Opinion leaders | Dai Zhifeng, Deng Meijun, Ma Zhihao

Key investment points

Core point: 1. A series of real estate policies show that the attitude of high-level policy change is clear, and the general trend is to continue to relax and determine. 2. The improvement of real estate fundamentals depends on the implementation of local governments and local state-owned enterprises, as well as the increased willingness of property buyers; It is expected to be a gradual process. 3. The strength of real estate policy is expected to be discretionary, and the bottom line thinking and risk prevention are the core considerations; The greater the fundamental pressure, the greater the strength will be. 4. In terms of investment: recently, the policy has clearly turned to improve market sentiment, which promotes the dominance of the real estate chain (such as joint-stock banks); In the medium and long term, it is expected that the strategy of high dividend yield is still dominant (high-quality urban rural commercial banks and big banks) by observing the fundamentals.

Sort out the content of the new real estate policy. 1. Adjustment of housing loan policy: The down payment ratio was lowered, the lower limit of interest rate was opened, and the interest rate of provident fund loan was lowered. 2. Regular briefing on policies of the State Council: The four departments made it clear and detailed that the housing guarantee work should be done well, and the Central Bank announced the establishment of 300 billion yuan of affordable housing refinancing.

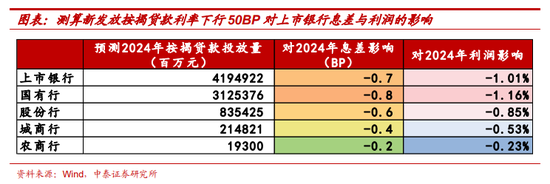

Impact of housing loan policy adjustment: the impact on bank interest margin is very limited. 1. Policy intention: Starting from the demand side and the residential sector, improve the leveraged housing purchasing capacity of the residential sector. 2. Mitigating downward pressure on the real estate market has limited impact on bank interest margin. The interest rate of commercial loans depends on the game between the bank cost and the residents' demand for housing. Suppose that the lower limit of mortgage loan interest rate pricing=debt cost+credit cost+expense cost=2.26%+0.25%+0.67%=3.2% (interest bearing debt cost is 2.26%, credit cost is 0.25%), The impact of a 50BP cut in the interest rate of newly issued mortgage loans on the annual interest margin of listed banks was 0.7BP, and the impact on profits was about 1% (The actual impact is smaller, and many cities have been adjusted due to urban policies).

Deposit collection and refinancing: help stabilize the quality of bank assets. 1. Policy intention: Stabilizing house prices and easing liquidity pressure of housing enterprises; 2. The project with a rental return rate of 1.95% or more has benefited significantly. Local state-owned enterprises will consider more in accordance with the principle of commercialization when purchasing; The pricing of such loans by banks is expected to be no less than 1.95% (refinancing interest rate 1.75%, bank debt cost 2.26%, 1.75% * 60%+2.26 * 40%); 3. To help stabilize the quality of bank assets. The liquidity injection brought by the purchase, storage and re lending has played a positive role in mitigating the risk of the real estate market. At the same time, the marginal stabilization of house prices has also led to the improvement of residents' wealth effect, both of which are conducive to the improvement of bank asset quality.

Investment suggestions: The economy determines the logic of bank stock selection. The weak and strong recovery of the economy correspond to different target varieties. Bank stocks are robust and defensive. See our annual strategy for details Vitality in steadiness - from macro to customer group and from customer group to income 。 1. High quality urban rural commercial banks have great certainty in their fundamentals, so they choose urban rural commercial banks with low valuation. We Continuous recommendation Bank of Jiangsu , Benefiting from the regional beta, the ability to handle various assets is strong. In addition, consumer finance is driven by the troika to make up the interest margin. Changshu Bank , Relying on the basic characteristics of small and micro businesses, we are small and scattered, little affected by chemical debt and stock housing loans, and maintain excellent asset quality. Concord Bank , Deeply cultivate inclusive microenterprises, make efforts in retail transformation, and take Shaoxing, a city with developed private economy, as its base, with strong regional economic certainty. Also recommended Chongqing Rural Commercial Bank 、 Shanghai Rural Commercial Bank 、 Bank of Nanjing and Qilu Bank 。 2. The weak economic recovery, the benefit of chemical bonds, high dividend yield varieties, and the choice of large banks: ABC, BOC, Postal Savings, ICBC, CCB, BOCOM, etc.). 3. The economic recovery is expected to be strong, so select the core assets in the bank: Bank of Ningbo 、 China Merchants Bank and Ping An Bank 。

Risk warning: The economic downturn exceeded expectations; Financial supervision exceeds expectations; The research report information was not updated in time.

