Article/Liang Hong, columnist of Sina Financial Opinion Leader Column (WeChat official account kopleader)

The "grey rhinoceros" on the long-term development path of China's economy is our extremely high savings rate and the "intestinal obstruction" of the investment and financing system that converts savings into investment. To prevent this "grey rhinoceros", China's policies should focus on two aspects: first, how to reduce some inefficient or forced savings, so as to structurally increase the proportion of consumption in total demand. The core part is to transfer state-owned assets to enrich social security, so as to significantly reduce the payment rate of five insurances and one fund. The second is how to improve the system and mechanism of converting savings into effective investment. The institutional defects of the A-share market have become the bottleneck of many reforms, which need to be broken through urgently.

The policy of deleveraging often backfires?

The rising leverage ratio in China has always been the focus of investors and policy makers. Scholars often use the ratio of debt to GDP to indicate China's monetary overissuance and rising leverage ratio, because this ratio has been rising in most years in the past three decades. However, its rising speed is not balanced, and it is negatively related to economic growth, that is, when economic growth declines, the growth of leverage ratio is accelerated [1]. That is to say, China's practical experience over the past two decades does not support the proposal to reduce leverage by reducing economic growth. On the contrary, during the period of economic slowdown after 1997 and 2008, the leverage ratio rose rapidly, while during the period of high growth in 2003-2007, the ratio even declined. In 2017, with the economic stabilization and recovery, the growth rate of debt/GDP ratio also began to slow down significantly. However, the re tightening of the financing environment in the first half of this year led to the passive rise of leverage of SMEs, private enterprises, etc.

This seemingly paradoxical phenomenon reflects an important structural imbalance in China's economy: the contradiction between the rapid development of the real economy and the high savings rate and the serious lag in the development of the financial system. The debt/GDP ratio itself is not the cause of inefficient growth caused by high leverage, but the performance of mismatch between high savings rate, high growth and underdeveloped financial markets, especially equity financing markets. The reason is simple. Due to the lack of effective equity financing channels, when the economy goes down, the ability of enterprises to supplement capital with profits declines, and China's high savings rate naturally shows that the proportion of debt financing in the overall financing increases.

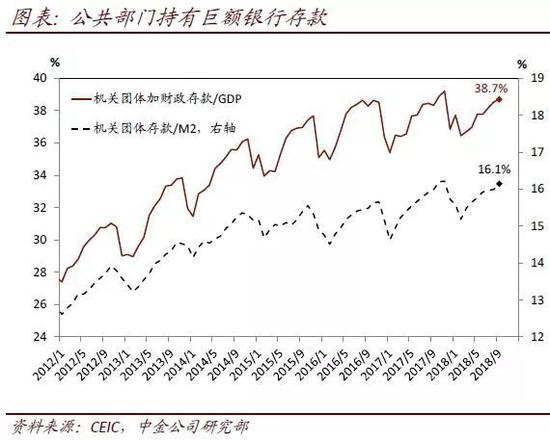

In addition to the lack of effective equity financing channels, the rise of the government savings rate in the past five years is also an important factor leading to the rise of China's overall leverage ratio. China's public sector (including governments at all levels and various public institutions, but excluding state-owned enterprises) holds a huge amount of bank deposits - financial deposits (5.2 trillion yuan) plus institutional deposits (29 trillion yuan) - which account for more than 30% of GDP. Moreover, the growth rate of these public sector bank deposits is also far higher than the nominal GDP growth rate or the growth rate of residents' and enterprises' deposits. In these deposits, there are not only a large amount of financial surplus settled down, but also a large number of "small coffers" of various public institutions. The social pension insurance fund and housing accumulation fund also account for about 20%. The high-speed accumulation of government deposits has reduced consumption and investment in the current period, resulting in inefficient "excess savings" in fact.

