Article/Ren Zeping, columnist of Sina Financial Opinion Leader Column (WeChat official account kopleader), congratulating Luo Zhiheng

The reform of property rights is a deeper level of opening and reform, and also an internal requirement for improving total factor productivity. At present, the reform has entered the deep water area, and further promoting property rights reform is the only way to promote China's high-quality development.

abstract

As a basic concept of institutional economics theory, property rights mainly include ownership, management rights, disposal rights, income rights, etc. Its essence is the check and balance of incentives and constraints, the equivalence of risks and benefits, and the unity of rights and obligations. Representative theories mainly include Coase theorem, principal-agent theory and contract theory. Institutional economics emphasizes that clear property rights and transaction costs are the cornerstone of effective resource allocation in the market. Protection of property rights, fair competition, income and risk symmetry, and reasonable and appropriate incentive mechanisms are the pillars to promote market efficiency.

The reform of state-owned enterprises in China can be divided into three stages: 1) from 1978 to 1992, "decentralization" and the contract responsibility system started the reform process; 2) From 1993 to 2002, we established a modern enterprise system and introduced a competitive elimination mechanism to improve market efficiency; 3) Since 2003, SASAC has been established to standardize management and deepen the reform of property rights system. In general, the essence of the past reform of state-owned enterprises was the organic combination of improving efficiency through internal property rights reform and introducing competition into the open market. At present, the state-owned economy has basically realized the transformation to a modern enterprise, the incentive mechanism has been gradually established, and the efficiency has been rapidly improved. In this process, the private economy has also achieved leapfrog development from scratch and from small to large, presenting the typical characteristics of "May, June, July, August, and September".

Although the efficiency of state-owned enterprises has been greatly improved, making great contributions to the country and society, the overall operating efficiency of state-owned enterprises is still lower than that of private and foreign-funded enterprises. With ROE and ROA as indicators of efficiency, except for a few industries, non-state-owned enterprises have efficiency advantages in competitive industries and even some monopoly industries. From a regional perspective, the proportion of state-owned asset industry in the province has a strong negative correlation with the proportion of GDP in each province and city in the country. On the whole, the higher the proportion of local state-owned industry, the lower the proportion of GDP in the country. Unclear property rights make it difficult for state-owned enterprises to become market economic entities that operate independently and assume sole responsibility for their own profits and losses. It is difficult to distinguish between government and enterprises, which is prone to soft budget constraints, financial resources advantages, administrative monopoly and other problems. Moreover, state-owned enterprises lack sufficient incentive and constraint mechanisms, which makes it difficult to adjust business strategies and resource allocation methods in a timely manner according to business conditions.

On the whole, China's manufacturing industry is basically open, mainly private enterprises, and the market competition is sufficient. However, state-owned enterprises in the upstream factor market account for a relatively high proportion, and there is still much room to improve market efficiency. At the same time, the service industry is still relatively open and competitive. At present, the proportion of Chinese state-owned and state holding capital investment in manufacturing industry basically remains around 10%, and is mainly concentrated in upstream factor industries, while the proportion of state-owned enterprises in some service industries is relatively high, accounting for more than 80%, and there are capital access restrictions, competitive barriers, low regulatory transparency and other problems. In terms of specific industries, fully competitive industries such as textile, catering, and express delivery are usually highly efficient, with improved total factor productivity and strong international competitiveness of products, while industries with administrative regulation and monopoly, such as steel, oil, natural gas, electricity, telecommunications services, finance, education, and medical services, have problems such as mismatch of social resources and low total factor productivity.

The reform of state-owned enterprises is mainly carried out in two directions: the reform of the property rights system and the reform of production efficiency by strengthening competition. The reform plan mainly includes radical "shock therapy", Thatcher's "no forbidden zone" reform, gradual incremental reform, classified system reform, mixed ownership reform, and strengthening, optimizing and making big countries have capital. In general, shock therapy and overly radical "no restricted area" reform and other programs will lead to results contrary to expectations, with a large negative impact. From China's practice, a series of reform explorations have gradually formed the reform methodology of "gradual+incremental+pilot" and the successful experience of adjusting measures to local conditions, implementing policies according to industry, introducing market competition mechanism, reforming single state-owned property rights, strengthening macro-control and relaxing micro intervention.

At present, the reform has entered the deep water area. Further promoting the reform of property rights is the only way to promote China's high-quality development. This requires us to focus on the basic economic system, take liberating and developing social productivity as the standard, take improving the efficiency of state-owned capital and enhancing the vitality of state-owned enterprises as the main line, clarify property rights, introduce competition, govern enterprises according to law, and implement policies based on industry, Replace invalid and inefficient property rights with effective property rights, and realize standardization of corporate governance of state-owned enterprises, marketization of company operation, and neutralization of enterprise competition.

We put forward the plan of "classification+mixed transformation+strengthening competition" for the reform of state-owned enterprises. Specifically, first, we should adhere to the basic economic system in terms of ideological cognition and stable expectations, treat state-owned and private economies equally, and implement the principle of competition neutrality. Secondly, in terms of methodology, the reform of state-owned enterprises adheres to the methodology of "gradual+incremental+pilot", establishes a reasonable assessment, reward and punishment mechanism, establishes a fault-tolerant and "exemption" mechanism, and improves local enthusiasm. The independent third party asset appraisal institution shall assess the reasonable value of state-owned assets or release the shackles of "state-owned assets loss" in the form of public bidding transfer. Third, we will continue to implement the reform of the classification system of state-owned enterprises, further clarify the division of public welfare, resource commerce and competitive commerce industries in line with local conditions, and fully open market access and eliminate the fittest in competitive commerce. Fourth, on the premise of clarifying the areas that state-owned enterprises should control or participate in, clarify property rights, promote the reform of mixed ownership, reform the operating system, and strengthen the complete performance appraisal standards. Fifthly, in the fields that state-owned enterprises must control or participate in, promote the internal competitive reform of state-owned enterprises, split public welfare and resource industries or establish new state-owned enterprises, introduce internal competition of state-owned capital, establish corresponding assessment mechanisms, entry and exit mechanisms, and formulate open, transparent and reasonable subsidy standards. Sixthly, in terms of the specific promotion of reform, we should avoid "one size fits all" and sports promotion, rely more on market-oriented means, improve the state-owned assets supervision system, and prevent the distortion of policy implementation.

Risk tip: policy promotion is less than expected, and the reform and opening up is too aggressive

catalog

1 Basic Theory of Property Rights

1.1 Property right theory

1.2 Basic definition of state-owned enterprises and relevant property rights

2. Main Course of SOE Reform

2.1 History of state-owned enterprise reform: clarify property rights, establish modern enterprise system, introduce competition and improve efficiency

2.2 Achievements of state-owned enterprise reform: diversified market economy entities jointly promote rapid economic development

2.3 Existing problems of state-owned enterprises: property rights are still unclear, and there is a gap between the overall efficiency and that of private enterprises

3 Market ownership structure and competition status

3.1 Overall: The manufacturing industry is dominated by private enterprises, the upstream factor market is dominated by state-owned enterprises, and the openness of the service industry is still relatively low

3.2 Manufacturing industry: private enterprises dominate, product competitiveness is strong, and a few industries are still protected

3.3 Factor market: state-owned capital monopoly, high protection barriers, resource mismatch

3.4 Service industry: the basic public service is mainly state-owned enterprises, and the overall restriction level is high

4. Comparison of state-owned enterprise reform plans

4.1 One step radical "shock therapy"

4.2 Privatization reform of Thatcher's "no restricted zone" in Britain

4.3 Gradual reform of stock adjustment and incremental reform

4.4 Reform of classified state-owned enterprises that implement policies based on industry

4.5 Mixed ownership reform

4.6 To be stronger and better, to be a big country with capital

5 Suggestions for SOE reform: classification+mixed transformation+strengthening competition

text

1 Basic Theory of Property Rights

1.1 Property right theory

As a basic concept of institutional economics theory, property right has a broader extension than ownership, mainly including ownership, management right, disposal right, income right, etc. Its essence is the check and balance of incentive and constraint, the equivalence of risk and income, and the unification of rights and obligations. Institutional economics developed gradually after Keynesianism lost its explanatory power to the economic phenomenon of "stagflation" in the 1970s. It believed that the arrangement of property rights would directly affect the efficiency of resource allocation. Therefore, "clarifying property rights" would stimulate the effective operation of the market. Its main contents include Coase theorem, principal-agent theory, contract theory, etc.

Coase Theorem points out that clarifying property rights is a necessary condition for realizing the optimal allocation of resources through market transactions. Transaction costs should include the costs of measuring, defining and safeguarding property rights. When property rights are clearly defined and effectively protected and transaction costs are zero, external factors will not cause improper allocation of resources, The market mechanism will automatically make the allocation of resources reach Pareto optimum.

