Article/Dai Zhifeng, columnist of Sina Financial Opinion Leader (WeChat official account kopleader)

The operation will be relatively simple in the near future. Next March is a vacuum period for bank fundamentals, during which investment is relatively clear.

Key investment points

Overall performance: the growth rate is fast, and scale is still the main contributor to the performance. 1. Net interest income: the overall month on month growth of listed agricultural commercial banks is positive, but there are differences among individual stocks. The difference in month on month growth of net interest income between individual stocks is mainly reflected in the difference in interest margin. At the same time, in the third quarter, the Rural Commercial Bank showed a comparative advantage on the debt side. 2. Non interest income: the service charge performance is weak, mainly driven by net other non interest income. 3. Cost income ratio: The marginal decrease trend in the third quarter is related to the rapid growth of revenue.

Growth rate and structure of asset side scale: 1. The growth rate of interest bearing asset scale has widened on a month on month basis driven by loans and bond investment, which is greater than the overall marginal improvement of listed banks. Among them, the month on month growth of loans continued to expand, while bond investment achieved positive growth in the third quarter on the basis of month on month drop in the second quarter. 2. The month on month growth of loans and bond investment led to a further increase in the proportion of interest bearing assets.

The scale growth and structure of the liability side: 1. The scale growth is matched with the asset side, which is mainly supported by the deposit scale. At the same time, the scale of bond issuance has also increased significantly compared with that of the second quarter, while the scale of interbank liabilities has continued to decline. Among them, the growth of interest bearing liabilities is mainly driven by deposits and bond issuance. The scale of interbank liabilities fell for three consecutive quarters. 2. The proportion of core liabilities increased, and the structure of active liabilities was adjusted. Over the same period, the proportion of total deposits of listed banks in interest bearing liabilities declined.

Asset quality continues to improve, and adverse pressure will drop in the future. 1. Rejection rate: In the third quarter, the overall non-performing rate of Rural Commercial Bank was 1.5%, down 1 bp month on month. 2. Single quarter annualized net generation of non-performing products: The overall month on month decline was 0.38 percentage points, and the marginal improvement was better than that of listed banks. 3. The overall asset quality pressure of rural commercial banks has declined : The proportion of special interest loans decreased month on month. 4. The overall provision of Rural Commercial Bank is relatively adequate, and the allocation coverage ratio and loan allocation ratio are higher than the average level of listed banks. The overall allocation coverage rate of Rural Commercial Bank increased, 60 percentage points higher than that of listed banks.

whole The corporate capital is relatively sufficient, and the growth rate of risk weighted assets is less than that of loans. The core tier one capital adequacy ratio of Rural Commercial Bank increased by 6bp to 11.19% month on month. The month on month growth of overall risk weighted assets was wider than that of the second quarter, and the growth rate was slightly lower than that of loans.

Investment suggestion: the operation will be relatively simple in the near future. Next March is a vacuum period for bank fundamentals, during which investment is relatively clear. 1. For relative returns, If the market is weak, the bank shares will be strong; if the market is strong, the bank shares will be weak; 2. For absolute return investors, observe the flow of allocated funds (overseas funds, large institutional funds and national teams) for medium and long-term assessment; 3. Since we judge that the "policy bottom" is clear (see details in depth《 Heavy weight depth: how to transmit "policy bottom" to "market bottom" 》)The steady return of banks is predictable.

Risk warning event: economic downturn exceeded expectations. Financial regulation exceeded expectations.

1、 Overall performance: rapid growth, mainly due to scale contribution

agriculture The year-on-year growth rate of the overall performance of commercial banks is higher than the average of listed banks, and the growth rate is higher than that of listed banks. Against the background that the performance of listed banks in the third quarter continued to rebound year on year, the overall rebound of Rural Commercial Bank was stronger, and the overall growth rate was higher than the average level of listed banks. The average revenue of Rural Commercial Bank in the third quarter was 17.2% year on year, 1.5 percentage points higher than that in the second quarter; PPOP was 17.4% year on year, 2.1 percentage points higher month on month; Net profit was 15.8% year on year, up 0.4 percentage points month on month. From the perspective of individual stocks, Jiangyin, Changshu and Zhangjiagang are the top three in terms of income growth; Changshu, Wujiang and Zhangjiagang are the top three in terms of profit growth.

The rapid year-on-year growth of performance is mainly due to the contribution of scale. Year on year splitting of agricultural and commercial industry performance in the first three quarters: 1) Scale contribution: The positive contribution to performance has been improved, far higher than the overall level of listed banks. 2) Margin: The positive contribution to performance has increased significantly, which is different from the change of the positive contribution of the overall interest margin of listed banks. 3) Non interest: The positive contribution to performance slightly weakened, still higher than the average level of listed banks.

