Article/Dai Zhifeng, columnist of Sina Financial Opinion Leader (WeChat official account kopleader)

Now the "policy bottom" is clear, and the "economic bottom" is relatively long. The market will focus on reform efforts and policy implementation. Our judgment is different from that of the market: while stabilizing the economy and the market, the government will also strengthen the construction of medium - and long-term market-oriented systems, and the system dividend is worth expecting.

Key investment points

The core logic of this policy turn is to enhance "confidence". This round of financial policy shift focuses on two aspects: one is to enhance the "confidence" of private economy; The second is to enhance the "confidence" of the capital market. The "confidence" improvement of private economy mainly focuses on two points: one is to improve the financing environment of private enterprises; The second is to reduce taxes and fees. The improvement of "confidence" in the capital market focuses on two points: first, maintaining market stability in the short term, and second, strengthening the medium - and long-term market system of the capital market. In order to enhance confidence in the future, it is expected that more and more reforms will be carried out; The direction is marketization. The "policy bottom" of this round is very clear (see our report three weeks ago for details《 Heavy weight depth: how to transmit "policy bottom" to "market bottom" 》)。

The aggregate policy is "weak stimulus" 。 This round of policy change is based on the premise of preventing systemic risks 。 So the infrastructure will continue to be loose, but will not be strongly stimulated; The future goal of the real estate policy is also to hold the market. In this context, the central bank will continue to be lenient, but lenient money will not transmit credit. Our model is "time for space". The economic and credit contraction lasts for a long time, but the speed is relatively slow.

Future combination: weaker economy+more and more reforms 。 As long as there is no strong stimulus, the economic downturn is the trend, and both the policy and the market need to accept it. However, more and more reforms have been pushed out, with the goal of improving market confidence. In the words of the capital market, policies cannot be changed in the short term when EPS drops; But the policy hopes to stabilize and even improve PE; Policies enable everyone to overcome difficulties and release institutional dividends 。

Investment suggestion: optimistic about the release of institutional dividends 。 Now the "policy bottom" is clear, and the "economic bottom" is relatively long. The market will focus on reform efforts and policy implementation. Our judgment is different from that of the market: while stabilizing the economy and the market, the government will also strengthen the construction of medium - and long-term market-oriented systems, and the system dividend is worth expecting.

1、 The core logic of "policy bottom" is to enhance confidence

01

Policies and models to enhance the confidence of private economy: comprehensive support from the state+financial institutions

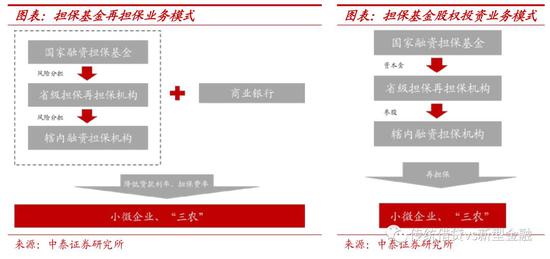

1.1 Establish a national financing guarantee fund to share risks between the government and commercial banks

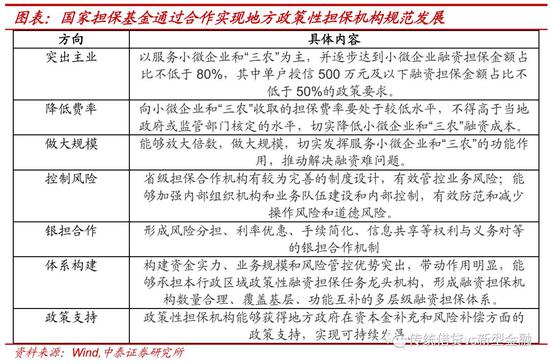

Guarantee is a normalized means of credit enhancement. The establishment of the national financing guarantee fund is a further deepening of the risk sharing mechanism between the government and commercial banks, targeting small and micro businesses and agriculture, rural areas and farmers. The earliest national credit guarantee institution in China was the China Economic and Technological Investment Guarantee Company (CETIC), which was established in November 1993. Then, during the 15-17 years, the top-level design and supporting documents on financing guarantee were successively issued. Finally, the national financing guarantee fund, which was highly concerned by the market, was officially launched in July 2018. The national financing guarantee fund is a further deepening of the risk sharing mechanism between the government and commercial banks in the previous documents. It is a quasi public fund, not for profit.

