solving the problems of small and medium-sized enterprises and private enterprises, such as difficult and expensive financing, heavy tax burden, environmental protection and capacity reduction that hurt private enterprises, stabilize expectations, implement the principle of "competition neutrality" of state-owned enterprises, and release water to raise fish. The upstream resource industries are dominated by state-owned enterprises. After the capacity reduction and environmental protection storm, the industry concentration has further increased significantly. The downstream manufacturing industry is dominated by private enterprises. Faced with the double squeeze of excessive upstream price increase profits and financial deleveraging financing discrimination, private enterprises are in a difficult position to survive, social resource mismatch and total factor productivity decline. The profits of state-owned enterprises in January September were 23.3% year on year, Profit of private enterprises was 9.3% year on year; From January to September, the interest expenditure of industrial private enterprises grew by 11.8% year on year, higher than the 6.7% of the interest expenditure of state-owned enterprises year on year. The above issues have been highly valued by the senior management and various rescue measures have been introduced. President Yi Gang said that the People's Bank of China has made precise efforts in credit, bond issuance and equity financing. Guo Shuqing, Chairman of the Banking and Insurance Regulatory Commission, considered that loans to private enterprises should achieve the goal of "One Two Five Year Plan". In addition, several securities companies have launched a series of asset management plans to support private enterprises. As of November 9, The scale of the asset management plan reached 18.1 billion yuan; The Ministry of Justice issued the "20 Opinions" on escorting private enterprises, requiring strict prevention of law enforcement to harass enterprises. The general illegal acts of private enterprises should focus on education, prevent law enforcement from being "one size fits all", and carefully use seizure, detention, and freezing.

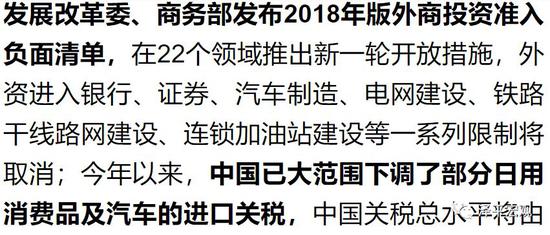

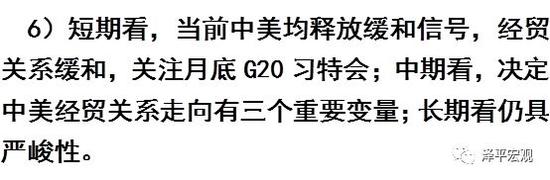

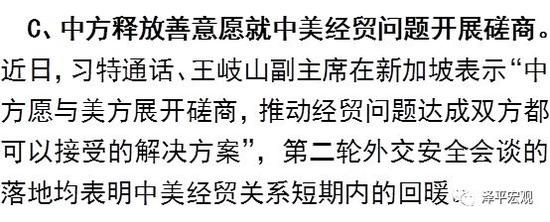

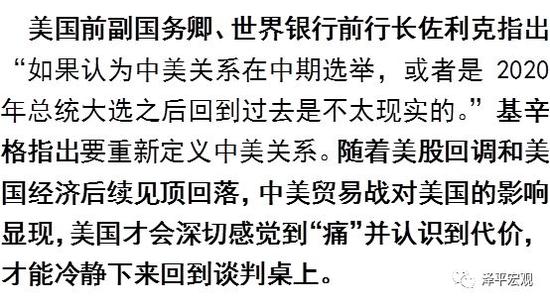

9、 China US trade frictions have moved from confrontation to easing in the short term, mainly because the US stock market pullback and the US economic slowdown have made the US realize the cost and return to calm, paying attention to the special session of the G20 summit at the end of the month. In the medium term, there are three important variables that determine China US economic and trade relations: first, the 2020 presidential election (launched in the second half of 2019), second, the speed of the peak decline of the U.S. economy and the pullback of U.S. stocks, and third, the strength of China's reform and opening up. Special attention should also be paid to the fact that Pelosi, an extreme anti China activist, became the Speaker of the House of Representatives again after the mid-term elections in the United States. Trump may make efforts in foreign affairs after being blocked in internal affairs. There is no difference in the policies of the two parties and the two houses towards China, and the tough trade policy towards China may continue. It is still serious in the long run. The most fundamental way to deal with Sino US trade frictions is to vigorously promote market-oriented reform and opening up. General Secretary Xi Jinping announced China's major measures for further reform and opening up at the Boao Forum for Asia in April and the First China International Import Expo in November, releasing a sincere signal of reform and opening up to the world and showing confidence in opening up. In dealing with Sino US trade frictions, we should follow the trend with greater determination and courage to promote a new round of reform and opening up and win a new period of strategic opportunities.