The principal-agent theory points out that the separation of ownership and management rights of enterprises will form a principal-agent relationship, while the public ownership of property rights will lead to the absence of the actual owner, amplifying the deviation of the objective function of the enterprise owner and the operator, information asymmetry, and the unobservability and unverifiable degree of the operator's efforts, resulting in low efficiency of enterprises, Damage to the interests of owners.

The contract theory believes that enterprises are the collection of a series of contracts. Because of the limited rationality of people, the incompleteness of information and the uncertainty of transactions, the cost of clarifying all special rights is too high. Ultimately, it is normal for enterprises to act as incomplete contracts. The pursuit of unclear residual property rights will distort specific investment incentives, leading to the rise of rent seeking costs in the later relationship.

In general, institutional economics emphasizes that clarifying property rights and transaction costs is the cornerstone of effective resource allocation in the market, and protecting property rights, fair competition, income and risk symmetry, and reasonable and appropriate incentive mechanisms are the pillars of market economy to maintain efficiency.

1.2 Basic definition of state-owned enterprises and relevant property rights

The IMF defines state-owned enterprises as "public companies, i.e. commercial companies owned or controlled by the government", reflecting the ownership of state-owned enterprises, while the UN working documents define state-owned enterprises as "publicly owned or controlled companies providing public services", reflecting the public service functions of state-owned enterprises. At present, China has not clearly defined state-owned enterprises in law, but based on the description and determination of state-owned enterprises by the State owned Assets Supervision and Administration Commission, the Ministry of Finance and the National Development and Reform Commission, we believe that state-owned enterprises are government institutions, departments, institutions and other state capital contributions, and the owner's equity belongs to enterprises owned by the state, mainly including wholly state-owned enterprises, state-owned holding enterprises and state-owned joint-stock enterprises.

From the perspective of property rights, the current unclear property rights of state-owned enterprises in China make it difficult for them to become market economic entities that operate independently and assume sole responsibility for their own profits and losses. It is difficult to distinguish between government and enterprises, which is prone to problems such as soft budget constraints, financial resource advantages, administrative monopoly, etc., and the lack of adequate incentive and constraint mechanisms, which makes it difficult to adjust the business strategy and resource allocation mode in time according to the business situation. From the perspective of property rights structure, property rights include at least two kinds of rights: ownership and property rights. At present, the ownership of state-owned enterprises in China is relatively clear, and the ownership of state-owned enterprises belongs to the central government and local governments. However, the property rights represented by the right to operate, the right to use, the right to benefit and the right to dispose are relatively vague in the operation of state-owned enterprises, and there are problems such as the confusion between government and enterprises, implicit guarantees, advantages in financial resources, administrative monopoly, rent-seeking, which lead to low efficiency, resource mismatch, and damage to the overall social welfare, which is not conducive to further promoting reform. Taking the right of management as an example, the right of management of some state-owned enterprises is still under control, and it is difficult to have full autonomy in terms of personnel appointment and salary incentive. There are problems such as "easy to go up and hard to go down" of state-owned enterprise leaders, long-term lower than market level salaries of grass-roots employees, difficulties in effectively encouraging and protecting innovative achievements, and inflexible decision-making and management.

There is no difference between state-owned enterprises and private enterprises. They have their own advantages and disadvantages, so they should not fall into ideological debate. They should be measured by the pragmatism standard of black cats and white cats. They should regard state-owned enterprises and private enterprises as complementary, cooperative relations rather than "either or" alternative relations, and clarify property rights, improve governance, and compete fairly on the basis of strengthening the development of public ownership, Carry out innovative cooperation and development.

2. Main Course of SOE Reform

Reviewing the reform process of state-owned enterprises, its essence is the organic combination of improving the efficiency of internal property rights reform and introducing competition into the open market. The efficiency of state-owned enterprises has been greatly improved in the past 40 years, and has made great contributions to the basic public sphere and national security strategy. However, it is worth noting that there are still many problems existing in state-owned enterprises, such as unclear property rights, high principal-agent costs, unclear ultimate owners, imperfect incentive mechanisms, some local governments and enterprises are indistinguishable, and soft budget constraints, which have led to the inefficiency of some state-owned enterprises compared with private enterprises.

2.1 History of state-owned enterprise reform: clarify property rights, establish modern enterprise system, introduce competition and improve efficiency

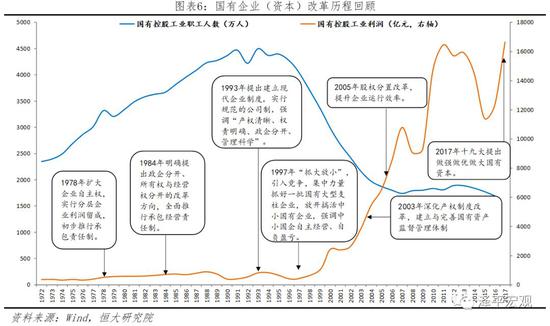

The reform process of state-owned enterprises can be divided into three stages: the first stage is the reform process of "decentralization" and contract responsibility system from 1978 to 1992. In 1978, the Third Plenary Session of the 11th Central Committee of the Communist Party of China set the tone of reform and opening up. Since Sichuan began to "expand the autonomy of enterprises" in urban areas, the success of the agricultural household contract system in Fengyang, Anhui, has led to the rapid expansion of the contract responsibility system based on the separation of ownership and management rights from agriculture to industry. At the end of 1980, the number of pilot enterprises nationwide expanded to more than 6000, accounting for 15% of the industrial enterprises within the national budget, 60% of the output value and 70% of the profits.

The second stage is to establish a modern enterprise system from 1993 to 2003, and introduce a competitive elimination mechanism to improve market efficiency. In 1993, the central government established a modern enterprise system to reform state-owned enterprises, emphasizing "clear property rights, clear rights and responsibilities, separation of government and enterprises, and scientific management". Then, through "focusing on the large and releasing the small", it concentrated its efforts on a number of large state-owned pillar enterprises, liberalized and invigorated small and medium-sized state-owned enterprises, allowed the latter to sell, reorganize, lease, and go bankrupt, and gave full play to the power of the market to allocate resources. From 1997 to 2003, the number of state-owned and state-controlled enterprises decreased by 37% from 238000 to 150000, while the employment of state-owned enterprises decreased from 110 million to 69 million, the employment of private enterprises increased from 7.5 million to 25.45 million, and the total industrial output increased from 11.4 trillion to 14.2 trillion in the same period.

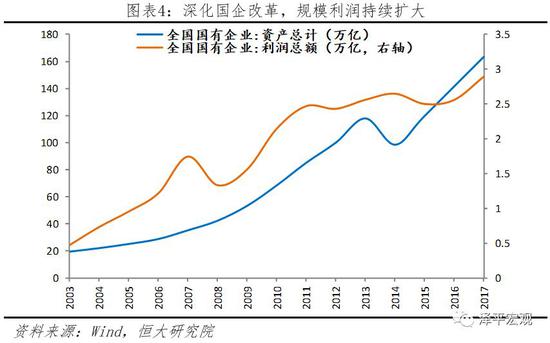

The third stage is the establishment of SASAC since 2003 to standardize management and deepen the reform of property rights system. In 2003, the State owned Assets Supervision and Administration Commission (SASAC) was formally established, which proposed the core content of modern property rights, namely, "clear ownership, clear rights and responsibilities, strict protection, and smooth circulation". The transfer of state-owned property rights was gradually standardized, and the hierarchical supervision system was gradually formed. With the efforts of reform and innovation, the labor productivity and profitability of state-owned enterprises have improved. Since 2003, the total assets of state-owned enterprises have increased from 20.0 trillion yuan to 173.9 trillion yuan in August 2018, and the total profits have increased from 476.9 billion yuan to 2.89 trillion yuan in 2017.

With the gradual deepening of reform, the current state-owned enterprises in China have basically transformed into modern enterprises. Incentives have been gradually set up, operating efficiency has been improved, and they have become the pillar to promote China's economic development, improve social welfare, and expand international influence.

2.2 Achievements of state-owned enterprise reform: diversified market economy entities jointly promote rapid economic development

After 40 years of reform, China is currently implementing an economic system with public ownership as the main body and diversified ownership economies developing together. The reform of domestic property rights of state-owned enterprises, the expansion of opening up to the outside world, the introduction of market competition and other measures have diversified the main body of the market economy and promoted China's economic take-off. At the same time, China's private economy has developed by leaps and bounds from scratch, from small to large, and its proportion in the whole social economy has risen rapidly, which has become an important foundation to support China's rapid economic development.

At present, the private economy presents the typical characteristics of "May 6789". The first meeting of the Leading Group for Promoting the Development of Small and Medium sized Enterprises of the State Council pointed out that at present, the private economy pays more than 50% of taxes, creates more than 60% of GDP, contributes more than 70% of technological innovation and new product development, provides more than 80% of jobs, and owns more than 90% of enterprises.