Text analysis

event: On May 17, the People's Bank of China successively issued three housing loan policies, including the reduction of down payment ratio, the liberalization of the lower limit of mortgage loan interest rate at the national level, and the reduction of individual housing provident fund loan interest rate; On the same day, the national video conference on housing guarantee was held in Beijing. Vice Premier He Lifeng said that the government could purchase some commercial houses at reasonable prices as affordable housing at its discretion; At the same time, as a clarification and supplement of the video conference, on the afternoon of May 17, the Ministry of Housing and Urban Rural Development, the Ministry of Natural Resources, the People's Bank of China and the General Administration of Financial Supervision introduced the relevant information about the supporting policies for ensuring housing delivery at the regular policy briefing of the State Council, and the Central Bank announced the creation of 300 billion yuan of guaranteed housing refinancing.

Part 1

Sorting out the content of the new real estate policy: housing loan policy, storage, and refinancing

1.1 Adjustment of housing loan policy: the down payment ratio is reduced, the lower limit of interest rate is opened, and the interest rate of provident fund loan is reduced

Down payment ratio decreased: At the national level, the minimum down payment ratio of the first and second set of housing will be reduced by 5 percentage points to 15% and 25%, and local governments can also adjust it according to the actual situation in their jurisdictions.

The lower limit of mortgage interest rate is opened: At the national level, the lower limit of housing loan interest rate was cancelled (the first one was LPR-20BP, the second one was LPR+30BP), and local governments can decide whether to set the lower limit.

Decrease of interest rate of provident fund loan: The loan interest rate of individual housing provident fund was reduced by 0.25 percentage points. After the reduction, the loan interest rate of the first and second housing less than five years (inclusive) was 2.35% and 2.775% respectively, and the loan interest rate of the first and second housing more than five years was 2.85% and 3.325% respectively.

1.2 Do a good job in the video conference of housing guarantee and delivery: first mention "the people's and political nature of real estate work", and define the local government's land recovery and storage

General requirements: It is the first time to put forward "the public and political nature of real estate work". The strategic significance of solving the problems faced by the real estate market was further improved, and the responsibilities of local governments, real estate enterprises, financial institutions and other parties were further consolidated.

Compacting the responsibilities of financial institutions, local governments and regulatory authorities.

① Financial institution - Baojiao Building. Fully support the financing of projects to be continued.

② Local government - land recycling+storage. Reclaimed land: Properly dispose of the idle stock residential land that has been transferred by means of recovery, acquisition, etc., as appropriate, to help real estate enterprises with financial difficulties. Storage: In cities with a large inventory of commercial housing, the government can purchase some commercial housing at a reasonable price to be used as affordable housing.

③ Regulatory authorities - financing coordination mechanism+re lending. Give full play to the role of financing coordination mechanism and refinancing policy.

1.3 Regular briefing on the policies of the State Council: the four departments made clear and detailed the work of housing guarantee and delivery, and the Central Bank announced the establishment of 300 billion yuan of affordable housing refinancing

Ministry of Housing and Urban Rural Development: do a good job in ensuring the delivery of housing, and compact the responsibilities of local governments, real estate enterprises and financial institutions.

① Local governments should assume territorial responsibilities, and promote the coordination of housing construction, financial management, public security, natural resources, audit and other departments and courts to perform their respective duties and form a joint force.

② Real estate enterprises should bear the main responsibility, formulate a "one project, one policy" disposal plan, actively dispose of assets, and raise funds from multiple sources to ensure the timely and quality delivery of projects.

③ Financial institutions should implement the due diligence exemption provisions, make sure that the eligible projects are "fully loaned", accelerate the approval and issuance of loans, and support the delivery of project construction.

Ministry of Natural Resources: dispose of idle land strictly according to law; We will increase support for the revitalization and utilization of existing land.

① Support enterprises to optimize development. It is mainly to remove obstacles to development and construction, reasonably exempt the liability for breach of contract due to natural disasters and epidemics, and allow enterprises to reasonably adjust planning conditions and design requirements in accordance with procedures to better adapt to market demand.

