Article/Huang Zhilong, columnist of Sina Financial Opinion Leader (WeChat official account kopleader)

We have reason to believe that after the offshore central bank bills enter Hong Kong, the policy stance of the central bank will be more distinct, the ammunition supply against international capital will be very sufficient, the international capital attempting to short RMB will also retreat from difficulties, and the phenomenon of disorderly devaluation of the offshore RMB exchange rate will disappear.

In recent months, the offshore market short RMB has made a comeback, and the central bank is facing the attack. In addition to foreign exchange risk reserves, counter cyclical factors and other tools, the offshore central bank bills landed on November 7 have become another sharp weapon to stabilize the offshore RMB exchange rate. You may be curious: what is the expected impact of offshore central bank bills on stabilizing the RMB exchange rate? Can it achieve the expected effect? See the analysis below.

The Past Life of Central Bank Bills

Before discussing offshore central bank bills, it is necessary to briefly analyze the origin of central bank bills.

Central bank bills (hereinafter referred to as central bank bills) are short-term debt certificates issued by the central bank to regulate the excess reserves of commercial banks, and their essence is central bank bonds. After commercial banks subscribe to central bank bills, their loanable funds will decrease in the same scale. In other words, issuing central bank bills is a tightening monetary policy tool to recover the base currency and increase the cost of capital.

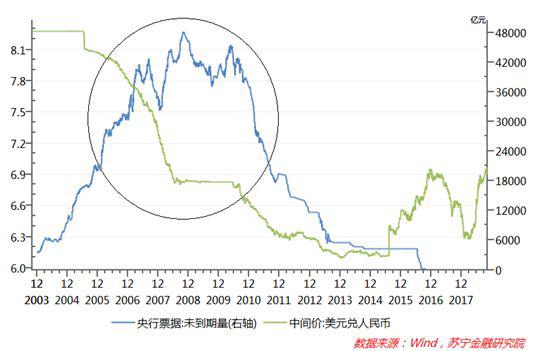

During the period of continuous appreciation of RMB from 2004 to 2011, international capital continued to flow in, the central bank's official foreign exchange reserves increased significantly, and a large number of base currencies were passively released in the form of foreign exchange funds. At that time, the central bank recovered a large number of base currencies by increasing the deposit reserve ratio and issuing central bank bills, in order to prevent liquidity flooding and the deterioration of inflation. During this period, the bank deposit reserve ratio and the central bank's bill issuance scale were at the historical peak, of which the bank deposit reserve ratio once reached the peak of 21.5%, and the central bank's bill issuance scale also reached the peak of 4.811 trillion yuan (see the figure below), accounting for 37.3% of the then basic currency balance (12.9 trillion yuan). It was not until 2015 that the RMB entered the stage of two-way fluctuation, the end of the base currency supply period dominated by foreign exchange, and the central bank began to actively release base currency through MLF and other policy tools, that the central bank bills gradually withdrew from the historical stage.

Three Functions of Offshore Central Bank Bills

The influence process of offshore central bank bills and domestic central bank bills on capital market size and cost is roughly the same. Since Hong Kong is the largest offshore RMB market, on September 20 this year, the People's Bank of China and the Hong Kong Monetary Authority signed the Memorandum of Cooperation on Issuing Bills of the People's Bank of China through the Central Settlement System of Debt Instruments, which means that the People's Bank of China will take advantage of the Hong Kong Monetary Authority to realize "central bank bills going overseas".

Specifically, it is expected that offshore central bank bills will stabilize the RMB exchange rate from the following three aspects:

First, offshore central bank bills will become a sharp weapon to stabilize the offshore RMB exchange rate. Since the RMB capital account has not yet been freely convertible, the RMB exchange rate has also formed two types of onshore (domestic) and offshore (overseas) exchange rates. In most cases, the offshore exchange rate has a more obvious trend of driving the onshore exchange rate. It is worth noting that the offshore market does not have any trading restrictions, so the offshore exchange rate is more vulnerable to speculative factors. Irrational and violent fluctuations not only directly affect the market sentiment of the onshore exchange rate, worsen market expectations, but also impact the onshore exchange rate under the arbitrage mechanism. Therefore, it is crucial to keep an eye on and guide the offshore exchange rate. Since June this year, the devaluation of the RMB exchange rate has accelerated. The central bank has successively taken measures such as "increasing the reserve ratio for foreign exchange risk", "suspending the sub ledger accounting unit of the Shanghai Free Trade Zone", and "restarting the counter cyclical factor", but these are only policy tools to stabilize the onshore exchange rate. Therefore, offshore central bank bills have become an important weapon for the central bank to directly guide the offshore exchange rate.