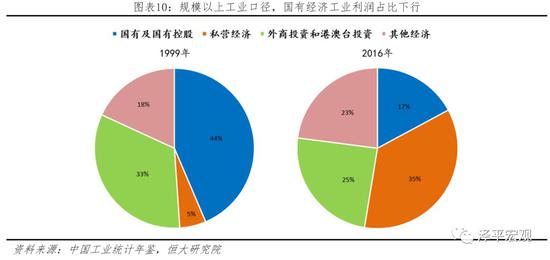

More specific calculations show that private economy has made great contributions to fixed asset investment, industrial output and employment. First, the proportion of private economy in fixed asset investment rose from 30% in 2004 to 62.4% in September 2018. Second, in terms of industrial output, the proportion of industrial output value of state-owned and state-owned holding units declined from 77.6% in 1978 to 19.8% in 2016, and the proportion of non-state-owned enterprises rose to 80.2%, of which private enterprises and foreign enterprises accounted for 35.9% and 21.6% respectively. Third, in terms of employment, the proportion of state-owned enterprises in the employment of cities and towns in the whole society dropped from 78.3% in 1978 to 14.9% in 2016, while the employment of non-public enterprises reached 84%. In 2016, the number of private enterprises and individuals added jobs reached 17.3 million, while the number of state-owned enterprises added jobs decreased by 380000 in the same period; For industries above designated size, the employment share of state-owned and state-controlled enterprises decreased from 58% in 1999 to 18% in 2016.

Note: Due to the availability of statistical data, except for the state-owned and state-owned holding companies and private economies, the data of state-owned enterprises and private enterprises do not include state-owned or private holding companies such as limited liability companies, joint-stock companies and self-employed enterprises, and the data underestimate the actual state-owned capital and private capital.

2.3 Existing problems of state-owned enterprises: property rights are still unclear, and there is a gap between the overall efficiency and that of private enterprises

Although the reform of state-owned enterprises has made remarkable achievements in the past, some state-owned enterprises in China still have administrative monopoly, financial financing advantages, soft budget constraints and other problems due to unclear property rights. Backward production capacity cannot be eliminated and efficiency is relatively low.

2.3.1 In the past, state-owned enterprises introduced competition and a large number of inefficient property rights were eliminated

At the end of the 1990s, China gradually opened up the textile, catering, manufacturing and other industries. The participation of private enterprises has greatly improved the degree of market competition. At the same time, the state-owned enterprises are allowed to "focus on the big and let go of the small", and the poorly managed state-owned enterprises are allowed to be eliminated. The market gradually gives play to the power of allocating resources.

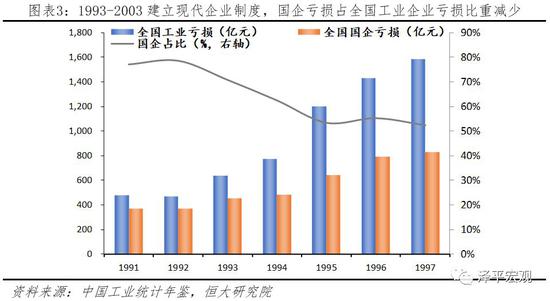

The problems of early state-owned enterprises are mainly reflected in serious losses, low returns and huge subsidies. According to the data from the China Industrial Statistics Yearbook, the losses of state-owned industrial enterprises from 1994 to 1995 reached 48.26 billion yuan and 63.96 billion yuan, respectively, accounting for 62.5% and 53.4% of the total losses of industrial enterprises. At the same time, compared with non-state-owned enterprises, the return rate of state-owned enterprises is generally low: from 1996 to 1997, the return rate of net assets of state-owned industrial enterprises was 2.2% and 2.1% respectively, while the return rate of net assets of private enterprises was 24.1% and 14% in the same period. In addition, most state-owned enterprises also enjoy financial subsidies, as well as "hidden subsidies" such as land rent and loan interest rate, which are much lower than those of non-state-owned enterprises.

After opening up some industry markets, the loss side of inefficient property rights in competitive industries is difficult to be effectively improved, and some inefficient state-owned enterprises either actively or passively exit the market. With the gradual opening up and introduction of competition in some highly competitive manufacturing industries such as the textile industry and some catering service industries, some state-owned enterprises with low production capacity and low efficiency are difficult to adapt to the market situation and suffer losses: from 1996 to 2003, the loss areas of state-owned holding industrial enterprises above the designated size were 33.5% and 35.2% respectively, with the loss area slightly expanding by 1.7%, In the same period, the loss of private enterprises decreased by 4.5 percentage points from 19.6% to 15.1%. In addition, from 1996 to 2003, the industries in which SOEs' loss areas significantly improved were mainly concentrated in the upstream resource-based industries, such as nonferrous metal mining, ferrous metal smelting, oil and gas mining, with the improvement rate exceeding or approaching 10%, while the downstream manufacturing industries with strong competitiveness, such as rubber, plastic, metal products, chemical fibers, and metal products, were difficult for SOEs to adapt to the competition, The number of losses increased rather than decreased, in contrast with private enterprises.

2.3.2 At present, the efficiency of state-owned enterprises has been greatly improved compared with the past, but there is still a gap between state-owned enterprises and private economy in general

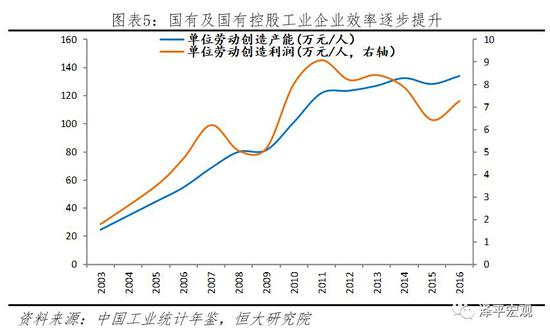

At present, the efficiency of state-owned enterprises has been greatly improved compared with the past. From the perspective of unit labor capacity and unit labor profit, from 2003 to 2016, the unit labor capacity and profit of state-owned industrial holding enterprises increased by 440%, 309% to 1341000 yuan and 73000 yuan per person respectively, with an average annual growth of 12% and 9%.

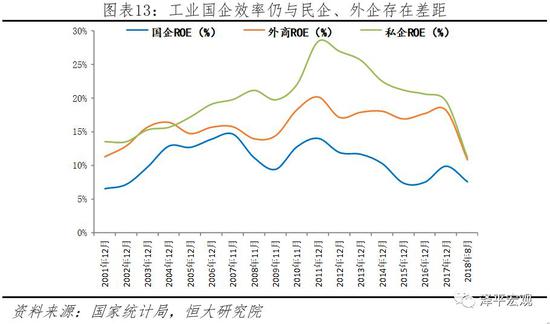

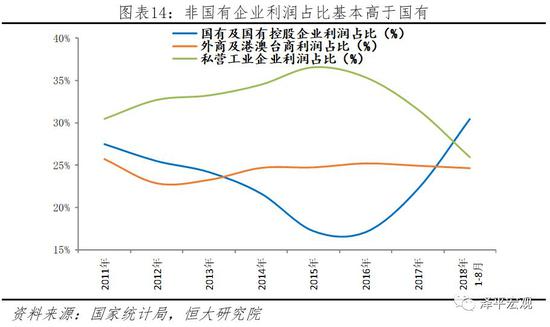

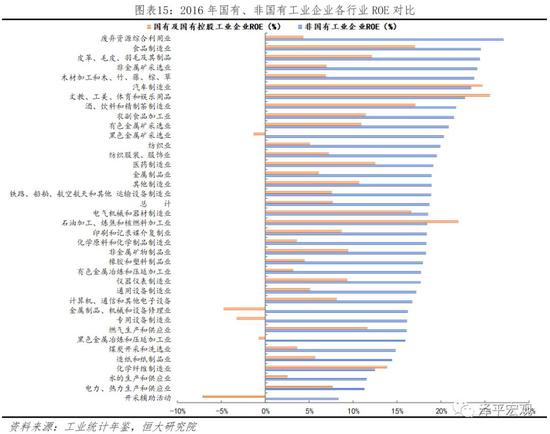

But overall, the efficiency of state-owned enterprises is still lower than that of private and foreign-funded enterprises. Excluding public and national security industries, the overall efficiency of state-owned enterprises in competitive industrial industries from 2003 to 2016 was still significantly lower than that of non-state-owned enterprises, and the overall efficiency was still low. From the perspective of return on equity (ROE) and return on assets (ROA) as the representative indicators of efficiency measurement, in 2016, the efficiency of non-state-owned enterprises was better than that of state-owned enterprises. The ROE and ROA of state-owned industrial enterprises were 7.7% and 3.0% respectively, while the ROE and ROA of non-state-owned enterprises were 18.7% and 8.9% respectively in the same period.

In terms of industries, except for a few industries, non-state-owned enterprises have efficiency advantages in competitive industries and even some monopoly industries. It is worth noting that since the supply side reform in 2015, the efficiency advantage of non-state-owned enterprises over state-owned enterprises has been significantly reduced, which is mainly reflected in the sharp and rapid decline in the profit rate of non-state-owned enterprises, and the sharp rise in the profits of state-owned enterprises, which has triggered the concern of the society about "national promotion and private withdrawal". From the data, the industries with sharply increased profits are mainly concentrated in the upstream industries with strong monopoly, because the "one size fits all" policies such as capacity reduction and environmental protection have caused great harm to private enterprises, and even some enterprises have withdrawn from the market, which does not indicate the relative improvement of the efficiency of state-owned enterprises.