② Promote market circulation and transfer. It is mainly to play the role of the secondary market of land, support advance notice registration transfer and "transfer with mortgage", and encourage transfer or cooperative development.

③ Support local governments to recover land at reasonable prices. It is mainly to support local governments to recover idle land at a reasonable price for affordable housing construction in accordance with the principle of "purchase on demand". Local governments are allowed to adopt the "recovery supply" parallel approach to simplify procedures, handle planning and land supply procedures, and better provide facilitation services.

People's Bank of China: set up low-income housing refinancing.

① The scale of affordable housing refinancing is 300 billion yuan, the interest rate is 1.75%, the term is one year, and it can be extended four times. The recipients include 21 national banks, including the National Development Bank, policy banks, state-owned commercial banks, postal savings banks, joint-stock commercial banks, etc. The bank shall grant loans according to the principle of independent decision-making and risk bearing. The People's Bank of China will issue re loans at 60% of the loan principal, which can drive bank loans of 500 billion yuan.

② The purchased commercial houses are strictly limited to the commercial houses that have been built but not sold by real estate enterprises, and real estate enterprises with different ownership are treated equally. According to the principle that indemnificatory housing is used to meet the rigid housing needs of wage earners, the house type and area standards of purchased commercial housing should be strictly grasped.

③ Selected by the city government Local state-owned enterprises are the acquisition subject. The state-owned enterprise and its affiliated group shall not be involved in the implicit debt of the local government, and shall not be the financing platform of the local government, At the same time, it should have bank credit requirements and credit space, and quickly allocate or lease after acquisition.

④ Voluntary participation. The city government decides whether to participate or not according to the local demand for affordable housing, the inventory level of commercial housing and other factors. The wage earners who meet the security conditions can independently choose whether to participate in the placement or leasing. The real estate enterprise and the acquisition subject negotiate on an equal basis and decide whether to sell or not independently. The 21 banks independently decided whether to grant loans to the acquisition subject in accordance with the principles of risk bearing and commercial sustainability.

General Administration of Financial Supervision: further play the role of urban real estate financing coordination mechanism to meet the reasonable financing needs of real estate projects.

① The financing coordination mechanism is headed by the main leader of the city government, the deputy mayor in charge of urban construction, housing and finance as the deputy leader, and the relevant departments and financial institutions as the member units, to set up a special team for centralized office work.

② The "white list" shall be voluntarily declared by the real estate project company, and the district/county of the city where it is located shall review and propose the list. The city coordination mechanism shall organize screening and review, and those that meet the conditions and standards shall be included in the "white list". Those that do not meet the conditions and standards shall be rectified to promote problem solving and form a closed-loop management mechanism.

Part 2

Adjustment of housing loan policy: limited impact on bank interest margin

2.1 Policy intention: starting from the demand side and the residential sector, improve the leveraged housing purchasing capacity of the residential sector

Give greater autonomy to local governments and financial institutions 。 In this round of housing loan policy adjustment, the national housing loan interest rate floor has been completely opened, marking that the housing loan interest rate floor for many years has become a history. The marketization degree of housing loan interest rate has improved, and the future will depend more on the game between the bank's own costs and residents' needs.

Reduce the pressure on residents to buy houses and slow down the downward slope of the real estate market. The reduction of down payment ratio, the opening of the lower limit of housing loan interest rate, and the reduction of provident fund loan interest rate jointly point to further reducing the pressure on the residential sector to purchase houses, which is the cooperation of the demand side and the residential sector to the real estate de transformation. However, the policy is essentially a further liberalization of restrictions, and does not provide incremental funds for residents to increase leverage as the "monetization of housing reform" policy does. Therefore, it has generally limited impact on residents' demand for housing. We believe that the policy is more targeted at slowing down the downward slope of the real estate market.

2.2 Policy impact: it is conducive to slowing down the downward slope of the real estate market, and its impact on bank interest margin is generally limited

Down payment ratio reduction: reduce the pressure of house purchase, but some cities are constrained by the consideration of bank credit line on income level, and some cities are constrained by the supply and demand relationship.

According to our grassroots research, most banks still require the monthly income to cover twice the monthly payment when determining the credit line of housing loans.

① For some cities with relatively high housing prices, For the house with a total price of 5 million yuan, the interest rate is based on the LPR level, and the down payment ratio is reduced from 20% to 15% when the repayment period is 25 years. The monthly supply will be increased by about 1300 yuan, and the corresponding monthly income level indicators need to be increased by about 2600 yuan. Therefore, the down payment pressure has decreased, but the monthly income pressure still brings some constraints on residents' ability to increase leverage.

