Opinion Leader | Wen Bin

On May 15, in order to maintain a reasonable and sufficient liquidity of the banking system, the Central Bank carried out a 7-day reverse repurchase of 2 billion yuan and a 1-year MLF of 125 billion yuan. The bid winning interest rate was the same as before, 1.8% and 2.5% respectively. Due to the maturity of RMB 2 billion reverse repurchase and RMB 125 billion MLF on that day, This month, MLF achieved the "equal parity" sequel, The window for reducing reserve ratio and interest rate still needs to be moved backward.

After two consecutive months of retrenchment and renewal of MLF, MLF ended the retrenchment and renewal in order to cooperate with the issuance of ultra long term special treasury bonds to be launched in the middle and late May, and to calm the fluctuation of tax period. However, considering the current overall stable and loose liquidity, the smooth issuance and lengthening pace of the special national debt also weakened the concentrated impact on liquidity, and under the background of preventing funds from settling and idling and the low demand of banks for MLF, MLF only maintained the same amount of continuation, and the need to reduce RRR in the short term is not high.

The domestic economy is stabilizing, the pressure of stabilizing the exchange rate is still on, the pressure of bank interest margin is further increasing, and the MLF interest rate also remains unchanged.

The central bank will pay close attention to the domestic economic trend and overseas policy changes, and flexibly and effectively carry out open market operations to maintain reasonable and sufficient liquidity. However, with the change of internal and external environment, based on the overall policy objectives, there may still be some room for the reduction of RRR and interest rate within the year.

1、 The disturbance factors on the capital side have weakened, MLF The same amount of continuous cropping should be supported by the financial department, and the market supply and demand should be stable

(1) The impact on liquidity of the decentralized issuance of ultra long term special treasury bonds weakened, and the expectation of reserve ratio reduction fell short in the short term, MLF Moderate operation can stabilize the fluctuation of capital

Since the beginning of the year, the monetary policy has been in advance. In order to strengthen coordination with fiscal policy and stabilize economic growth, the central bank cut the deposit reserve ratio by 0.5 percentage points in February, providing about 1 trillion yuan of long-term liquidity to the market. However, due to the slow pace of government bond issuance, the smooth pace of credit and other factors, the capital level remained stable and loose, and the central bank did not intend to invest too much money. The net return continued every month. Since March, the daily reverse repurchase has remained at the land level of 10 billion yuan or 2 billion yuan.

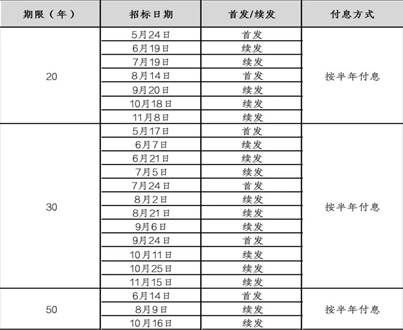

Since May, the biggest concern of the market for liquidity is the impact of the concentrated supply of 1 trillion yuan of ultra long term special treasury bonds, and it is believed that the central bank may hedge it by reducing the reserve ratio. However, according to the latest arrangement of the Ministry of Finance for the issuance of general treasury bonds and ultra long term special treasury bonds on May 13, this year the Ministry of Finance plans to issue three types of special treasury bonds of 20 years, 30 years and 50 years, 7 times, 12 times and 3 times respectively, scattered in May November. The smooth issuance and lengthening rhythm of the special treasury bonds weakened the concentrated impact on liquidity, and accordingly, the need for the central bank to cooperate through the RRR reduction has also declined.

However, considering that the issuance of 30-year and 20-year super long term special treasury bonds will be launched on May 17 and 24 respectively, MLF will end shrinking this month, and will stabilize the capital surface and strengthen policy coordination through equal amount of renewal.

Table 1: Issuance Plan of Extra Long term Special National Debt in 2024

Source: Ministry of Finance

(II) five Month is the tax payment month, MLF The end of the contraction also helps to stabilize the capital disturbance in the tax period

Generally speaking, tax payment will have a certain impact on liquidity, thus affecting the trend of capital. May is the traditional tax month. In addition to the normal monthly payment of VAT, income tax, consumption tax, resource tax and other taxes, the annual income tax payment of the previous year will also be carried out, and the income tax of the previous year will be refunded for the excess and supplemented for the deficiency. Therefore, the impact of tax payment in May on capital will be more significant.

