Article/Dai Zhifeng, columnist of Sina Financial Opinion Leader (WeChat official account kopleader)

The Bank's 17th annual report continued to improve, the profit growth rate (including pre provision profit) in the fourth quarter rose steadily, the net interest margin in the fourth quarter rose month on month (flat), and asset quality continued to improve. The differentiation among banks continues: excellent banks' reports continue to be beautiful, poor banks are still weak, and mediocre banks still cannot find a good point. The outstanding ones in the released statements are CMB, Ningbo, CCB, ABC and ICBC; What is weaker is people's livelihood and security.

preface

Annual report of 2017: overall improvement and differentiation. The Bank's 17th annual report continued to improve, the profit growth rate (including pre provision profit) in the fourth quarter rose steadily, the net interest margin in the fourth quarter rose month on month (flat), and asset quality continued to improve. The differentiation among banks continues: excellent banks' reports continue to be beautiful, poor banks are still weak, and mediocre banks still cannot find a good point. The outstanding ones in the released statements are CMB, Ningbo, CCB, ABC and ICBC; What is weaker is people's livelihood and security.

The future quarterly report will continue to improve, and the upward trend of high-quality banks will be determined, Looking ahead, the Bank's quarterly and semi annual reports in the first half of 2018 will continue to improve. The market's expectation of the economic trend has weakened, and the concern about the sustainability of the bank statements in the past 18 years has risen to a higher level; But we judge that the statements of excellent banks will continue to improve. Looking forward to 18 years, if the financial supervision is strict and the economy is flat (weak), the inter-bank differentiation is expected to continue. If one of the above two preconditions changes, the inter-bank differentiation will converge.

Analysis on the structure of bank assets and liabilities: individual loan development, interbank compression, and continuous deposit pressure. The asset side industry as a whole has made efforts to develop personal loans, of which credit cards and consumer business loans are the main growth parts. Inter bank assets have been compressed to varying degrees. With the breakdown of bond investment details, state-owned banks have increased trading and held to maturity investments; The joint-stock bank increased the investment in trading and available for sale financial assets, and the receivables decreased significantly. The liability side faces certain pressure: From the perspective of deposit structure, demand deposits of state-owned banks grew rapidly, while demand deposits of joint-stock banks grew weakly. From the perspective of customer structure, the proportion of state-owned bank enterprises' deposits increased and the growth rate was strong.

From a multi-dimensional perspective, the industry's asset quality shows obvious signs of stabilizing. Overdue and attention rates of all kinds of banks have decreased compared with the mid year link ratio, and the non-performing recognition is also more strict; Net generation of non-performing loans rose slightly in the fourth quarter. The stability of bank provisions increased, and the overall coverage rate of the industry increased.

The performance growth is steady and upward. In the fourth quarter, the revenue of state-owned banks grew rapidly year on year, while the growth of joint-stock banks slowed down; The growth rate of net profit in the fourth quarter was stable for state-owned banks, and the month on month increase for joint-stock banks. The net interest margin improved in the fourth quarter as a whole, the calculated value of joint-stock banks improved significantly, and the daily average net interest margin of big banks was expected to improve significantly; The service charge growth rate of joint-stock banks was significantly repaired. In 2017, the overall profitability of the industry declined slightly, and ROE and RWA were generally stable.

The overall asset quality of the industry is improving

Summary: From a multi-dimensional perspective, the industry's asset quality shows obvious signs of stabilizing: the overdue rate and attention rate of various banks have declined compared with the mid year link ratio, and the non-performing recognition is also more stringent; Net generation of non-performing loans rose slightly in the fourth quarter. The stability of bank provisions increased, and the overall coverage rate of the industry increased.

one

The defective rate has decreased month on month. According to the data published in the annual report, the non-performing ratio of listed banks in 2017 was 1.52%, down 3 bp month on month and 19 bp year on year; The average non-performing ratio of state-owned banks was 1.56%, down 3 bp month on month and 15 bp year on year, while that of joint-stock banks was 1.66%, down 1 bp month on month and 8 bp year on year.