② For areas with low housing prices, The decrease in the down payment ratio has brought about a relatively small increase in the monthly supply (for houses with a total price of 1 million yuan, the down payment ratio has dropped from 20% to 15%, and the corresponding indicators of monthly income level only need to be increased by about 500 yuan), and the effectiveness of this policy will be more obvious. But at the same time, the lower the housing price, the weaker the supply and demand relationship of local real estate, and the supply and demand relationship will become a greater constraint.

Interest rate reduction: it is conducive to the recovery of demand. The interest rate of commercial loans depends on the game between bank costs and residents' demand for housing, which has limited impact on the overall interest margin of banks.

① It is conducive to the recovery of demand that provident fund loans can cover the loan demand areas: The interest rate of provident fund loan has clearly defined the range of reduction, while the interest rate of commercial loan depends on the game between the cost of bank funds and the demand of residents for housing purchase. Therefore, the interest rate reduction this time is more conducive to the coverage of provident fund loan in the area of loan demand. However, similar to the above analysis on the down payment ratio reduction, the supply and demand relationship of real estate in some cities is relatively poor, and the loan demand in some cities is difficult to be fully covered by provident fund loans.

② The impact on bank interest margin is generally limited: As for the commercial loan interest rate, it depends on the game between the bank cost and the housing purchase demand of residents. According to the data of listed banks, the average interest bearing debt cost of listed banks in 2023 will be 2.26%, and the average credit cost in 2023 will be 0.75%. According to the comparison between the non-performing ratio of mortgage loans and the overall non-performing ratio of banks, assuming that the credit cost of mortgage loans is one third of the average credit cost, that is, 0.25%. In combination with the expenses of listed banks in 2023 The lower limit of mortgage loan interest rate pricing=debt cost+credit cost+expense cost=2.26%+0.25%+0.67%=3.2%. Assume that the amount of mortgage loan released after the addition of early repayment in 2024 is equivalent to that in 2023 (the amount of early repayment is estimated according to the early repayment index of RMB conditions, and the amount of loan released after the addition is negative is adjusted to 0), The impact of a 50BP cut in the interest rate of newly issued mortgage loans on the annual interest margin of listed banks was 0.7BP, and the impact on profits was about 1% (The actual impact will be smaller. For cities where the sales price of new commercial residential buildings has decreased for three consecutive months month on month and year on year, the lower limit of the loan interest rate for commercial individual housing of the first housing has been relaxed periodically, and many cities have adjusted due to the urban policy).

Part 3

Deposit collection: stabilize house prices, relieve liquidity pressure on real estate enterprises, and help stabilize the quality of bank assets

3.1 Policy intention: stabilize house prices and ease liquidity pressure of real estate enterprises

Stable housing prices. Local governments "purchase some commercial houses at reasonable prices as appropriate", which helps to stabilize the marginal value of housing prices in some cities where housing prices have declined more; At the same time, the improvement of the "wealth effect" brought by this will also help to stabilize the consumption willingness of the residential sector.

Relieve liquidity pressure of real estate enterprises, Promote guaranteed delivery of housing and prevent real estate market risks. The government's purchase and storage at a reasonable price will also ease the liquidity pressure of housing enterprises brought by high inventory. On the one hand, the injection of liquidity is conducive to the promotion of guaranteed delivery of housing, but also plays a role in preventing real estate market risks.

3.2 Policy impact: second tier cities may benefit more significantly, helping banks stabilize the quality of public real estate assets

Second tier cities may benefit more significantly. This round of local government collection and storage also faces some constraints, including "more inventory", "order according to demand", and "reasonable price", corresponding to cities with high inventory and more price decline, that is, second and third tier cities and below. However, the demand for affordable housing in third tier and lower tier cities is also relatively low. Therefore, second tier cities are more likely to benefit from the purchase and storage policy.

To help stabilize the quality of bank assets. The liquidity injection brought by the purchase and storage has played a positive role in mitigating the risk of the real estate market. At the same time, the marginal stabilization of house prices has also led to the improvement of residents' wealth effect, both of which are conducive to the stability and improvement of bank asset quality.

