Article/Huang Zhilong, columnist of Sina Financial Opinion Leader (WeChat official account kopleader)

Supporting the development of private enterprises is the focus of attention from all walks of life. In order to solve the financing problems of private enterprises, the Central Bank, the Banking and Insurance Regulatory Commission and other departments have introduced a series of preferential policies. There is also a voice in the industry that cutting interest rates may be a current policy option. Now the question comes, can interest rate reduction solve the financing problem of private enterprises? See the analysis below.

The "benchmark" effect of benchmark deposit and loan interest rates is weakening

The trend of weakening the "benchmark" effect of deposit and loan interest rates on the financial market is mainly reflected in the following two aspects:

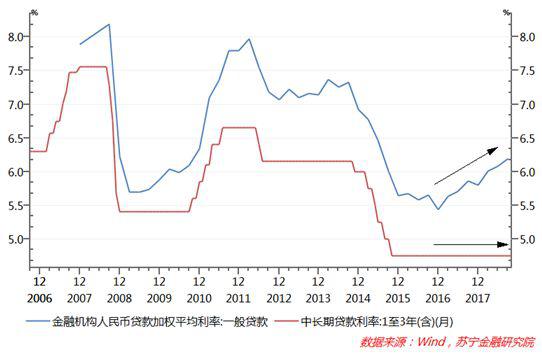

First, the benchmark interest rate remains unchanged for a long time, and the financing cost of the real economy continues to rise. In the past decade, the financing cost of the real economy (the weighted average interest rate of general loans of financial institutions) has experienced two complete cycles of decline and rise. From 2008 to 2016, the weighted average interest rate of financial institutions' loans was basically in sync with the trend of the benchmark interest rate of loans, and the "benchmark" effect of the benchmark interest rate was significant. After 2017, the benchmark interest rate of loans remained unchanged for a long time, while the weighted average interest rate of loans experienced a sustained recovery of nearly two years, and the trend of the two trends was significantly differentiated (see the figure below).

The reason for this phenomenon needs to start from the results of interest rate marketization. In the interest rate marketization environment, commercial banks enjoy greater autonomy in the policy of interest rate floating up or down. For example, in the last two years' rising cycle of real interest rate of loans, the main driving factor is that the loan interest rate of commercial banks has risen more and more in the interest rate marketization environment (see the figure below).

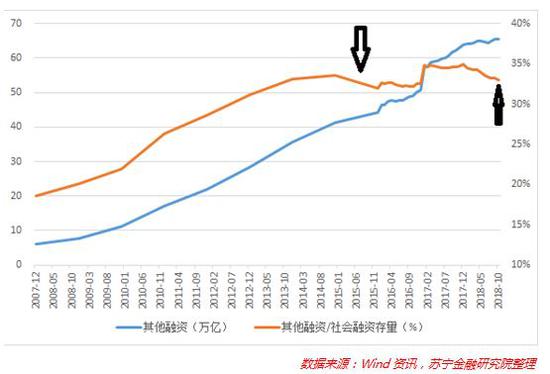

Secondly, the benchmark loan interest rate cannot guide the capital cost of shadow banks and off balance sheet financing. Since 2008, the biggest change in the social financing structure is: before that, commercial banks had the largest number of on balance sheet loans, and shadow banks and off balance sheet financing methods had flourished. The balance of other financing deducted from loans in the social financing stock rapidly expanded from 5.96 trillion yuan at the end of 2007 to 65.36 trillion yuan at the end of October 2018, and the proportion of social financing balance also rose from 18.5% to 33%. Although the expansion of non loan financing experienced a temporary slowdown in the process of cleaning up shadow banks from 2014 to 2015, its long-term growth trend is still significant (see the figure below).

The basic reason why the current private enterprises' problems become more and more serious is that private enterprises have a high degree of dependence on shadow banks and off balance sheet financing. According to the data recently disclosed by Guo Shuqing, Chairman of the Banking and Insurance Regulatory Commission, commercial banks' loans to private enterprises account for less than 40% of corporate loans, and the incremental part is less than 20%. In other words, the huge financing needs of private enterprises are mainly met by shadow banks, off balance sheet financing, private lending and other financing methods.

Compared with on balance sheet loan growth of banks, the impact of strong financial supervision on non bank financing channels is more prominent, and the financing costs of off balance sheet and non bank financing channels rise more significantly.

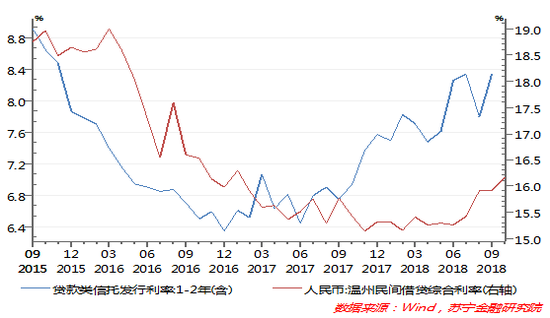

For example, in the past two years, the issuance rate of trust products jumped 200 basis points, reaching 8.34% at the end of September; Since the beginning of the year, the borrowing cost of SMEs represented by Wenzhou private loan interest rate has also increased by 100 basis points, reaching 16.17% by the end of October (see the figure below). The interest rate changes of these non bank financing are limited by the benchmark interest rate of loans, and more affected by the financial supervision cycle.

It is worth mentioning that the financing of stock market and bond market is mainly affected by the market sentiment of short-term capital at home and abroad, the risk preference of financial institutions, and is not affected by the adjustment of benchmark loan interest rate.

