There is no doubt that industrial M&A is the most common denominator of the exit channel and regulatory support encouragement urgently needed by a large number of primary market investment targets with the current slow pace of IPO. At the same time, it is also the most expected tool for a large number of small and medium-sized listed companies that account for the main body of A-share capital market to "break the circle" in the era of registration 2.0.

From the perspective of listed companies, we define the marketization M&A related to the main business of listed companies (excluding related transactions such as asset injection of major shareholders and acquisition of equity of holding subsidiaries by listed companies) as industrial M&A. Judging from the market situation in the past two years, this type of transaction is not active. At a time when the pace of IPO is slowing down, industrial M&A should shoulder the dual expectations of market and regulation, and there are still some "blockages" to be solved.

Industrial M&A in the past few years

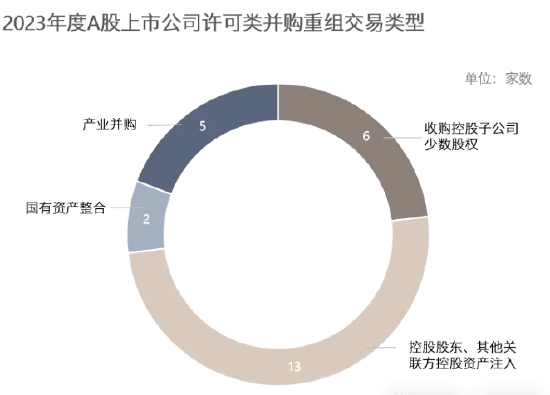

In 2023, among the 26 listed companies' share issuance and asset purchase transactions approved by the Reorganization Committee, there are as many as 13 asset injections belonging to controlling shareholders and other related parties; 6. Acquisition of minority shares of holding subsidiaries; 2. Integration of state-owned assets; The remaining five are industry mergers and acquisitions defined in this paper, accounting for less than 20%.

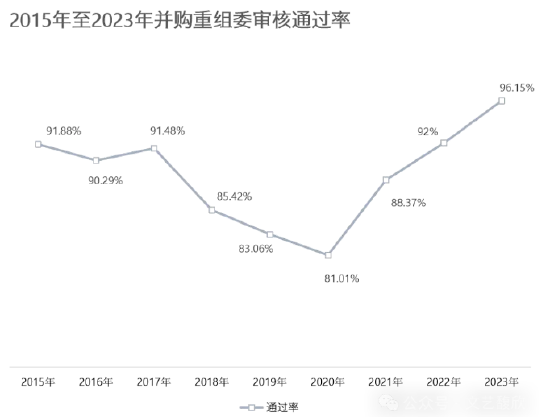

In general, in recent years, the trend of restructuring audit for stock issuance permits has become more and more strict. Although the pass rate of the audit will continue to rise after reaching the bottom in 2020, the pass rate of the audit in 2023 will be as high as 96.15% According to the analysis in the article "Review of the Restructuring Market of Listed Companies", the transactions that can go through a year long review cycle are really tempered into steel at the moment of the meeting, and a large number of transactions actually fall before the review of the meeting.

From 2022 to 2023, the statistical data of the time spent by all licensed restructuring projects in each stage are as follows:

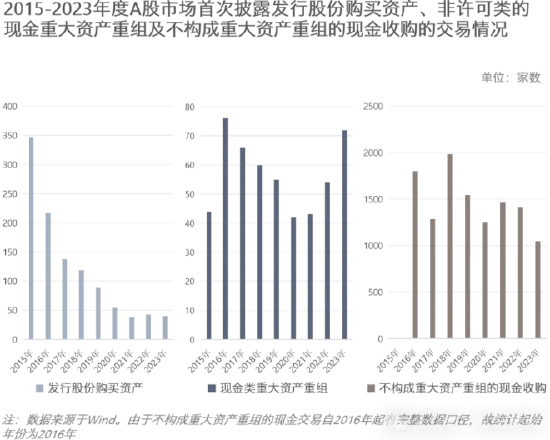

In fact, the low proportion of mergers and acquisitions in all industries in 2023 is just a microcosm. Let's look at the first disclosure of asset purchase transactions by issuing shares, non licensed major cash asset restructuring and cash acquisitions that do not constitute major asset restructuring in the past years after the peak of the last round of mergers and acquisitions in 2015:

It is obvious that non licensed cash transactions do not show a continuous downward trend of licensed transactions such as issuing shares to purchase assets, which may be more representative of the real market demand for M&A transactions.

In addition, the suppression of stock issuance transactions also indirectly stimulated the refinancing needs of listed companies after completing cash M&A. This situation has also been noticed by the regulator. One of the most important things that the "827 New Deal" had a profound impact on the M&A market last year was to strictly require refinancing and investment into the main business. This requirement will greatly inhibit the launching ability of cross-border cash mergers and acquisitions. Of course, under the current background of "strict refinancing review and check", cash is more precious with superimposed dividend requirements, and it is expected that cash M&A of industrial M&A types will also become more difficult.