Further split the revenue of agricultural commercial banks. The overall net interest income of Rural Commercial Bank continued to increase on a month on month basis on the high growth in the second quarter, but there were differences between individual stocks. Among them, the net interest income of Jiangyin and Changshu grew faster month on month, 28.1% and 11.5% respectively, Wujiang Bank On the basis of the negative month on month growth of net interest income in the second quarter, the third quarter saw a 9.9% month on month growth. However, the month on month growth of net interest income in Wuxi and Zhangjiagang slowed down, including Zhangjiagang Branch Net interest income in the third quarter grew negatively month on month.

Continue to split the net interest income. The month on month ratio of net interest income is highly correlated with the month on month ratio of interest margin. From the performance growth split quarter on quarter, the interest margin of Jiangyin, Changshu, Wujiang and Wuxi contributed positively to the performance, while the interest margin of Zhangjiagang Bank contributed negatively, This is consistent with the month on month growth trend of net interest income. Specifically, 1) Margin: The interest margin of Jiangyin, Changshu, Wujiang and Wuxi rose 51, 22, 13 and 1 bp month on month respectively, while that of Zhangjiagang narrowed by 17 bp month on month. 2) Scale: Interest bearing assets achieved positive month on month growth in the third quarter, including Changshu Bank On the basis of the high growth in the second quarter, the month on month growth slowed down, and the scale of other rural commercial banks grew wider than that in the second quarter.

In the third quarter, the Rural Commercial Bank showed a comparative advantage on the debt side. Continue to split the yield/interest payment rate in the third quarter. The yield of interest bearing assets of Rural Commercial Bank increased by 11bp month on month in the third quarter, higher than the overall growth of 7bp of listed banks; At the same time, the debt side interest payment rate went down 4 bp month on month, which is different from the trend of the overall interest payment rate of listed banks going up 2 bp month on month, reflecting the relative advantage of ABC in the debt side. Specifically, for individual stocks, except Wuxi and Zhangjiagang Bank, the return on interest bearing assets increased month on month. The interest bearing cost on the liability side, with the exception of Wujiang Bank, has seen a month on month decline in interest payment rates.

Net non interest income: the service charge performance is weak, mainly driven by net other non interest income. 1) As a whole, the growth rate of net non interest income in the third quarter continued to expand year on year, driven by net other non interest income. However, the net service charge income grew negatively year-on-year for three consecutive quarters, which is inconsistent with the trend of widening year-on-year growth of listed banks in the overall third quarter. 2) From the perspective of individual stocks, there is differentiation between agricultural and commercial banks. Changshu and Wujiangjing achieved positive year-on-year growth in service fee income, which, together with net other non interest income, led to positive year-on-year growth in non interest income. The net commission income of Wuxi and Zhangjiagang was relatively weak, which dragged down the year-on-year negative growth of net non interest income.

Cost income ratio: the overall cost income ratio of Rural Commercial Bank of China is higher than the average of listed banks, showing a marginal decrease trend in the third quarter, which is related to the rapid growth of revenue 。 1) As a whole, the year-on-year growth rate of business management fees of Rural Commercial Bank of China is smaller than that of listed banks, And the absolute growth rate is still relatively fast, which is determined by the overall business characteristics of Rural Commercial Bank of China, and is also related to the fact that Rural Commercial Bank of China has relatively little technology investment and relatively weak cost control ability compared with large banks. 2) In terms of individual stocks, Jiangyin, Changshu and Zhangjiagang have improved the marginal cost income ratio The year-on-year growth rate of business and management fees of Zhangjiagang Branch was lower than that of the second quarter. The year-on-year growth rate of business and management fees of Wujiang Bank also decreased by 1 percentage point compared with that of the half year, but its revenue growth rate was weak, resulting in a 0.4 percentage point increase in cost and income compared with the month on month.

2、 The asset side is driven by loans and bond investment, and the performance of individual stocks is differentiated

2、 The asset side is driven by loans and bond investment, and the performance of individual stocks is differentiated The scale of interest bearing assets grew wider month on month driven by loans and bond investment 。 1) The month on month growth of interest bearing assets of Rural Commercial Bank continued to expand And the overall marginal improvement is greater than that of listed banks. 1) From the point of view of the month on month growth of interest bearing assets of individual stocks, except Changshu, whose month on month growth slowed slightly on the basis of the high month on month growth of interest bearing assets in the second quarter, the month on month growth of the other four rural commercial banks was wider than that in the second quarter. 2) From the perspective of segmentation, interest bearing assets are driven by loans and bond investment, and the scale of interbank assets has declined month on month. Among them, the month on month growth of loans continued to expand, while bond investment achieved positive growth in the third quarter on the basis of month on month drop in the second quarter. 3) Zhangjiagang Bank's interbank assets declined significantly, reducing interbank assets and investing in bonds for three consecutive quarters. At the same time, in the third quarter, Changshu Bank also saw a large drop in interbank assets, Wuxi Bank On the other hand, interbank assets achieved positive growth month on month.