Overall judgment: the current downward pressure on the economy is increasing, and the superposition of internal and external economies will double dip. The early policies of financial deleveraging, fiscal tightening, environmental storm, and social security changing from tax collection to increase the burden on enterprises are more policies in the period of economic overheating. In the current and next period of economic downturn, fiscal, monetary and regulatory policies should be adjusted to play a counter cyclical regulatory role. The short-term counter cyclical adjustment policy of demand management should not be opposed to the long-term supply side structural reform, which requires a short-term stable macro environment. In terms of reform methodology, the top-level design and the methodology of "gradual+incremental+pilot" should be combined in the future. It is suggested that counter cyclical policies should be adopted in the future: 1) Monetary and financial structures should be relaxed, from deleveraging to stabilizing leverage, to unblock the monetary policy transmission mechanism, to direct funds to the real economy, and to solve the problem of small and medium-sized enterprises and private enterprises that are difficult and expensive to finance. 2) We will be more proactive in finance. We will shift from balanced finance to functional finance, with the focus on tax cuts and infrastructure construction. It is suggested to increase the deficit ratio in 2019 to 3% - 3.5%, increase the special debt to 2 trillion yuan, reduce expenditures other than people's livelihood and social security, improve efficiency, significantly reduce taxes and fees to stabilize the expectations of micro entities, increase the living capacity of enterprises, and shift the way of tax reduction from increasing indirect tax cuts such as deduction to directly reducing the nominal tax rate, especially reducing the corporate income tax rate (e.g., from 25% to 22%) And VAT rate (taking the opportunity of VAT rate simplification to reduce the manufacturing tax rate from 16% to 10% in stages), and improve the sense of gain of enterprises and residents after tax reduction. 3) According to the actual situation in various regions, we should improve the policy implementation methods such as environmental protection governance, and strengthen the collection and management on the basis of reducing the social insurance rate to avoid "making things worse" for SMEs and private enterprises.

The task of capacity and inventory reduction of supply side structural reform has been basically completed. The deleveraging has moved to the middle and stable leverage. The future policy focus should be increased to reduce costs and address weaknesses. Confidence is more important than gold. In the medium and long term, we should take the six major reforms and greater opening up as a breakthrough to boost the confidence of enterprises and residents and open a new era of high-quality development First, establish a high-quality development assessment system, encourage local pilots, and mobilize local enthusiasm in the new round of reform and opening up. Second, we should firmly adhere to the reform of state-owned enterprises. We should not get caught up in ideological debates, and we should measure it according to the market-oriented orientation and the pragmatism standards of black cats and white cats. Third, we should vigorously and massively revitalize the service industry. Fourth, reduce the cost of micro entities on a large scale. Reduce taxes, simplify administration, and reduce basic costs such as logistics, land, and energy. Fifth, prevent and resolve major risks, promote the return of finance to its roots, and better serve the real economy. Sixth, according to the positioning of "houses are for living, not for speculation", the key to establishing a new housing system and long-term mechanism oriented by housing is to link people with land and financial stability.

2. The effect of credit easing policy has not yet appeared, and the financing situation is still tight

Recently, the structural easing of monetary policy and financial supervision have gradually shifted from deleveraging to stabilizing leverage. The Central Bank, the CBRC and local governments have successively introduced relief measures for private enterprises and small and medium-sized enterprises. However, the financing situation is still tight, and the effect of credit easing policy has not yet appeared. From January to October, the newly added social financing was 16.1 trillion yuan, 2.8 trillion yuan less than the same period last year. Off balance sheet financing contracted significantly, and M2 growth rate was 8% at a historical low.

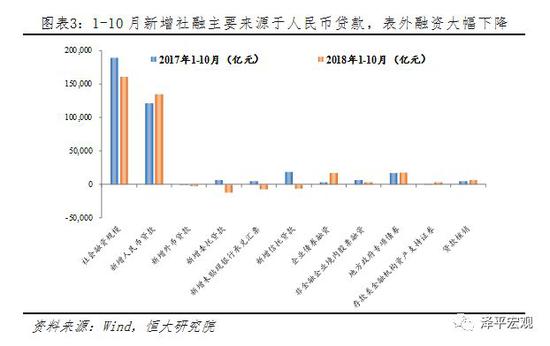

Although the reserve ratio has been lowered four times this year and the central bank has increased the supply of basic currency, the credit derivatives, currency creation and transmission mechanism are not smooth, and the financing of real estate, small and medium-sized enterprises and private enterprises is difficult. From the perspective of money supply Although the on balance sheet funds of banks have greatly improved, due to the recession of the real economy and the rise of non-performing loan ratio, the phenomenon of "loan sparing" is obvious, and the funds are deposited, which makes it difficult to flow to the real economy; The off balance sheet business and shadow banking business of banks were subject to strict supervision, and the ability to create money declined significantly. In the past, off balance sheet financing, as the main source of financing for SMEs and private enterprises, continued to shrink. From January to October, off balance sheet financing decreased by 2.6 trillion yuan, including an increase in the drop in the scale of entrusted loans by 1.25 trillion yuan and a decrease in trust loans by 592.5 billion yuan. From the perspective of money demand The financing difficulty of real estate enterprises, private enterprises and small and medium-sized enterprises has increased, while the investment expansion of local governments and state-owned enterprises is constrained by the debt reduction policy.