Part 4

Re lending: improve the liquidity of real estate enterprises, and the regions with high rental return rate will benefit more significantly

4.1 Policy intention: improve the liquidity of real estate enterprises and promote the financing coordination mechanism

The scale of affordable housing refinancing is 300 billion yuan, and the interest rate is 1.75%. The refinancing based on 60% of the loan principal can drive bank loans of 500 billion yuan. Local state-owned enterprises shall be the subject of acquisition, and they shall be quickly allocated or leased after acquisition. This policy helps local state-owned enterprises to acquire the completed but unsold commercial housing by means of liquidity investment, and promotes the digestion of the stock of commercial housing in combination with the financing coordination mechanism, which helps to improve the liquidity of real estate enterprises and promote the financing coordination mechanism.

4.2 Policy impact: cities with rental return rates above 1.95% have benefited significantly, helping to improve the quality of bank assets

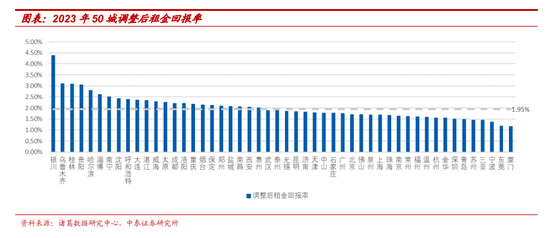

Cities with rental return rates above 1.95% have benefited significantly. This refinancing policy emphasizes that "local state-owned enterprises shall be the subject of acquisition. The state-owned enterprises and their affiliated groups shall not be involved in the implicit debt of local governments and shall not be the financing platform of local governments". Therefore Local state-owned enterprises will consider more in accordance with the principle of commercialization 。 The interest rate of the refinancing is 1.75%. The refinancing is granted at 60% of the loan principal. In combination with the bank's own debt cost (estimated at the level of 2.26% of the listed banks), the debt cost of such loans is 1.95% (1.75% * 60%+2.26% * 40%), while the corresponding credit cost of such local state-owned enterprises is relatively low, so it can be assumed that The pricing of such loans by banks shall not be lower than 1.95% 。 Therefore, from the perspective of profitability of local state-owned enterprises, a rent return rate higher than 2% in this area will bring positive benefits to them. Thus, Regions with rental return rate higher than 1.95% will benefit more obviously from this refinancing policy 。 According to the rent return rate of 50 cities in 2023 disclosed by "Zhuge Data Research Center", considering the time consumed in the rental process, we multiply the rent return rate by 11/12 to get the adjusted rent return rate. About half of the 50 cities have adjusted rental returns of over 1.95%.

Help improve the quality of bank assets. Consistent with the above analysis on deposit collection, the improvement of real estate enterprise liquidity is also conducive to the stabilization and improvement of banks' quality of public real estate loan assets.

Part 5

Investment suggestions and risk tips

Investment suggestions: The economy determines the logic of bank stock selection. The weak and strong recovery of the economy correspond to different target varieties. Bank stocks are robust and defensive. See our annual strategy for details Vitality in steadiness - from macro to customer group and from customer group to income 。 1. High quality urban rural commercial banks have great certainty in their fundamentals, so they choose urban rural commercial banks with low valuation. We Continue to recommend Bank of Jiangsu, Benefiting from the regional beta, the ability to handle various assets is strong. In addition, consumer finance is driven by the troika to make up the interest margin. Changshu Bank, Relying on the basic characteristics of small and micro businesses, we are small and scattered, little affected by chemical debt and stock housing loans, and maintain excellent asset quality. Ruifeng Bank, Deeply cultivate inclusive microenterprises, make efforts in retail transformation, and take Shaoxing, a city with developed private economy, as its base, with strong regional economic certainty. Meanwhile, Chongqing Rural Commercial Bank, Shanghai Rural Commercial Bank, Bank of Nanjing and Qilu Bank are recommended. 2. The weak economic recovery, the benefit of chemical bonds, high dividend yield varieties, and the choice of large banks: ABC, BOC, Postal Savings, ICBC, CCB, BOCOM, etc.). 3. The economic recovery is expected to be strong, so select the core assets in the bank: Bank of Ningbo, China Merchants Bank and Ping An Bank.

Risk warning: The economic downturn exceeded expectations; Financial supervision exceeds expectations; The research report information was not updated in time.

(The author of this article introduces: Chief of the banking industry of Zhongtai Securities, head of the financial team, and a special researcher of the National Finance and Development Laboratory.)