NPL net generation increased month on month and improved year on year. The state-owned bank 1Q17-4Q17 measured the net generation of non-performing loans at 0.71%, 0.57%, 0.63% and 0.74% in a single quarter, and the cumulative annualized net generation of non-performing loans was 0.66%, up 4 bp month on month and down 22 bp year on year. The Bank's 1Q17-4Q17 single quarter estimated the net generation of non-performing loans was -0.31%, 1.48%, 1.25% and 1.32%, and the cumulative annualized net generation of non-performing loans was 1.38%, up 2 bp month on month and down 59 bp year on year.

The write off of non-performing loans in the fourth quarter of the industry increased, and the write off of state-owned banks and joint-stock banks decreased year on year. The non-performing write off rate of listed banks was 57.7%, up 3.87% month on month and 3.6% year on year; The non-performing write off rate of state-owned banks was 38.1%, up 3.7% month on month and down 2.45% year on year; The non-performing write off rate of joint-stock banks was 72%, up 3.57% month on month and down 22.48% year on year.

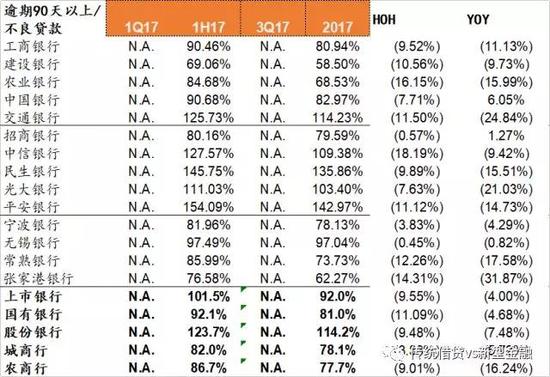

2 Other bad indicators: industry asset quality is stable and improving

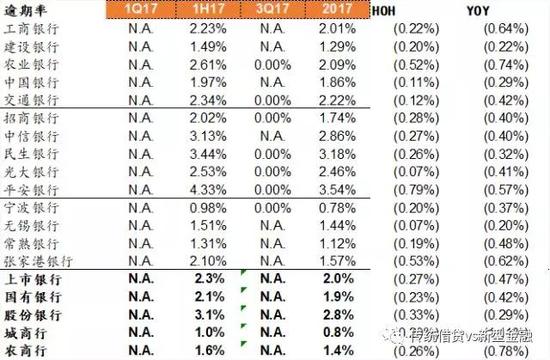

Proportion of concerned categories: The listed banks as a whole declined by 13 bp over the middle of the year, with a large decline in joint-stock banks. The proportion of special mention category in total loans decreased by 14bp over the middle of the year; State owned banks dropped by 38bp year-on-year and 3bp year-on-year, mainly driven by the increase of 5bp, 14bp and 4bp on a month on month basis of ICBC, BOC and BOCOM. At the individual stock level, the proportion of special interest loans declined rapidly in the middle of the year compared with that of Agricultural Bank of China (- 35bp), Everbright (- 35bp), Ping An (- 44bp), Changshu (- 48bp) and Zhangjiagang (- 46bp).

Overdue rate: The listed banks as a whole declined by 27 bp over the middle of the year, and the stock banks declined significantly. The overall overdue rate of the industry declined. The overdue rate of state-owned banks and joint-stock banks decreased by 23bp and 33bp over the middle of the year; The year-on-year decrease was 42bp, 29bp and 41bp. At the plate level, urban commercial banks( Bank of Ningbo )The overdue rate of agricultural commercial banks (Wuxi, Changshu, Zhangjiagang) is lower than that of other sectors; The overdue rate at the individual stock level dropped faster than that in the middle of the year, including Agricultural Bank of China (- 52bp), Ping An (- 79bp) and Zhangjiagang (- 53bp).

The identification of defects is also becoming stricter: The identification of non-performing loans by state-owned banks was stricter than that by joint-stock banks, and the proportion of loans overdue for more than 90 days in non-performing state-owned banks and joint-stock banks decreased by 11.09% and 9.48% compared with the middle of the year; The year-on-year decrease was 4.68% and 7.48%. From the perspective of individual stocks, the proportion of non-performing loans overdue for more than 90 days declined faster than that in the middle of the year, including Agricultural Bank of China (- 16.15%), CITIC (- 18.19%) and Zhangjiagang (- 14.31%).