Affected by the May Day holiday, the tax declaration period of this month was postponed to May 22. The days before and after tax payment had a great disturbance on the capital. Therefore, the MLF ended its contraction in May, stabilizing the capital surface and smoothing the fluctuation of interest rate through the continuation of the same amount.

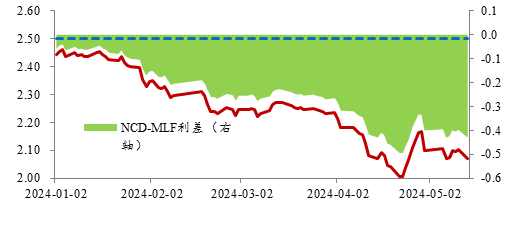

(III) MLF The interest margin with interbank deposit receipts is still high MLF The demand for, MLF Maintain the balance between supply and demand in the market by continuing to grow in equal quantities

Recently, the call to stop "manual interest compensation" has accelerated the flow of funds from the banking system to non bank institutions such as wealth management and funds, and the pressure on the bank's liability side has increased. However, from the perspective of the interest rate on the issuance of certificates of deposit since May, big banks have not continued to raise the price of issuance, and the debt pressure should be controllable under the condition that the capital surface is stable and loose and the current trend of not blindly rushing against the scale.

At the same time, the central bank's recent continuous attention and voice on ultra long bonds triggered the market to adjust its operating strategy. Many institutions "avoid long bonds and take short ones", which led to a rapid decline in the interest rate of deposit receipts. On May 14, the yield to maturity of 1-year AAA interbank deposit receipt was 2.07%, and the interest margin with MLF of the same period was inversely expanded to 43 basis points. The interbank deposit certificate interest rate is still low, MLF and its interest margin are widening, and financial institutions do not have strong demand for MLF. The continuation of MLF in equal volume helps to maintain the balance between supply and demand in the market.

Figure 1: Interbank deposit receipt interest rate is still low, and the interest margin with MLF is widening (%)

Source: Wind

(4) The central bank has raised its demand for preventing capital from settling and idling, MLF The same amount of continuation is also intended to reduce leverage and prevent idling

At present, under the environment of stable and loose funds and downward market returns, some institutions still have obvious asset allocation pro cyclical, prolonged and leveraged behaviors, and the average daily turnover of inter-bank pledge repo remains relatively high.

At the same time, in the context of economic transformation and upgrading, residents' consumption needs to be restored, and total demand is insufficient, money supply exceeds demand, which also causes some capital precipitation and idle arbitrage, reduces the efficiency of capital use, disturbs the market order, and is not conducive to the virtuous circle of economy and finance. Therefore, MLF only continues to produce in equal quantity, which is also intended to reduce leverage and prevent idling.

2、 Considering internal and external factors, five month MLF Interest rates remain unchanged

(1) From the domestic situation, many economic indicators have stabilized and improved, and the urgency of interest rate reduction in the short term is not high

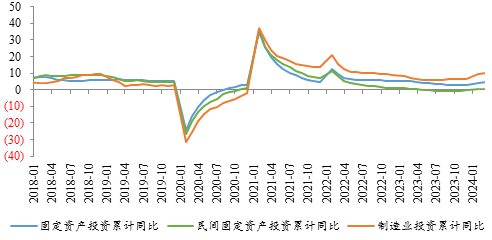

In the first quarter of 2024, the domestic economic growth rate rose to 5.3%, higher than the market expectation. In the "troika", investment and export or economic recovery have been driven, CPI and private investment have turned from negative to positive year on year, and travel consumption continues to be strong. Since April, high-frequency data has not weakened significantly, PMI continues to maintain an expansion range of more than 50, import and export data rebounded more than expected, and inflation data rebounded slightly.

Figure 2: The cumulative investment in private fixed assets turned from negative to positive year on year (%)

Source: Wind

Although the social financing increment in April was negative, the growth of money supply slowed down significantly, and the financial data performance was lower than expected, indicating that the effect of the demand side policy still needs to be shown, but this situation is mainly affected by the factors of the current regulatory initiative.