The operation mode of the national financing guarantee fund. Give priority to re guarantee business, and properly carry out equity investment business. For the financing guarantee business included in the scope of cooperation, in principle, 20% of the original guarantee amount will share the risk responsibility, and the preferential re guarantee rate will be implemented. On this basis, cooperative institutions with good risk control, less compensation and large business scale will be given appropriate risk compensation rewards; For cooperative institutions with poor risk control, more compensation and small business scale, risk compensation should be appropriately reduced. Through cooperation and guidance, promote local policy guarantee institutions to gradually achieve standardized development, repair the risk preference of banks and other financial institutions, and ease the financing pressure of SMEs.

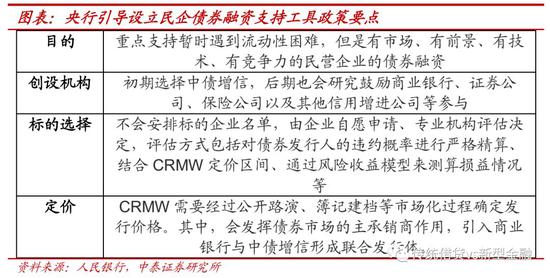

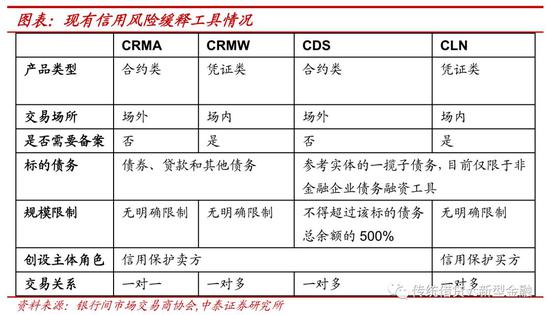

1.2 Guide the establishment of private enterprise bond financing support tool - credit risk mitigation tool (CRM)

There are policy guidelines before credit risk mitigation tools, But the market implementation has been slow. The earliest attempt in the domestic market was in 2010 Bank of China The Inter market Dealers Association issued the Guidelines for Pilot Business of Credit Risk Mitigation Tools in the Inter bank Market, and launched two products: credit risk mitigation contracts (CRMA) and credit risk mitigation certificates (CRMW). Then in 2016, the Association of Dealers launched a revised version of the Pilot Business Rules for Credit Risk Mitigation Tools in the Inter bank Market, and launched two new products: credit default swaps (CDS) and credit linked notes (CLN). However, at the initial stage of CRM launch, the domestic credit environment was relatively stable, the scale and number of bond defaults were small, and the implementation of CRM market has been slow. By the end of 2017, only 10 CRMW products had been released.

In October, the central bank raised credit risk mitigation tools again, and CRMW issuance accelerated 。 On October 22, the People's Bank of China issued a notice specifying that it should guide the establishment of private enterprise bond financing support tools, support private enterprise bond financing in a market-oriented way, and at the same time increase the 150 billion yuan of refinancing line for supporting support.

1.3 Increase rediscount and refinancing line

The core change points of this re loan line adjustment: It is mainly to cooperate with and guide the establishment of private enterprise bond financing support tools to achieve targeted credit delivery. The refinancing rediscount tools can be divided into two categories: one is the liquidity refinancing and rediscount that provide short-term liquidity support, and the other is the refinancing that supports agriculture, small businesses and poverty alleviation to achieve targeted credit support. Since 2012, the central bank has raised the amount of refinancing and rediscount for many times, aiming to achieve targeted funding support. This refinancing rediscount, in cooperation with private enterprise bond financing support tools, focuses more on strengthening targeted money supply, and can be more accurately combined with private enterprise credit enhancement function by separating private enterprise debt transactions from their risk transactions.