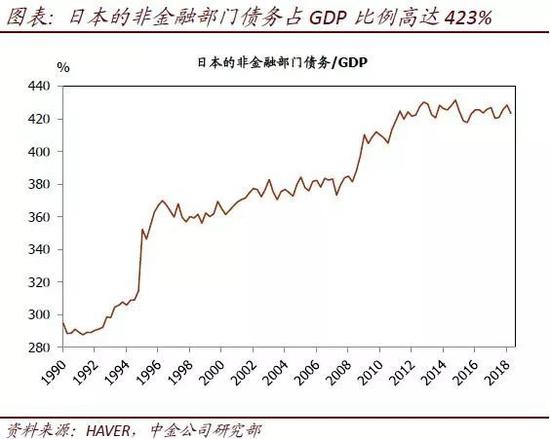

The "grey rhinoceros" on the long-term development path of China's economy is our extremely high savings rate, which superimposes the "intestinal obstruction" of the investment and financing system that converts savings into investment, Eventually, it will inevitably lead to the continuous decline of the rate of return on investment. If we do not change the current situation of China's high savings rate and the extreme lack of development of equity financing in the market, but try to use monetary policy or other short-term liquidity tightening policies to adjust structural problems, it will certainly backfire. Japan is a lesson for China: today its non-financial sector debt accounts for 423% of GDP, and its economic growth has stagnated for 20 years, but there has never been a debt crisis like that of countries with low savings rates (such as the United States).

We believe that, China's policy efforts to prevent this "grey rhinoceros" should focus on two aspects: first, how to reduce some inefficient or forced savings, so as to structurally increase the proportion of consumption in total demand, the core part of which is to transfer state-owned assets to enrich social security, so as to significantly reduce the payment rate of five insurances and one fund; The second is how to improve the system and mechanism of converting savings into effective investment. The institutional defects of the A-share market have become the bottleneck of many reforms, which need to be broken through urgently.

Revitalize stock assets

Use the "addition" reform to reduce savings rate and leverage

Although the current short-term growth of China's economy and the medium - and long-term structural problems are facing serious challenges, compared with 20 years ago, the government now has a large number of assets, including cash, providing China with more space to cope with the pressure of short-term growth and the pain of structural adjustment. Timely and effectively promoting the reform focusing on revitalizing the existing government assets and "adding" the income of enterprises and residents will not increase the debt risk, but can also expand the total demand in a high-quality way, so as to address both the symptoms and short-term debt risks.

1. Reduce inefficient or forced savings to effectively increase consumption rate and control the growth of macro leverage

A large number of economic studies have found that savings is an economic variable with high viscosity, obvious structural characteristics, and very small short-term changes. Population structure and economic growth are the most important factors that determine the overall savings rate of a country:

1) First of all, China's one-child policy and the early retirement age have a greater impact on the continuous improvement of the residents' savings rate since the early 1990s.

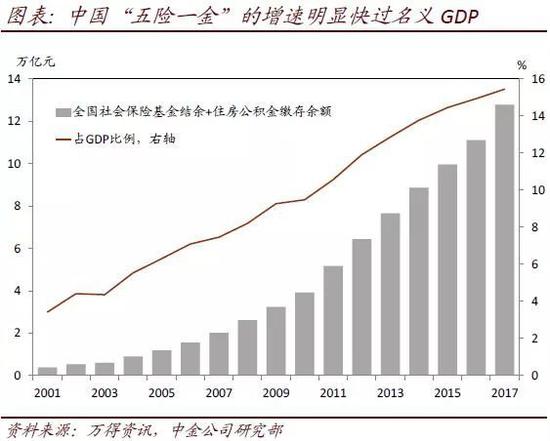

2) Second, since the late 1990s, the "five insurances and one fund" collected by the government from the income of enterprises and individuals has become the fastest growing part of the savings rate. With more and more working people paying "five insurances and one fund", the growth rate of this part has far exceeded the nominal GDP. At the same time, since the main deposit mode of "five insurances and one fund" is bank deposits, this part of savings can only be converted into investment through the bank in the form of creditor's rights, that is, the arrangement of "five insurances and one fund" has inadvertently become the institutional driver of the rising debt to GDP ratio.

3) Finally, since 2012, with the anti-corruption and strict control of public expenditure, the collection of taxes and fees has not been curbed from the source, and the bank deposits of government agencies and groups have also precipitated at a growth rate far higher than the nominal GDP, resulting in the rise of the savings rate of the government departments in fact.

Therefore, to reduce inefficient or forced savings, China should focus on revitalizing the stock of government assets, including cash deposits, to curb all kinds of arbitrary charges at the source, while significantly improving the efficiency of the use of funds. This is a way to reduce leverage by "adding" the income of enterprises and residents at the same time. These policy options include:

► Transfer state-owned assets to enrich social insurance, thus greatly reducing the payment rate of five insurances and one fund.

