Article/Guo Huashan, columnist of Sina Financial Opinion Leader Column (WeChat official account kopleader)

Will the loan scale, net interest margin and non-performing ratio, which determine the growth rate of banking profits, support the banking sector to go further in the future? Is the rebound of bank stocks a repair of valuation or a double click of Davis? Is it profitable to buy bank shares now?

The medium and long-term funds released by this round of reserve ratio reduction effectively reduced the comprehensive cost of the bank's liability side, and the decline was greater than the decline of the loan interest rate. The overall net interest margin of listed banks in the third quarter was 1.97 from the second quarter % Expand to 2.07 % Compared with 2.055% in the third quarter of last year, it still expanded slightly. At the same time, the year-on-year growth rate of net profits of 16 listed banks (excluding banks listed after 2017) also rose gradually, with 5.2%, 6.6% and 7.2% respectively in the first, second and third quarters. In addition, the last round of replacement of local government debt to bonds has been completed, reducing the overall risk premium of banks. Asset quality is digesting the burden of bad stock, and the pressure on loan write off and non-performing generation rate are showing signs of improvement. However, can the loan scale, net interest margin and non-performing ratio, which determine the growth rate of the banking industry's profits, support the banking sector to go further in the future? Is the rebound of bank stocks a repair of valuation or a double click of Davis? Is it profitable to buy bank shares now?

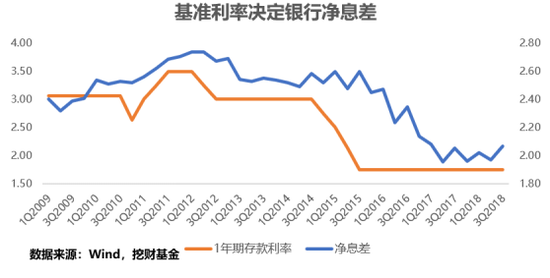

First of all, the improvement of the net interest margin of the current round of banks reached the extreme value, and the possibility of the continuous expansion of the net interest margin without interest rate rise in the future is very low. The bank's net interest margin is fundamentally determined by the central bank's benchmark interest rate. When the central bank raises the benchmark interest rate, it is usually a period of tightening money, which means that although the bank's debt side cost increases, the asset side cost increases more, which can correspondingly expand the bank's net interest margin. Historically, the overall net interest margin (average) of the banking industry is highly matched with the central bank's benchmark interest rate, and the expansion space of the bank's net interest margin is limited when the central bank maintains the benchmark interest rate unchanged. As far as the current overall net interest margin of the banking industry is concerned, the 2.07% interest margin has reached the limit. In the future, if banks want to continue to improve their profit growth, they need to continue to increase the growth rate of asset scale.