From the perspective of the month in October, the shrinkage of off balance sheet financing and seasonal factors are the main reasons for the sharp plunge in social finance. The loan structure is unbalanced, the medium and long-term loans of enterprises are low, and the downward pressure on the economy is increasing. The new social financing scale in October was 728.8 billion yuan, a new low since July 2016, and a decrease of 471.6 billion yuan compared with the same period last year. The new standard of social financing stock was 10.2% year on year, and the standard of local special debt fell to a historical low of 9.3% year on year from 9.7% in September. The sharp decline in the new social financial link ratio in October was related to seasonal factors. Local special bonds and RMB loans in October were lower than those in other months, down 652.1 billion yuan and 720 billion yuan respectively from September. From the perspective of structure In October, RMB loans increased by 714.1 billion, with a year-on-year growth rate of 7.6%, which is still the main force supporting social finance, but the growth rate slowed down significantly, reflecting the sluggish financing demand of the real economy. Off balance sheet financing continued to shrink, with a decrease of 267.5 billion yuan, which was still the main drag on social finance. Credit continues to flow to residents, mainly in the short term 。 New RMB loans were further tilted towards households, and the proportion of resident loans in new loans reached 81%, a new high since November 2016. Corporate loans plunged year on year, dominated by bill financing 。 In October, non-financial enterprises increased loans by 150.3 billion yuan, a year-on-year sharp decrease of 29.8%, of which bill financing was the main part, reaching 106.4 billion yuan, an increase of 144%.

It is expected that in the short term, the downward pressure on the growth of social finance and money supply will remain large, and the loan structure may improve under the guidance of policy expectations and regulatory constraints. In the face of the accelerated macroeconomic downturn and tight financial situation, the monetary policy in the next stage needs to actively play the role of countercyclical adjustment. While increasing the supply of base currency, the structural relaxation of financial regulation will increase the ability of credit derivatives to support the real economy. In November, a number of policies were introduced to ease the financing problems of private enterprises, and it was made clear that the MPA assessment of commercial banks should add evaluation indicators for financing of small and micro enterprises, and blind loan withdrawal and loan suspension should not be allowed to alleviate the liquidity risk of private enterprises. In the future, private enterprises will improve the availability of loans, which is conducive to improving the current loan structure dominated by resident loans.

3. Industrial production is still low, cars are sluggish, and high-end manufacturing such as communication and electronics is growing rapidly

Industrial production slightly recovered from the previous month, but still less than 6%. The slight increase in production is mainly due to the relaxation of the environmental protection margin, the rapid growth of ferrous metal smelting and non-metallic mineral production, and the acceleration of the production of electronic communication products driven by export competition. In the next stage, the decline in exports and domestic demand led to a sustained downturn in industrial production. In October, the industrial added value above designated size was 5.9% year on year, 0.1 percentage points higher than that of the previous month, 0.3 percentage points lower than that of the same period last year. In terms of power generation, the power generation in October was 4.8% year on year, 0.2 percentage points higher than that in the previous month. In terms of the three categories, the added value of mining, manufacturing, power, heat, gas and water production and supply industries increased by 3.8%, 6.1% and 6.8% year on year respectively in October, 1.6, 0.4 and - 4.2 percentage points higher than that in September. In the context of export competition, the export delivery value of industries above designated size in October accelerated by 3 percentage points to 14.7% compared with the previous month.

From the perspective of structure, automobile manufacturing is still sluggish, and high-end manufacturing of communication and electronics continues to increase. From January to October, the added value of high-tech manufacturing and equipment manufacturing increased by 11.9% and 8.4% respectively year on year, 5.5 and 2.0 percentage points faster than that of industries above designated size. New products grew rapidly. From January to October, the output of new energy vehicles and smart TVs increased by 54.4% and 19.6% respectively. But, The added value of automobile manufacturing is still low year on year. In October, it was - 0.7% year on year, 1.4 percentage points lower than that of the previous month. Main reasons: First, this year, the vehicle purchase tax will be recovered at the rate of 10%, and the preferential policies will be canceled, which will hit the market demand to a certain extent. Second, the high leverage of the residential sector has led to the crowding out of consumption and the decline of output and output value.

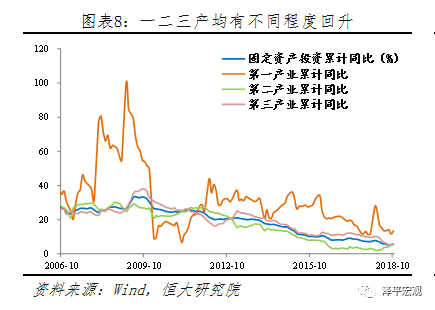

4. The growth rate of fixed asset investment rose slightly but remained sluggish, mainly supported by manufacturing investment. The low M2 level and the downward trend of social finance indicate that investment growth is difficult to rise in the short term

From January to October, the nominal growth of fixed asset investment was 5.7% year on year, 0.3 percentage points higher than that of the previous month. In terms of industries, both primary and secondary industries have rebounded to varying degrees, and the growth rate of tertiary industry has recovered slightly. From January to October, the investment in primary industry was 13.4% year on year, 1.7 percentage points higher than that from January to September; Investment in secondary industry was 5.8% year on year, 0.6 percentage points faster than that from January to September, and maintained a recovery trend under the support of manufacturing investment. Investment in tertiary industry was 5.4% year on year, and the growth rate stopped falling, rising 0.1 percentage point. In terms of regions, investment in the eastern region increased 5.8% year on year, unchanged from January to September; Investment in the central and western regions increased by 9.9% and 3.2%, with growth rates increasing by 0.3 and 0.9 percentage points; Investment in Northeast China increased by 0.9%, and the growth rate dropped by 0.8 percentage points.

From the perspective of investors, private investment has generally kept accelerating. From January to October, private investment was 8.8% year-on-year, 0.1 percentage points higher than that from January to September, the highest point since 2016.