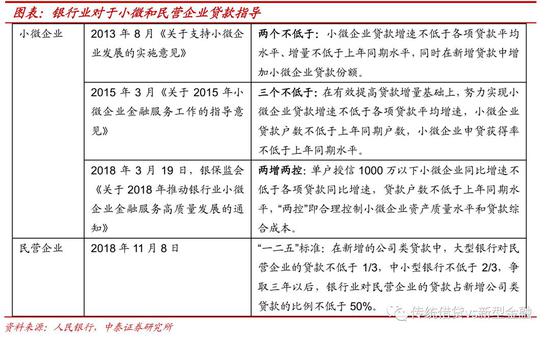

1.4 "One Two Five Year Plan" Policy to Increase Loan Support for Private Enterprises

The original intention of the "12th Five Year Plan" policy is to force commercial banks to increase the enthusiasm of private enterprise loans, Only when the target is set high, can the reverse force effect be achieved. On November 7, Guo Shuqing, Chairman of the Banking and Insurance Regulatory Commission, said that it was preliminarily considered that loans to private enterprises should achieve the goal of "One Two Five Year Plan": That is New corporate loans The loans from large and medium-sized banks to private enterprises should not be less than 1/3, and that from small and medium-sized banks should not be less than 2/3. Three years later, the proportion of loans from the banking industry to private enterprises should not be less than 50% of new corporate loans. The previous regulatory guidance for commercial banks was mostly aimed at small and micro enterprises, such as the "three not lower than" goal proposed in 2015 and the "two increases and two controls" goal proposed in March 2018. This "12th Five Year Plan" policy is the first time to put forward requirements for private enterprise loans. The goal is to increase the enthusiasm of commercial banks for private enterprise loans, and dredge the transmission channel from money to credit.

We expect that the "One, Two, Five" principle will not become a regulatory indicator (not mandatory), but a similar monitoring indicator. In the future, the bank will ensure the rapid growth of private enterprise loans, but will not ignore the risks, making the growth of private enterprise loans too fast.

02

Policies and models to enhance confidence in the "capital market": repurchase+financing+sentiment three levels of progression to improve market liquidity

Multiple policies eased the liquidity pressure of private enterprises, and the pressure on stock quality of the market to recover was relieved. Since November 9, policies in the field of non banking have provided policy support to the market in terms of liberalizing mergers and acquisitions, encouraging listed repurchases, special asset management plans of financial institutions, optimizing transaction supervision, establishing a pilot registration system for the Science and Technology Innovation Board, and continuing to expand opening up, with different effects.