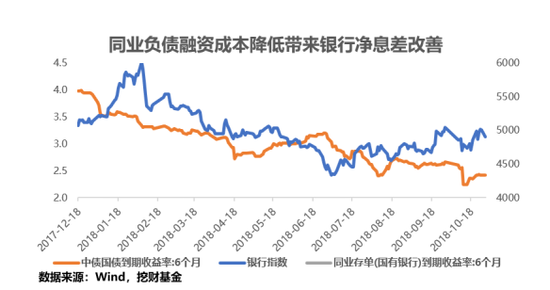

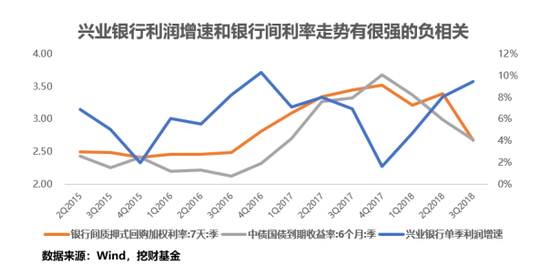

The net interest margin of the banking industry in the third quarter was due to the sharp reduction of interbank debt costs In particular, the second half of 2017 was particularly painful for joint-stock banks with high dependence on interbank debt. The average net interest margin of joint-stock banks in the first three quarters of 2017 reached 2.16%, while the 2017 annual report showed that the average net interest margin fell to 1.956%, which means that the net interest margin of joint-stock banks in the fourth quarter narrowed significantly, dragging down the annual net interest margin. Therefore, the performance of joint-stock banks in this round has improved most significantly. With "the king of the industry" Industrial Bank For example, the proportion of interbank liabilities (including interbank deposit receipts) is still high, which is 40.2% Benefiting from the decline of money market interest rates, the cost of interbank debt fell from the high point at the beginning of the year, and the interest margin expanded from 1.78% of the mid report in 2018 to 2.09%, which brought about a significant improvement in the third quarter earnings of Industrial Bank. Since 2015, there has been a strong negative correlation between the net profit growth rate of Industrial Bank and the inter-bank interest rate. The 2.27% net interest margin of Industrial Bank in the first three quarters of 2017 is also the extreme value of this cycle. In the short term, the expansion space of the net interest margin of Industrial Bank is limited.

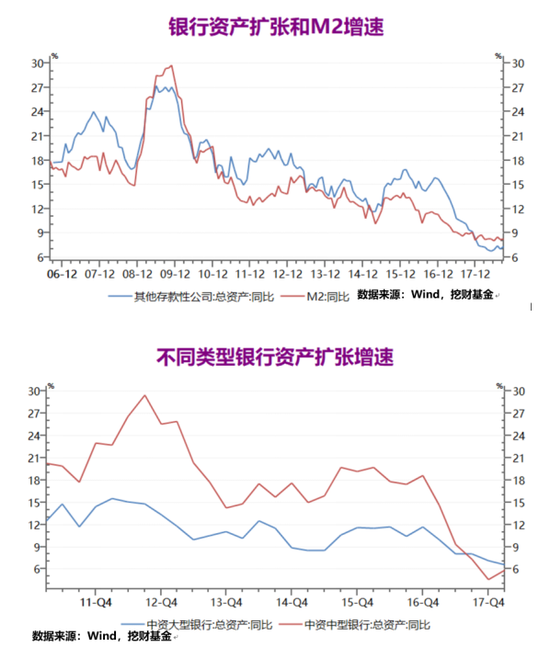

secondly , Bank asset expansion speed and M two The growth rate is highly correlated. Under the financial deleveraging, banks open off balance sheet businesses to shrink the balance sheet, while on balance sheet businesses are subject to capital and M PA assessment Constraints cannot complete non-standard business 。 Due to weak deposit growth, the year-on-year growth rate of bank deposit balance in September remained low (8.5%), and the expansion of assets on and off the bank balance sheet was constrained. Financial stability and reduced risk appetite for economic downturn were the core constraints on the expansion of the banking balance sheet. The growth rate of assets of the four major banks is obviously faster than that of joint-stock banks, Industrial and Commercial Bank of China and agricultural bank The growth rate of total assets reached 9.44% and 8.5% respectively, and the capital adequacy ratio was 1 4.8% And 15%, while joint-stock banks continue to reduce the proportion of broad interbank liabilities, and the highest growth rate is Everbright Bank and Ping An Bank The asset growth rate was 8.1% and 6.8%, and the capital adequacy ratio was 12.69% and 11.7% respectively. As large commercial banks have more retail outlets, their stable source of low debt is an important support for their debt expansion, while joint-stock banks are restricted by the continuous compression of non-standard and the assessment of interbank business on the liability side, and their asset liability expansion is limited 。