Second, offshore central bank bills will declare the central bank's policy intention on the RMB exchange rate to international capital. On October 26, Pan Gongsheng, Director of SAFE, made a speech—— "For those forces that try to short the RMB, we all had hands a few years ago, and we are very familiar with each other." It has aroused widespread concern in the market. Among them, the "power of short RMB" mainly refers to the international capital in the offshore market. Generally speaking, the short selling ability of international speculative capital is mainly restricted by two factors: the scale of RMB that can be incorporated, and the cost of integrating RMB. Previously, the exchange between the central bank and international capital was mainly through the way of forward purchase of foreign exchange and foreign exchange swap by Chinese banks in Hong Kong to recover RMB liquidity and raise the cost of funds for short positions in RMB. Similarly, after the introduction of offshore central bank bills, the central bank will directly face the market through the Hong Kong Monetary Authority, and make a clear statement of its own position. By issuing central bank bills, it will recover RMB liquidity, increase capital costs, and combat the short selling force of RMB.

Third, offshore central bank bills will enrich the offshore RMB asset market and promote the process of RMB internationalization. Previously, in the offshore RMB asset market, there were only a small number of medium - and long-term treasury bonds and bonds of financial institutions with maturities of more than two years, while offshore central bank bills were mainly medium - and short-term ones. For example, the first phase of central bank bills issued on November 7 was 10 billion yuan for three months, with a bid winning interest rate of 3.79%; The term of the second central bank bill is 10 billion yuan a year, and the bid winning interest rate is 4.2%. Therefore, once the issuance of central bank bills in the offshore market is normalized, it will further improve the yield curve of the RMB asset market, become the benchmark of short-term interest rates in the offshore RMB financial market, enrich the variety and structure of offshore RMB asset allocation, and help the RMB "going global" and internationalization.

The era of offshore guided onshore exchange rate may end

Since offshore central bank bills are in their infancy, we can only indirectly predict the policy effect of future offshore central bank bills from the impact of changes in Hong Kong's offshore RMB interest rate on the offshore exchange rate.

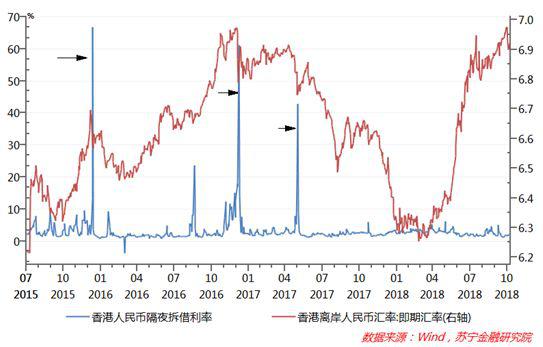

Since the "811 exchange rate reform" in 2015, the trend of the RMB exchange rate passively following the two-way fluctuation of the US dollar index is obvious. Once the US dollar index becomes stronger, international capital has repeatedly prohibited short selling RMB in the offshore market. The People's Bank of China has begun to guide Chinese banks in Hong Kong to tighten their RMB funding, increase the short capital cost of speculative forces, and achieve the expected effect of stabilizing the exchange rate. The following three time points are examples:

From January 11 to 13, 2016, under the pressure of continuous devaluation of RMB, Chinese banks guided Hong Kong's overnight RMB lending to reach 13.44%, 66.81% and 8.3% respectively, and the spot exchange rate of offshore RMB against the U.S. dollar also rose sharply to 6.5673 from 6.6832 on January 10 for three consecutive days.

Around the New Year's Day of 2017, the exchange rate of RMB against the US dollar hit a new low, and the short position of RMB hit again. Chinese banks faced the challenge. The overnight lending rate of RMB was above 7% for 16 consecutive trading days, reaching a high of 61.33% on January 6, and the RMB exchange rate also rebounded from a low of 6.974 to 6.8024.

At the end of May 2017, the People's Bank of China began to take the initiative to attack. On May 31 and June 1, the overnight lending rate of RMB was 21.08% and 42.81%, respectively. The exchange rate of RMB against the U.S. dollar rose sharply again, consolidating the momentum of appreciation of RMB against the U.S. dollar throughout 2017 (see the figure below).

It can be seen that after the capital cost of shorting RMB has been greatly increased, the RMB offshore exchange rate will rise in response, and the policy effect can be described as immediate. We have reason to believe that after the offshore central bank bills enter Hong Kong, the policy stance of the central bank will be more distinct, the ammunition supply against international capital will be very sufficient, the international capital attempting to short RMB will also retreat from difficulties, and the phenomenon of disorderly devaluation of the offshore RMB exchange rate will disappear. As a result, the era that the onshore exchange rate is led by the offshore exchange rate may end, and the RMB exchange rate will also be more determined by changes in the US dollar index and China's economic fundamentals.

(The author of this article introduces: Director and Senior Researcher of the Macroeconomic Research Center of Suning Institute of Finance.)