Article/Xue Hongyan, columnist of Sina Financial Opinion Leader (WeChat public account kopleader)

This article will start with the business data of the head platform, and analyze the current dilemma of the P2P industry from the point to the surface, as well as how to survive in the dilemma? How to break the game?

According to the data of the online loan home, the transaction volume of the online loan industry in the third quarter of 2018 was 374.8 billion yuan, down 29.48% month on month and 49.24% year on year. Since October, the trading volume has continued to shrink, with a turnover of 102.3 billion yuan in that month, down 7.65% month on month.

It is said that there is no end under the nest, and behind the downturn of industry data, there are difficulties in the operation of single platforms. This article will start with the business data of the head platform, and analyze the current dilemma of the P2P industry from the point to the surface, as well as how to survive in the dilemma? How to break the game?

Looking at the Development Dilemma of P2P Industry from the Head Platform

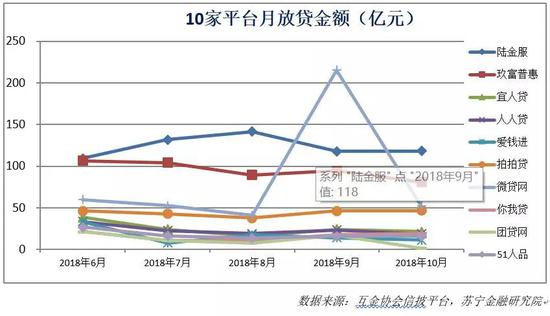

Based on the ranking of the outstanding balance by the end of October 2018, this paper selects 10 platforms (hereinafter referred to as "the top 10 platforms") as the head platform representatives, including Lujinfu, Jiufu Puhui, Yirendai, Renrendai, Aiqianjin, Paipaidai, WeChat, Youwodai, Tuandai and 51 Renpin.

First, under the current industry environment, the market position of the head platform is improving. From June to October 2018, the outstanding balance of the industry dropped from 1029.2 billion yuan to 832.3 billion yuan, a decrease of 19.14%; The top 10 platforms achieved the basic stability of the outstanding balance, a slight increase of 2.2 billion yuan, and the market concentration increased from 34.33% to 42.72%, an increase of 8.39 percentage points in four months.

However, although the head platform was able to maintain the weak growth of the outstanding balance, affected by the pressure of potential capital outflow, all companies slowed down the pace of issuing new loans.

From the data point of view, in addition to Lujinfu, the monthly lending amount of several leading platforms has declined since June, with the exception of September. The lending data showed signs of recovery, in which the lending amount of WeChat loan network in the current month increased sharply from 4.1 billion yuan to 21.5 billion yuan, but in October, the lending amount of the platform returned to the downward trend. In October 2018, the loans issued by the top 10 platforms totaled 38.6 billion yuan, a month on month decrease of 20 billion yuan, 11.2 billion yuan less than that in June.

This is true for the head platform, not to mention the industry data. From June to October 2018, the monthly decline of borrowers and lenders in the P2P industry was 39.57% and 44.32% respectively. In the context of the rapid growth of the entire consumer finance industry, the rapid decline in the number of borrowers is not due to external factors, but the result of the active flow restriction of the P2P platform, that is, it is difficult for a clever woman to make bricks without straw.

As an information matchmaking intermediary, the scale of lenders determines the scale of lending funds on the P2P platform. The continued decline in the number of lenders is tantamount to taking drastic measures to continuously weaken the development foundation of the platform.

First, the ability to lend declined and core businesses shrank. The decline in the number of lenders has directly brought about a net outflow of funds. At this time, limited funds are often used preferentially for debt to debt projects to ensure the smooth withdrawal of lenders and ease their panic. The priority of borrowers' new demands is postponed, and they cannot be satisfied, so they will inevitably flow to consumer finance companies, small loan companies and other institutions. The participation and influence of P2P in the consumer finance industry will continue to decline between entry and exit.

Second, the foundation of development has been weakened and the vitality of the platform has been seriously damaged. The foundation is not solid, and the earth shakes. The borrower is the bread and butter of the P2P platform, and the decline in lending ability directly brings about the decline in revenue. In order to survive, the platform tends to reduce costs, pay cuts, layoffs and other issues have also followed, and with the loss of core talents, the foundation of development has been shaken. Even if the platform can recover and finally get the record, it has been greatly damaged.

