Article/Dai Zhifeng, Lu Jie, columnist of Sina Financial Opinion Leader (WeChat official account kopleader)

The consumer finance industry is obviously cyclical, and the risk is often caused by the stimulus policy after the financial crisis. From several cases in Asia, the development path is basically the same. After the 1997 financial crisis, the government issued policies to stimulate consumption, relax the supervision of consumer finance, increase the number of participating institutions in the consumer finance industry, excessive competition, excessive issuance of credit cards, lagging supervision, and finally led to the outbreak of bad debt rate.

Core viewpoints

Analysis of the current development of consumer finance: 1. In 2017, the growth rate of personal short-term consumer loans of banks accelerated and has stabilized since this year, with the current scale of 7.8 trillion yuan, accounting for 17.4% of personal loans, which is generally controllable. 2. The number of credit cards issued increased significantly in 2017, and fell back in the first half of 2018. The growth of credit card quota and loan balance was relatively stable. In the past two years, the quota utilization rate has basically remained around 43% - 44%. The quality of credit card assets was generally stable. The growth rate of the balance of overdue loans has continued to decline in the past two years, and the proportion of overdue loans has also declined steadily, the latest proportion being 1.21%. 3. The performance of licensed consumer finance companies is significantly differentiated. Among the 12 consumer finance companies that announced their operations in the first half of 2018, 9 achieved profits. As consumer finance companies are still in the early stages of development, there are significant differences in opening time and business progress. 4. Internet consumer finance is most affected by regulatory policies and changes in the market environment. The introduction of cash loan regulatory policies, P2P explosion and bank credit contraction have had a great impact on the Internet consumer finance industry, and the overdue rate has risen significantly in the short term; At the same time, the loan approval rate of each platform dropped significantly, and the growth rate of scale fell back.

A lesson from the past: The consumer finance industry is obviously cyclical, and the risk is often caused by the stimulus policy after the financial crisis. Japan, South Korea and Taiwan have all experienced the outbreak of credit card risk, and the development path is basically the same. After the financial crisis, the government issued policies to stimulate consumption and relax the supervision of consumer finance. The number of participating institutions in the consumer finance industry increased, excessive competition, excessive issuance of credit cards, and lagging supervision led to the outbreak of bad debt rate.

At present, China does not have the conditions for a large-scale outbreak of non-performing loans: 1. Financial regulatory environment: finance is in the regulatory cycle, not the innovation cycle. The risk appetite of financial institutions is on the decline channel. 2. Credit business data: there is no continuous card issuance and high growth rate of loan balance, and the growth rate of credit balance is slower than that of card issuance, and there is no widespread over consumption. 3. Penetration rate of consumer finance: China has a large population base. At present, the per capita number of cards is 0.46, and the leverage ratio of residents is relatively low.

The current problem: the debt sharing ratio. The failure to grasp the overall debt situation of borrowers is a major problem faced by consumer finance business. The improvement measures include: (1) Accelerating the construction of credit infrastructure, managing the license of companies engaged in lending business, and integrating their credit data into a unified system. (2) Establish a reasonable and effective regulatory framework for consumer finance business, provide appropriate guidance for loan interest rates and loan lines, make clear requirements for collection behavior, and establish a punishment mechanism for dishonest people. Create a market-oriented development environment for the consumer finance industry under the general framework.

Risk warning: Macroeconomic downturn, credit data integration was less than expected, and the leverage ratio of residents continued to rise

preface

Consumer finance has flourished in the past few years. Internet consumer finance has grown from scratch, greatly increasing the penetration rate of consumer credit and expanding the audience of financial services. Commercial banks accelerated the transformation of retail business and vigorously developed short-term personal loans and credit card business. In the trend of rising leverage of residents, the quality of personal consumption credit assets has attracted attention.

Classification of consumer finance: (1) According to business entities, it mainly includes commercial banks, licensed consumer finance companies, auto finance companies, e-commerce platforms, P2P platforms, small loan companies, etc. (2) By product, it mainly includes short-term consumer loans, credit cards, shopping installments, cash loans, etc. (3) From the perspective of business model, offline is mainly consumer loans with large amount and long loan cycle, while online is mainly small and short-term loans.