Valuation difference between M&A and private financing

Since last year, there has been a widespread view in the market that the current valuation gap between M&A and private financing has inhibited M&A activities. That is, at present, the P/E ratio of the M&A market that can be generally accepted by the regulators is about 10-15 times, which is much lower than the current valuation level of private financing. The latter generally takes IPO as the valuation center, and from the perspective of P/E ratio, it is often more than ten times more than P/E ratio. In order to solve this problem, regulators have also proposed to "improve valuation inclusiveness" on many occasions.

The above view is fine from the perspective of price difference, but it seems to ignore the "buyer's willingness" in M&A transactions - even if the price earnings ratio is 10-15 times, will the buyer be willing to accept it? From the perspective of the principle of the income approach valuation model, under the assumption of normal discount rate and other parameters, the estimated future performance of the evaluated enterprise will maintain a growth rate of 20% - 30%, and it is difficult for the backward valuation result itself to exceed 15 times the P/E ratio. The so-called 10-15 times P/E ratio range is not "brain beating", but the result of the financial model under the selection of conventional parameters. Except for a few high-tech enterprises with high growth space, the 10-15 times P/E ratio is not an underestimate for most ordinary enterprises.

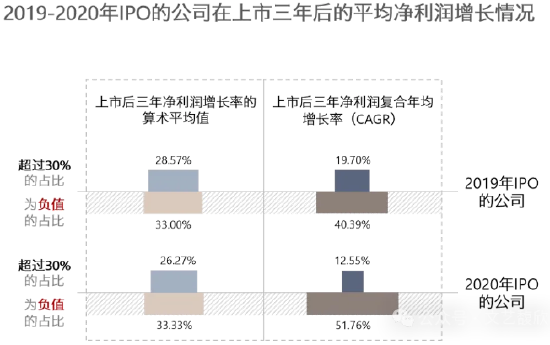

We select the listed companies that have fully announced their financial data for the three years after listing, that is, the IPO companies in 2019 and 2020. The proportion of the arithmetic average of the net profit growth rate in the three years after listing that exceeds 30% is 28.57% and 26.27% respectively, and the proportion of the net profit compound annual growth rate (CAGR) that exceeds 30% is 19.70% and 12.55% respectively; The proportion of negative arithmetic mean of net profit growth rate in the next three years is 33.00% and 33.33% respectively, and the proportion of negative CAGR of net profit is 40.39% and 51.76%. From the data point of view, even the successful IPO companies can achieve an average net profit growth rate of more than 30% in the three years after listing. So is the 10-15 times P/E ratio valuation range really the bottleneck?

In industrial M&A transactions, due to the industry relevance, the buyer probably has one or more capabilities of the M&A target in the procurement, market, R&D and technology and other resources required for operation. From the buyer's perspective, how many M&A targets are worth 10-15 times or even higher P/E ratios should be questioned. From our communication with many buyers of listed companies, we can see that a large number of buyers' views on the valuation of the subject matter of M&A are not "regulatory failure" but "expensive".

Therefore, the real problem of valuation difference is not the gap between "the valuation acceptable to the supervision" and "the marketization valuation of the seller", but the gap between "the valuation that the buyer is willing to accept" and "the private valuation of the seller". The expansion of the IPO market in the past few years has led to a high level of private equity valuation in the primary market. Among them, it may not be easy for the target company that wants to turn to the M&A market to be accepted by the buyers of industrial M&A before completing the painful "bubble extrusion" process.

On the other hand, it may just be that buyers of cross-border listed companies are more tolerant of target valuation. Originally, this type of transaction was expected to undertake a considerable number of M&A exits of primary market targets in the form of "bubble to bubble", and a number of high-quality listed companies could also be born in the turbulent market several years later. But perhaps the painful lessons from a large number of cross-border mergers and acquisitions in 2012-2015 are too profound, and this type of transaction is not currently encouraged by the regulatory authorities.

What is M&A risk

There is no doubt that the failure of M&A is certainly a risk to both buyers and sellers. But for the whole market, is the failure of M&A necessarily a risk? For M&A transactions, the transaction itself is the result of poor expectations between the buyer and the seller, and no one can predict the outcome of the transaction in advance.

It is said that "most mergers and acquisitions are failures". For most enterprises, mergers and acquisitions must be high-risk activities, but the birth of large enterprises also depends on mergers and acquisitions.

Taking the listed companies that have completed their IPO in 2019 and 2020 and have fully disclosed their financial data for the three years after listing as an example, one third to half of the listed companies with different caliber have negative average net profit growth in the three years after listing. If these companies are the subject of mergers and acquisitions, the approximate rate will be withdrawn for goodwill impairment. Similarly, in the area of mergers and acquisitions, if regulators need to cover for failed mergers and acquisitions or be responsible for the results of mergers and acquisitions with a certain failure rate in the whole market, only a few stable transactions can be completed in the end.

Only by allowing failures and mistakes can the strong be bred in the cruel competition and elimination, and no mistakes can be made. In the end, only the "little old tree" of moderation can be reverse screened. If M&A is to become an important exit channel in the primary market against the backdrop of the current slowdown in IPO, moderate risk tolerance may be necessary.

(The author of this article introduces: the founder of Wenyi Fuxin Capital Consultant, an early member of Huatai's joint M&A team, and the former joint head of Huatai Joint Investment Bank in East China.)