Article/Sina Financial Opinion Leader (WeChat public account kopleader) columnist Sheng Songcheng, Long Yu

At present, it is very important to maintain the basic stability of the RMB exchange rate at a reasonable and balanced level, regardless of the constraints faced by China's economy and finance in the short term or the long-term stable and healthy development of China's economy. The benefits of exchange rate stability are far greater than its costs.

China implements a managed floating exchange rate system based on market supply and demand, adjusted by reference to a basket of currencies. After years of reform, RMB exchange rate pricing has become more and more market-oriented. Since this year, affected by trade frictions, changes in the international exchange market and other factors, plus the recent downward pressure on China's economy, the foreign exchange market has shown signs of pro cyclical fluctuations. On October 26, the central parity rate of the RMB against the US dollar fell below 6.95 for the first time since the beginning of last year, marking the fourth consecutive trading day of depreciation, with a cumulative reduction of 247 basis points. The deficit of foreign exchange settlement and sales of banks in September was US $17.6 billion, significantly larger than that in August, and the largest deficit since last June. This does not prevent people from recalling the "war of defense" of exchange rate and foreign exchange reserves at the end of 2016. At that time, I made it clear that we should seize the best opportunity to stabilize exchange rate expectations, and avoid the negative impact of exchange rate overshoot on the economy, or even trigger large-scale capital outflows, endangering financial stability. In the period when the depreciation expectation is still controllable, stabilizing the exchange rate at a lower cost can effectively reduce panic, enhance public confidence, and avoid the double losing situation of the loss of foreign exchange reserves and the loss of exchange rate. The practice has preliminarily confirmed that the overall thinking and policy measures of China's exchange rate regulation in the last year or two are correct. It not only maintains the basic stability of the exchange rate, but also does not cause excessive reduction of foreign exchange reserves.

Recently, the market has a strong expectation of RMB depreciation, the macro-economy is not stable enough, and the prospect of Sino US trade friction is unclear. Therefore, it is not a good time to free the RMB exchange rate. Whether the exchange rate of RMB against the US dollar will break the "7" has also been hotly discussed again, and has become an important psychological threshold. First of all, from the perspective of market transactions, first, falling below the key threshold will trigger a large area of stop loss transactions, artificially "creating" exchange rate devaluation, and second, it will urge the trading subjects who originally stayed on the sidelines to enter the market in the short direction. All these factors will cause the exchange rate to overshoot. Secondly, expectation is a major factor affecting the short-term exchange rate. Once an important psychological threshold is breached, it will trigger the readjustment of market expectations and further reduce the valuation of the exchange rate. As expectations are self fulfilling and self reinforcing, the impact of key points on market expectations cannot be underestimated. In fact, there is no question of whether to "preserve exchange rate" or "preserve reserves". If the exchange rate falls below an important threshold, it will cost more to maintain the stability of the exchange rate, which will also make the monetary authority more passive. This is the significance of the key point.

At present, it is very important to maintain the basic stability of the RMB exchange rate at a reasonable and balanced level, regardless of the constraints faced by China's economy and finance in the short term or the long-term stable and healthy development of China's economy. The benefits of exchange rate stability are far greater than its costs.

1、 Under the downward pressure of the economy, "foreign exchange reform" should not be carried out alone

The good time for "exchange rate reform" is often when the domestic and foreign economies are relatively stable, especially when the domestic fundamentals are good. At present, China's economy is under downward pressure. Although the manufacturing PMI in October showed that the economy remained in the boom zone, there was a significant decline (the manufacturing PMI index recorded 50.2), which was the lowest since August 2016. From the PMI sub index, the index of new orders, new export orders and orders in hand declined significantly. The order related drama index declined more. The new order index was 1.2 percentage points lower than last month, and the new export order fell 1.1 percentage points month on month. The economic downturn may further pressure the exchange rate, but the more this is the case, the more it is not suitable to carry out "foreign exchange reform" alone.