2.1 Repurchase policy plays the most direct role

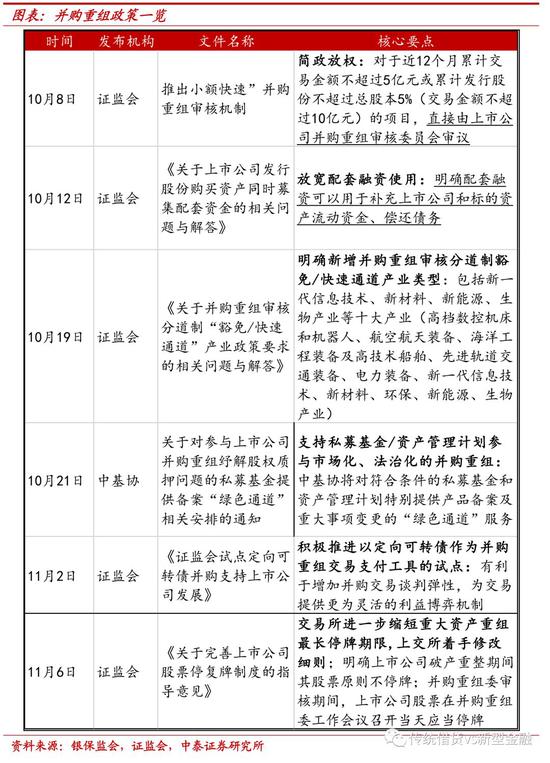

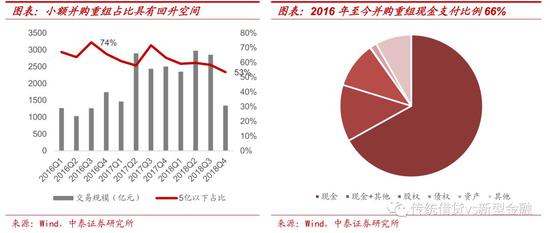

Repurchase is an effective tool to enhance investor confidence in mature capital markets, optimize decision-making procedures, and improve the enthusiasm of active market value management. Institutional issues The Ministry of Justice pointed out in the notes on the drafting of this amendment that too strict procedural requirements made it difficult for listed companies to seize market opportunities in time and reasonably arrange repurchase plans. After enterprises disclosed repurchase plans in actual operation, the stock price often rose above the repurchase price range. This procedure is simplified to the resolution of the board of directors, and the acquisition of no more than 10% of shares is expected to have a greater role in boosting the enthusiasm of listed companies. From the data, although the number and scale of stock incentive active repurchases have increased since 2018, the proportion has declined significantly year on year, and there is much room for subsequent growth.

2.2 Rescue plan: launch fast, focus on layout and solve pain points

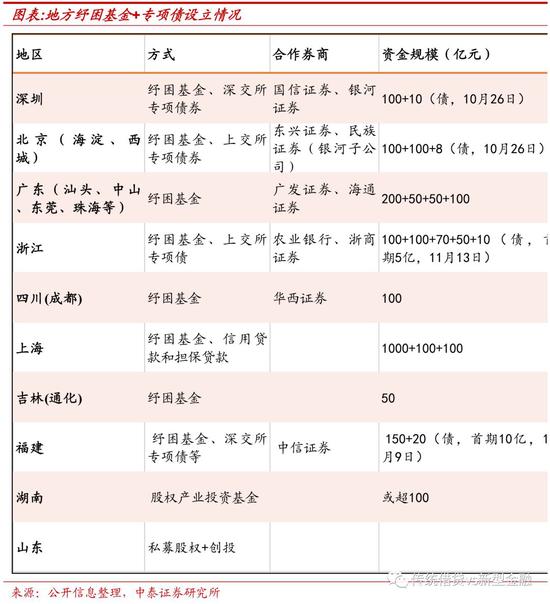

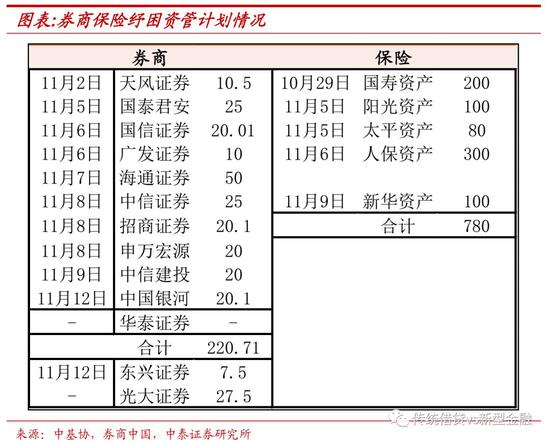

The non bank financial rescue plan was launched quickly. The current methods can be classified into four categories: 1) Resolve through stock pledge business of securities companies The new OTC stock pledge transaction to solve the stock default contract is not recognized as a new contract. 2) Make financial investment by setting up a special asset management plan, As of November 12, the asset management plans of 11 securities companies have been filed, involving 22.8 billion yuan of capital. Later, it is planned to expand the scale of social fundraising, and five insurance companies have set up plans to invest 78 billion yuan. 3) Set up a master sub fund to invest through private fund subsidiaries, Galaxy Securities plans to raise 60 billion yuan. 4) Establish a rescue fund through cooperation with local governments At present, more than 10 provinces and 9 cities have set up rescue funds, with a total size of more than 100 billion yuan, Kangdexin 、 Wanxun Automatic Control And other company announcements.