3. Provision for improvement of bad coverage

Loan allocation ratio analysis: The allocation and loan ratio of state-owned banks and joint-stock banks increased on a month on month basis: state-owned banks increased by 5 bp on a month on month basis and 1 bp on a year on year basis; The shares rose 10 bp month on month and 2 bp year on year. Banks with high ratio of provision to loan include Agricultural Bank of China (3.77%), China Merchants Bank (4.22%), Bank of Ningbo (4.04%) Changshu Bank (3.72%); The banks with a larger month on month increase are CCB (+11bp), BOC (+14bp), CMB (32bp) and CITIC (+17bp).

Provision coverage analysis: The stock provision of state-owned banks and joint-stock banks increased their coverage of non-performing loans in the fourth quarter. The allocation and coverage rate of state-owned banks rose 7.11% month on month and 13.68% year on year; The shares increased by 7.78% and 10.78% month on month. Among state-owned banks, the provision coverage rate of Agricultural Bank of China was the most adequate (208.4%), and among joint-stock banks, the provision coverage rate of China Merchants Bank was the most adequate and increased rapidly year on year (262.1%,+27%). The provision coverage rate of Bank of Ningbo increased by 63.2% to 493.2% in the fourth quarter.

Performance growth and profitability

Summary: In the fourth quarter, the revenue of state-owned banks grew rapidly year on year, while the growth of joint-stock banks slowed down; The growth rate of net profit in the fourth quarter was stable for state-owned banks, and the month on month increase for joint-stock banks. The net interest margin improved in the fourth quarter as a whole, the calculated value of joint-stock banks improved significantly, and the daily average net interest margin of big banks was expected to improve significantly; The service charge growth rate of joint-stock banks was significantly repaired. In 2017, the overall profitability of the industry declined slightly, and ROE and RWA were generally stable.

1. Overall performance growth: the growth of net profit is steady and upward

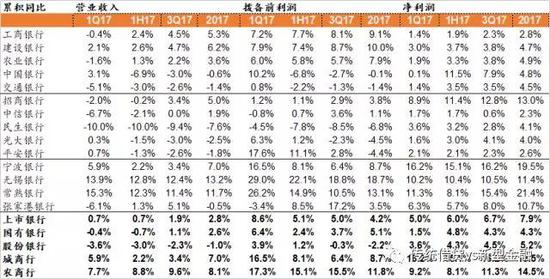

Analysis of performance growth in the fourth quarter: The revenue of state-owned banks grew rapidly year on year, and the growth of joint-stock banks slowed down; The growth rate of net profit of state-owned banks was stable, while that of joint-stock banks rose month on month. Revenue growth rate: Compared with 1-3Q17, state-owned banks and joint-stock banks increased by 1.5 and 1.3 percentage points to 2.6% and - 1% respectively. Among state-owned banks, China Construction Bank (+6.2%) and Industrial and Commercial Bank of China (+5.3%) had the fastest growth in revenue, while BOC and BOCOM had negative growth in revenue growth year-on-year (- 0.6%, - 1.4). The negative year-on-year growth rate of share trading revenue was mainly affected by Minsheng (- 7.6%). Net profit growth: the overall growth of the industry 。 Compared with 1-3Q17, state-owned banks and joint-stock banks increased by 0% and 0.7% respectively to 4.3% and 5.2%. On the whole, the net profit growth of urban commercial banks and rural commercial banks is higher than that of state-owned banks and joint-stock banks. From the perspective of individual shares, except for the low growth rate of ICBC's net profit (2.8%) among state-owned banks, the growth rate of CCB, ABC, BOC and BOCOM's net profit is relatively average (4.7%, 4.9%, 4.8% and 4.5%). Among joint-stock banks, CMB's net profit grew at the fastest rate of 13%.