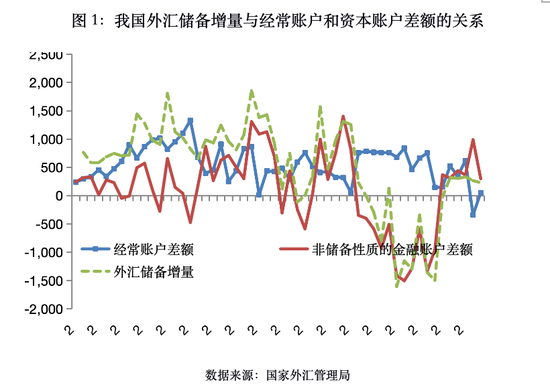

After years of reform, RMB exchange rate pricing has become more market-oriented. Capital flow has an increasing impact on China's exchange rate pricing, and the asset price attribute of exchange rate is strengthening. From the perspective of changes in foreign exchange reserves in the balance of payments, in the past, changes in China's foreign exchange reserve increment were mainly driven by the current account balance, but in recent years, it has been driven by the capital account balance (Figure 1). In the current economic and financial situation, if the exchange rate is allowed to float freely, I am afraid that it will not have the effect of stabilizing capital flows, but will be counterproductive. Short term capital flows are vulnerable to fluctuations in market sentiment, and even deviate significantly from fundamentals, resulting in exchange rate overshoot. Just as on the eve of the "August 11" exchange rate reform, the market's estimate of the RMB equilibrium exchange rate was generally about 2% devaluation. However, after the one-time devaluation of the central parity rate of the RMB against the US dollar, the exchange rate did not seem to be adjusted in place at one time. Instead, the market expected that the RMB would further depreciate, as if opening a "Pandora's box". It can be said that we are not prepared enough, or even unexpected, to bear great pressure on the RMB exchange rate after the exchange rate reform on August 11, 2015. Therefore, it is necessary to reflect and summarize historical experience.

In addition, promoting the "exchange rate reform" requires the coordination and cooperation of various reforms in China's economic and financial fields. A more flexible exchange rate system needs a financial system that can withstand exchange rate fluctuations, a market-oriented interest rate formation and transmission mechanism, sound macro prudential management, and a mature foreign exchange market. Financial reform should also be coordinated with the reform of the real economy, macro-control policies and economic transformation and upgrading. Coordination and cooperation means that the order of reform is not always the same, nor does it mean that the reform in a single field is infinitely lagging behind, but that the reform is carried out more smoothly and at a lower cost.

2、 Exchange rate fluctuations do not ensure the independence of monetary policy

The famous "impossible triangle" theory (also known as the "ternary paradox") believes that fixed exchange rate, free capital flow and the effectiveness (or independence) of monetary policy cannot be satisfied at the same time. The policy implication of this theory is that if we want to maintain the effectiveness of monetary policy and realize the free flow of capital, we must give up the fixed exchange rate system. The "Three Paradox" points out that a more floating exchange rate system has strengthened the ability of countries to absorb external shocks and enhanced the independence of monetary policy, which is a theoretical basis for supporting a clean exchange rate floating.

However, in practice, the policy choices of most countries are not located in the corner of the "impossible triangle", but widely used intermediate policy choices. Moreover, macro prudential management measures can effectively alleviate the so-called triangular conflict. China itself is an example. China's monetary policy is highly independent, and the domestic economic and financial situation is the main consideration. For example, on September 26, the Federal Reserve announced that it would continue to raise the target interest rate range of the federal funds by 0.25 percentage points. The People's Bank of China did not follow the United States in raising interest rates, but kept the exchange rate basically stable at a reasonable and balanced level through foreign exchange risk reserve policy and other means.

The "ternary paradox" has also been challenged theoretically. The Impossible Triangle Theory does not fully consider the influence of big countries on the international market and other countries' economic and policy choices, so big countries have a strong ability to implement monetary policies independently. Some studies also show that the loss of the independence of monetary policy does not depend on the choice of the exchange rate system of each country. Even under the floating exchange rate system, the exchange rate can also affect the macro-economy through the current account and asset price channels, thus requiring the monetary policy to respond accordingly and restricting the independence of monetary policy.

From the "ternary paradox" to the "dualistic paradox", it reflects that exchange rate fluctuations may not always effectively hedge against external shocks and act as a "stabilizer" of the macro-economy. On the contrary, large fluctuations in the exchange rate will have a negative impact on the stable operation of the macro-economy, which has been repeatedly proved by historical experience. In other words, there are many controversies about what kind of exchange rate system is ideal in theory, but the actual impact of the big fluctuations of exchange rate is real.