Financial institutions+local governments, focus on the layout to solve the pain points 。 Local government funds have been put into use quickly in a variety of ways, including financial investment in equity: 1) direct acquisition of old shares, and the purchase price is expected to be "one enterprise, one policy"; 2) Cash capital increase and fixed increase of shares; Creditor's rights: 1) undertaking stock pledged assets through bridge loans, entrusted loans, creditor's rights acquisition, etc; 2) Special bonds to support the development of science and technology enterprises; Local governments have a better understanding of the local area, and most of them have medium - and long-term plans. They can communicate more smoothly on the follow-up improvement and growth of enterprises, and pay more attention to the sustainability of planned cities.

2.3 Merger and reorganization: supporting financing to supplement liquidity and encourage various funds to participate

The way of payment for raised funds was improved, allowing the supplement of working capital to enhance the enthusiasm of enterprises to participate. 1) Guarantee the quality and efficiency improvement of M&A and restructuring business We will practice the "road separation system", better serve the development of the real economy in the system, and shorten the application period for failed IPO M&A and reorganization, which has a significant signaling effect. 2) It provides a new payment tool for mergers and acquisitions of listed companies , promote the pilot project of directional convertible bonds proposed in 2014, and play a positive role in facilitating M&A and restructuring transactions; 3) Widening the path of private equity fund M&A and reorganization , gradually close to the European and American market model, encourage financial institutions to set up M&A funds to participate in. Under a series of policies, private equity funds can also gradually close to the European and American market model by means of early venture investment, assisting the company in capital operation, holding LBO, etc; 4) Direct mitigation of equity risk It is allowed to supplement funds and improve the liquidity risk of enterprises.

2.4 Market system reform: improve the construction of multi-level capital market

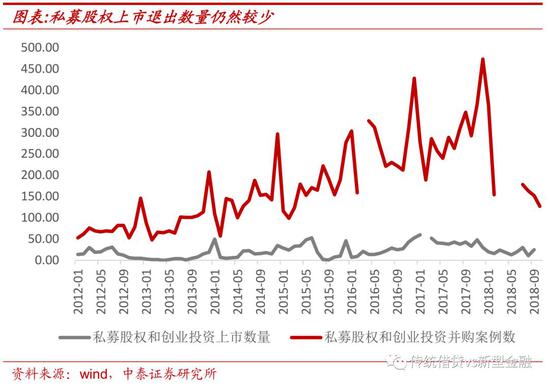

The pilot registration system of the science and technology innovation board, expand the scale of direct financing, and improve the construction of multi-level capital markets 。 1) As an innovation market in the existing sector, the Science and Technology Innovation Board continues to focus on the national innovation drive and science and technology development strategy, In the future, we can expect to promote pilot reforms in the medium and long term, including the registration system and delisting system The regulatory logic may become more market-oriented and become an important step in the construction of a multi-level capital market. 2) In terms of impact, In the short term, it is beneficial for venture capital funds to broaden the exit channels of early investment and improve the performance of venture capital, The medium and long term are conducive to attracting early investors, expanding direct financing, and helping SMEs grow.

Summary: The core logic of this policy shift is to enhance "confidence". This round of financial policy shift focuses on two aspects: one is to enhance the "confidence" of private economy; The second is to enhance the "confidence" of the capital market. The "confidence" improvement of private economy mainly focuses on two points: one is to improve the financing environment of private enterprises; The second is to reduce taxes and fees. The improvement of "confidence" in the capital market focuses on two points: first, maintaining market stability in the short term, and second, strengthening the medium - and long-term market system of the capital market. In order to enhance confidence in the future, it is expected that more and more reforms will be carried out; The direction is marketization.