For example, since this year, the government bond issuance has lagged significantly, the "seesaw" effect of debt and loan under the low interest rate environment, the gradual slowdown of the growth rate of balanced investment and loan, and the decline of stock notes have all caused disturbances to social finance. However, the recent increase in the regulation of capital idling and manual interest compensation, the increased diversion of bank deposits to wealth management under the price comparison effect, and the weakening of the motivation of individual local governments to increase financial added value through deposits and loans, have pushed M2 growth downward. However, considering that the current M2 balance has exceeded 300 trillion yuan, the decline in growth does not mean that the financial support for entities has weakened, but that the quality and efficiency of the financial system in serving the real economy has further improved.

In the future, the greater pressure on enterprise operation and the more risks and hidden dangers in key areas will still restrict economic growth, but the favorable conditions to support the economic recovery are also increasing compared with the previous period, such as the government's efforts to stabilize growth continue to increase, residents' willingness to consume is accelerating to recover, and the activity of the private economy continues to increase. For this reason, the urgency of cutting interest rates in the short term is not high. Whether to cut interest rates still needs to continue to observe the economic trend.

(2) From the perspective of foreign situation, the dollar index continues to operate at a high level, and the RMB still has some depreciation pressure

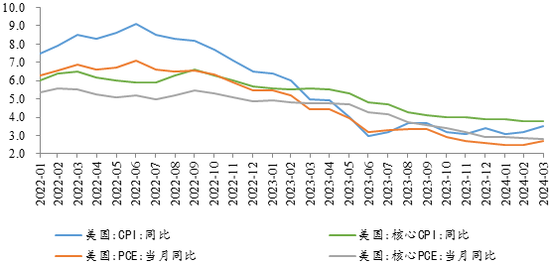

Since this year, the US economy has been generally stable, inflation still remains sticky, and the prospect of interest rate cuts has become more uncertain. Although with the recent decline of US employment data, the expectation of interest rate cut has increased. At present, the market expects that the Federal Reserve will cut interest rates in September with a high probability, and there is a possibility of 1-2 interest rate cuts in a year. However, considering that the European and British central banks may cut interest rates faster than the Federal Reserve, or they will start to implement in June and August respectively. Affected by this, the US dollar index is highly likely to continue to operate at a high level, and the RMB still has some depreciation pressure.

Late at night on May 14, Federal Reserve Chairman Powell said in a speech at an event that the Federal Reserve needs to be patient and wait for more evidence to show that high interest rates are curbing inflation and inflation continues to cool, so it is necessary to keep interest rates high for a longer time.

Therefore, even if the Federal Reserve starts to cut interest rates later, the policy interest rate will remain high for a long time. Global liquidity still faces some tightening pressure. It is still necessary to pay close attention to overseas economic and policy trends, and launch timely adjustment of domestic monetary policy. Under the consideration of "internal focus, internal and external balance", it is the best choice to maintain the stable level of policy interest rate in the short term.

Figure 3: US inflation fell less than expected (%)

Source: Wind

(3) From the perspective of policy orientation, it is necessary to maintain a reasonable interest margin, improve capital efficiency and keep interest rates at an acceptable level

Since this year, the central interest rate of loans and long-term bonds has obviously declined. The "manual interest compensation" behavior of collecting deposits at high interest rates has disrupted the market order. The competition for deposits has intensified. The net interest margin of banks continues to be under pressure. The irrational market performance has also attracted great attention from regulators.

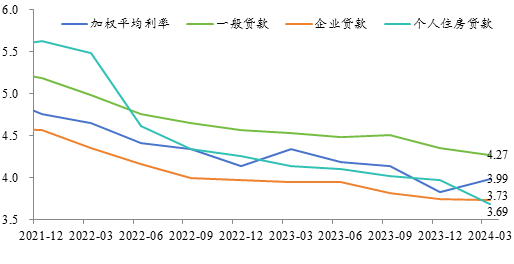

In March, the weighted average interest rate of newly issued loans was 3.99%, down 35bp year on year. Among them, the weighted average interest rate of corporate loans was 3.73%, down 22bp year on year and 2bp year on year; The weighted average interest rate of individual housing loans was 3.69%, a significant decrease of 45bp year on year and 28bp year on year.

