Opinion leaders | Cheng Shi, Zhang Hongxu, Zhou Ye

As a traditional safe haven asset, the yen has continued to depreciate since the Federal Reserve tightened its monetary policy in 2022. Compared with gold, which is also a safe haven asset, the trend is significantly different. In the past two months, it has broken through a new low against the dollar since 1990. The accelerated depreciation of the yen in this round was mainly driven by the adjustment of the policy stance of the Federal Reserve and the Bank of Japan and the change of the expectation of the US Japan interest rate gap. Although the long-term hedging attribute of the yen still exists, in the turbulent pattern of frequent geopolitical conflicts in Eurasia, the improvement of the hedging attribute of the dollar has substantially weakened the hedging value of the yen.

As far as Japan is concerned, the high government debt pressure and the uncertainty of inflation make the Bank of Japan's monetary policy regulation space limited. The Bank of Japan's intervention in the yen is more likely to be through foreign exchange market operations rather than tightening monetary policy. Judging from the recent wave of devaluation of other Asian currencies in the yen, the exchange rate of major Asian economies may face pressure in the short term, but with steady economic growth, a sound exchange rate control mechanism and sufficient foreign exchange reserves, it is expected that major Asian economies will still have room to stabilize their exchange rates.

The change of interest rate spread expectation accelerated the depreciation of the yen and weakened the hedging nature of the yen. As a traditional safe haven asset, the yen has continued to depreciate since the Federal Reserve tightened its monetary policy in 2022, diverging from the trend of gold and the Swiss franc, which are also safe haven assets. It also fell for four consecutive days after the Bank of Japan's monetary policy meeting in April this year, breaking 160 yen, a new 34 year high since June 1990. The accelerated depreciation of the yen in this round is mainly due to the change in the expectation of the US Japan interest rate gap caused by the policy adjustment of the US Japan Central Bank in the past two months (Figure 1).

one side, The expectation of the Federal Reserve to cut interest rates is receding. As we mentioned in the report "It is difficult to cut interest rates, it is also difficult to raise interest rates", the inflation level in the United States has dropped from the steep range on the left side of the Phillips curve to the depression curve, and the pressure of the periodic rebound of inflation in this range is increasing, which makes the market constantly reassess the time of the Federal Reserve's interest rate cut, The Federal Reserve maintained a higher interest rate for a longer time, which further kept the nominal yield of US bonds at a high level.

on the other hand, The monetary policy tone of the Bank of Japan is still loose. At the monetary policy meeting in March, although the Bank of Japan announced its withdrawal from the ultra loose monetary policy framework, it still took a cautious attitude overall, weakening the market's expectation of further tightening monetary policy in the second and third quarters of this year. In the long run, the pressure on Japanese government debt has further intensified since 2020, with the ratio of public debt to GDP exceeding 260%. The Bank of Japan still needs to maintain a low interest rate to maintain debt sustainability. In addition, in the face of high global inflation, especially the soaring global raw material prices after the Russia Ukraine war, Japan, as a raw material import dependent country, is difficult to maintain the past long-term trade surplus under a significant negative impact, which also further puts pressure on the yen exchange rate.

From the perspective of the hedging nature of currency, Our research finds that in the past four years, the traditional hedging attribute of the yen has weakened: Japan's long-term loose monetary policy and low inflation rate have made the market form long-term stable expectations for the Bank of Japan's monetary policy. Investors' risk appetite for yen is relatively stable, which enables investors to borrow low interest currencies for a long time and invest in overseas high interest markets. As a low interest currency, yen not only has good capital liquidity and foreign exchange reserve support, but also is the best choice for borrowing funds in arbitrage transactions. When the global risk appetite is further reduced, Japan's relatively moderate economy and stable policy expectations also make global investors tend to transfer more funds to Japan's domestic market, which highlights the value of the yen as a hedge. However, in recent years, the frequent occurrence of global geopolitical conflicts and the acceleration of the pace of globalization of the world economy have led to changes in the risk aversion behavior of global investors.

Figure 1: Japanese Yen/US Dollar Exchange Rate and Japan US Interest Margin

Source: iFinD and ICBC International

In the long run, it is difficult for the yen to strengthen. The weak yen has more advantages than disadvantages for the export-oriented Japanese economy.

