Article/Yang Wang, columnist of Sina Financial Opinion Leader (WeChat official account kopleader)

In recent years, the two-way fluctuation of the RMB exchange rate and the differentiation of market expectations are obvious, and the flexibility of the RMB exchange rate against the US dollar has gradually increased. Since April 2018, the RMB has continuously depreciated against the US dollar. The monthly average exchange rate of RMB depreciated from 6.2975 in April to 6.8445 at the beginning of September, reaching 8.69%.

Over the past two weeks, the RMB exchange rate has gradually approached the 7 level. On October 31, the onshore RMB exchange rate fell below the 6.97 level, and the offshore RMB closed at 6.9804. On November 2, influenced by such favorable factors as the short-term collapse of the US dollar index and the close communication between China and the US, both onshore and offshore RMB recovered 6.89 on that day. In the past week, the onshore and offshore RMB exchange rates fell back to 6.96 again. For a while, the topic of "breaking the 7" or "keeping the 7" triggered constant market disputes.

Yang Wang, Research Fellow of International Monetary Institute of Renmin University of China

Yang Wang, Research Fellow of International Monetary Institute of Renmin University of China What's the mystery? Historical boundaries and psychological gateways

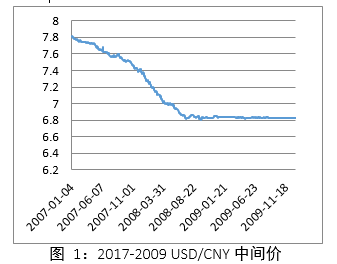

In July 2005, China began to implement the floating exchange rate system, which released the growth dividend accumulated by China's decades of reform and opening up, and the RMB appreciated all the way. The exchange rate of the RMB against the US dollar rose from 8:1 to 6.8:1 in August 2008.

In 2008, the US subprime crisis broke out and the global financial market plummeted. In order to stabilize the RMB exchange rate, the central bank took the measure of pegging the US dollar exchange rate to stabilize the US dollar/RMB exchange rate between 6.8 and 6.89 (as shown in Figure 1). This is the first time that the market has known the 7 bottom lines of the RMB exchange rate. After 2010, with the recovery of the world economy and the accelerated development of China's economy, the RMB has been on the fast track of appreciation. At the end of 2014, the RMB exchange rate appreciated to around 6.

In 2016, events such as Brexit, the Federal Reserve's interest rate hike, Trump's election and so on strengthened the US dollar, devalued the RMB by nearly 6.83% throughout the year, and at the end of 2016, the central parity rate between the US dollar and the RMB broke the 6.96 threshold (as shown in Figure 2). In the end, the central bank used a quarter of its foreign exchange reserves to combat international shorting forces and kept the exchange rate at the 7 level. This has established the important position of the "seven pass of the US dollar/RMB exchange rate".

Data source: China Foreign Exchange Trading Center, Hande Financial Technology Research Institute

Data source: China Foreign Exchange Trading Center, Hande Financial Technology Research Institute The "7" exchange rate pass is not only a boundary that has never been broken in history, but also a milestone for the central bank to "protect the exchange rate". It is also a psychological pass for investors. Some studies have pointed out that every time the exchange rate approaches the threshold of 7, there will be a wave of short-term liquidity concentration of short selling RMB. Once the exchange rate breaks through the psychological threshold of 7, investors' expectations of the future depreciation space of RMB may be enlarged. The herding effect of chasing up and killing down will make the difficulty and cost of exchange rate adjustment multiplied. Especially when the international environment is unstable and China's economy has entered the gear shifting range of growth, a breakthrough of 7 may give a big blow to investors' confidence.

Keep the bottom spirit of 7 and the pressure of breaking 7

One of the bottom lines is that China's economic fundamentals are sound.

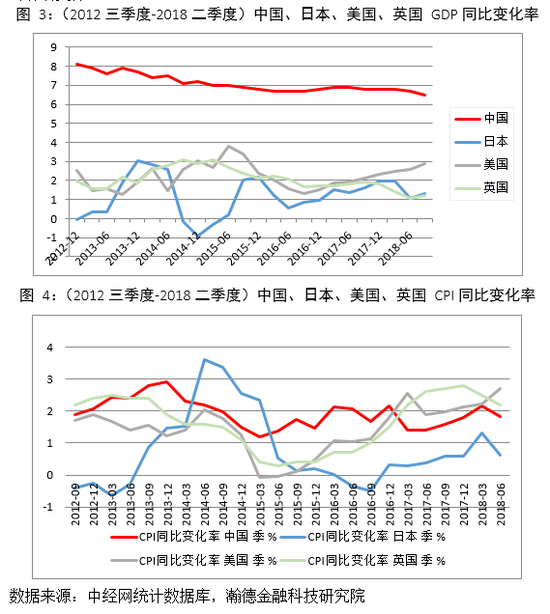

The quarterly fluctuation does not exceed 0.1%, and the annual GDP growth rate is still in the range of 6.7% - 6.9%. China's economy has entered the "L" shift phase, but the growth rate is still significantly higher than that of the United States by about 2% (as shown in Figure 3). The employment situation is good. In August 2018, the unemployment rate in the national urban survey was 5%. In terms of prices (as shown in Figure 4), inflation was moderate. From 2001 to 2017, China's average inflation was 2.3%, far lower than that of other developing countries and close to that of developed countries, which became a favorable support for the long-term exchange rate.