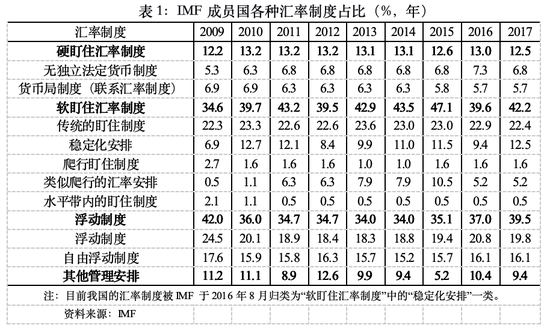

According to IMF statistics, the number of countries adopting stabilization arrangements in the exchange rate system is increasing. Table 1 shows the percentage of exchange rate regime classification of IMF member countries. The proportion of countries implementing the floating exchange rate system dropped from 42% in 2009 to 39.5% in 2017, of which the proportion of countries adopting the free floating exchange rate system dropped by 1.5 percentage points during this period. The proportion of countries implementing the soft pegged exchange rate system increased from 34.6% in 2009 to 42.2% in 2017, of which, the proportion of countries adopting stabilization arrangements in the exchange rate system increased by 5.6 percentage points in eight years. China's current exchange rate system arrangement also belongs to this category.

Why have more countries adopted stabilization arrangements in their exchange rate systems in the past decade? What is the significance of a completely free floating exchange rate? Too frequent exchange rate fluctuations often increase the transaction costs of the real economy. In the special period when the international financial crisis broke out in 2008, the RMB briefly resumed its peg to the US dollar. As an "extraordinary means" to deal with the global financial crisis, it is also a choice to reduce transaction costs in a sense.

3、 Exchange rate stability is conducive to international trade and investment

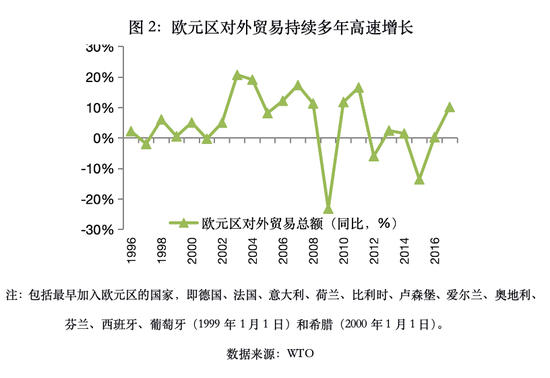

A stable exchange rate will expand the scope for economic entities to participate in cross-border economic activities. For example, the euro (which can be regarded as a special case of the fixed exchange rate system) was born on the basis of the economic integration of the European continent, and monetary integration is crucial to the maintenance of the European unified market. After almost all trade barriers have been eliminated, attempts to promote net exports through currency depreciation will not be welcomed by other member countries. Research shows that from the collapse of the Bretton Woods system to the early days of the establishment of the euro area, current account balance, GDP growth, and terms of trade relative to the currency anchor country (Germany) have significantly reduced the devaluation rate and exchange rate fluctuations of EU member countries. The Eurozone clearly believes that the benefits of implementing a fixed "exchange rate" among member countries are greater than their costs, so it is willing to give up its exchange rate policy. After the establishment of the Eurozone, the overall trade volume of the Eurozone also continued to grow significantly (Figure 2). From 2000 to 2008, the average annual growth rate of the total volume of imports and exports of goods in the euro area reached 11%, from US $3.74 trillion in 2000 to US $8.96 trillion in 2008, 2.4 times that at the beginning of the establishment of the euro area.

Of course, maintaining the stability of the exchange rate is faced with a similar challenge to sticking to the fixed exchange rate system, that is, the risk of speculative currency sniping. However, China's large-scale foreign exchange reserves provide adequate protection against short-term fluctuations in exchange rates. By the end of 2017, the ratio of short-term foreign debt to foreign exchange reserves in China was only 35% (the international alert standard is that foreign exchange reserves are not less than one time of short-term foreign debt), with a high margin of safety. However, the big fluctuations of exchange rate are not conducive to the current situation of China's trade. China is known as the "world factory". The manufacturing industry accounts for 93.7% of China's exports and 64.9% of China's imports (2016). At present, China is still at the lower end of the global value chain. Exchange rate risk has a high price transmission effect on China's trade sector, and producers are forced to bear exchange rate risk. Therefore, from the perspective of trade, the benefits of maintaining a stable RMB exchange rate at this stage are also greater than its costs.

It is worth mentioning that we cannot continuously rely on low prices to gain competitive advantage. Letting the RMB depreciate will make enterprises lack incentives to improve product quality and enhance core competitiveness. When China's products have enough advantages, they are no longer passive bearers of exchange rate fluctuations, but can actively transfer exchange rate risks, the free floating of RMB will also have more space.