2、 Aggregate policy (currency and policy) is a weak stimulus: worry about future systemic risks

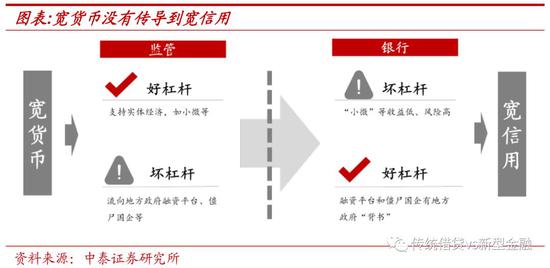

Why can't loose money transmit to loose credit? Because the policy did not stimulate real estate and local financing platforms 。 Since the top management is still worried about systemic risks and will not stimulate real estate and local financing platforms, the regulatory framework still distinguishes between "good leverage" and "bad leverage", which is the so-called "optimizing leverage structure". In fact, the behavior of banks is also divided into "good leverage" and "bad leverage". If the central government implicitly guarantees, real estate and infrastructure are undoubtedly the best for banks, while banks in other fields worry about risks and are more cautious. The contradiction between the two sides' behaviors, like two gears, has blocked our credit expansion.

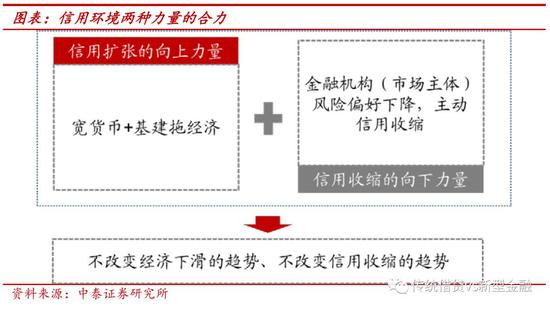

Weak stimulus, hoping to support the economy 。 In the future, the aggregate policy will be weak stimulus: loose money will continue to be loose, high-level infrastructure will be relaxed, and real estate will be fine tuned. However, the downward force of the economy is still: the risk preference of financial institutions and market entities is declining, and the market is actively contracting credit. The weak stimulus of the policy continues, and the market economy itself is downward. The result of the joint efforts of both parties is that the trend of economic decline and credit contraction will not be changed; The ability and willingness to change are speed and slope.

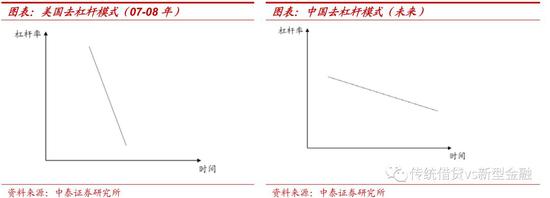

Our economic "clearing" mode: time for space. In comparison, the U.S. deleveraging model in 2007-08: quick marketization clearing (advantages), short-term misery and pain (disadvantages). The mode of deleveraging: time for space. It is relatively stable (advantages) and takes a long time (disadvantages). Therefore, it will be a long time for our "economic bottom" to emerge.