Second, policy guidance should avoid excessive depreciation of the exchange rate.

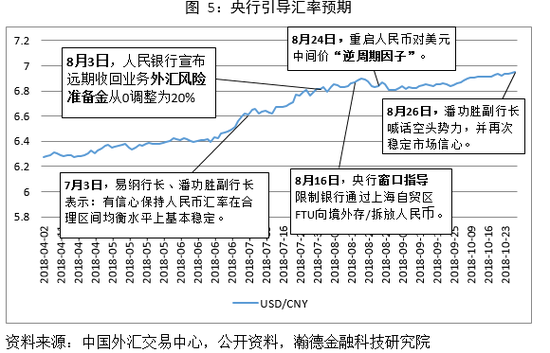

For some time, the monetary authorities and foreign exchange management departments have withdrawn from the normal intervention in the foreign exchange market and will not directly participate in foreign exchange transactions. At present, its main indirect policy instruments include: adjusting the foreign exchange demand in the offshore market, increasing transaction costs, adjusting the exchange rate formation mechanism, and guiding market expectations. (See Figure 5) In April 2018, since the RMB entered the channel of accelerated depreciation against the US dollar, the authorities have comprehensively used indirect adjustment means to guide expectations and hedge the pro cyclical behavior of the market in the direction of depreciation.

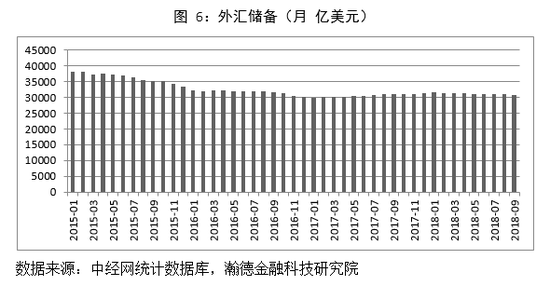

Of course, under certain circumstances, the authorities will also use foreign exchange reserves to intervene in the market to prevent excessive depreciation of the RMB. (See Figure 6) Since 2015, China has always maintained foreign exchange reserves of more than three trillion dollars, and the overall trend is stable.

Third, the process of RMB internationalization has accelerated.

In January 2018, according to the statistics of SWIFT, the share of RMB in international payment currencies was 1.66%, making it the fifth largest payment currency in the world. By the end of 2017, the amount of financial assets held by overseas entities in domestic RMB stocks, bonds, loans and deposits totaled 4.29 trillion yuan, up 41.3% year on year.

The People's Bank of China released the 2018 RMB Internationalization Report, which shows that the development of RMB internationalization presents the following characteristics: First, the scale of cross-border settlement of RMB under service trade continues to rise; Second, securities investment led to rapid growth of RMB cross-border settlement scale under capital account; Third, the macro prudential management policy of full caliber cross-border financing has been further improved, which is conducive to reducing the financing cost of the real economy; Fourth, the participation of overseas entities in the domestic financial market has increased significantly, especially the introduction of the bond link, which has further promoted the two-way opening of China's domestic financial market; Fifth, the introduction of RMB crude oil futures trading has made breakthroughs in the RMB pricing function of bulk commodities.

In recent news, Abe visited China on the 25th, and the People's Bank of China announced on the 26th that China and Japan would restart currency swap, with an agreement size of 200 billion yuan/3.4 trillion yen and a validity period of three years. Compared with the swap agreement five years ago, the scale of the swap agreement has expanded by as much as 10 times this time. The signing of the bilateral monetary agreement between China and Japan marks an important step in the internationalization of the RMB.

It can be seen that the process of RMB internationalization is accelerating, and the position of RMB in international trade is also rising, which will be one of the important driving forces for the long-term appreciation of RMB.

One of the pressures is that the US economy continues to improve, and the expectation of interest rate increase remains.

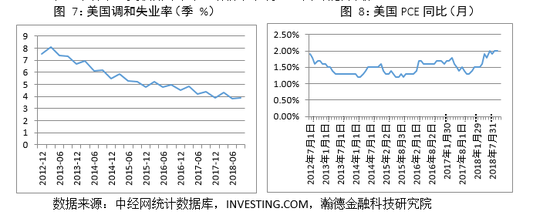

Since 2018, the U.S. economy has continued to improve, and the employment market and economy have shown strong performance. The unemployment rate dropped to a new low (as shown in Figure 7). At the same time, the US GDP grew at an annual rate of 2.3% in the first quarter, and further increased to 4.1% in the second quarter, the best level since the third quarter of 2014. In terms of inflation, there are signs of rising (as shown in Figure 8). The core personal consumption expenditure deflator (PCE) of the United States hit the 2% target of the Federal Reserve for the first time in six years. Under these conditions, the Federal Reserve is optimistic about the future economic prospects and may raise interest rates again in December.