From the perspective of three types of investment, infrastructure investment rebounded at the bottom, manufacturing investment continued to rise, and real estate investment fell at a high level.

From the historical data, M2 has a strong correlation with fixed asset investment. At present, M2 is at a historical low, indicating that the growth rate of fixed asset investment is difficult to rise in the short term.

5. Investment in real estate sales fell back, financing situation remained tight, and real estate enterprises accelerated pre-sale collection

The sales area of real estate from January to October was 2.2% year on year, down 0.7 percentage points from January to September. In terms of single month year-on-year growth, the sales area of real estate in October was - 3.1% year on year, continuing the downward trend, with negative sales growth in the same month for two consecutive months. As the effect of early real estate enterprises accelerating high turnover and monetization resettlement of shed reform faded, real estate sales gradually fell back. In terms of regions, the sales area of commercial housing in the eastern, central, western and northeastern regions from January to October was - 4.7%, 8.7%, 8.6% and - 4.7% respectively, down 0.4, 1.5, 0.3 and 1.2 percentage points respectively from January to September. Under the background of tightening monetary resettlement for shantytown reform, rising personal housing loan interest rate, continuous increase in real estate regulation, and decline in residents' income, the sales area of the country, especially the third and fourth tier real estate, will gradually decline year-on-year.

The funds in place of real estate enterprises are still mainly from sales receipts (residents' own funds for house purchase). Loan financing continues to grow negatively year-on-year, and financing pressure continues to increase. From January to October, the paid in capital of real estate enterprises was 7.7% year on year, down 0.1 percentage points from January to September. Among them, domestic loans were - 5.2% year on year, personal mortgage loans were - 0.9% year on year, self raised funds were 10.8% year on year, and deposits and advance receipts were 16.3% year on year.

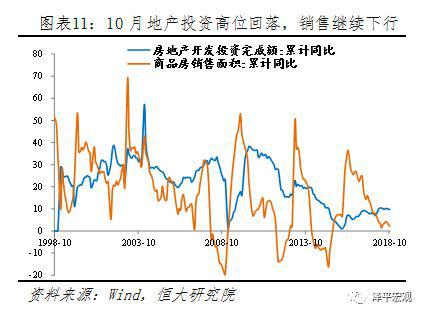

The high level of real estate investment fell for three consecutive months, and in the later period, it will decline due to financing pressure, the monetization of shantytown reform, the decline of sales, the increase of land auctions, stricter regulation and other factors. The growth rate of newly started construction area is high, while the growth rate of completed construction area is declining, and real estate enterprises are accelerating pre-sale payment collection. Real estate investment from January to October was 9.7% year on year, 0.2% lower than that from January to September. Among them, the real estate investment in October was 7.7% year on year, 1.2 percentage points lower than that in September. From January to October, the newly started area fell 0.1 percentage points to 16.3% year on year, still growing at a high speed, and real estate enterprises are accelerating their high turnover; The construction area increased by 4.3% year on year, 0.4 percentage points higher than that from January to September; The completed area of houses decreased by 12.5% year on year, with a decrease of 1.1 percentage points. This is because the real estate enterprises are accelerating to obtain pre-sale qualification payments. At the same time, land auctions continued to increase. From January to October, 1139 residential land auctions were conducted nationwide, including 13 in the first tier cities; 254 second tier cities, up 179% year on year; There were 872 land auctions in third and fourth tier cities, up 23% year on year. Land auctions are due to the great financing pressure of real estate enterprises and the increase of cities with price limits. With the attitude of the central government to resolutely curb the rise of house prices, enterprises' land acquisition behavior is more rational, and the local government has not substantially reduced the land auction price. Land auctions will lead to the decline of subsequent real estate investment, the decrease of land transfer income, and the limited source of capital for infrastructure.

6. Manufacturing investment is at a new high in the past three years, and the production capacity is verified in a fresh cycle, but the downstream private enterprises are squeezed

From January to October, investment in manufacturing continued to rise year on year, and investment in high-tech and equipment manufacturing continued to accelerate, which is the main force to accelerate investment in manufacturing. From January to October, the investment in manufacturing industry rose by 9.1% year-on-year for seven consecutive months, 0.4 and 5.0 percentage points faster than that of last month and the same period last year, respectively, and was at the highest level since August 2015. Among them, investment in high-tech manufacturing industry and equipment manufacturing industry increased by 16.1% and 11.1% respectively year on year, with the growth rate accelerating by 1.2 percentage points, 10.4 and 5.4 percentage points faster than the total investment respectively.

