Article/Lin Caiyi, columnist of Sina Financial Opinion Leader (WeChat official account kopleader)

From the long-term trend, the RMB exchange rate will gradually move towards a clean floating exchange rate system. In this process, the regulator will stabilize foreign exchange market expectations by improving the RMB exchange rate marketization mechanism, and using interest rates, reserve ratio and various policy tools for counter cyclical intervention when necessary.

Core point:

-

In terms of the long-term trend of the RMB exchange rate, the dislocation of the economic cycle between China and the United States has led to the long-term depreciation of the exchange rate; The current account deficit and capital market inflows have increased the uncertainty of the balance of payments, making the total amount of foreign exchange reserves remain stable but the structure has changed, weakening the support for the exchange rate; The dislocation of the financial cycle between China and the United States will keep the RMB exchange rate under pressure.

-

From the perspective of short-term factors affecting the short-term fluctuation of the RMB exchange rate, the change of the US dollar index and the difference in the month on month growth rate of the Sino US equity markets have affected the short-term currency supply and demand and exchange rate fluctuations to a certain extent;

-

From the perspective of market expectations, the depreciation expectations of enterprises and individuals have formed but are narrowing; From the perspective of government intervention, the RMB exchange rate will gradually move towards a clean floating exchange rate system, and the intervention measures will mainly guide the RMB exchange rate expectations.

I Economic fundamentals affecting the exchange rate of RMB against the US dollar

1. Slow variables affecting the long-term trend of RMB exchange rate

1) The misplacement of economic cycle leads to the increase of long-term fluctuation space of exchange rate

In the context of structural deleveraging, China's macroeconomic growth rate has fallen into single digits since 2011 and dropped below 7% in 2015. It is a trend phenomenon that macroeconomic growth continues to slow down. Superimposed by the aging population and the impact of Sino US trade friction on foreign demand, China's economic growth rate will continue to face downward pressure in the next two years. At the same time, thanks to the tax reform and the long-term loose environment, the US economy performed relatively strongly. In September 2018, the US unemployment rate fell to 3.7%, a new low in 50 years. IMF predicts that the US economy will reach a peak of 2.9% in 2018, and the economic growth will slow to 2.5% in 2019. The economic cycle between China and the United States is misplaced, and the RMB exchange rate still has room for depreciation for a long time.

2) Increased uncertainty in balance of payments

Since the end of 2015, with the growing prosperity of the economy, the Federal Reserve has begun to gradually tighten liquidity, and both the dollar index and the 10-year treasury bond interest rate have risen. In the same period, China's balance of payments in capital and non reserve financial accounts have shown a large deficit. With the continuation of the interest rate increase cycle in the United States and the narrowing of the interest rate gap between China and the United States, the pressure of cross-border capital outflows is gradually increasing, which will exert certain pressure on the RMB exchange rate expectations.

In addition, Sino US trade frictions and tariff barriers have a certain impact on China's export trade, and led to the expansion of the current account deficit. In the first half of 2018, China's current account deficit was about $28 billion for the first time. In terms of breakdown, while the service deficit was expanding, the goods trade surplus was shrinking, leading to a deficit in the general ledger of the current account. The current account deficit and capital inflow in the capital market (stock and bond markets) have made the total amount of foreign exchange reserves stable, but the structure has changed to some extent. The hot money in the capital market has the characteristics of fast coming and going, and the fund stability is weak, which makes the uncertainty of the total amount of foreign exchange reserves increase and the role of supporting the RMB exchange rate weakened.

3) The central bank withdrew from the normalization intervention in the foreign exchange market

Since 2016, China's foreign exchange reserves have been stable at about $3 trillion. Since April 2018, the exchange rate of RMB against the US dollar has declined by more than 10%, but the average monthly change of foreign exchange reserves is only US $9.3 billion, far less than the average monthly change of the RMB exchange rate from 2015 to 2016 (US $37.7 billion). It can be seen that the People's Bank of China has withdrawn from the direct intervention in the normalization of the foreign exchange market and is more inclined to play the role of macro prudential management. From the perspective of foreign exchange reserve structure, since 2016, the currency mismatch measured by short-term foreign debt/foreign exchange reserves has slightly increased, mainly due to the increase in foreign debt of the banking sector.

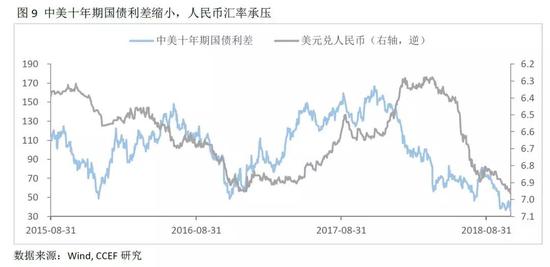

4) The dislocation of the financial cycle has narrowed the interest margin between China and the United States, resulting in pressure on the RMB exchange rate

From 2017 to 2018, the pace of interest rate hikes in the United States gradually accelerated, and the interest rate spread between the 10-year treasury bonds of China and the United States entered a downward channel. By the end of October, the interest rate spread between the 10-year treasury bonds of China and the United States had dropped to 36BP. The United States is still in the cycle of interest rate hikes, while China's monetary policy will remain neutral, and the dislocation of the financial cycle between China and the United States will continue to put pressure on the RMB exchange rate.