2 Margin analysis

In the fourth quarter, the interest margin of state-owned banks was flat month on month, while that of stock banks rose month on month. The month on month growth rate of net interest income of listed banks, state-owned banks and joint-stock banks was 2.13%, 2.26% and 4.58% respectively; Interest bearing assets increased by 2.77%, 0.77% and 2.48%; The net interest margin measured by us in the fourth quarter increased by 0.01, 0.03 and 0.06 percentage points respectively compared with the third quarter. Among state-owned banks, BOC had a negative month on month increase in dividend margin, with a decrease of 2 bp; All the interest margin of the stock banks increased on a month on month basis, including Minsheng Bank and Everbright Bank The marginal improvement range is relatively large, with a link increase of 10bp.

The year-on-year growth of net interest income throughout the year was dragged down by interest margin. Net interest income of listed banks, state-owned banks and joint-stock banks increased by 3.05%/-6.99%/-3.37%. YoY change of interest margin is -0.15/-0.05/-0.24 percentage points; The scale of interest bearing assets increased by 7.16%/7.54%/2.18% year on year, and the price was supplemented by quantity. whole In terms of annual interest margin on a year-on-year basis, the dividend margin of state-owned banks was outstanding, The interest margin of ICBC, ABC and BOC increased by 4bp, 2bp and 1bp compared with last year.

Divide the interest margin: yield of interest bearing assets and interest payment rate of interest bearing liabilities

The average rate of return on interest bearing assets and the rate of interest payment on interest bearing liabilities of listed banks are both lower than last year, and the rate of return on interest bearing assets is lower than the rate of interest payment on interest bearing liabilities. The rate of return on interest bearing assets of state-owned banks declined year on year, while the rate of interest payment on interest bearing liabilities remained unchanged year on year. The rate of return on interest bearing assets of joint-stock banks increased year on year, but the increase was less than that of interest payment rate of interest bearing liabilities. The rate of return on interest bearing assets of listed banks, state-owned banks, joint-stock banks, urban commercial banks (Bank of Ningbo) and rural commercial banks rose by -0.34%/-0.05%/0.06%/-0.26%/-1.49% respectively; The interest payment rate of interest bearing liabilities rose by -0.03%/0.0%/0.32%/0.13%/-0.71%. At the individual stock level, ICBC has seen an upward trend in the rate of return on interest bearing assets of state-owned banks, with a year-on-year increase of 1bp. Among joint-stock banks, CMB, Everbright and Ping An have seen a larger upward trend, with 8bp, 6bp and 6bp respectively. The banks whose interest payment rate of interest bearing liabilities decreases significantly are agricultural bank , a year-on-year decrease of 8 bp.

3 Non interest income analysis

Analysis of non interest income and service charge income: the growth rate of net non interest income of state-owned banks declined due to service charges and other non interest income; Net non interest income and net commission income of joint-stock banks maintained high growth. In 2017, the net non interest income/net commission income of state-owned banks, joint-stock banks and urban commercial banks (Bank of Ningbo) increased by -9.65%/-2.78%, 4.49%/5.39% and 46.63%/6.42% year on year respectively. The growth rate of net commission income in the fourth quarter at the individual stock level was faster than that in the third quarter, including CCB (+2.05%), BOCOM (4.29%), CMB (+5%) and Ping An (+14.3%).

The non interest income contribution of joint-stock banks accounted for a large proportion, and the contribution of net non interest income of state-owned banks and joint-stock banks to total revenue weakened month on month. The proportion of net non interest income in the revenue of state-owned banks declined rapidly, down 1.38 percentage points month on month, and the proportion of net commission income in the revenue fell 0.7 percentage points to 19.5%. The proportion of net non interest income in the revenue of the joint-stock bank decreased by 0.45 percentage points month on month to 34.6%, and the proportion of net commission income in the revenue decreased by 0.43 percentage points to 31.1%.

From the perspective of service fee structure, state-owned banks and joint-stock banks have balanced development of various businesses; Rural Commercial Bank of China has a relatively simple collection business, only remittance settlement and agency business. In state-owned banks, remittance settlement (18.7%), agency service (14.1%) and wealth management (10.9%) accounted for a relatively high proportion of intermediate collection business; The joint stock banks accounted for a relatively high proportion of intermediate income business, including wealth management (15%), agency services (13.2%) and remittance settlement (6.5%).