Analysis of the current development of consumer finance

Bank personal loan business: limited scale of short-term consumer loans

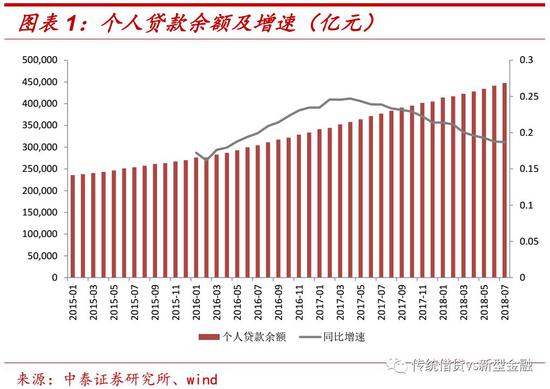

The balance of personal loans of financial institutions grew rapidly, and the growth rate slowed down. As of July 2018, the balance of domestic RMB personal loans of financial institutions was 44.76 trillion yuan, with an average growth rate of about 21% in the past three years. Since 2017, the monthly growth rate has continued to slow down. In terms of structure, medium and long-term consumer loans (mainly real estate mortgage loans) accounted for the highest proportion, reaching 60.9%, followed by short-term consumer loans (including credit cards and consumer finance), accounting for 17.4%. Therefore, the scale of personal short-term consumer loans of banks is 7.8 trillion yuan.

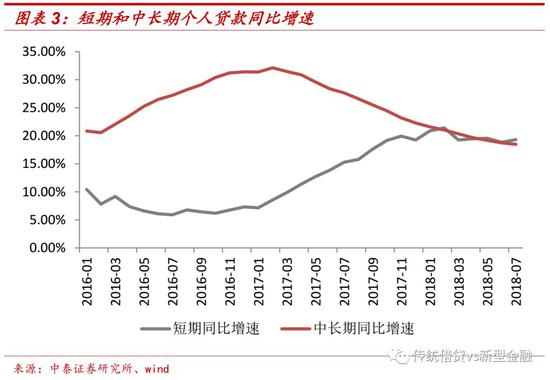

The growth of personal short-term loans accelerated. On the whole, the growth rate of medium - and long-term loans continues to be higher than that of short-term loans. From the end of 2016, the balance of personal short-term loans began to accelerate growth, and the growth rate of personal medium and long-term loans fell back. At present, the growth rate of the two is converging. In general, the proportion of short-term loans is less than 30%; The proportion of consumer loans has continued to rise, approaching 80%.

Credit card: the number of cards issued soared, the loan balance grew steadily, and the quality was stable

The number of credit cards issued increased significantly in 2017, and fell back in the first half of 2018. As of June 2018, the number of credit cards in use and issued reached 638 million, and the number of cards held per capita was 0.46. In 2016, the number of new credit cards in use was 33 million, while in 2017, it reached 123 million, significantly accelerating the issuance of cards. The reasons include: (1) The bank's retail business transformation has strengthened the development of retail business, and the credit card business has become an important focus; (2) The rise of Internet consumer finance has accumulated consumer finance customers and credit data in the long tail market. The bank has adjusted its credit card business strategy, expanded access to Internet channels, integrated big data credit into the risk control model, and harvested high-quality consumer credit customers. In the first half of 2018, the speed of card issuance slowed down, with 50 million new cards issued, compared with 55 million in the same period last year.

The growth of credit card quota and loan balance was relatively stable. As of June 2018, the total credit card limit was 13.98 trillion yuan, the used limit was 6.26 trillion yuan, and the line utilization rate was 44.78%. Since 2013, the growth rate of total credit card lines and loan balances has been close and stable, basically maintaining around 30%; The credit utilization ratio has increased from 37% at the beginning of 2013 to 45%. In the past two years, the credit utilization ratio has basically remained at about 43% - 44%.