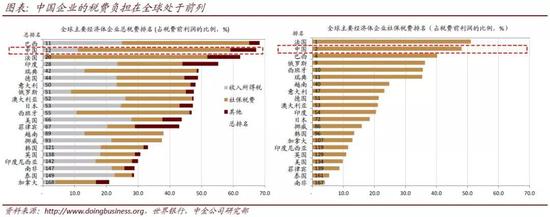

World Bank data show that the comprehensive tax burden of Chinese enterprises ranks 12th among 189 countries in the world, with the social security tax burden ranking second. The high social security rate is equivalent to compulsory savings, which will restrain the entity investment and consumption, and the negative impact is more prominent in the current macro context. This year, the United States has significantly reduced the corporate income tax rate by more than 10 percent, compared with China's 1 or 2 points of tax and fee reductions. We believe that the space for tax and fee reduction in the future mainly lies in the social security payment of "five insurances and one fund".

The 28% contribution rate of China's pension is far higher than the international level, which is more than twice the contribution level of the United States. This is mainly to deal with the problem of empty accounts at the beginning of the establishment of the basic old-age insurance system for enterprise employees. However, it has also brought a long transition period and heavy historical debt burden. This kind of historical debt is reasonable to be solved by transferring state-owned assets to enrich social security, and has the effect of "one stone and three birds", that is, to promote the in-depth governance reform of state-owned enterprises, reduce the social security rate, ease the pressure of enterprises, and cultivate a healthy capital market.

The dividend income after the transfer of state-owned assets enables the social security fund to have a stable source of funds every year, which can be used for investment and operation, or make up for the reduction of the collection income after the rate reduction. At the end of 2017, the owner's equity of state-owned non-financial and financial enterprises totaled 75 trillion yuan. Assuming a dividend yield of 3%, every 4 percentage points of transferred state-owned assets can support a 1 percentage point reduction in the rate. If the social security rate can be reduced by 10 percentage points, it will effectively improve the international competitiveness of Chinese enterprises, boost the proportion of consumer demand in the national economy, and hedge the negative impact of the US tariff.

► Take out some external reserves or financial balances to directly inject equity capital into important infrastructure projects or systemically important departments (such as banks, stock markets, social security).

In 2004, China used about $80 billion of the then $400 billion in foreign exchange reserves to inject equity capital into large state-owned banks. This capital injection has not only achieved good commercial returns (according to the estimation of Huijin Company, the original investment of 80 billion dollars has now increased to more than 420 billion dollars), but more importantly, this action Bank of China The system has been restored to health, enabling residents' savings to be converted into investment in the real economy again and more efficiently.

► Reform the budget preparation and implementation process, and strengthen the reform of the fiscal and taxation system.

Reduce the size of idle cash held by the central government and the size of "small vaults" of government agencies and groups. In particular, we should reform the public institutions that actually engage in commercial operations, which is of great significance to reduce the inefficient "savings surplus" of the public sector. In recent years, the government's work plan has repeatedly stressed the need to increase the active stock of financial funds, but at present, the deposit of government organizations is still on the rise.

► Invest some government or public savings in other assets with higher return rate than bank deposits.

Historically, social pension insurance funds and housing provident funds were only allowed to be deposited in banks or purchase national bonds. Recently, social security fund investment has gradually moved towards market-oriented investment, and three provinces and cities have begun to pilot tax deferred pension insurance. Looking ahead, there is still much room for improvement in the allocation of these funds, such as the reform of the provident fund system and the acceleration of tax deferred pension insurance.

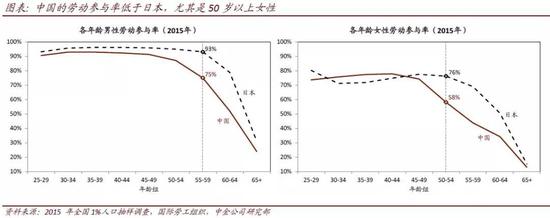

► Liberalizing the birth policy and gradually extending the retirement age to the international universal level will help reduce the savings rate and reduce the pressure of increasing investment and financial leverage at the source.

The legal retirement age of 50 years old women and 55 years old men in China is quite different from that of most countries in the world. The labor participation rate of women over 50 years old is even far lower than that of Japan.

2. The institutional defects of the A-share market have become the bottleneck of many reforms and need to be broken through

China's stock market, which has been established for more than 20 years, has experienced ups and downs, and system construction, innovation and opening up have never stopped. However, the long-term depressed stock index and sudden huge adjustment also highlight the lag and inadequacy of China's stock market infrastructure construction. China urgently needs to promote the real reform of the system and mechanism in the construction and improvement of the basic market system, instead of continuing to make short-term repairs to deep problems by means of Band Aids.