3、 Future combination: weaker economy+more and more reforms

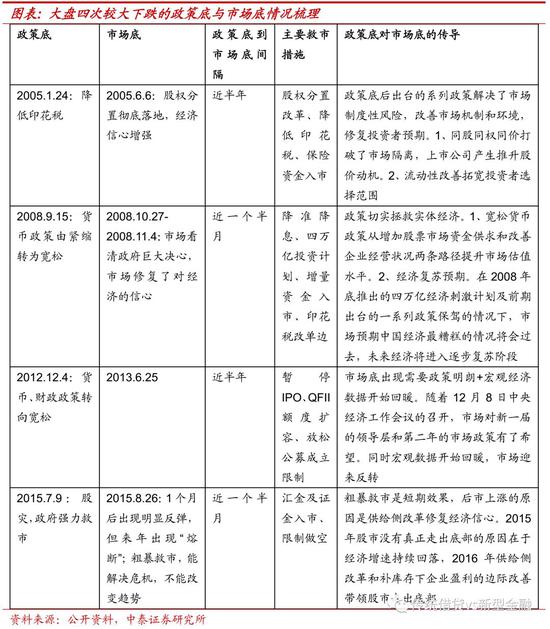

Review of the process of our four bail outs: in fact, they are all "strong stimulus"+"weak reform". We compared the process of four policy rescues in 2005, 2008, 2012 and 2015. Generally speaking, the "market bottom" is between the "policy bottom" and the "economic bottom" (see our in-depth report for details:《 Heavy weight depth: how to transmit "policy bottom" to "market bottom" 》), These four times, the "economic bottom" is actually the result of monetary and fiscal policy stimulus; After the "economic bottom" appeared, the market reform was weakened. But this time, the policy will not be strong and sustainable. The "economic bottom" is a relatively long thing, and reform cannot be avoided. Everyone has said for a long time that "reform has come to the deep-water area", and this time it is true.

The market will be more tangled in the future. On the one hand, the economy continues to bottom out, and the company's EPS declines. The policy cannot be stimulated in the short term. On the other hand, there are more and more policy reforms, and the policy hopes to stabilize or even improve the valuation (PE); The policy allows everyone to overcome difficulties and release institutional dividends. The rise and fall of the stock market is the game and entanglement between this downward force and an upward force.

Observe the reform intensity and implementation effect. The market will continue to observe the strength of market-oriented reform and the implementation of various policies, so as to judge whether the market valuation can be improved. The market may be "no rabbit, no hawk". There will also be a game between policy and market.

4、 Investment suggestion: Be optimistic about the release of institutional dividends

Be optimistic about the release of institutional dividends 。 Now the "policy bottom" is clear, and the "economic bottom" is relatively long. The market will focus on reform efforts and policy implementation. Our judgment is different from that of the market: while stabilizing the economy and the market, the government will also strengthen the construction of medium - and long-term market-oriented systems, and the system dividend is worth expecting.

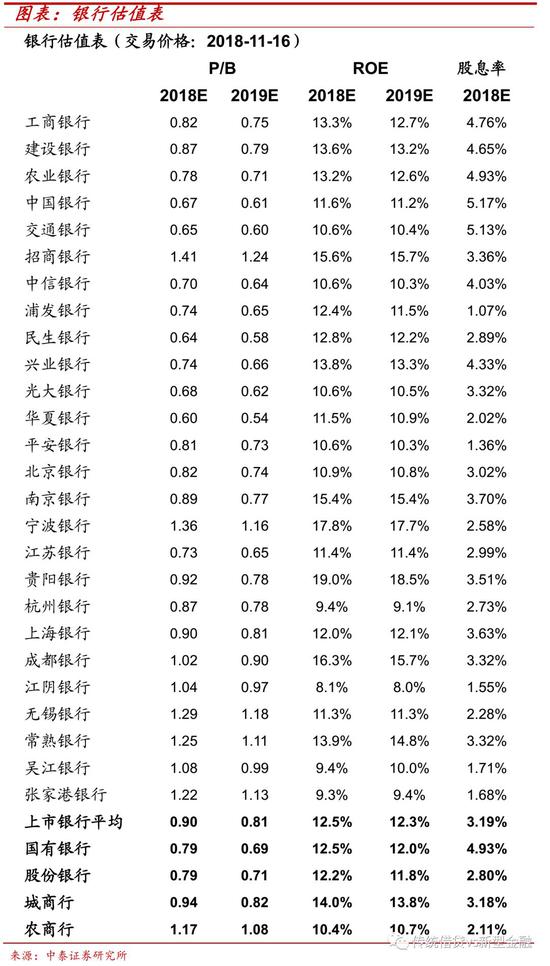

We are optimistic about the steady earnings of bank stocks. The weaker the market, the stronger the banks will be; The stronger the market, the weaker the banks will be. However, in both cases, bank shares can maintain "steady" returns, which would be a good allocation variety. The core logic of selecting bank shares next year is "asset quality".

(The author of this article introduces: Chief of the banking industry of Zhongtai Securities, head of the financial team, and a special researcher of the National Finance and Development Laboratory.)