In the short term, with the G20 meeting approaching, the Sino US trade negotiations are ushering in a critical time window. If the RMB exchange rate is allowed to depreciate pro cyclically at present, it will easily lead to the escalation of the already tense Sino US trade friction. At the beginning of the Sino US trade friction, the RMB was still appreciating and rising very fast, even rising to the 6.2-6.3 range against the US dollar. At that time, I made it clear that to avoid Sino US trade friction turning into financial friction, we should neither guide the devaluation of the exchange rate nor allow the exchange rate to appreciate significantly. If the exchange rate issue and trade friction overlap, the situation will be more complex. In the report issued by the US Treasury Department on October 18, China was not listed as an exchange rate manipulator. In fact, both China and the United States do not want the RMB to depreciate significantly. The Brexit of the United Kingdom and the United States' provocation of trade frictions have, to some extent, cast the world in the shadow of "anti globalization". Maintaining a stable exchange rate also helps to curb the further deterioration of the international trade situation.

4、 Stable exchange rate is suitable for the internationalization of RMB and China's economic development at this stage

The stability of RMB exchange rate is more conducive to the current stage of RMB internationalization. RMB is the sixth largest payment currency in the world, but its market share is only 1.68%. At the same time, the RMB ranked seventh among reserve currencies, accounting for 1.39%, much lower than the Japanese yen (4.81%) and the British pound (4.81%), while the US dollar and the euro accounted for 62.48% and 20.39% of the reserve currencies, respectively. Obviously, the internationalization of RMB has a long way to go. RMB internationalization cannot be completed overnight, nor is it urgent to seek success. Whether considering international or domestic, economic or financial factors, it is not a good time to promote the internationalization of RMB. However, in this process, maintaining a relatively stable exchange rate is conducive to establishing the worldwide credit of RMB. Just as the US dollar was linked to gold at the beginning of internationalization (i.e. gold exchange standard system), this will help the US government win the reputation of anti inflation. In 1973, when the Bretton Woods system collapsed and the dollar was decoupled from gold, the dollar had become the world currency.

From the history of the internationalization of the US dollar, we can see that the exchange rate system of developed countries has also undergone long-term evolution, which has formed today's appearance. The choice of exchange rate regime and exchange rate policy will be affected by a country's economic structure and development stage, because its impact on different economic entities is different. For example, non trade sectors often benefit from the strong local currency, while foreign trade sectors want to see the depreciation trend of their own currencies.

In the history of the United States, there have also been heated debates about the exchange rate policy. In the late 19th century, commercial institutions and international financial institutions with a large amount of international exposure were the main supporters of the gold standard, while trade goods producers expected the dollar to depreciate, and the latter naturally opposed the gold standard. Behind the fierce struggle of the United States on the gold standard is that in the 19th century, the United States was a leading producer of primary products, with a large number of agricultural products and raw materials exports. At the same time, it was the world's largest debtor country, with a powerful international financial sector.

No exchange rate system is suitable for all countries and all periods of a country. China's national conditions determine the complexity of exchange rate selection. As a transitional economy, China's financial market is not deepened enough, its economic system needs to be improved, and its economic structure is still in the process of transformation. At the same time, China is the world's largest trading country, with a considerable economic volume and influence. Although from the general rule, large countries tend to choose floating exchange rate system and flexible exchange rate policy, it is the practical need of our current development stage to manage the floating exchange rate.

In a word, considering the short-term economic and financial situation at home and abroad and the medium and long-term reform and transformation and development of China's economy, the reform of individual breakthroughs often outweighs the gains and losses, and maintaining the stability of the RMB exchange rate is more urgent at the moment.

The formulation of exchange rate system and the choice of exchange rate policy should be tools that serve the economic development of a country. The flexible and two-way fluctuation of exchange rate itself should be a means to effectively mitigate external shocks, not the ultimate goal, and should not therefore reverse restrict the initiative of macroeconomic and financial regulation. With the continuous improvement of China's financial system and financial market, as well as the peaceful, stable and healthy development of economic transformation and upgrading, if China can be less and less constrained by exchange rate fluctuations and has a stronger ability to pass on exchange rate risks, there will be no so-called "fear of floating".

This article only reflects the views of the author, not the views of the organization

(The author of this article introduces: counselor of the People's Bank of China, part-time professor of China Europe International Business School.)