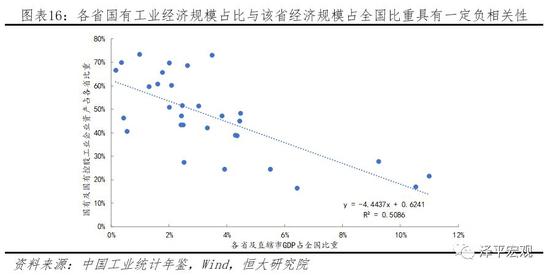

From a regional perspective, the proportion of state-owned economy and industry in each province has a strong negative correlation with the proportion of GDP in each province in the country. The higher the proportion of state-owned industry, the lower the proportion of GDP in the province in the national GDP, reflecting the relatively weak economic vitality of regions with a high proportion of industrial state-owned enterprises. Through the calculation of the proportion of state-owned holding enterprises above designated size in the assets of all industrial enterprises in 31 provinces, cities and autonomous regions and the GDP, the proportion of assets of state-owned holding enterprises in provinces with relatively low proportion of state-owned economy, such as Jiangsu, Guangdong, Zhejiang and other regions, has basically maintained at 10% - 20%, but the proportion of GDP has exceeded the national average, including the GDP of Jiangsu and Guangdong They accounted for 10.5% and 11% respectively. However, in provinces with slow industrial upgrading and state-owned industrial economy accounting for more than 50% of industrial assets, such as Liaoning, Jilin, Heilongjiang, Guizhou, Shanxi, Qinghai, Gansu and other places, economic growth is significantly lower than the national average.

3 Market ownership structure and competition status

At present, China's reform has entered into a deepwater area. The problems of inefficient property rights and low total factor productivity caused by the ambiguous definition of powers and responsibilities, soft budget constraints, administrative monopoly and other issues have become obstacles that constrain China's transition from high-speed growth to high-quality development. The successful experience of China in the past 40 years is the reform and opening up, the introduction of competition, and the need for a new round of reform and opening up with greater strength to "seek happiness for the people and rejuvenation for the nation" in the future. Therefore, it is necessary to comprehensively sort out the property right structure and competition status of various industries in China.

3.1 Overall: The manufacturing industry is dominated by private enterprises, the upstream factor market is dominated by state-owned enterprises, and the openness of the service industry is still relatively low

At present, China's manufacturing industry is basically open and the market competition is full. China's competitive manufacturing industry is basically open to private enterprises and foreign capital, and only some restrictions are reserved in automobile and other industries. This year, the restrictions on the proportion of foreign shares in the automobile manufacturing industry were again significantly lifted. The proportion of state-owned and state-controlled capital in fixed asset investment in manufacturing industry is basically maintained at about 10%. The total factor productivity of the fully competitive market has been improved, and the international competitiveness of products is strong. China has gradually become a major exporter of industrial manufactures.

The upstream factor market is dominated by state-owned enterprises, and there is still room for improving market efficiency. At present, a few state-owned enterprises still occupy a monopoly position in the oil, natural gas, electricity and other energy factor markets. At the same time, after the overcapacity reduction and environmental protection storm, the industry concentration has further improved significantly. Upstream price rises, excessive profits and liquidity ebb in the second half of the financial cycle. Some private enterprises have difficulty in financing and take the initiative to merge into large enterprises to seek help. The survival difficulties of small and micro enterprises, the mismatch of social resources and low total factor productivity need to be highly valued.

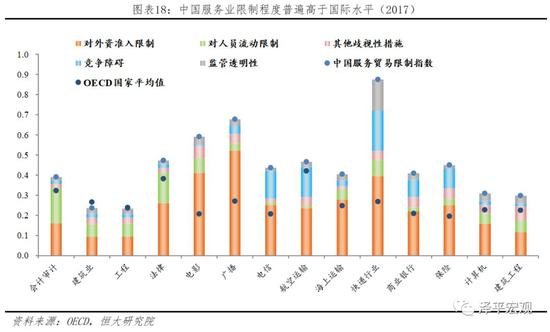

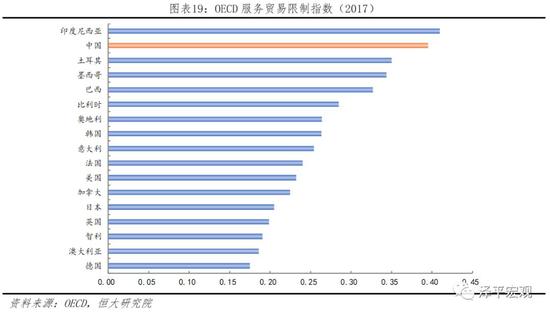

The openness of the service industry is still relatively low. At present, in some service industries in China, state-owned enterprises account for a high proportion, and state-owned capital accounts for more than 80% of fixed asset investment in telecommunications services, transportation and other service industries. Some service industries are less open to the outside world due to capital access restrictions, competition barriers, regulatory transparency and other factors. According to the service trade restriction index issued by the Organization for Economic Cooperation and Development (OECD), OECD countries generally open up competition in the construction industry, engineering, broadcasting, telecommunications, commercial banks, and insurance, while China's postal, financial and insurance, telecommunications services, construction, broadcasting, and film industries are significantly higher than the average level of OECD member countries, resulting in a series of problems such as low efficiency, low service level, weak international competitiveness, and low service exports.

On the whole, currently, fully competitive industries in China are generally more efficient, with higher total factor productivity and stronger international competitiveness of products, while industries with administrative regulation and monopoly have problems such as mismatch of social resources and low total factor productivity.

3.2 Manufacturing industry: private enterprises dominate, product competitiveness is strong, and a few industries are still protected

From the perspective of the degree of opening up and internal competition, the overall level of competition in the current manufacturing industry is relatively high. Private capital investment dominates, accounting for more than 90%. There are relatively few industries where foreign investment is restricted or state-owned enterprises dominate. Specifically, according to the property right structure and competition intensity, manufacturing industry can be divided into two categories: first, private enterprises dominate, state-owned enterprises basically withdraw from the competition, with sufficient market competition and strong product competitiveness, such as textile, chemical manufacturing and other industries; Second, state-owned enterprises dominate or monopolize, and the property rights are mainly state-owned holding or sole proprietorship, and there are still restrictions on foreign investment or private enterprises, such as automobiles and steel.

3.2.1 Category I: full market competition, dominated by private enterprises, and strong product competitiveness

Textile industry: led by private enterprises, less administrative control, strong international competitiveness of products

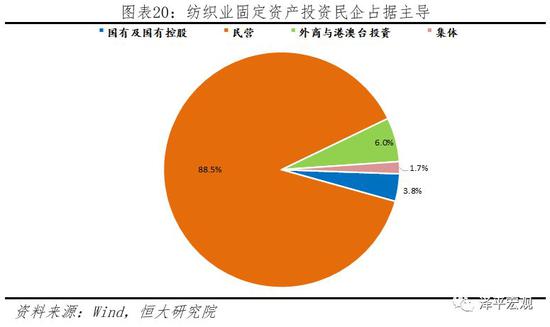

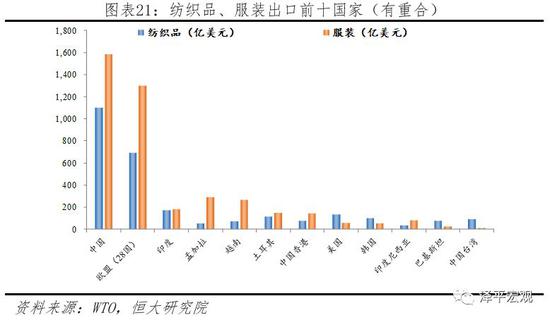

The textile industry, as one of the industries that opened up significantly in the 1990s, private enterprises have gradually become the leading force in the textile industry, and their products have strong international competitiveness. At present, the state has less administrative control and intervention in the textile industry, the textile industry has a high degree of marketization, and the products have strong international competitiveness. By the end of 2016, the number of non-state-owned enterprises in the textile industry and their total assets were 19566 and 2325.8 billion yuan respectively, accounting for 99% and 94.5% of the industry. The fixed investment of the private economy in the textile industry accounts for 88.5%. The full competition in the textile industry makes China's textile industry more competitive internationally. The export of textiles and clothing ranks first in the world.