4 Analysis of overall profitability

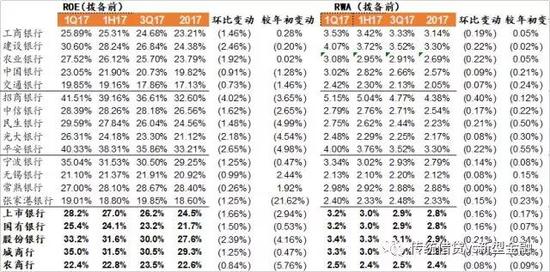

Profitability analysis of the whole year: the overall profitability of the industry declined slightly, and the ROE of state-owned banks declined slightly 。 1) The annual average ROE of listed banks was 12.3%, down 0.89% year on year. The ROE of joint-stock banks decreased by 0.83% to 12.1% year on year. The average year-on-year decline of state-owned banks was 0.55% to 12.7%. From the perspective of individual stocks, The ROE of state-owned banks BOCOM and ABC declined slightly, Decreased by 0.26% and 0.37% year on year respectively, CCB has a large year-on-year decrease (- 0.8%), but its overall ROE is still the highest among state-owned banks (13.90%) ; Among joint-stock banks, China Merchants Bank had the smallest year-on-year decrease in ROE (- 0.3%) and the highest ROE level (15.3%). 2) The year-on-year decline in RWA of state-owned banks exceeded that of joint-stock banks. The annual RWA of listed banks, state-owned banks and joint-stock banks decreased by 3bp, 8bp and 4bp respectively. In terms of individual shares, the state-owned banks CCB, BOC and BOCOM saw a large year-on-year decrease in RWA, with a decrease of 10bp, 11bp and 7bp respectively; Minsheng, Ping An and CITIC in the joint-stock bank decreased by 11bp, 9bp and 7bp year on year.

Analysis of profit level before provision: the decline of profit level before provision of state-owned banks is lower than the industry average, while that of joint-stock banks is higher than the average. The ROE of listed banks, state-owned banks and joint-stock banks before provision was 24.5%, 21.7% and 27.6% respectively, down 2.94, 0.53 and 4.16 percentage points year on year. The RWAs before provision were 2.8%, 2.8% and 2.9% respectively, down 0.17%, 0.07% and 0.34% year on year. From the perspective of individual shares, ICBC (+0.28%) and Agricultural Bank of China (0.02%) had a year-on-year increase in ROE before provision in state-owned banks, while those in joint-stock banks had a year-on-year decrease in ROE before provision, with CITIC (- 2.65%) and China Merchants (- 3.65%) having the smallest decline. From the perspective of RWA before provision, ICBC and ABC respectively increased by 5bp year on year, while China Merchants Bank had the smallest decline among joint-stock banks, - 0.12% year on year.

Asset liability structure analysis

Summary: Individual loan development, inter-bank compression and continuous deposit pressure. The asset side industry as a whole has made efforts to develop personal loans, of which credit cards and consumer business loans are the main growth parts. Inter bank assets have been compressed to varying degrees. The state-owned banks increased trading and held to maturity investment by splitting the details of bond investment,; The joint-stock bank increased the investment in trading and available for sale financial assets, and the receivables decreased significantly. negative The debt end faces certain pressure: From the perspective of deposit structure, demand deposits of state-owned banks grew rapidly, while demand deposits of joint-stock banks grew weakly. From the perspective of customer structure, the proportion of state-owned bank enterprises' deposits increased and the growth rate was strong.

1. Analysis of asset structure: individual loan development, interbank compression

The retail business of all banks has made great efforts, and the retail loan scale of joint-stock banks has the largest year-on-year growth. The loan scale of listed banks, state-owned banks and joint-stock banks increased by 11.6%, 9.4% and 12.6% year on year; Among them, corporate loans increased by 5.5%, 4.9% and 2.4%; Personal loans increased by 23.1%, 18.2% and 29.9% respectively. Among personal loans, credit cards and consumer business loans are the most powerful. (Housing mortgage increased by 20.5%, 18.8% and 31.2%; credit card increased by 37.5%, 25.9% and 42.3%; consumption and business loan increased by 19.1%, 15.8% and 18.6%). CITIC (29%), Ping An (57%) Zhangjiagang Branch (38%); Among them, CITIC is driven by credit cards and consumer business loans (40%, 37%); Ping An is driven by housing mortgage (79.4%).