1) The lagging reform of the stock market system has become the bottleneck of other reforms.

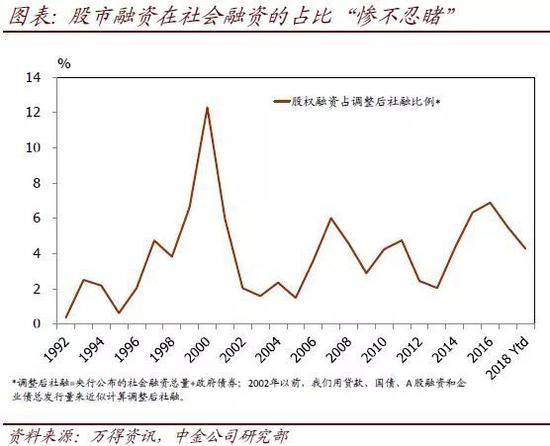

Equity financing is the only way to reduce leverage in China's economy. However, in recent years, compared with the huge demand for debt financing, the amount of equity financing of A-shares has always been a drop in the bucket.

A-share has again become the bottleneck of state-owned enterprise reform. The A-share market can play an important role in the mixed ownership reform of state-owned enterprises. On the one hand, an effective stock market can optimize the allocation of resources, find market prices, and improve corporate governance, reduce disputes over the loss of state-owned assets, and promote the realization of mixed reform through the market platform. On the other hand, the stock market undertaking the mixed reform of state-owned enterprises can provide investors with more high-quality investment targets, so that all people have the opportunity to share the dividends of state-owned enterprise reform.

However, in the last round of state-owned enterprise reform, due to various constraints of the A-share market at that time, a large number of high-quality state-owned enterprises had to choose to go overseas first. Taking PetroChina as an example, when it was listed in Hong Kong in April 2000, the issue price per share was 1.27 Hong Kong dollars. From the listing to November 2007, before returning to A-share market, it created 22% of annual capital gains for overseas investors. The annual dividend ratio was as high as 45%, and the average dividend yield was 6%. Overseas investors fully enjoyed the dividends of China's state-owned enterprise reform, However, a large number of domestic investors are unable to share this opportunity. Therefore, although the last round of state-owned enterprise reform contributed a huge reform dividend to the rapid development of China in the first decade of this century, it is often criticized by investors and even questioned by the loss of state-owned assets from the perspective of domestic capital market returns.

Since the Third Plenary Session of the 18th CPC Central Committee opened this round of state-owned enterprise reform in November 2013, new progress has been made in state-owned enterprise reform from top-level design to implementation, such as the establishment of China Tower Corporation, the mixed reform of Sinopec, and the reorganization and integration of state-owned enterprises in a continuous stream. However, with the promotion of this round of state-owned enterprise reform, many high-quality state-owned enterprises after restructuring are faced with the choice of listing place. Will the chronic disease of A-share once again become the bottleneck for domestic investors to share the dividend of state-owned enterprise reform?

Under the trend of China's aging population, the stock market needs to provide Chinese residents with investment channels other than real estate. The assets of Chinese residents are concentrated on real estate and deposits, while the proportion allocated to other financial investment products is about 20% (only 5% for stocks and funds), which is significantly lower than the proportion of about 60% for American residents (32% for stocks and funds, and 21% for pensions). Under the trend of China's aging population, the profitability of the two major Chinese residents' allocation entities, real estate and savings, will be weakened in the past. Excessive investment will not be able to maintain and increase the value effectively, nor can it meet the needs of elderly care. The stock market should become a high-quality investment channel for Chinese residents.

2) What are the key points missing in China's stock market system?

If we compare the investor structure, new share issuance, delisting and repurchase system, corporate governance and investor protection of China's stock market with those of overseas mature markets, it is not difficult to find that the institutional construction of China's stock market is lacking in some key nodes.

One of the cruxes: the lack of long-term investors.