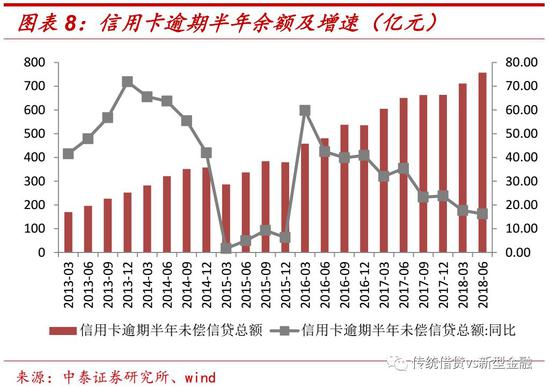

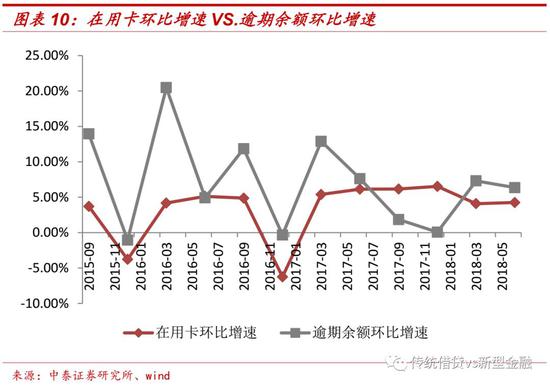

The quality of credit card assets was generally stable. As of June 2018, the balance of credit card loans overdue for half a year was 75.667 billion yuan. The growth rate of the balance of overdue loans continued to decline in the past two years, and the year-on-year growth rate in the first two quarters of 2018 fell back to below 20%. The proportion of overdue loans also declined steadily, with the latest proportion being 1.21%. From the quarter on quarter data, the growth rate of overdue balance is basically positively related to the growth rate of cards in use. However, in 2017, card issuance accelerated, but the overdue rate did not rise but fell. The outbreak of cash loan business may be an important reason. The increase in financing supply has also become a source of funds for credit card repayment. Since the issuance of the cash loan regulation document in November 2017, the overdue credit card has significantly improved, and the impact of cash loans has gradually eliminated.

Distribution of consumer finance business of various banks

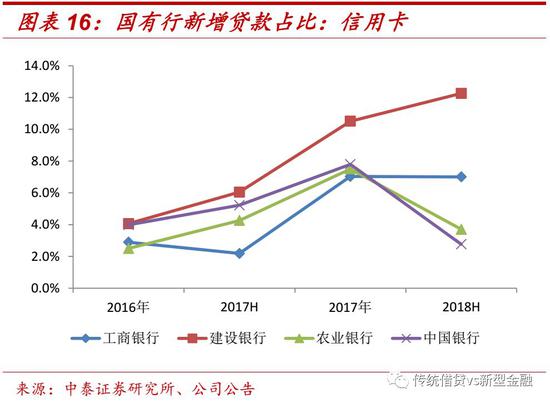

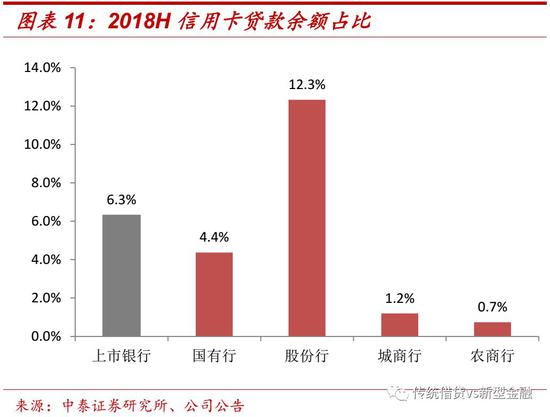

Credit card business is mainly concentrated in joint-stock banks and state-owned banks. In terms of the proportion of loan balance, joint-stock banks account for the highest proportion of credit card loans, followed by state-owned banks. Rural commercial banks and urban commercial banks account for a relatively small proportion of credit card business. Among all listed banks, Ping An Bank 、 Everbright Bank and China Merchants Bank The balance of credit card loans accounted for the top three.

Rural commercial banks and urban commercial banks have a high proportion of personal consumption and operating loans. In terms of the proportion of loan balance, state-owned banks, joint-stock banks, urban commercial banks and agricultural commercial banks increase in turn. The main reason lies in the high proportion of small and medium-sized banks and regional banks serving small and micro enterprises and individual businesses. Their short-term retail loans include small and micro financial businesses.

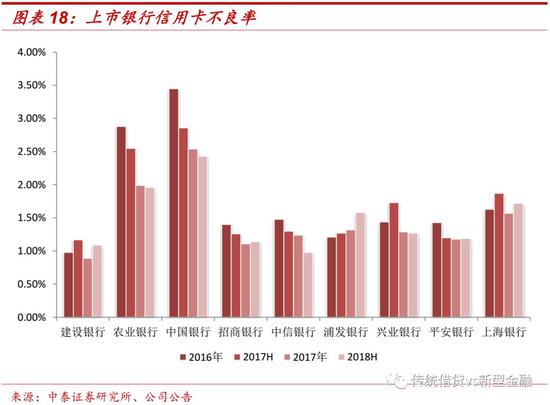

The quality of assets is relatively stable, and business growth is flexibly adjusted. On the whole, the proportion of credit cards in new loans increased significantly in 2017. In the first half of 2018, the proportion of credit cards in new loans of joint-stock banks dropped significantly.