On the basis of profit accumulation and capacity utilization improvement, the new capacity cycle is verified and the investment structure is optimized. Investment in computer communication, special equipment manufacturing and metal products increased by 19.5%, 15.8% and 16.4% year on year respectively, 1.2, 1.9 and 0.9 percentage points faster than that of last month respectively. Investment in automobile manufacturing increased by 3.2%, 1.9 percentage points higher than that of last month. However, downstream industries, such as agricultural and non-staple food processing, textile, chemical raw materials and products, and pharmaceutical manufacturing, still face survival difficulties with investment growth rates of - 1.7%, 4.5%, 2.8%, and 1.9%, and the effects of a series of policy rescues need to be further demonstrated. From the perspective of industry, the upstream resource industries are dominated by state-owned enterprises, and the industry concentration has further increased significantly after the overcapacity and environmental storm. The downstream manufacturing industry is dominated by private enterprises, facing the double squeeze of excessive upstream price increases and financial deleveraging discrimination. Private enterprises have been given high priority at present due to their survival difficulties, the mismatch of social resources and the decline of total factor productivity. First, from the perspective of profits, the profits of state-owned enterprises and private enterprises from January to September were 23.3% and 9.3% respectively. The industries with high profit growth include oil and gas exploitation (400.6%), ferrous metal smelting (71.1%), non-metallic mineral products (44.9%), and oil and coal processing (30.8%), which are mostly concentrated in upstream state-owned enterprises and are in a monopoly position. Low or even negative profit growth is found in textile (2.7%), furniture (4.0%), metal products (4.6%), automobile manufacturing (- 3.8%) and other fields with more middle and downstream private enterprises, which are distributed in industries with more competition. On the one hand, the competition in this field is fierce and it is difficult to raise the price; on the other hand, it is squeezed by the high cost of raw materials in the monopoly industry of upstream state-owned enterprises, which makes it difficult to operate. Second, from the perspective of financing, private enterprises are at a disadvantage compared with state-owned enterprises in terms of the amount and price of financing, and financing of private enterprises is more discriminated against against against against the backdrop of declining liquidity. According to grassroots research, large state-owned enterprises can still enjoy a benchmark loan interest rate of about 6%, while even listed private enterprises have a financing cost of more than 10%. From January to September, the interest expenditure of industrial private enterprises grew by 11.8% year on year, higher than the 6.7% of the interest expenditure of state-owned enterprises year on year. Third, from the perspective of the target of policy implementation, hard indicators such as capacity reduction and environmental protection limit are more likely to lead to the passive exit of private enterprises that lack the right to speak, and private enterprises will pay the bill.

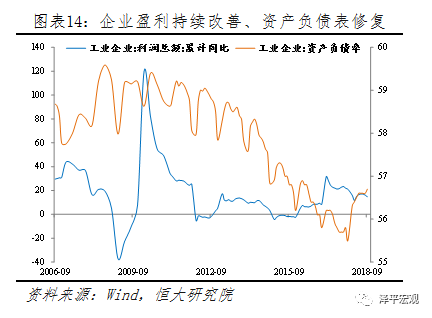

In 2016-2017, the investment in the manufacturing industry has reached the bottom, but the new capacity has been restricted due to the restrictions of banks on lending to the "two high and one surplus" industries, environmental protection supervision, supply side capacity reduction, etc. From January to September, the profits of industrial enterprises increased by 14.7% year on year, 1.5 percentage points slower than that from January to August, the second highest point this year. With capacity clearing, capacity utilization rate increasing, corporate profitability improving, and balance sheet repair, we expect to start a new round of corporate capital expenditure cycle around 2019. However, due to the downward pressure of the financial cycle, the future range will not be too large. The new round of capacity investment in the future is more with the connotation of a new era, new cycle and new economy, representing the high-end manufacturing of the future with high-quality development.

7. The growth rate of infrastructure investment rebounded at the bottom, and the rebound was supported by "stabilizing investment" and "reinforcing weakness" in the future, but the range was limited

Broad finance is still tight, but spending accelerated from September to October, and the growth rate of infrastructure investment hit the bottom and rebounded. From January to October, the growth rate of infrastructure investment (excluding water, electricity and gas) was 3.7%, 0.4 percentage points higher than that of last month, the first recovery in this year. After considering water, electricity and gas, the large-diameter infrastructure increased 0.6 percentage points to 1.3% compared with the previous month, far lower than 15.9% in the same period last year and 14.9% in the whole year last year. The growth rate of infrastructure construction in the current month was 3.3%, up 7.5 percentage points from - 4.2% in the previous month. In terms of industries, the cumulative investment in water, electricity and gas from January to October was - 9.6% year on year, 1.1 percentage points higher than that of the previous month; the cumulative investment in transportation, storage and water conservancy and environmental protection was 4.6% and 2.1% year on year respectively, 1.4% higher and 0.1% lower than that of the previous month. Among them, the investment in road transport industry increased by 10.1%, with the growth rate increasing by 1.2 percentage points; Investment in railway transportation industry dropped by 7%, with a decrease of 3.5 percentage points, and some effects were achieved by making up for weaknesses.