2. Fast variables affecting short-term fluctuations of RMB exchange rate

1) The trend of the dollar index and the fluctuation of the equity market

After the "811" foreign exchange reform in 2015, the formation mechanism of the central parity rate of the RMB exchange rate (that is, the closing price+the exchange rate of a basket of currencies+the counter cyclical factor) determines that the RMB exchange rate is affected by the supply and demand of the foreign exchange market and changes in the US dollar index in the short term. The cross-border capital flows caused by the difference in the month on month growth of China US equity markets have also affected short-term money supply and demand and exchange rate fluctuations to some extent. From January to September 2018, the month on month growth difference between the Chinese and American equity markets was basically negative, that is, the growth of China's equity markets was basically lower than that of the United States. In contrast, the exchange rate of the RMB against the US dollar also went down all the way. (Figure 11)

2) The Impact of the Change of Interest Margin between China and the United States on Financial Capital Flow and Exchange Rate

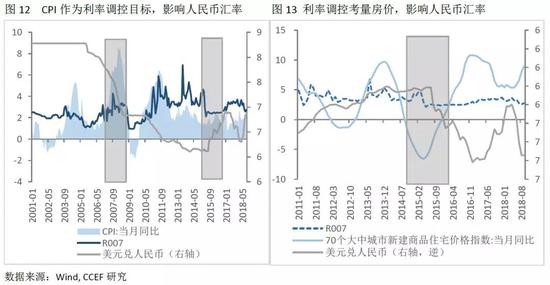

The change of the interest rate gap between China and the United States will directly affect the cross-border flow of financial capital and the RMB exchange rate. The central bank must consider economic growth, inflation and real estate regulation when adjusting interest rates. From the beginning of 2007 to the beginning of 2009, inflation exceeded 3% and house prices rose sharply. The central bank has raised interest rates for "inflation prevention and overheating prevention" for many times. After the financial crisis, the United States has been in quantitative easing for a long time and the RMB exchange rate has appreciated. Since 2013, the domestic CPI has been stable below 2% for a long time. The central bank has paid more attention to housing prices when regulating interest rates. From 2014 to 2015, the real estate market was stimulated. The central bank has cut reserve requirements and interest rates for five consecutive times, and the RMB has entered the devaluation channel.

2、 Other factors affecting the RMB exchange rate

1. Market expectation

1) Enterprise and individual expectations

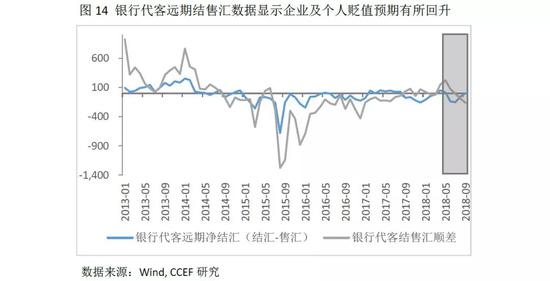

The contracted scale of forward foreign exchange settlement and sales in the current month reflects the exchange rate expectations of enterprises and individuals. Since May 2018, the surplus of foreign exchange settlement and sales by banks on behalf of customers has been declining. In July, it entered the deficit state and showed an expanding trend. It can be seen that the depreciation expectations of enterprises and individuals for the RMB exchange rate have been formed, but the degree is still far lower than that from 811 in 2015 to the beginning of 2016. According to the forward net foreign exchange settlement data, the depreciation expectation has narrowed since July 2018 (of course, it may also be related to the foreign exchange trading center's increase of forward foreign exchange sales margin).

2) Expectations of institutional investors

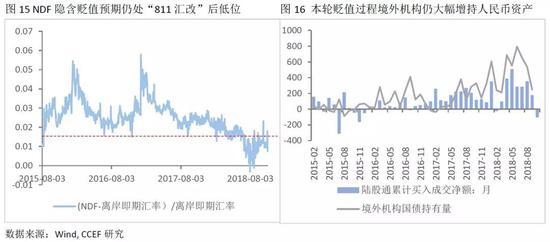

The transaction participants in the NDF (non principal delivery forward foreign exchange transaction) RMB offshore market are mostly institutional investors with high risk appetite. By the end of October, the implied depreciation expectation (NDF offshore spot exchange rate/offshore spot exchange rate) in the NDF was still in a low position. The average implied depreciation expectation in 2018 was 0.152, far lower than that from the "811 exchange rate reform" in 2015 to the beginning of 2016. With the inclusion of RMB bonds and stocks in relevant international indexes, from January to September 2018, foreign institutional investors continued to enter the A-share market and RMB bond market to increase their holdings of RMB assets. The continuous inflow of foreign capital has a certain supporting effect on the RMB exchange rate.

3) Market speculation

Speculative arbitrage between onshore and offshore markets. As the offshore market is more free than the onshore market, once the market has strong depreciation expectations, the market can carry out forward contract arbitrage through DF and NDF markets. Speculative transactions triggered by arbitrage opportunities between the onshore and offshore markets will also have a certain impact on the short-term fluctuations of market exchange rates.

2. Government intervention

At present, China's former economic growth is stable, structural deleveraging has achieved results, financial risks are generally controllable, and foreign exchange reserves are stable at around 3 trillion yuan, with certain intervention strength. However, to keep the RMB exchange rate above 7 for a long time, the intervention cost will continue to rise.

On the one hand, under the background of the strong performance of the US economy, the unabated pace of the Federal Reserve's interest rate increase and the rise of US protectionism, the uncertainty of the external environment has increased; On the other hand, as China's economic growth slows down, the investment drive weakens, the trade surplus shrinks, and the return on capital declines, both industrial capital and financial capital have the incentive to seek investment opportunities.

From the long-term trend, the RMB exchange rate will gradually move towards a clean floating exchange rate system. In this process, the regulator will stabilize foreign exchange market expectations by improving the RMB exchange rate marketization mechanism, and using interest rates, reserve ratio and various policy tools for counter cyclical intervention when necessary. Since April 2018, the central bank has raised foreign exchange risk reserves, restarted counter cyclical factors and window guidance and other measures to guide RMB exchange rate expectations.

(The author of this article introduces: Chief Economist of Hua'an Fund.)