3.2.2 Category II: state-owned enterprises monopolize or dominate, while private enterprises are numerous but not strong

Iron and steel: state-owned enterprises are dominant, private enterprises are numerous but not strong

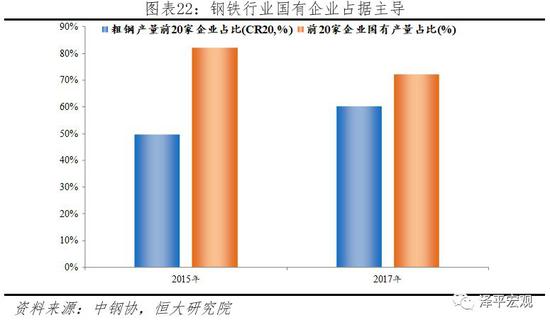

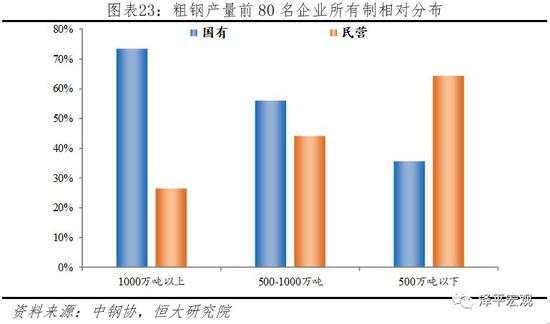

In the past, the output of private enterprises in China's steel industry increased rapidly, mainly producing crude steel, while state-owned enterprises basically occupied the leading position in high-end steel research and development and market. In recent years, the concentration of the steel industry has increased. Since 2015, in the environment of capacity reduction, the steel industry has experienced intense competition, and a large number of zombie enterprises, small and medium-sized private enterprises have been closed down. Central enterprises and local state-owned enterprises have dominated the industry by virtue of their scale and technology advantages, and the industry concentration has increased. In 2017, the output of the top 20 crude steel enterprises in China accounted for 60.3% of the total crude steel output in that year, 10.2 percentage points higher than 49.8% in 2015, including 13 state-owned enterprises. There are 22 steel enterprises with an annual output of more than 10 million tons, among which 15 are Chinese enterprises, accounting for 73.5% of the total output.

Automobile industry: state-owned holding enterprises dominate, and the competitiveness of state-owned brands is relatively weak

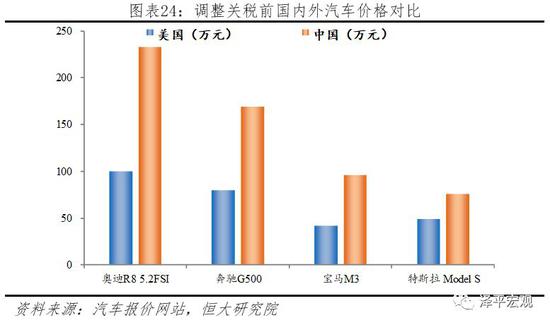

In the past, the automobile industry was heavily affected by administrative intervention, which was reflected in the high level of administrative control over foreign investment access, product catalogue, import and export, consumption policies and other aspects, as well as the existence of many taxes, high tax rates and high administrative costs. In the past, China stipulated that foreign capital should not hold more than 50% of the total vehicle and special purpose vehicle manufacturing shares, and imposed access restrictions on foreign investors entering the automotive industry. At the same time, before the reform, the purchase of imported complete vehicles was subject to 25% tariff (some 20%) (reduced to 15% from July 1, 2018), 16% value-added tax, 1% - 40% consumption tax based on vehicle displacement, and 2% - 13% "double anti-dumping" (anti-dumping, countervailing) for some models. The high tariff plus the premium in the intermediate link has led to the price of domestic imported vehicles, especially luxury cars, being significantly higher than the overseas price, which has damaged the rights and interests of consumers. At the same time, taking Audi A8 as an example, before the reform in 2018, the price of the car was about 500000 to 630000 in the United States and 88-2570000 in China, with a price increase of 76% - 308%.

At present, China's automobile industry is still dominated by Sino foreign joint ventures and state-owned holding enterprises. The long-term protection of the automobile industry leads to low market competitiveness, poor enterprise efficiency and innovation ability, relatively weak competitiveness of state-owned brands, and relatively low market share. The long-term policy protection has not improved the competitiveness of domestic brands and economic benefits. The excessive dependence of state-owned holding enterprises on foreign technology has led to the structural development imbalance of state-owned enterprises, insufficient innovation capacity and weak product competitiveness. In August 2018, foreign brands accounted for 62.8% of the Chinese market, and the market share of independent brands, high-end models, and new energy vehicles still have much room for improvement.

3.3 Factor market: state-owned capital monopoly, high protection barriers, resource mismatch

Different from the natural monopoly formed after full competition in foreign countries, the current monopoly position of state-owned capital in the energy factor market in China is mainly caused by early administrative policies. Administrative barriers make it difficult for private capital to enter, and some state-owned enterprises have low operating efficiency, serious resource mismatch, low total factor productivity, and inflated regulatory prices.

Oil and natural gas: state-owned enterprises monopolize and set the proportion of foreign equity

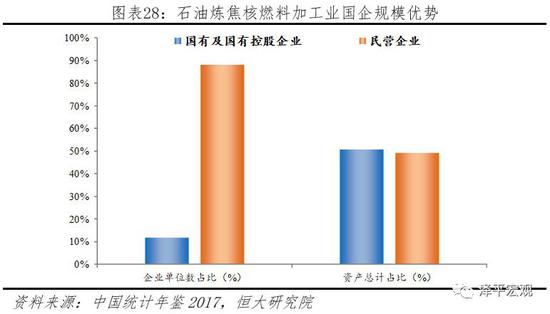

At present, state-owned enterprises in the oil and gas industry occupy a monopoly position. At present, China stipulates that the exploration and development of oil and natural gas (including coalbed methane, oil shale, oil sand, shale gas, etc.) by foreign investment is limited to joint ventures and cooperation, and the restrictions on foreign investment in the construction and operation of gas stations will only be lifted in 2018. From the perspective of distribution structure, in 2016, there were 136 registered oil and natural gas exploration enterprises with total assets of 1999.57 billion, among which there were 83 state-owned enterprises with assets of 1889.5 billion, accounting for 94.5% of the whole industry. The number of state-owned economic enterprises in the petroleum processing, coking and nuclear fuel processing industries accounted for 11.8%, while the assets accounted for 50.7%.

The oil and gas industry has high barriers in the whole chain from exploitation, import, refining to sales, which are mainly monopolized or dominated by state-owned enterprises, and private capital is difficult to enter. Taking oil exploitation as an example, China has implemented a block registration system for domestic oil resources, which makes it difficult to meet the qualification review requirements, making a few large state-owned enterprises in a monopoly position. The degree of marketization of oil and gas exploitation is low, the pricing power of suppliers is high, the price control lacks scientific pricing basis, and the domestic oil price is falsely higher than that of foreign countries.

Power industry: state-owned enterprises monopolize or dominate, and resources are misallocated

At present, state-owned enterprises almost occupy a monopoly or dominant position in power generation, market dispatching, transmission, distribution and sales, and private capital is difficult to enter. Different from the natural monopoly formed after free competition in foreign countries, the current monopoly of state-owned enterprises in the power industry is mainly caused by early administrative policies. Although in recent years the state has liberalized the restrictions on private capital's power distribution business, and this year has liberalized foreign capital's operation and construction of power grids, the monopoly formed for a long time still makes it difficult for private capital to enter.

The monopoly power without competition leads to unreasonable allocation of market resources: on the one hand, some local governments pursue local performance and vigorously develop wind power generation, and excessive construction of power plants leads to a large number of wind power plants being idle; On the other hand, in order to maintain local employment, backward enterprises such as thermal power plants that pollute the environment can never be eliminated, and the overall social welfare is damaged. In addition, with seasonal changes and changes in industrial power consumption, state-owned enterprise groups regulate and control power monopoly mutually, and maintain a false high electricity price, resulting in violations of people's livelihood interests.

3.4 Service industry: the basic public service is mainly state-owned enterprises, and the overall restriction level is high

At present, China's basic service industry has high restrictions on foreign investment, mainly state-owned enterprises, and the market competition is relatively insufficient, while the new economy service market competition is relatively sufficient. Specifically, it can be divided into three categories: first, the basic service industries that restrict foreign investment and are monopolized by state-owned enterprises, such as telecommunications services, education, medical services, etc; Second, service industries, such as the financial industry, where state-owned enterprises occupy a dominant position and more administrative regulations lead to insufficient market competition; The third is the life service industry with full market competition and private enterprises, including catering services, express delivery, etc.