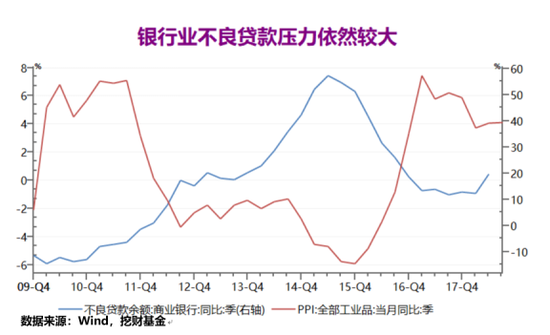

last , P PI Downward pressure increases, and the banking industry will still face bad debt pressure in 2019 。 The continuous rise of non-performing loans will have a double squeeze on the growth of bank net profit and valuation. On the one hand, the continuous rise of non-performing loans will increase bank write off efforts, increase the provision provision and erode bank profits, and on the other hand, it will depress the overall valuation of the banking industry. The year-on-year growth rate of non-performing loans in history and P PI There is a strong negative correlation between , reflecting the pro cyclical characteristics of the banking industry. As industrial products benefited from the sharp rise in the price of supply side reform, the growth rate of non-performing loans in the banking industry declined. However, due to the current high price of industrial products and the diminishing marginal effect of supply side reform, the year-on-year growth rate of industrial products prices will continue to slow in 2019, and the sustainability of the growth rate of industry profits will decline, although it will not be turned into non-performing loans immediately in the short term, But it will put pressure on bank valuation.

In terms of different banks, state-owned banks are the banks that have benefited the most from this round of supply side reform. However, it cannot be ignored that the leverage ratio of China's enterprise sector has ranked among the top in the world. According to the central bank's report, the high leverage of state-owned enterprises and local implicit debt are still the source of China's financial risks in the future 。 According to the 2018 China Financial Stability Report of the People's Bank of China, 2 At the end of 2017, the leverage ratio of the enterprise sector was 163.6%, Among them, the leverage ratio of state-owned enterprises is high, as of At the end of 2017, China's scale The average asset liability ratio of state-owned industrial enterprises reached 60.4%, negative compared with all industrial enterprises above designated size Higher debt ratio four point nine % Measures must be taken to effectively prevent and resolve the debt risk of state-owned enterprises. At the same time, the central bank also gave examples The implicit debt balance of X province is 80% higher than the explicit debt. Implicit debt grew rapidly and in a large scale , debt maturity mismatch risk is large, and there is guarantee chain risk.

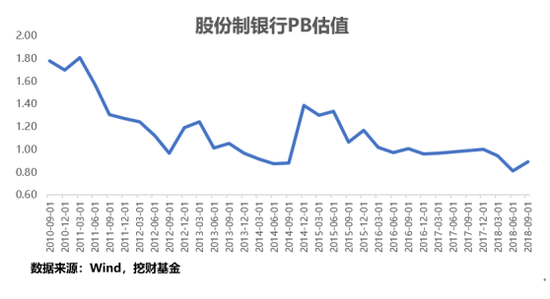

In the short term, joint-stock banks still have the highest performance flexibility Its overall valuation is at the historical bottom (P B 0.81), the interbank debt end cost reduction brought by the central bank's continuous reduction of reserve ratio can support the profit growth of joint-stock banks in the fourth quarter, and the strong credit demand under the continued compression of shadow banks' scale has certain support for pricing. In general, the large probability of interest margin will still rise steadily, and its valuation also has room for improvement. However, both the growth capacity and valuation space of joint-stock banks have obvious ceiling, and the large state-owned banks have shown better growth than joint-stock banks in the first three quarters of 2018 The valuation of joint-stock banks obviously cannot exceed P B =1. With reference to ICBC, the valuation of joint-stock banks is likely to be restored to 0.9 times and will be ended.

In the medium term, the fundamentals of large state-owned banks are healthier, their capital adequacy ratio is higher, their asset quality is relatively higher, they have more room for expansion in interbank business, and their more stable operation can withstand the pressure of future economic downturn In addition, under the stock game, all walks of life are concentrated to the head. In addition to the above advantages, state-owned banks enjoy more preferential policies. Taking debt to equity swap as an example, the five major state-owned banks of China Construction Communications Industry and Agriculture Corporation and their subordinate debt to equity implementing agencies have comparative advantages in market-oriented debt to equity swap business.

(The author of this article introduces: Doctor of Economics, director of investment research of Digging Fund.)