Since this year, financial constraints on infrastructure have been obvious. With the completion of the issuance of local special bonds, the infrastructure is expected to rebound, but the increase is limited. Since this year, the state has made adjustments to value-added tax, personal income tax, tariff and corporate income tax in terms of reducing tax rates, raising the threshold and expanding the proportion of R&D expenses added and deducted. The effect of tax reduction and fee reduction is reflected in the second half of the year. In October, the growth rate of fiscal and tax revenue turned negative, respectively - 5.1% and - 3.1%. The growth rate of fiscal expenditure was low from May to August. In September and October, the growth rate of expenditure increased to 11.7% and 8.2%. From January to October, the cumulative year-on-year growth rate of expenditure was 7.6%, but still lower than the 9.8% of the same period last year. The year-on-year growth rate of fiscal expenditure for infrastructure projects such as agriculture, forestry, water and transportation rose to 9% and 3.9% in October, still low. At the same time, financial clean-up and rectification continued to strengthen, the financial situation became tighter, and the funds invested in infrastructure projects such as PPP, government purchase of services, and non-standard projects decreased. The meeting of the Political Bureau and the executive meeting of the State Council in late July called for more proactive fiscal policies To play a greater role in restructuring and expanding domestic demand; At the meeting of the Political Bureau at the end of October, the six stabilities were raised again; On October 31, the Office of the State Council issued the Guiding Opinions on Maintaining the Strength of Shortcomings in the Field of Infrastructure, which proposed that efforts should be made to complement the weaknesses in the fields of railways, roads, water transport, airports, water conservancy, energy, agriculture and rural areas, ecological environmental protection, public services, urban and rural infrastructure, shantytown reconstruction and other fields, and accelerate the promotion of major projects that have been included in the plan. With the completion of the cleaning up of non compliant projects in the early stage, the implementation of compliance projects has been accelerated, and the issuance of new bonds for local government special bonds in the current year has been completed and funds have been put in place. The State Council requires that the projects under construction should not be blindly withdrawn. The year-on-year rebound of infrastructure investment is expected to continue, but the recovery rate is limited.

8. Low consumption, upgrade and demotion reflect social stratification, declining liquidity and downward pressure on the economy

The growth rate of consumption is still low, at the low point since 2003, which is mainly affected by the decline of income growth and the squeeze of debt such as housing loans. In October, the total retail sales of consumer goods grew by 8.6% in nominal terms on a year-on-year basis, 0.6 percentage points lower than that of the previous month, and the actual growth rate was 5.6%, the lowest since 2003. The cumulative growth rate from January to October was 9.2%, down 0.1 percentage points from the previous month, which was related to the delayed consumption of the "Double 11" promotion. On the whole, the growth of consumption slowed down. On the one hand, affected by the slowing growth of residents' income, the nominal growth rate of per capita disposable income of residents in the first three quarters was 7.9%, down 0.4 percentage points compared with the same period last year; On the other hand, the debt to disposable income ratio of China's household sector exceeds 100%, and the household debt/GDP reaches 48%, squeezing consumption. Since this year, the main drag on consumption has been automobiles. The sales volume in October was - 6.4% year on year, and the cumulative sales growth rate from January to October was - 0.6%. This year, the vehicle purchase tax was resumed at the rate of 10%, and the preferential policies were canceled, hitting some market demand.

From the perspective of structure, the consumption of new business types and upgrading types still maintains rapid growth, consumption upgrading and downgrading coexist, and the characteristics of consumption grading are obvious. From January to October, the national online retail sales increased by 25.5% year on year. The sales of upgrading commodities grew rapidly From January to October, among the retail sales of commodities above the designated size, the retail sales of cosmetics and communication equipment increased by 11.4% and 10.4% respectively year on year, 2.2 and 1.2 percentage points faster than the total retail sales of consumer goods.

In the short term, the consumption of some middle - and low-income people has been downgraded, liquidity ebbs, high rigid debts, housing rents and medical prices have risen significantly, and consumption has been downgraded, which is mainly reflected in the decline in the proportion of entertainment and cultural consumption compared with last year, and is concentrated in the middle class, For example, people such as middle-class white-collar workers with high debt who buy houses with leverage and urban workers who rent first and second tier houses (neither property income nor financial transfer income guarantee obtained by people with similar minimum income). According to the division of five equal incomes, the income growth of high income households has increased year by year, while the income growth of lower middle income households, middle income households and upper middle income households has continued to decline. The slowest growth in 2017 was that of lower middle income households, which was 7.3%. The gap between the rich and the poor has risen for two consecutive years, and the consumption classification characteristics between urban energy levels and high-income groups are obvious. The world's largest luxury consumption country coexists with Pinduoduo, which prevails in the third and fourth tier cities and below. High growth of high-quality automobile consumption coexists with low growth or even negative growth of middle and low grades. The price of high-end liquor continues to rise, and competition for low-end liquor is fierce. The above phenomenon needs to be highly valued.

On the whole, in the long run, the trend of consumption upgrading continues, and the Engel coefficient continues to decline to below 30%. However, in the short run, the consumption of some low-income people is degraded. The consumption growth rate in October was still weak, which was related to the decline in the growth rate of residents' income, the decline of the stock market, the explosion of P2P, and the high debt of housing loans. China's economy is entering a stage of consumption led economic development, with heavy macro tax burden, high housing prices, high medical education costs and other constraints. It is urgent to deepen reform and opening up. The proportion of service industry in GDP has exceeded 50%; The growth rate of consumption has exceeded that of fixed asset investment; GDP per capita is about 8800 US dollars; Upgrading from housing and transportation to service consumption and a better life; The huge market and scale effect of 1.39 billion people; The gradient effect of the first, second, third, fourth, fifth and sixth tier cities.

9. Both imports and exports rose sharply on a year-on-year basis, and exports may decline significantly after the "scramble for exports" effect disappears

In October, both imports and exports rose sharply year on year, and the effect of seizing exports still exists but the margin is weakened. The export in October was 15.6% year on year, 1.2 percentage points higher than that in the previous month. In terms of countries and regions, exports to developed economies in the United States, Europe and Japan declined year on year, down 0.8, 2.8 and 6.4 percentage points respectively from the previous month, of which the growth rate of exports to the United States was 13.2%. Exports to Hong Kong, Taiwan, South Korea, and emerging economies such as India, Brazil, and Russia have increased to varying degrees, reflecting that the production of exports to the United States and early orders is still continuing, but this effect will gradually weaken over time; It also reflects that under the background of trade friction, Chinese enterprises bypass Hong Kong, China for export, and gradually open up markets outside Europe and the United States.