The second pressure is that China's trade surplus advantage has faded, and the financial surplus foundation is unstable.

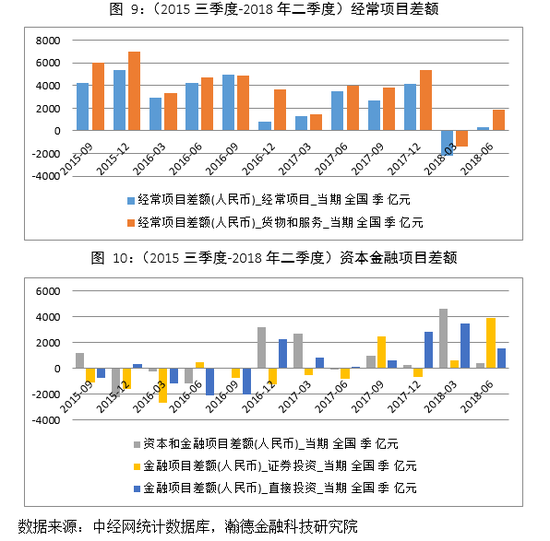

Although the balance of payments has shown a double surplus since 2017, the current account surplus of the balance of payments has decreased significantly due to the impact of Sino US trade (see Figure 9). The difference between capital and financial items fluctuates greatly (as shown in Figure 10). The market's concern about the "double deficit" may lead to negative sentiment.

Third, the uncertainty of the international situation has increased.

Since the Trump government imposed global tariffs on steel and aluminum in April 2018, international trade disputes have continued, protectionist trends continue to rise, and the global pattern is changing. The international situation is increasingly uncertain.

The Democratic Party's victory in the recent mid-term elections in the United States has plunged the Congress into a "split" state. There is greater uncertainty about whether Trump's tax cuts, infrastructure expansion and other related policies can be successfully launched, and whether Trump can be re elected. In addition, the political turmoil in the euro area cannot be ignored. In addition to Brexit and Italy's fiscal easing, Germany has also become an important uncertainty factor in the Eurozone. The Christian Social Union (CSU), a sister party of the Christian Democratic Union (CDU) led by German Chancellor Merkel, lost in the local elections in Bavaria on the 14th. On October 28, Merkel's conservative party and its Berlin ally, the Social Democratic Party, lost the election in Hessen again, which brought a new blow to the fragile Merkel government. Merkel said she would give up running for the party chairman. As the "actual leader" of the EU and the euro area, Merkel's departure will have a greater impact on the euro area. As the euro accounts for more than half of the dollar index, the situation in the euro zone will benefit the dollar.

It doesn't matter whether it breaks 7 or not, but reasonable and balanced fluctuation is more important

Holding a certain point will conflict with other policy objectives. According to Mundell's classic theory of impossible triangle, maintaining foreign exchange stability, ensuring independent monetary policy and free capital flow cannot coexist. In order to maintain the stability of the exchange rate, foreign exchange control or capital control measures need to be taken, which is very passive in the current situation of increasing external environment variables. It will also cause distortion in price formation and resource allocation. In fact, whether it is 6.9 or 7, holding a certain point is not a reference for keeping the exchange rate stable. More consideration should be given to the stability of the exchange rate, whether it fluctuates near a reasonable equilibrium level, which can change dynamically according to market conditions.

Exchange rate marketization needs to break the point thinking. In recent years, the market-oriented reform of the RMB exchange rate has been deepening. From the 811 exchange rate reform, to increasing the number of CFETS basket currencies, to the introduction of "counter cyclical adjustment factors", all these have improved the RMB dollar central parity mechanism and deepened the reform of exchange rate marketization. It needs to be recognized that an important problem in the current foreign exchange market is that there is a certain deviation between the market perception and the government policy guidance framework, which leads to irrational fluctuations in the RMB exchange rate and more obvious herd effect. "The threshold of US dollar against RMB 7" is a reflection of this market cognitive bias. Therefore, breaking the point thinking of investors and shaping the concept of "RMB will fluctuate within a reasonable range" is a very important booster for the market-oriented reform of the exchange rate.

Finally, we need to realize that, first, the possibility of RMB exchange rate plummeting in a short term is very low, and two-way fluctuation within a reasonable range is a trend with high probability in the future; Second, the reasonable and balanced level of the RMB exchange rate is dynamic; Third, we also need to recognize that the RMB still has a long-term appreciation basis.

(The author of this article introduces: Vice President of Hande Institute of Financial Science and Technology, and researcher of International Monetary Research Institute of Renmin University of China.)