The quality of assets is stable. Some listed banks have announced the non-performing rate of credit card business. On the whole, the non-performing rate of credit card business is controlled at a low level, with an average of less than 1.5%. Relatively high reject rate agricultural bank and Bank of China In recent three years, the non-performing rate has been continuously improved.

Licensed consumer finance companies: obvious differentiation of performance, steady operation and success

Performance differentiation is obvious. At present, there are 22 licensed consumer finance companies in operation, including 19 banks, accounting for 86%. Among the 12 consumer finance companies that announced their operations in the first half of the year, 9 made profits, and Zhaolian Consumer Finance and Instant Consumer Finance were among the first echelons in the industry. As consumer finance companies are still in the early stage of development, there are large differences in opening time and business progress, and the level of profit margin is uneven.

The industry has experienced a painful period. After the explosive growth of consumer finance from 2016 to 2017, industry risks gradually emerged. With the strengthening of supervision of the consumer finance industry and the rectification of cash loan business by the regulatory authorities, a large number of small and medium-sized platforms were eliminated naturally, and other platforms were affected to varying degrees. The overdue rate and non-performing rate increased, and the loan growth slowed down. After a large number of P2P platforms and small loan companies withdrew from the consumer finance market, the industry concentration has increased, and the vicious competition has decreased. The consumer finance company with sound operation is expected to win in the long run.

The advantages of the scene are prominent. Whether it is installment business or cash loan business, obtaining customers from scenarios is the core competence of consumer finance. On the one hand, it can effectively obtain target customers and reduce fraud risk; On the other hand, it is helpful to the structural design and pricing of credit products and reduces credit risk. In addition to capital cost advantages, bank shareholders can provide risk control models and outlet customer resource support, and industrial shareholders can provide rich online and offline consumption scenarios. On this basis, they can strengthen their own operational capacity and risk control capacity, and the sustainable development of the consumer finance industry is expected.

Internet consumer finance: industry shuffle, the rest is king

It is most affected by changes in regulatory policies and market environment. Non licensed institutions carry out Internet consumer finance business mainly including e-commerce platform, P2P platform and other models. Their service objects focus on the sub optimal population, and the service content is complementary to financial institutions. On the whole, the risk appetite of this part of consumer finance business is high, the asset quality is relatively lower than the assets on the bank's balance sheet, and is vulnerable to changes in the external environment. In the past year, the introduction of cash loan supervision policy, P2P explosion and bank credit contraction have had a great impact on the Internet consumer finance industry, and the overdue rate has risen significantly in the short term; Compared with the previous two years, the loan approval rate of each platform has dropped significantly this year, leading to a slowdown in the growth of business scale. According to the recent industry survey, the overdue situation is no longer deteriorating, and the industry development is expected to slowly recover from the trough.

Industry change trend: (1) The source of funds is institutionalized. Leverage ratio and capital requirements constrain the development scale of the platform. More and more Internet consumer finance businesses directly connect with the funds of banks, trusts, licensed consumer finance companies and other financial institutions. Institutionalized sources of funds can also reduce the compliance risk of consumer finance business. (2) Return to the scene. The cash loan business that purely covers high risks through high interest rates will disappear. From the perspective of customer acquisition and risk control, the regression scenario is the main development direction of consumer finance. Compared with banks' on balance sheet assets, Internet consumer finance has advantages in pricing flexibility.

warning taken from the overturned cart in front

Taiwan: Card debt crisis in 2005

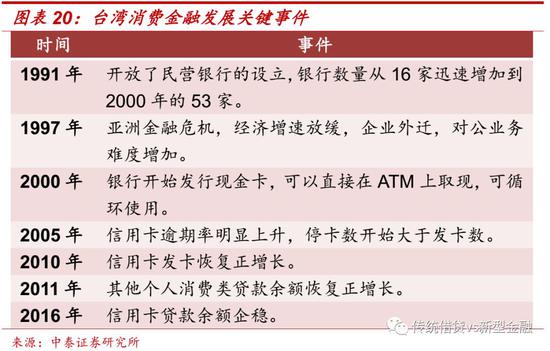

Development history: Taiwan's consumer finance business entered a period of rapid development from 2000. It reached its peak in 2005. The industry risk broke out and the overdue rate rose rapidly. According to the statistics of the "Monetary Authority" in February 2006, 520000 people became "card slaves", with an average overdue amount of NT $300000 per person. It was not until 2010 that credit card issuance resumed its positive growth. In 2011, the balance of other personal consumption loans began to rise, and in 2016, the balance of credit card loans stabilized.