Although exports continued to rise sharply, all signs showed that there was great downward pressure on exports in the later period. First, Shanghai's comprehensive index of export container freight rates was relatively stable (22.9% year-on-year in October), but the prices of the West America and East America routes soared to 79.9% and 77.4% year-on-year, resulting in tight shipping. Second, global external demand continued to weaken in October, and new export orders fell below the boom and bust line for five consecutive months, hitting a three-year low. Third, the global economic margin slowed down. The global manufacturing PMI was 52.1%, falling for six consecutive months and at the lowest point since November 2016. The PMI of manufacturing industry in the United States and Europe was 57.7% and 52.0% respectively, down 2.1 and 1.2 percentage points from the previous month, and the PMI of Europe was the lowest since September 2016; The PMI of Japan's manufacturing industry was 52.9%, a slight increase of 0.4 percentage points over the previous month. As the U.S. economy has peaked, the economic margin of the euro area has declined, the risk of emerging economies has expanded, and foreign demand has weakened. The United States has imposed 10% tariffs on China's exports of $200 billion since September 24. The phenomenon of seizing exports has ebbed, and the impact of trade frictions will gradually emerge, exerting downward pressure on China's exports.

Imports rose more than expected, and the Expo released a positive signal that China's trade surplus will narrow in the future. The import in October was 21.4% year on year, up 6.9 percentage points from the previous month. The reason for the sharp increase in imports is that infrastructure construction has supplemented weaknesses to boost demand, environmental protection has limited production, which has led to a sharp increase in demand for bulk commodities and an increase in oil prices. The trade surplus in October was US $34.02 billion, an increase of US $2.74 billion over the previous month. Recently, China has accelerated the introduction of a series of import expansion policies. In July, the Ministry of Commerce officially released the Opinions on Expanding Imports to Promote Balanced Development of Foreign Trade. The first Import Expo was held in Shanghai on November 15. The General Secretary proposed that in the next 15 years, China's imports of goods and services will exceed 30 trillion US dollars and 10 trillion US dollars respectively, and the future import growth will rise, To meet the people's needs for a better life, the trade surplus will narrow.

10. The Sino US trade friction has moved from confrontation to relaxation in the short term, but it is still severe in the long term. The best response is reform and opening up

Objectively speaking, at the beginning of Sino US trade friction, both sides made obvious miscalculations:

11. CPI rose moderately and PPI continued to fall

With the disappearance of short-term supply shocks, the basic completion of "capacity reduction" and the relaxation of environmental protection margins, CPI and PPI are expected to be moderate on the whole. However, in the first half of next year, attention should be paid to the role of rising pork prices caused by the superposition of pig cycle and swine plague on inflation.

China's CPI in October was 2.5% year on year, expected to be 2.5%, the previous value was 2.5%; PPI was 3.3% year on year, expected to be 3.3%, and the previous value was 3.6%. CPI is rising moderately at present, and the periodic factors that affect CPI rising in the earlier stage are gradually fading away In terms of food prices, the prices of vegetables, pork and eggs dropped. The main vegetable producing areas resumed supply, autumn vegetables and winter stored vegetables came into the market, and vegetable prices fell 3.5% month on month; The production capacity of laying hens increased, and the price of eggs fell 3.3% month on month; The recent rise in pork prices has eased. In terms of non food prices, the rise in domestic oil product prices in early October led to an increase in energy prices. Gasoline, diesel, coal and liquefied petroleum gas were the main factors driving the rise in non food prices, which rose by 4.2%, 4.7%, 2.9% and 1.8% respectively. The four factors together affected CPI growth by about 0.12 percentage points. Recently, the United States imposed sanctions on Iran, but exempted 8 countries, including China, South Korea and Japan, mainly for the purpose of curbing the rapid rise of oil prices. However, considering the uncertainty of the situation in the Middle East, the oil price may fluctuate at a high level in the later period. At present, the inflation pressure is not large, which will not restrict the monetary policy, but we need to pay attention to the pressure of African swine plague on inflation. At present, the response of the market to African swine fever is passive, but the epidemic has not been effectively curbed, and the scope of the epidemic has expanded to 14 provinces. In the provinces greatly affected by the epidemic, consumption decreased and pig prices fell, while in the provinces not affected for the time being, pig prices continued to rise in the previous period. As the end of the year approaches, the demand for pork will gradually increase. In order to prevent the spread of the epidemic, the trans provincial transfer of pigs has been limited recently, and the price of pigs in Northeast China has begun to rise again. In the medium and long term, after a long period of low prices, the excess capacity accumulated in the previous round of pig cycle has been fully depleted under the dual role of the market and environmental protection. The momentum of rising pig prices has gradually accumulated, entering a new round of rising cycle. As the supply gap caused by the epidemic superimposes the pig cycle, the pig price will face strong upward pressure in the first half of next year, and its role in boosting inflation cannot be ignored.