3.4.1 The first category: basic service industries monopolized or dominated by state-owned enterprises, limiting the proportion of foreign equity

Telecommunication services: state-owned enterprises dominate and set the proportion of foreign equity

At present, state-owned enterprises occupy a dominant position in the telecommunications service industry. Due to restrictions on foreign investment, nature of natural monopoly industry and other factors, it is difficult for private enterprises and joint ventures to enter the telecommunications service field. Since 1999, China's telecommunications service industry has experienced two rounds of splitting. The introduction of competition and the breaking of monopoly have promoted the rapid rise of the level of telecommunications services for a period of time. However, the current level of openness of China's telecommunications service industry is still low, and foreign capital should not hold more than 50% of value-added telecommunications services (excluding e-commerce). The basic telecommunications services must be controlled by the Chinese side. Private capital entering the field of basic telecommunications mainly includes China Telecom, China Mobile and China Unicom Introduction of strategic investors, lack of decision-making power and management power, and state-owned capital still occupies a dominant position. By the end of 2017, China Telecom, China Mobile and China Unicom all had more than 50% of their state-owned capital shares. The result of the monopoly position imposed by administrative intervention is that China's telecommunications service industry has problems such as slow technology upgrading, high fees, poor services, etc.

Education: state-owned capital dominates, and educational resources are unevenly allocated

At present, compulsory education, high school education and higher education are dominated by state-owned capital, and the distribution of educational resources is uneven. Education is the foundation of a country's development. The investment of state-owned capital in the education industry belongs to public services, which is conducive to the promotion of social welfare. However, there are still some problems in China, such as unbalanced distribution of schools, unbalanced teacher resources, and unbalanced school hardware resources, which lead to the concentration of students to schools in a few areas, the loss of teacher resources, and vicious competition among schools. In the education industry, state-owned capital should give full play to its advantages, forward-looking balanced resource allocation, reasonable planning, standardized operation and the establishment of appropriate internal incentive mechanisms. Private capital should supplement state-owned capital in higher education, preschool education and other fields to meet diversified needs.

Medical service: public hospitals dominate, while private hospitals are numerous but not strong

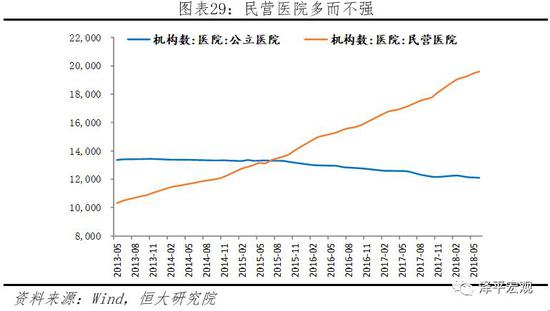

Foreign investment in medical institutions is limited, and private hospitals are numerous but not strong. At present, foreign investment in Chinese medical institutions is limited to cooperation and joint venture with China, and foreign investment is limited. There are many private hospitals but not strong ones in domestic medical institutions. According to the National Bureau of Statistics, there were 30000 hospitals in 2017, including 12000 public hospitals and 18000 private hospitals. Although the number of private hospitals is more than that of public hospitals, due to the inclination of medical resources and policies, private hospitals are still unable to compare with public hospitals in terms of scale, overall technical level and medical service capacity.

In addition, the disorder of drug circulation and the imperfection of the internal salary incentive mechanism for medical staff in public hospitals have jointly pushed up the cost of medical care, which has damaged consumer welfare and made it difficult to solve the problem of expensive and difficult medical care. In the past, the tariff of imported drugs in China was about 4% - 8%, and 16% of value-added tax was paid. The high drug tax burden caused the price of imported drugs to rise by nearly 30%. Since May 1, 2018, China has exempted or lowered tariffs on most drugs, such as anti AIDS drugs, anti-cancer drugs, hormone contraceptives, and reduced VAT, and the price of imported drugs has been lowered. However, the current order of drug circulation in China is chaotic, and the sales expenses of pharmaceutical enterprises are abnormally high, which mainly flow to public relations bidding, doctors' rebates, medical representatives' commissions, etc. (see the earlier report "Uncovering the Mystery of the Abnormal High Sales Expenses of Chinese Pharmaceutical Enterprises" for details). In addition, China provides less subsidies to public hospitals, which is lower than the international average level. The basic salary of medical staff is relatively low, and the internal salary incentive model is not perfect, resulting in "medicine for medicine" and "equipment for medicine". The multiple premiums of dealers and hospitals have further pushed up drug prices. It is necessary to further reduce tariffs and value-added taxes, strengthen the maintenance of drug circulation order, improve the reward and punishment mechanism for medical staff, reduce drug prices, and solve the problem of ordinary people The problem of expensive medication.

3.4.2 Category II: dominated by state-owned enterprises, limited foreign equity ratio, more administrative controls, insufficient market competition

Financial industry: state-owned enterprises dominate, set foreign equity ratio, limit business scope and license

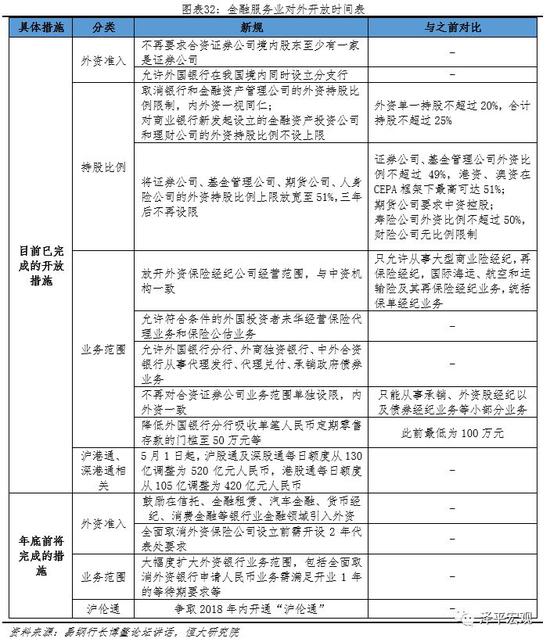

At present, state-owned enterprises in China's financial industry still dominate, the degree of institutional openness lags behind the international level, and private capital is difficult to access. For a long time, due to the differences between domestic and overseas market rules and systems, inadequate supporting laws and regulations, exchange rate system and other factors, the opening up and reform of the financial industry has been repeated and slow (see the previous report "China's financial opening up: achievements, shortcomings and changes" for details). Before the implementation of further opening measures in 2018, banks, securities and insurance companies have strict shareholding ratio restrictions. Taking the banking industry as an example Bank of China The industry is still dominated by state-owned enterprises, and the proportion of foreign and private banks is relatively low. Since the 1990s, the proportion of foreign banks' assets has been hovering around 2%, and in 2017 it has dropped to 1.1%, far below the average level of over 10% in OECD countries.

In addition, in the past, foreign-funded and private enterprise institutions also faced administrative policy constraints such as business scope and license issuance. Foreign securities institutions were limited to joint ventures, and their business was limited to underwriting, foreign stock brokerage, bond brokerage and other small businesses; The waiting period for RMB business of foreign banks is long, and the requirements for the total assets scale of foreign banks to set up business institutions in China are too high; Foreign insurance faces strict license approval and quantity control; Foreign securities institutions are limited to joint ventures and can only engage in underwriting, foreign stock brokerage, bond brokerage and other small businesses.

In April 2018, General Secretary Xi Jinping stressed in his speech in Boao that we will further expand the opening up and ensure the implementation of major measures to relax the opening up of foreign capital in banking, securities and insurance industries in the service industry, especially in the financial industry. With the announcement of the new round of opening up schedule of the financial industry and the continuous implementation of some opening measures, China will promote the opening up of the financial industry with greater determination and firmer courage.

3.4.3 The third category: life service industry with full market competition and private enterprises

Express industry: full market competition, dominated by private enterprises

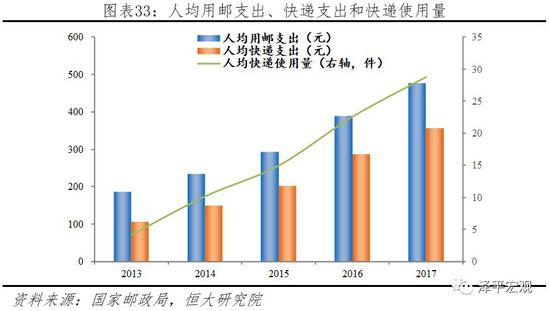

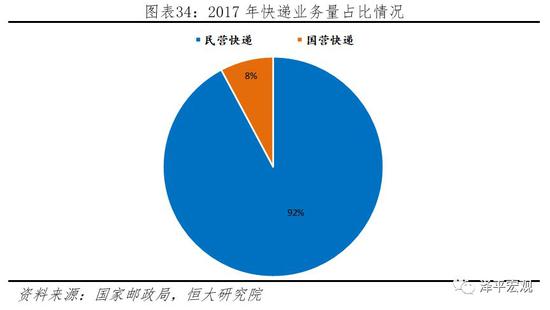

In addition to ordinary mail and letter post, China's express industry is currently fully competitive, forming a competitive pattern of Shunfeng+"Four Links and One Access", and greatly improving market efficiency and product services. With the innovation of new retail in China and the expansion of globalization, as well as less administrative control, China's express logistics is fully competitive, and the industry service, efficiency, and scale are all accelerated, and gradually promoted to the overseas market. In 2017, the business volume of express service enterprises completed 40.06 billion pieces, a year-on-year increase of 28%; The express business revenue reached 495.71 billion yuan, up 24.7% year on year. Among them, the business volume of private express enterprises reached 36.95 billion pieces, with a business income of 424.39 billion yuan. The market share of business volume of private express enterprises is 92.2%, and the market share of business income is 85.6%.