For the corporate sector, The relative depreciation of the yen can boost the competitiveness of export-oriented enterprises. From 2021 to 2023, the growth rate of Japan's export amount will be 21.5%, 18.2% and 2.8% respectively, which has maintained the growth momentum for three consecutive years. In 2023, it will reach a record high of about 100 trillion yen. Although the depreciation of the yen will increase the costs of importers, the uncontrollable raw material prices and transportation costs have the most significant impact on the profits of Japanese importers.

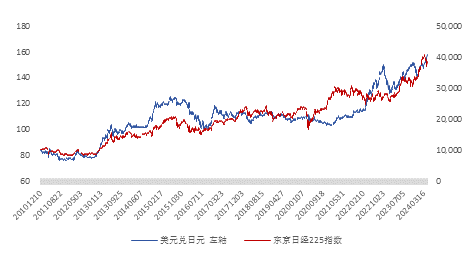

For the economic sector, The devaluation of the yen often helps to stimulate the Japanese stock market, thus enhancing the wealth effect of the Japanese residential sector (Figure 2). Due to the large export proportion of Japanese high-tech electronic manufacturing such as automobiles and semiconductors. The depreciation of the yen will help improve the profit margin of enterprises and stimulate the rise of stock prices. For Japanese multinational companies, the depreciation of the yen means that the same foreign currency will exchange for more yen during the settlement of foreign exchange. Even if the overseas currency income remains stable, the change of exchange rate will also improve their performance in financial reports, thus improving the stock price.

For the Bank of Japan, For many years, the Japanese economy has been in a state of slow growth or stagnation, and it is difficult to raise the inflation level. Japanese politicians and the central bank generally have a high tolerance for inflation.

From the perspective of economic structure The aging trend of Japan's population is obvious, and the potential economic growth rate continues to decline. Higher inflation will help reduce the real interest rate and stimulate the consumption level, thus easing the economic pressure caused by the aging population. Secondly, Japan's government debt level remains high, and higher inflation is conducive to gradually "diluting" these debt burdens. In addition, tolerating higher inflation will help provide the Bank of Japan with more room for policy adjustment, especially after experiencing long-term deflation and low inflation, the Bank of Japan may be more cautious about raising interest rates.

Figure 2: Yen vs USD and Nikkei 225

Source: iFinD and ICBC International

It is too early to talk about the crisis when looking at the depreciation pressure of Asian currency market from the perspective of yen.

After the recent market revaluation of the Federal Reserve's interest rate cut expectations, Asian money markets are generally facing depreciation pressure (Figure 3), of which the yen depreciated the most. In the future, whether there is further devaluation risk in the Japanese and Asian money markets still depends on the expected trend of the Japan US interest rate gap. In view of the limitations of Japan's monetary policy regulation space, the Bank of Japan's intervention in the yen may be more likely to be through foreign exchange market operations rather than tightening monetary policy.

At present, The fluctuation of the dollar against the yen at about 160 is the level that has been included in the current monetary policy expectations of Japan and the United States. Unless the market has further revised the expectations of the monetary policies of Japan and the United States, the dollar against the yen will still fluctuate at about 150-160 in the short term. As a typical export-oriented economy in the Asian market, the trend of Japan's yen is closely related to the underlying logic of the trend of other Asian currencies. Although in the short term, the exchange rates of Asian economies may be under pressure, similarly, the further devaluation of the currencies of the economies depends on the further revision of the market's expectations of the monetary policies of all parties. On the one hand, the economic growth of developing economies in Southeast Asia is still stable. In 2023, the GDP growth of India, Indonesia and Vietnam will maintain more than 5%, while the economic growth of developed economies such as Japan, South Korea and Singapore is relatively slow. The choice of economic fundamentals and monetary policies has put some pressure on their exchange rates. On the other hand, since the Asian financial crisis in 1997, Major Asian economies have generally improved their exchange rate control mechanisms, reduced their dependence on international capital, and retained sufficient foreign exchange reserves. It is expected that major Asian economies will be able to stabilize their exchange rates sufficiently to withstand the impact of external factors.

Figure 3: Changes of Asian currencies against the US dollar since 2024 (based on January 2, 2024)

Source: iFinD and ICBC International

(The author of this article introduces: Head of ICBC International Research Department, Chief Economist. His research fields include global macro, Chinese macro and financial markets.)