PPI rose 0.4% month on month, but the year-on-year growth rate narrowed to 3.3% driven by the high base effect, which was in line with expectations. In October, PPI rose mainly driven by the oil and natural gas exploitation and processing industries, up 6.3% and 3.1% month on month respectively, reflecting the role of oil prices in driving PPI. At the margin, the ferrous metal smelting and rolling processing industry has a more obvious downward effect. The month on month growth rate in October was 0%, down 1.5 percentage points from the previous month. At present, the spot price of rebar and other major steel industrial products is still at a high level, but the futures price has declined significantly recently, reflecting the cautious attitude of the market towards the total demand next year. Considering the marginal relaxation of environmental protection policies this year and the improvement of the supply situation compared with last year, the price increase of industrial products is likely to further slow down. With the high base effect of last year, the year-on-year growth slowdown of PPI may continue.

On the whole, the price difference between CPI and PPI is expected to be further narrowed or even inverted next year. The rise of CPI will be more from the supply side, while the decline of PPI will be more from the demand side. This will bring some challenges to the monetary policy next year. The central bank needs to closely follow the price situation. From the perspective of the current policy trend, the central bank will give priority to stable growth when there is still room for inflation. Later, it will not rule out the possibility of a small increase in the desired inflation level.

12. PMI of the manufacturing industry dropped to a new low in two years, and new orders, especially new export orders, declined significantly, showing the impact of trade friction

In October, the PMI of China's manufacturing industry was 50.2%, a new low in two years. The index of new orders, especially new export orders, fell below the boom and bust line for five consecutive months, a new low in nearly three years. PMI sub indicators show that production, internal and external demand, and expectations are all down. From the perspective of index composition, the expected index of production and business activities was the lowest in two years, and the economic momentum index (new orders inventory) fell for five consecutive months.

New orders, especially new export orders, reached a 33 month low, indicating weak external demand, On September 24, the US imposed tariffs on 200 billion yuan worth of goods in China. From January to September this year, the export growth rate was as high as 12.2%, including 13%, 11.6% and 8.5% of exports to the United States, Europe and Japan, which is related to enterprises' competition for exports. The future export situation is grim. First, Shanghai's comprehensive index of export container freight rates was relatively stable (21.6% year-on-year at the end of September), but the prices of the West America and East America routes rose sharply to 65% and 67% year-on-year, resulting in tight shipping between China and the United States. Second, the export delivery value has risen significantly for three consecutive months, including the export delivery value of computer communication electronic equipment, which has risen significantly since June (1.5% in June, 10.4% in July, and 17.3% in August). Third, the global economic margin slowed down, and China's exports rose against the trend. In September, the surplus with the United States reached an all-time high of $34.1 billion.

The import index fell to 47.6% for five consecutive months and below 50% for four consecutive months, reflecting the downturn in domestic demand and production activities.

From the perspective of the industry, cars are a big drag. Among the 21 industries surveyed by PMI, only 13 industries maintained PMI above the boom and bust line. Among them, the PMI of agricultural and sideline food processing, refined tea for food and alcohol drinks, textile, clothing and clothing, medicine and other manufacturing industries are all at a high operating level of more than 53.0%, with a rapid growth rate; The PMI of textile industry, automobile manufacturing industry and other industries is in the contraction range, with year-on-year and month on month declines.

From the price point of view, the price index has retreated, and PPI is expected to fall back. As the purchase price falls less than the factory price, the profits of middle and lower reaches and private enterprises are still squeezed. The purchase price index and ex factory price index of main raw materials were 58.0% and 52.0%, respectively 1.8 and 2.3 percentage points lower than that of the previous month, easing the pressure of price rise. However, the difference between the two has expanded to 6.0 percentage points, indicating that the increase in the purchase price of raw materials in the manufacturing industry continues to exceed the ex factory price of products, and the difference between the profit growth of private economy, which is relatively concentrated in the middle and lower reaches, and the profit growth of state-owned enterprises, which are dominated by the upper reaches, continues to expand.

From the perspective of enterprises of different scales, large enterprises are still the main body supporting the manufacturing industry. The PMI of large enterprises was 51.6%, down 0.5 percentage points from the previous month, and continued to expand; The PMI of small and medium-sized enterprises was 47.7% and 49.8%, down 1.0 and 0.6 percentage points respectively from the previous month, lower than the critical point.

The PMI of non manufacturing industry fell back, but the business activity index, new order index, employees and business activity expectation index of the construction industry rose, which was related to the infrastructure weakness. The non manufacturing business activity index was 53.9%, down 1 percentage point from the previous month. It was still in the expansion range, but the expansion rate slowed down. The index of new orders was 50.1%, down 0.9 percentage points from the previous month. It is worth noting that the construction industry continues to operate at a high level. Under the circumstances that a large number of special bonds have been issued, financial expenditure has been accelerated, and the State Council has identified specific areas to address weaknesses, infrastructure will stabilize and recover, driving the construction industry's business activity index, new order index, employee index, and business activity expectation index up to 63.9%, 56.2%, 54.1%, and 66%, respectively, 0.5, 0.5, 0.2 and 0.9 percentage points higher than last month.

(The author of this article introduces: Chief Economist of Evergrande Group, President of Evergrande Economic Research Institute. He once served as Deputy Director of the Research Office of the Macro Department of the Development Research Center of the State Council, Director General Manager and Chief Macro Analyst of Guotai Jun'an Securities Research Institute.)