Third, the decline of the platform's revenue capacity will further weaken the confidence of lenders, As a result, lenders accelerated their flight, forming a vicious circle.

All kinds of signs show that many P2P platforms in the market have fallen into the above vicious circle, with business decline, brain drain, lenders fleeing

Exchange space for time: output assets and self rescue with arms broken

What should we do?

The first thing is to actively cooperate with the record inspection and obtain the record, which can effectively restore the confidence of lenders and break the chain of the whole vicious circle.

The problem is, I'm afraid there is not enough time. According to the relevant requirements of the Notice on Conducting Compliance Inspection of P2P Network Lending Institutions issued by the National P2P Network Lending Rectification Office in August 2018, the filing work can be roughly divided into three steps:

First, after three rounds of self inspection, self-discipline inspection and administrative inspection, the deadline is the end of December 2018;

Second, the qualified platform is allowed to access the information disclosure and product registration system, and the specific duration of trial operation is unknown;

Third, institutions with mature conditions apply for filing as required.

The most optimistic estimate is that it will take at least half a year to complete the above steps. As far as the platform is concerned, it needs to race against time. Before getting the record, it needs to find ways to maintain the basic aspects of the platform's sustainable operation, namely, the user base of borrowers, lenders and other users and a relatively stable staff team.

The loss of lenders is an objective trend that must be accepted, which can be delayed but difficult to reverse. In the current industry environment, the cost of attracting new users has increased significantly, and it is relatively easy to retain old users. Constantly improving the re investment rate of old users has become the key work. According to the disclosure of WeChat loan website in the prospectus, in the first half of 2018, the reinvestment lenders contributed 95% of the loan funds, which to some extent indicates the difficulty of obtaining new users. In the second half of 2018, the difficulty of acquiring new users has further increased, and the contribution rate of old users is expected to further increase.

The stability of the staff team depends on the stability of the revenue, and the source of the revenue is the borrower. Since there is not enough funds to meet the needs of borrowers, the platform can also follow the example of Fintech Open Platform to match borrowers to various licensed institutions with sufficient funds, that is, to explore B-end funds. Taking Xiaoying Technology as an example, according to the prospectus, as of June 30, 2018, corporate investors and institutional financing partners had contributed 15.8% of the capital.

The problem is that since June 2018, B-end funds have been away from P2P platforms. It is not difficult to understand that after the explosion of thunder, the uncertainty of P2P platform has greatly increased. The B-end funds pursue safety first, and are not as stable as personal funds, although personal funds are also affected by emotions. The "escape" of B-end funds shows that the market lacks confidence in the institutional credit of P2P platforms. At this time, it is much more difficult to expand B-end funds than personal funds.

In terms of P2P platforms, capital cannot be raised and asset capacity shrinks. Rather than letting the borrowers drain naturally, we should actively divert the borrowers to licensed financial institutions to earn a flow fee. The borrower is the core asset of the P2P platform. It is hard to avoid the suspicion of drinking poison to quench thirst. However, in a specific period when space is needed for time, it is not a way of survival.

In addition, powerful shareholders can also be introduced to exchange shares for time. Since the second half of 2018, many P2P platforms have chosen to go public with blood IPO, which, to some extent, also has this effect.

Outlook

There are two sides to everything, especially the dilemma. If you can't cross this threshold, you will sink a boat on the side. If you cross this threshold, you will see a bright future.

Since the establishment of the first P2P platform in China in 2007, the P2P industry has seen many ups and downs in just ten years. It is needless to mention that for practitioners who want to develop in the long run, P2P has always lacked a "compliant" identity, which may be a deep regret.

The emergence of P2P thunder wave is a critical hit for the normal operation of the platform; It is also a catalyst and accelerator for the platform to obtain compliance identity (filing). This can be regarded as a gift and gift given to P2P platform by the explosion of thunder.

But who can get this gift?

(The author of this article introduces: Director and Senior Researcher of Internet Finance Center of Suning Financial Research Institute.)