Further split bond investment and interbank assets. 1) The bond investment mainly includes the month on month growth of available for sale and held to maturity assets, It is expected to increase the allocation of local debt in the third quarter. The investment in receivables decreased for three consecutive quarters. (Due to the adjustment of financial instruments by some listed banks, it is not comparable to the average situation of listed banks.) 2) As a whole, the Agricultural Commercial Bank of China, an inter-bank asset, has reduced its interbank lending and repurchase agreements, and the scale of interbank deposits has slightly increased. From the perspective of individual shares, Changshu Bank has reduced the three types of interbank assets to varying degrees, while Wujiang Bank has reduced the deposit and lending of interbank assets, and the redemptory assets for sale have slightly increased.

Structural decomposition: the month on month growth of loans and bond investment drives the proportion of interest bearing assets to rise further 。 1) The proportion of overall loans to interest bearing assets of Rural Commercial Bank rose 0.7 percentage points month on month to 53.8%, and the proportion of bond investment rose 0.3 percentage points to 32%. 2) Specifically, for individual stocks, Changshu Bank has the highest absolute value of loan proportion and the largest marginal improvement in the third quarter, with its proportion rising 2.2 percentage points to 56% month on month. The loan proportion of Wuxi and Zhangjiagang banks declined slightly, down 0.1 and 0.4 percentage points month on month to 51% and 53.7% respectively.

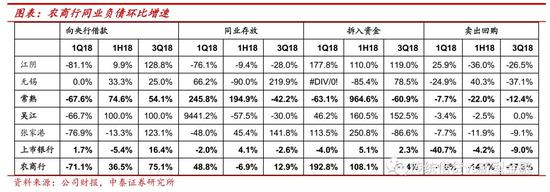

3、 The growth rate of the liability side matches the asset side, and the internal structure is optimized

3、 The growth rate of the liability side matches the asset side, and the internal structure is optimized The growth rate of the scale of the liability side matches that of the asset side, which is mainly supported by the deposit scale. At the same time, the scale of bond issuance has also increased significantly compared with that of the second quarter, while the scale of interbank liabilities has continued to decline. 1) Compared with the second quarter, the overall interest bearing debt scale of Rural Commercial Bank grew further, matching the asset side. 2) From the perspective of segmentation, the growth of interest bearing liabilities is mainly driven by deposits and bond issuance. The scale of interbank liabilities fell for three consecutive quarters. 3) In terms of specific stocks, Zhangjiagang Bank, Wujiang Bank and Wuxi Bank grew faster month on month in terms of deposit scale. In addition, the interbank debt scale of Wujiang Bank and Zhangjiagang Bank also grew to a certain extent.

Further split the growth rate of inter-bank liabilities. The decline in the scale of inter-bank liabilities of Rural Commercial Bank was mainly due to the large decline in the scale of borrowing funds and selling and repurchasing funds (of which the borrowing funds grew faster in the first two quarters on a month on month basis), and the borrowing from the Central Bank grew faster on a month on month basis, and the growth rate was far higher than the average level of listed banks. From the perspective of individual stocks, in the third quarter of Changshu Bank, in addition to borrowing from the Central Bank, other subdivisions have decreased to varying degrees.

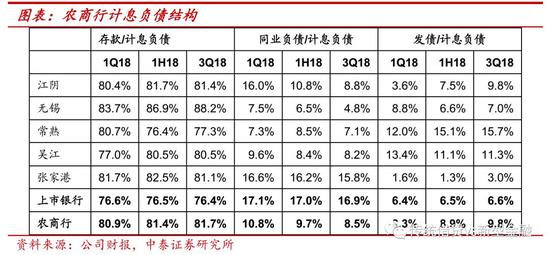

Debt structure splitting: the proportion of core debt increased. 1) Deposit: The proportion of overall deposits in interest bearing liabilities of Rural Commercial Bank increased by 0.3 percentage points month on month to 81.7%, while the proportion of overall deposits in interest bearing liabilities of listed banks decreased. In terms of specific stocks, Wuxi, Jiangyin and Zhangjiagang banks have higher absolute value of deposits, However, the proportion of deposits in Jiangyin and Zhangjiagang banks decreased slightly in the second quarter compared with the previous quarter, Changshu Bank (+0.9 percentage points month on month) has a large increase in month on month ratio 。 2) Active liabilities: The overall structure is adjusted from interbank debt to debt issuance. Changshu Bank and Wujiang Bank account for a relatively high proportion of debt issuance, while Zhangjiagang Bank accounts for a relatively high proportion of interbank debt.