Catering industry: mainly private enterprises, with full market competition, actively exploring overseas markets

State owned enterprises have basically withdrawn from the catering industry, while private enterprises are facing fierce competition and rapidly expanding overseas markets. The catering industry, as a relatively early industry of reform and opening up, is developed by individual, private and foreign-funded enterprises before other industries. The focus of competition is from simple price competition and product quality competition to competition between products and corporate brands and cultural tastes. The degree of marketization is relatively high, and the products are exported to overseas markets. In 2016, the catering industry employed 1.295 million people, of which 1.244 million were employed by non-state-owned enterprises, accounting for 95.8%.

4. Comparison of state-owned enterprise reform plans

From the perspective of international experience, in the past, countries adopted different methods to reform state-owned enterprises at different levels, mainly from the two directions of property rights system reform and strengthening competition to promote the reform of production efficiency. In general, shock therapy and overly radical "no restricted area" reform and other programs will lead to results contrary to expectations, with a large negative impact. From China's practice, a series of reform explorations have gradually formed the reform methodology of "gradual+incremental+pilot" and the successful experience of adjusting measures to local conditions, implementing policies according to industry, introducing market competition mechanism, reforming single state-owned property rights, strengthening macro-control and relaxing micro intervention.

4.1 One step radical "shock therapy"

The core of "shock therapy" is rapid liberalization, stabilization and privatization. Its theory originated from western neo liberalism and modern monetarism, and was introduced into the economic field by American Jeffrey Sachs in the 1980s. "Shock therapy" emphasizes that the reform should be carried out in one step, and advocates that the liberalization of prices, foreign trade and currencies should be realized once and for all in terms of liberalization; In terms of stabilization, we should adopt tough and tight macro policies to curb the total social demand and achieve short-term supply and demand rebalancing; In terms of privatization, it advocates the full and rapid privatization of state-owned enterprises, even at the expense of free distribution.

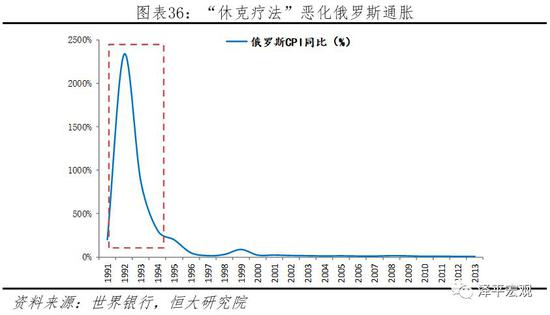

In the 1980s, "shock therapy" was implemented in Bolivia in Latin America and achieved initial success. After curbing hyperinflation, it was welcomed by Russia and some countries in Eastern Europe, which were plagued by economic recession and hyperinflation. However, the "sports style" radical implementation of privatization, excessive copying of the Western market economy model, and incompatibility with the basic national conditions, market economy transition laws and other issues make the radical "shock therapy" ineffective in Russia, Eastern Europe and other countries. Since the implementation of "shock therapy" in 1991, Russia's GDP did not rise but fell, and hyperinflation further worsened. From 1991 to 1992, the GDP growth rate dropped significantly from - 5.05% to -14.53% in 1992, and the year-on-year CPI growth rate rose from 200% to 2333.3%.

4.2 Privatization reform of Thatcher's "no restricted zone" in Britain

In the mid-1970s, Britain fell into the stage of "stagflation", with inflation rising and economic growth declining. In addition, due to the excessive expansion of government functions and government size, the financial burden increased. Thatcher came to power in 1979, believed in modern monetarism theory, and announced the implementation of the largest privatization reform in British history.

The characteristics of Thatcher's privatization reform plan for state-owned enterprises are that it is easy before it is difficult, and it is comprehensively promoted "without restricted areas". From 1979 to 1991, Thatcher gradually pushed the privatization field from competitive manufacturing to natural monopoly fields such as oil, natural gas, electricity, water supply, postal services and railways in three stages through direct sale of state-owned enterprises, public listing, internal management acquisition of state-owned enterprises, contracting, and implementation of employee share ownership. In addition, Thatcher also pushed privatization to social welfare and government administrative institutions, including traffic safety supervision, private weapons inspection and the transportation of ordinary prison prisoners.

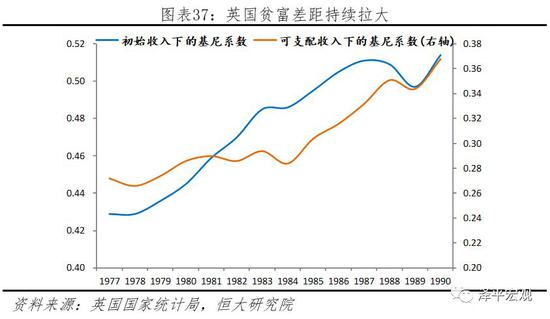

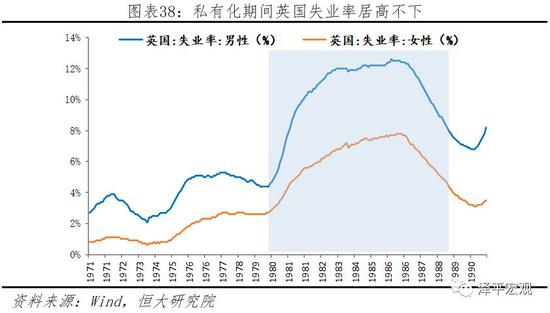

Thatcher's privatization reform effectively curbed inflation, stabilized economic growth and improved the efficiency of state-owned enterprises, but it also brought negative effects: 1) "no forbidden zone" privatization led to the decline in the quantity and quality of public services. Due to the pursuit of profit maximization by private enterprises, investment tends to focus on short-term profit seeking areas, private enterprises have a weak sense of public service, and people's interests are damaged. 2) The functions of enterprises and the government are separated, and unemployment is serious. Since a large number of state-owned enterprises pursued the maximization of benefits after privatization, a large number of employees were fired. After Thatcher's privatization, from 1979 to 1989, the unemployment rate in Britain remained high, up to 11.8%. 3) Rent seeking was serious during privatization, and the gap between rich and poor was further aggravated.

4.3 Gradual reform of stock adjustment and incremental reform

Progressive reform is a market-oriented reform carried out on the basis of industrialization and the socialist constitutional system. Its core can be summarized as the reform from point to area, from part to the whole, combining reform within the system with promotion outside the system, and coordinating reform, development and stability. It emphasizes the implementation of item by item, step by step, and incremental reform on the premise that the basic does not touch the pattern of vested interests. The success of China's reform and opening up in the past 40 years is based on the method of "gradual+incremental+pilot", which is in line with epistemology.

In terms of state-owned enterprise reform, the gradual reform advocates that the reform of state-owned economy should be gradually promoted through stock adjustment and incremental improvement. Specifically, the state ownership has changed from a single property right subject to a diversified property right subject, and the reform process has shown obvious phased and gradual characteristics. Its essence is the partial reform of the original state-owned economic property rights system, and the reform of state-owned enterprises has been deepened in accordance with the principles of point to surface, easy before difficult, and from simple to deep.

Compared with "shock therapy", the advantages of gradual reform lie in gradually advancing, allowing trial and error, reducing reform resistance, accumulating reform strength, and diluting the proportion of stock through increment, but at the same time, it also relatively ignores the construction of supporting mechanisms for stock assets, which creates bottlenecks for further economic development. When the reform enters the deepwater area, the space for incremental reform is getting smaller and smaller, and the stock has to be adjusted.

4.4 Reform of classified state-owned enterprises that implement policies based on industry

The classification system reform advocates that according to the externalities and strategic significance of different industries, whether and to what extent state-owned capital will enter, adopt corresponding assessment methods, and clarify the strategic positioning and development goals of state-owned capital.

In 2015, the Guiding Opinions on Deepening the Reform of State owned Enterprises issued by the Central Committee of the Communist Party of China and the State Council clearly proposed that state-owned enterprises should be divided into public welfare and commercial categories. Among them, public welfare state-owned enterprises, with the main goal of ensuring people's livelihood, serving the society, and providing public goods and services, should adopt the form of solely state-owned enterprises, focusing on cost control, product and service quality, operating efficiency, and social security capabilities. For commercial state-owned enterprises, commercial operation is carried out according to the requirements of marketization, with the main goal of enhancing the vitality of the state-owned economy, enlarging the function of state-owned capital, and achieving the preservation and appreciation of state-owned assets. In principle, the reform of the corporate shareholding system is implemented, competition is introduced, and the survival of the fittest is achieved. The state-owned commercial enterprises, which are in important industries and key fields related to national security and the lifeline of the national economy and mainly undertake major special tasks, shall be kept state-owned.