Risk explosion. (1) The number of circulating cards peaked in October 2005, reaching 457 million, and the number of cards held per capita exceeded 2. In October 2005, it became a watershed. After that, the number of credit cards suspended each month was more than the number of cards issued, and it lasted for 26 months. Until December 2007, there was a time when the number of cards issued was more than the number of cards suspended, and then there was a negative growth in the number of cards for 28 months. After May 2010, credit card issuance really resumed. (2) The balance of credit card and other personal consumption loans also reached the maximum in October 2005. The balance of credit card loans has continued to decline, from NT $467.1 billion to more than NT $100 billion; The balance of other personal consumer loans fell from more than NT $10 trillion to more than NT $600 billion, and slowly recovered from 2011. (3) The overdue rate of more than three months exceeded 3% in 2006, and banks wrote off a large number of bad debts of credit cards. The amount of bad debts written off by most credit card issuing banks in 2016 exceeded 30% of credit card income. It takes many years for banks to recover from substantial profits to substantial losses.

Cause analysis: (1) Macro environment: After the financial crisis, the government hopes to stimulate consumption to stimulate economic growth. (2) Banking: it is difficult to do corporate business due to the relocation of enterprises; A large number of private banks have opened, and industry competition has intensified. (3) Business level: lowered the threshold for credit card application, increased the credit line, and reduced the minimum repayment amount. The hype misleads excessive consumption, and attracts low - and middle-income young people to apply for credit cards and spend in advance through various preferential activities.

Solution: (1) Establish a debt negotiation mechanism platform, requiring the banking industry to actively contact the debtor for negotiation, and stop collecting during the negotiation. (2) Once the excess ratio of double cards exceeds 2.5%, the bank will be ordered to stop issuing new cards. (3) It is stipulated that the interest rate information shall be disclosed in the double card agreement, and the double card interest rate shall be calculated as simple interest. (4) The maximum amount of bank double card and credit loan is 22 times of the borrower's monthly income. (5) Increase the minimum repayment amount of credit card to 10%. (6) Implement differential interest rates. (7) It is prohibited for banks to delegate collection and improper collection. (8) The "Sunshine Asset Management Company" was established, and the bank can invest the double card creditor's rights of middle and low income households into shares for processing. (9) Commission of Labor is entrusted to cooperate with social welfare units to actively contact unemployed debtors and provide job opportunities. (10) Promote financial knowledge education. (11) Standardize advertising marketing.

South Korea: 2002-2004 credit card crisis

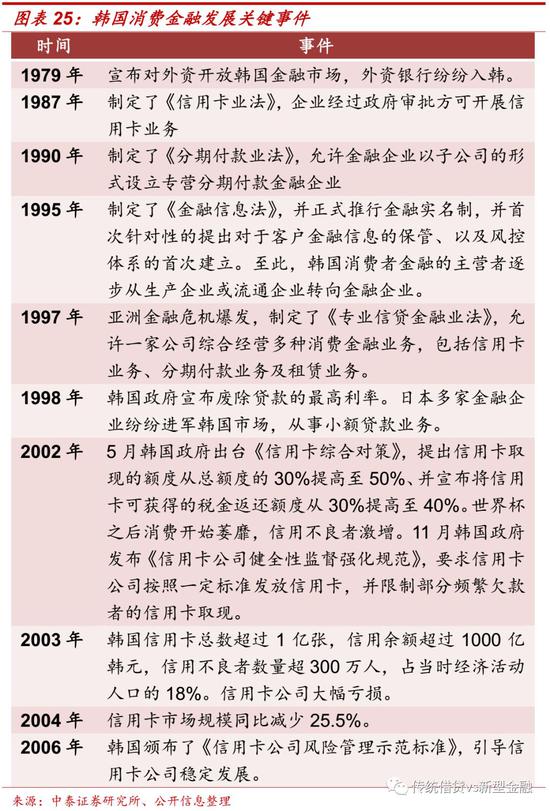

Reasons for the credit card crisis: (1) Excessive policy relaxation leads to excessive credit card borrowing. Specific policies include lowering the threshold for card application, increasing the credit line, tax reduction policies, promotions and lottery activities. The policy encourages credit card business, which leads to unfair competition among card issuers, leads to excessive consumption of consumers, and the debt ratio rises rapidly. (2) The credit system is not perfect. At that time, South Korea had not yet established a complete, timely and shared personal credit database, which led to loopholes in the risk assessment of borrowers by card issuers. The total debt ratio climbed and the risk increased.