4、 Marginal improvement of asset quality and overall capital adequacy

4、 Marginal improvement of asset quality and overall capital adequacy In the third quarter, the overall asset quality of Rural Commercial Bank continued to improve, and the future adverse pressure decreased. 1) Rejection rate: In the third quarter, the overall non-performing rate of Rural Commercial Bank was 1.5%, down 1 bp month on month. Among them, Wuxi Branch and Zhangjiagang Branch witnessed a large month on month decline in non-performing ratio, both of which decreased by 5 bp month on month. The non-performing ratio of Wujiang Bank rose to 1.55% from 9bp on a month on month basis. 2) Single quarter annualized net generation of non-performing loans : The overall month on month decline was 0.38 percentage points, and the marginal improvement was better than that of listed banks. Among them, the NPL net generation ratio of Jiangyin and Zhangjiagang banks decreased by 2.78 and 0.72 percentage points month on month compared with the second quarter. The net generation of non-performing loans of Wujiang Bank increased. 3) Adverse pressure in the future : The overall asset quality pressure of Rural Commercial Bank has declined, and the proportion of special interest loans has declined month on month. Among them, the absolute value of the proportion of special interest loans of Wuxi Bank is relatively low, while the proportion of special interest loans of Wujiang and Zhangjiagang is relatively high, but the overall trend is downward. Jiangyin Bank The proportion of special mention loans rose 0.87 percentage points month on month to 2.55%.

The overall provision of Rural Commercial Bank is relatively adequate, and the allocation coverage ratio and loan allocation ratio are higher than the average level of listed banks. 1) Coverage rate: The overall allocation coverage rate of Rural Commercial Bank increased, 60 percentage points higher than that of listed banks. With the exception of Wujiang Bank, the allocation coverage rate of other rural commercial banks has increased. Changshu Bank, with the highest coverage rate, increased 20 percentage points to 407% month on month in the third quarter. 2) Allocation ratio: The loan allocation ratio of Wujiang Bank and Zhangjiagang Bank decreased month on month, while that of Jiangyin Bank increased by 0.77 percentage points to 5.5% month on month, the highest absolute value.

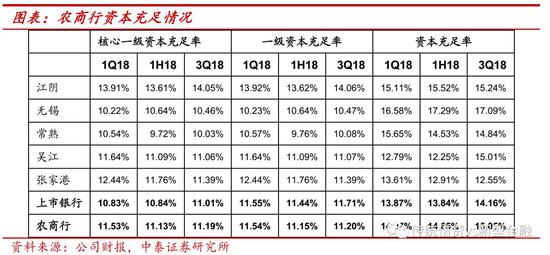

The overall capital of rural commercial banks is relatively sufficient. The core tier one capital adequacy ratio of Rural Commercial Bank increased by 6bp to 11.19% month on month. From the perspective of individual shares, only the core tier one capital adequacy ratio of Jiangyin Bank and Changshu Bank increased by 0.44 and 0.31 percentage points respectively month on month. However, in terms of absolute value, the core tier one capital adequacy ratio of Changshu Bank is still at the lowest level of Rural Commercial Bank.

The growth rate of risk weighted assets is less than that of loans. In the third quarter, the overall risk weighted assets of Rural Commercial Bank increased by 4.1% month on month, which was somewhat wider than that in the second quarter. The growth rate is slightly lower than the month on month growth rate of loans. Among them, the month on month growth of risk weighted assets of Changshu Bank slowed down, and the month on month growth of risk weighted assets of Wuxi Bank was higher than that of loans.

5、 Investment suggestion: attach importance to the allocation value and steady return of bank shares

In the third quarter, banking stocks showed obvious comparative advantages. Because the market's expectation of the economy is getting worse, it is difficult to explain its strength from the perspective of fundamentals. We believe that if there is a sustained inflow of medium and long-term funds and the economy remains weak, we should pay attention to the "allocation value" and "relative return" of bank shares in the general context.

Investment suggestion: the operation will be relatively simple in the near future. Next March is a vacuum period for bank fundamentals, during which investment is relatively clear. 1. For relative returns, If the market is weak, the bank shares will be strong; if the market is strong, the bank shares will be weak; 2. For absolute return investors, observe the flow of allocated funds (overseas funds, large institutional funds and national teams) for medium and long-term assessment; 3. Since we judge that the "policy bottom" is clear (see details in depth《 Heavy weight depth: how to transmit "policy bottom" to "market bottom" 》)The steady return of banks is predictable.

(The author of this article introduces: Chief of the banking industry of Zhongtai Securities, head of the financial team, and a special researcher of the National Finance and Development Laboratory.)