Figure 4: The loan interest rate continues to decline, and the decline of individual housing loans is more obvious (%)

Source: Wind

The return on bank assets continued to be under pressure, while the cost control of liabilities was still not ideal on the whole, which made the bank interest margin continue to be under pressure in the first quarter. In the first quarter of 2024, the weighted average net interest margin of major listed banks [1] will be 1.57%, narrowing by 13bp year-on-year. Among them, the net interest margin of state-owned banks, joint-stock banks and urban rural commercial banks was 1.51%, 1.79% and 1.8%, respectively, narrowing by 13bp, 13bp and 8bp year on year.

In this context, if the MLF interest rate is lowered, it will lead to the continued decline of the loan interest rate, and squeeze the interest margin when the effect of self-discipline constraints on deposits is not fully manifested; At the same time, considering that the confidence of market participants still needs to be boosted, it may aggravate the capital idling and arbitrage behavior; It will also lead the bond market interest rate to continue to decline, deviating from the current desirable level of the central bank, further separating the long-term bond interest rate from the economic fundamentals.

3、 Short term RRR and interest rate cuts are difficult to be realized, but there may still be room for implementation within the year

On the whole, in order to promote the moderate recovery of prices and increase support for the real economy, the importance of aggregate instruments remains, and monetary policy will adhere to the general tone of steady and loose; However, in order to stabilize the exchange rate and prevent the idle arbitrage of funds, it is hard to realize the reduction of reserve ratio and interest rate in the short term. However, with the change of condition accumulation, it may still be possible to implement it within the year.

First, the time point of RRR reduction may move back significantly, and it is possible to land in the fourth quarter.

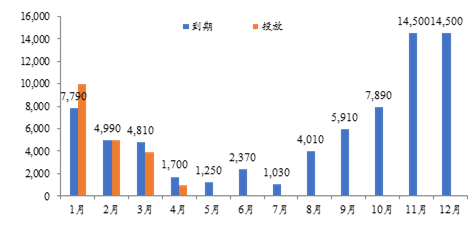

At present, according to the decentralized issuance plan of ultra long term special treasury bonds, the probability of the central bank to implement the cooperation of reducing reserve ratio has been greatly reduced; At the same time, in combination with the statement in the first quarter's monetary policy report, the central bank has paid great attention to the fund idling and long-term treasury bond interest rates. It is unlikely that the RRR reduction will be implemented in the near future. It is expected that more MLF volume increase and continuation and OMO net investment will be used to stabilize the volatility of capital.

However, judging from the estimated net financing amount of government bonds, the liquidity pressure from May to October was fair. From November to December, the liquidity pressure was relatively large due to the low maturity of government bonds. At the same time, considering that the MLF maturity in the next two months is also the highest, the central bank may implement a RRR reduction at that time to protect liquidity and ease the pressure on the central bank to continue MLF.

Figure 5: Monthly MLF launches and maturities in 2024 (100 million yuan)

Source: Wind

Second, combining internal and external factors, the implementation conditions of interest rate reduction are gradually accumulating.

3.21 At the press conference of the National New Office of the People's Republic of China, the Central Bank said that "the downward trend in deposit costs and the shift in monetary policies of major economies are conducive to broadening the autonomy of interest rate policy operations".

In the follow-up, the expectation of the Federal Reserve to cut interest rates has increased, and the pressure to stabilize the exchange rate has relatively eased compared with the previous period; Under the constraint of super self-discipline deposits (call a halt to manual interest compensation), there is a strong certainty that deposit costs will fall within the year. In this context, if prices rise and endogenous financing demand is still not repaired, the actual financing cost needs to be further reduced, thus increasing the probability of reducing the policy interest rate.

five month MLF With the interest rate unchanged, this month LPR Probably keep "hold your ground".

[1] Note: The main listed banks here include: six A-share listed large banks, CMB, Industrial, CITIC, SPD, Minsheng, Everbright, Ping An, Huaxia, Zhejiang, Beijing, Jiangsu, Shanghai, Ningbo, Nanjing, Hangzhou, Chengdu, Changsha, Guiyang, Zhengzhou, Suzhou, Qingdao, Qilu, Xi'an, Chongqing Rural Merchants, Qingdao Rural Merchants, Changshu, Zijin, Wuxi Zhangjiagang, Sunong Jiangyin Bank 。

(About the author: Chief Economist of Minsheng Bank)