4.5 Mixed ownership reform

Mixed ownership reform is a mixed reform of public ownership and non-public ownership under the condition that public ownership is the main body. From a macro perspective, mixed ownership is a diversified form of mixed ownership in which public ownership and non-public ownership coexist in the socio-economic system; From a micro perspective, it is a form of ownership in the same economic organization, which includes public and non-public ownership, and gives play to their respective advantages.

The core of mixed ownership reform of state-owned enterprises is marketization, introducing non-public capital to participate in the reform of property rights system, improving governance mechanism and strengthening market-oriented operation and management. Among them, the foundation of mixed ownership reform is to clarify property rights. Only by establishing a sound modern enterprise property rights system can we truly introduce strategic investors into state-owned enterprises, improve corporate governance mechanisms, and achieve market-oriented operation and internal management. At present, the forms of mixed ownership reform of state-owned enterprises mainly include the listing of state-owned enterprises as a whole, the introduction of private capital and foreign capital and other strategic investors to participate in the shares, the acquisition of private enterprises by state-owned enterprises and the maintenance of a certain proportion of private enterprises' equity, employee equity, etc.

China Unicom, COFCO CNNC And other state-owned enterprises have made progress and improved efficiency. Taking the mixed reform of China Unicom as an example, in August 2017, China Unicom privately issued 9.037 billion shares and introduced strategic investors such as Alibaba, Baidu and JD through private placement. After the completion of the mixed reform, China Unicom Group held about 36.67% of the company's shares in total, China Life , Tencent Cinda, Baidu Penghuan, JD Sanhong, Ali Venture Capital, Suning Cloud Commerce and other strategic investors hold about 35.19% of the company's shares in total. After further forming the diversified equity structure of mixed ownership, China Unicom changed its board of directors in February 2018. Among the eight non independent directors, five came from strategic investors such as Alibaba, Tencent and Baidu. At the same time, China Unicom also streamlined its organization and laid off staff, and promoted the Interim Measures for the Management of Incentive Plans for Restricted Stocks. After the mixed transformation, the profitability of China Unicom has significantly improved. The ROE disclosed by China Unicom in the first quarter report and the middle report in 2018 was 0.96% and 1.89%, respectively, 171% and 89% higher than the same period in 2017.

4.6 To be stronger and better, to be a big country with capital

The 19th National Congress of the Communist Party of China (CPC) has made a breakthrough and transformation in the concept of state-owned enterprises and assets reform, from strengthening and optimizing state-owned enterprises to strengthening and optimizing the capital of large countries, further delegating power and reducing the intervention in market micro entities.

Specifically, in terms of state-owned assets supervision, it is necessary to change from enterprise management to capital management, transform the functions of state-owned assets supervision institutions based on capital management, clarify the supervision content based on capital management, change the administrative management mode, improve the assessment system and methods, and accelerate the development and improvement of corresponding supporting assessment mechanisms; In terms of state-owned capital management, it is required to reform the authorized management system of state-owned capital, scientifically define the boundaries of ownership and management rights of state-owned capital, and implement the property rights of legal persons and management autonomy of enterprises; In the market environment, the management of capital, regardless of the nature of the enterprise, requires the improvement of fair and fair market access and competition neutrality.

5 Suggestions for SOE reform: classification+mixed transformation+strengthening competition

The reform of property rights is a deeper level of opening and reform, and also an internal requirement for improving total factor productivity. General Secretary Xi Jinping clearly pointed out that "we must unswervingly develop the public economy, and unswervingly encourage, support, guide and protect the development of the private economy". "The private economy is the internal element of China's economic system, and private enterprises and private entrepreneurs are our own people.". There is no difference between state-owned enterprises and private enterprises. Both of them have made important contributions to China's economic development and are indispensable components to achieve the "two centenary goals".

At present, the reform has entered the deep water area, and further promoting the reform of property rights is the only way to promote China's high-quality development. This requires us to focus on the basic economic system, take liberating and developing social productivity as the standard, take improving the efficiency of state-owned capital and enhancing the vitality of state-owned enterprises as the main line, clarify property rights, introduce competition, govern enterprises according to law, and implement policies based on industry, Replace invalid and inefficient property rights with effective property rights, and realize standardization of corporate governance of state-owned enterprises, marketization of company operation, and neutralization of enterprise competition.

Specifically, we put forward six suggestions:

First, we should adhere to the basic economic system, treat state-owned and private economies equally, and implement the principle of competition neutrality. Cancel the differentiated treatment of ownership classification, emphasize the neutrality of competition, and do not easily get on the agenda and fall into ideological debate. It should be measured by the pragmatism standard of black cats and white cats. All enterprises registered in China, whether state-owned, private or foreign, are Chinese enterprises, which are subject to the management of the Chinese government and contribute to China's economic growth and employment creation.

Secondly, in terms of methodology, the reform of state-owned enterprises adheres to the methodology of "gradual+incremental+pilot", establishes a reasonable assessment, reward and punishment mechanism, establishes a fault-tolerant and "exemption" mechanism, and improves local enthusiasm. In the past, great progress has been made in the reform of state-owned enterprises. However, at the current local implementation level, there are problems of "doing more and making fewer mistakes, not doing well", "not daring to change, unwilling to change, and not able to change". We should adhere to the successful experience of "gradual+incremental+pilot" in the past, link the reform measures with the establishment of the rule of law, and establish a fault-tolerant, error correction and "exemption" mechanism for local governments, Mobilize the enthusiasm and enthusiasm of local governments for reform. In the reform of state-owned enterprises, the "loss of state-owned assets" has become an invisible shackle and sensitive area that shackles the government and state-owned enterprise leaders, which can be removed by an independent third-party asset appraisal agency to assess its reasonable value or by means of public bidding transfer.

Third, we will continue to implement the reform of the classification system of state-owned enterprises, further clarify the division of public welfare, resource commerce and competitive commerce industries in line with local conditions, and fully open market access and eliminate the fittest in competitive commerce. The classification should be further clarified according to the characteristics of the industry, pointing out the direction for the reform: first, the central government issued guidance, clarified the industry classification standards, and guided the division of public welfare and commercial state-owned enterprises in various regions; Second, the local government has studied and issued relevant documents, implemented industry division according to local conditions, launched a negative list, implemented policies according to the implementation, classified development, classified supervision, classified accountability, and classified assessment; The third is to moderately and dynamically adjust the classification according to the development and changes of the industry on the premise of following the principle of national unified classification. For competitive fields, we will fully liberalize market access and allow private enterprises and foreign capital to compete fully.

Fourth, on the premise of clarifying the areas that state-owned enterprises should control or participate in, clarify property rights, promote the reform of mixed ownership, reform the operating system, and strengthen the complete performance appraisal standards. First, it is necessary to clarify the definition of ownership, management right, income right and disposal right in the property rights of state-owned enterprises, define the relationship between the government and the market, define the powers and expenditure responsibilities, break the rigid cashing and implicit government guarantee, and strengthen the budget constraints of state-owned enterprises; Second, improve the management system of various state-owned assets, reform the authorized management system of state-owned capital, accelerate the optimization of the layout, structural adjustment and strategic restructuring of the state-owned economy, and promote the preservation and appreciation of state-owned assets; Third, strengthen performance appraisal standards, establish a salary incentive mechanism linked to the market, and encourage, reward, and protect innovative technologies and applications; Fourth, for the reform of mixed ownership, we should effectively transform the operating mechanism and protect the legitimate rights and interests of all kinds of property rights.

Fifthly, in the fields that state-owned enterprises must control or participate in, promote the internal competitive reform of state-owned enterprises, split public welfare and resource industries or establish new state-owned enterprises, introduce internal competition of state-owned capital, establish corresponding assessment mechanisms, entry and exit mechanisms, and formulate open, transparent and reasonable subsidy standards. In the public welfare and resource industries, there is no conflict between adhering to the dominance of state-owned capital and introducing competition. Monopoly state-owned enterprises and newly established state-owned enterprises can be split. The focus is to introduce competition between state-owned capital in suitable key industries, establish corresponding assessment indicators and entry and exit competition mechanisms, activate the stock and increment of state-owned capital, and further improve the efficiency of state-owned capital. For long-term implicit government subsidies, they should be open and transparent, and subsidy standards should be formulated.

Sixthly, in terms of the specific promotion of reform, we should avoid "one size fits all" and sports promotion, rely more on market-oriented means, improve the state-owned assets supervision system, and prevent the distortion of policy implementation. Local governments are encouraged to implement policies in a more flexible and local way, and avoid one size fits all and moving forward. More rely on marketization rather than administrative order. We will improve and strengthen the classified supervision system of state-owned assets to prevent policy deformation and failure in the implementation process.

(The author of this article introduces: Chief Economist of Evergrande Group, President of Evergrande Economic Research Institute. He once served as Deputy Director of the Research Office of the Macro Department of the Development Research Center of the State Council, Director General Manager and Chief Macro Analyst of Guotai Jun'an Securities Research Institute.)