The central bank's interest rate cut will be constrained by three factors

In addition to the gradual weakening of the "benchmark" role of the benchmark loan interest rate, the current interest rate cut faces other constraints, including the following three aspects:

First, the depreciation pressure of the RMB exchange rate. The central bank's interest rate cut action must be concerned about the pressure on the RMB exchange rate caused by the differentiation of monetary policies between China and the United States. Both the theoretical mechanism of "interest rate parity" and the practice of European and American countries show that interest rates are the key factor affecting short-term exchange rate fluctuations, and this correlation (narrowing of interest margin and falling of RMB exchange rate) has been particularly prominent in December 2015, December 2016 and the second half of this year (see the figure below). At present, the market expects that the Federal Reserve will raise interest rates 3-4 times in 2019. At this time, if China lowers the benchmark interest rate, it will intensify the differentiation of monetary policies between China and the United States, resulting in further narrowing of the interest rate gap between long-term treasury bond yields between China and the United States, and increasing the pressure on maintaining the stability of the RMB exchange rate in the later period.

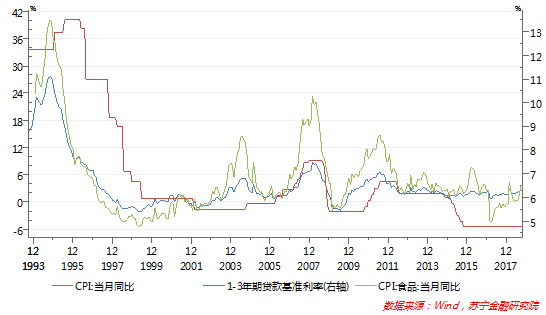

Second, the rise of inflation pressure will become an important constraint for interest rate reduction. In October, the year-on-year growth rate of national CPI was 2.5% for two consecutive months, maintaining a moderate inflation trend. What is more noteworthy is that the year-on-year growth of food prices, the weather vane of China's inflation situation, has remained high, rising 3.6% and 3.3% respectively in September and October, and has become the main factor driving CPI recovery. From a long-term historical perspective, in the CPI recovery cycle, the benchmark interest rate of loans has never been lowered (see the figure below). In the fourth quarter of this year and 2019, with the rising inflation pressure in the United States, the domestic inflation situation may deteriorate. Under this background and trend, lowering the benchmark interest rate will not be conducive to stabilizing inflation expectations.

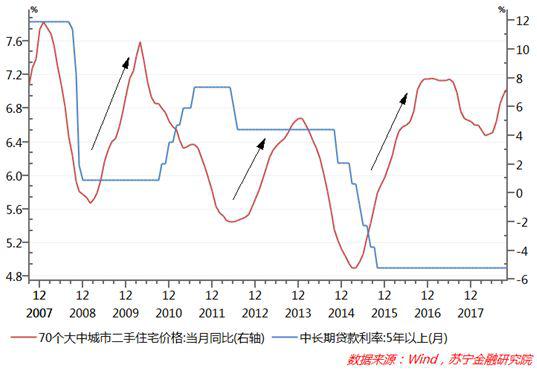

Third, interest rate cut will hedge the policy effect of real estate regulation. At present, the real estate regulation is in a critical period. The data of the past decade shows that every time the benchmark loan interest rate is lowered, it is the starting point of every round of house price rise cycle (see the figure below). In recent months, there is still upward pressure on the overall increase of the national housing price. If the benchmark lending rate is lowered at this time, it may once again stimulate the bubble rise of housing prices and hedge the policy effect of early real estate regulation.

Difficulty in financing will solve the problem that financing is more expensive than financing

From the perspective of the central bank's policy orientation, let's take a look at the latest statement of the central bank governor Yi Gang:

We should give priority to solving the problem of difficult financing, because without financing, we can't talk about expensive financing. We should first solve the problem of difficult financing, and then focus on solving the problem of expensive financing. If we pay too much attention to the financing cost and ignore the financing availability, it will undermine the risk pricing autonomy of financial institutions, form a reverse incentive, lead to financial institutions dare not to lend, unwilling to lend, but increase the difficulty of financing, and even threaten the survival of enterprises. Only on the premise of ensuring the availability of financing, giving financial institutions appropriate risk compensation and strengthening the internal incentives of financial institutions can form a long-term mechanism to serve private enterprises, especially small and medium-sized micro enterprises. The key is how to unblock the transmission mechanism of monetary policy. Especially, as the core channel from monetary policy to credit policy, the incentive compatible assessment mechanism and risk preference improvement of commercial banks are still key elements.

The full text of the just released Third Quarter Monetary Policy Implementation Report of the Central Bank did not mention the policy orientation of reducing financing costs, but emphasized "Maintain reasonable and sufficient liquidity and maintain reasonable growth of monetary credit and social financing scale" At the same time, the macro prudential assessment (MPA) mechanism is used to increase financial institutions' support for weak links such as small and micro enterprises and private enterprises. As for the interest rate policy, the report emphasizes that "Strengthen the ability of interest rate regulation, further dredge the transmission of the central bank's policy interest rate to the financial market and the real economy, and promote the gradual" integration of the two tracks "of the interest rate system.". in short, The central bank's policy focus will be on targeted easing policy and accelerating the dredging of the monetary policy transmission mechanism, rather than adopting a comprehensive easing and flood flooding policy of interest rate reduction.

(The author of this article introduces: Director and Senior Researcher of the Macroeconomic Research Center of Suning Institute of Finance.)