The growth rate of bond investment was stable for state-owned banks and compressed for joint-stock banks; The scale of interbank assets was reduced as a whole. The scale of bond investment/inter-bank assets of listed banks, state-owned banks and joint-stock banks increased by 7.8%/- 16.7%, 9.3%/- 4.6% and - 2.3%/- 27.7% year on year. Split the details of bond investment, State owned banks increased trading and held to maturity investments , investment in receivables slightly compressed; The joint-stock bank has increased the investment in trading and available for sale financial assets, and there is a significant drop in receivables: The year-on-year growth rate of transactions, available for sale financial assets, held to maturity investment and receivables investment in state-owned banks is+26.5%,+2.9%,+13.4%, - 0.5%; Share banks+35.7%, 610.8% (mainly Ping An Bank A large year-on-year change), 16.5%, - 16.8%.

2 Debt structure analysis: deposit growth is stable

The deposit growth rate of state-owned banks is stable, while that of joint-stock banks is weak; The interbank debt shares declined, and the simultaneous issuance of bonds increased rapidly year-on-year 。 The average growth rate of deposits/interbank liabilities/bonds issued by state-owned banks was 6.3%, 6.9% and 34.1% respectively; Share behavior: 1.6%, - 1.7%, 17.2%. In terms of the growth rate of individual share deposits, ICBC (7.9%) and Agricultural Bank of China (7.7%) grew faster among state-owned banks; CITIC (- 6.4%) and Minsheng (- 3.8%) witnessed a decline in the scale of deposits in joint-stock banks. From the perspective of liability structure, the proportion of deposits in joint-stock banks in total interest bearing liabilities has slightly increased, while the proportion of deposits in state-owned banks, urban commercial banks (Bank of Ningbo) and agricultural commercial banks has slightly decreased.

Demand deposits grew rapidly and their proportion increased. The proportion of demand deposits of listed banks, state-owned banks and joint-stock banks increased by 1.0%, 0.9% and 0.6% respectively. Agricultural Bank of China (+2.2%), CITIC (+2.5%), Minsheng (+3.7%) Wuxi Bank (+3.2%)。 In terms of overall growth, demand deposits of state-owned banks grew rapidly, while those of joint-stock banks grew weakly. The growth rate of demand deposits of listed banks, state-owned banks and joint-stock banks was 8.4%, 8.1% and 2.7% respectively. From the perspective of customer structure, the proportion of state-owned bank enterprises' deposits increased and the growth rate was strong, +9.1% year on year, listed banks and joint-stock banks+9.4% and 3.1% year on year respectively.

Capital and shareholder changes

The core tier one capital of state-owned banks was improved. The core tier one capital adequacy ratio of listed banks, state-owned banks and joint-stock banks increased by - 2bp, 4bp and - 2bp respectively month on month, and the capital race increased by 50bp, 40bp and 22bp month on month. From the perspective of individual shares, the core tier one capital adequacy of China Construction Bank, a state-owned bank, increased the fastest, with a link ratio of+25bp, and Everbright, a joint-stock bank, increased by+87bp.

Seen from the change of shareholders, CSF increased its shareholding in stock banks by a large margin. In the fourth quarter, the listed banks with increased holdings of CSF included: Agricultural Bank of China (+3bp, 1.83%), Bank of China (+15bp, 2.74%), Bank of Communications (+63bp, 3.24%), China Merchants (+15bp, 3.41%), CITIC (+25bp, 2.11%), Everbright (+70bp, 3.2%), Ping An (+16bp, 2.85%). ICBC (- 10bp, holding 1.12%) and Minsheng (- 24bp, holding 4.75%) are the companies whose shares are reduced by CSF.

Special note: The information and opinions in this article are for reference only and do not constitute investment advice for any individual.

(The author of this article introduces: Chief of the banking industry of Zhongtai Securities, head of the financial team, and a special researcher of the National Finance and Development Laboratory.)