China's stock market is not short of speculators, but it is extremely short of long-term investors. Analyzing the investor structure of A-share market, the market value of individual investors accounts for 20%, and the trading accounts for 90%, which is the highest among other major markets in horizontal comparison. The development of long-term investors such as pension and annuity in China lags behind. At present, the market value of pension in the A-share market accounts for only about 1%, while the market value of pension in the U.S. market plus the indirect investment in the stock market through mutual funds and other investments account for more than 20%. The domestic pension not only did not benefit from the growth and development of the stock market, but also did not play a role in this process. China has introduced overseas institutional investors through policies such as QFII and RQFII, and achieved connectivity between the A-share market and the Hong Kong market through the Shanghai Hong Kong Stock Connect and Shenzhen Hong Kong Stock Connect. However, compared with the real economy or other emerging market countries, China's stock market is still not open enough, and there is still a long way to go to integrate into the world.

From the experience of mature overseas markets, the existence of long-term investors helps to establish an investment style that pursues long-term stable returns and improve the efficiency of market system formulation and implementation. The positive utility of institutional investors is based on a sound stock market system and ecological environment, and the development of institutional investors is also part of the continuous improvement of the stock market. Therefore, strengthening the power of professional institutional investors, developing social security pension funds internally and introducing overseas institutional investors externally have a great space for reform in both aspects, In particular, the design and launch of the basic old-age insurance system is extremely urgent.

The second crux: the loss of a good company.

Due to the lack of system in the A-share market in history, many excellent domestic enterprises have embarked on the road of overseas listing, and domestic investors are not able to fully share the rich returns brought by the growth of Chinese enterprises. The abundance of good companies in the stock market is inseparable from the market-oriented system of issuance, delisting and repurchase.

First of all, the market-oriented issuance and delisting mechanism will help reduce the time for administrative response, form a dynamic balance between supply and demand of stocks, thus helping to improve the stability of the stock market, and also help the regulatory authorities to invest more limited human and material resources in post supervision, promote the survival of the fittest, and improve the effectiveness of the law enforcement mechanism.

Secondly, delisting and issuance should form a balance. The hot issue of new shares compared with the delisting of few companies makes the A-share market "enter without exit", reducing the quality of listed companies in the A-share market, the vitality of equity trading and the efficiency of resource allocation. The stock market is a market for equity trading, which is consistent with the enterprise life cycle theory. In fact, delisting is not the standard to measure the quality of enterprises. In mature markets, well managed enterprises can also delist. The standards of the compulsory delisting system need to be specific, clear, diversified and operational. The procedures give consideration to efficiency and rhythm, and focus on fairness and flexibility, which will help improve the effectiveness of the compulsory delisting system.

The third crux: the lack of effective supervision.

In a market with insufficient supervision, it is easy for bad money to drive out good money, that is, effective supervision is actually a prerequisite for introducing good companies. According to the experience of overseas mature markets: i) The system should be designed strictly to increase the cost of violations. The United States and Hong Kong have imposed severe penalties for violations of laws and regulations in the stock market, and those who are serious will also be prosecuted for criminal responsibility. In recent years, the CSRC has strengthened the supervision and punishment of violations of laws and regulations, but the laws and regulations have not kept pace with the times. For example, the law only imposes criminal penalties on insider trading and other acts, and only administrative penalties are imposed on violations of information disclosure of listed companies, with a maximum fine of only 600000 yuan, compared with the maximum fine of 5 million dollars and the maximum imprisonment of 20 years in the United States, As well as Hong Kong's maximum fine of 10 million Hong Kong dollars and the maximum criminal punishment of 10 years' imprisonment, it is difficult to play a good warning role. Ii) Adequate supervision and law enforcement personnel shall be provided for implementation. The number of SEC law enforcement personnel in the United States accounts for 31%. If supervision and inspection departments are considered, the number of supervision and law enforcement personnel accounts for up to 53%. Considering that the A-share market is dominated by small and medium-sized investors and the market system is still under construction, the requirements for the number and efficiency of law enforcement personnel will be higher.

Summary:

We believe that the current challenges facing China's economy, on the one hand, reflect the impact of recent policies, on the other hand, reflect some deep-seated challenges faced by economic development for many years, that is, under the condition of high savings rate, the contradiction between the demand of fast growing real economy for capital financing in terms of total volume and structure and the development of the financial system. The top priority is to readjust the package of policies to stabilize growth, while fostering a smooth mechanism for the formation of long-term capital and equity capital, which can not only achieve sustainable deleveraging by consolidating the capital base, but also stabilize growth and adjust the structure, so as to address both the symptoms and the short term.

(About the author: Chief Economist of CICC)