Improvement measures: (1) Strengthen the supervision of credit card business, guide credit card companies to operate steadily, and formulate standards for threshold requirements for card handling, loan limit setting, rate setting, overdue debt resolution measures, collection and disposal of non-performing assets. (2) Improve social credit infrastructure. For individuals with accounts of multiple financial institutions, it is required to share information through the platform of the Banking Federation and credit investigation institutions, including their bank card information, income and arrears records. Credit agencies score and grade personal credit. In addition to financial institutions, they also access the data of communication companies, power companies, medical insurance and other systems.

Development enters the mature period: After the clearing of credit card risks in 2005, credit card transactions resumed their sustained growth. In 2011, there was a significant increase in the number of credit cards issued, but this time there was no large-scale outbreak of non-performing rate. Although the non-performing rate rose, it was limited, and soon declined. The regulatory authorities have accumulated experience and introduced more timely and detailed policies.

Japan: The Rise and Fall of Consumer Finance

Development history. Japan's consumer finance development has been closely linked with the commercial circulation industry since the beginning. The target customer group has real consumer demand, financial services and commodity sales complement each other, and has advantages in risk control mode. After the gradual deregulation of the regulation, consumer finance companies gradually lent to the subprime group, which led to the rise of non-performing rate and serious problem of violent collection. Finally, strong supervision shuffled the industry and a large number of consumer finance companies withdrew from the market.

Membership based credit reporting system. The government does not directly participate in the construction of the credit reporting system, but improves the relevant laws, clarifies the regulatory requirements for credit reporting agencies, protects the legitimate rights and interests of consumers, and promotes the development of the credit reporting industry in a market-oriented manner. Personal credit information institutions in Japan can generally be divided into banking system, consumer credit system and sales credit system, corresponding to banking industry association, credit industry association and credit industry association respectively. Members of these associations include banks, credit card companies, insurance companies, other financial institutions, commercial companies and retail stores. All industry associations have become the main body of the construction of the credit information center, and provide individual and enterprise credit information exchange platforms for association members to collect and use through the internal credit information sharing mechanism.

Strong supervision brought about industry reshuffle, and a large number of consumer finance companies went out of business and went bankrupt. (1) Interest rate restrictions. The upper limit of interest rate was reduced from 29.2% to 20%, in which the interest included all fees except the principal, such as service fees and cash gifts. The maximum annual interest rate for loans below 100000 yen is 20%, the maximum annual interest rate for loans below 1 million yen is 18%, and the maximum annual interest rate for loans above 1 million yen is 15%. (2) The loan balance of the borrower shall not exceed one third of the total annual income, or new borrowing will be prohibited. (3) The borrower is allowed to claim more than 20% of the interest of the previous loan from the consumer finance company. It is this policy that has led to the bankruptcy of a large number of consumer finance companies.

Conclusion: The probability of systematic risk occurring in the short term is not high

Analysis on the Causes of Risk Outbreaks in the Past Consumer Finance Industry

The consumer finance industry is obviously cyclical, and the risk is often caused by the stimulus policy after the financial crisis. From several cases in Asia, the development path is basically the same. After the 1997 financial crisis, the government issued policies to stimulate consumption, relax the supervision of consumer finance, increase the number of participating institutions in the consumer finance industry, excessive competition, excessive issuance of credit cards, lagging supervision, and finally led to the outbreak of bad debt rate.

Relaxed monetary environment: After the financial crisis, the government took active monetary policies to stimulate the economy, creating a broad monetary external environment, and financial institutions have abundant borrowing funds. Consumption is an important driving force to stimulate the economy, which is stimulated by residents' leverage.

Radical stimulus policies: The regulatory authorities have relaxed the restrictions on credit card business. First, they have increased the number of business entities that can carry out credit card business, including opening business permissions to foreign financial institutions. Second, they have forced the retail industry to accept credit card payment methods, expanded the use of credit cards, and provided preferential tax policies for credit card transactions. In addition, it gives autonomy to set the interest rate level and interest calculation method of credit cards.

The vicious competition in the industry: The growth of corporate business was weak. All banks focused on retail business, and credit cards became the key layout direction. In order to compete for customers, various banks launched various advertising and promotional activities to attract card application. In addition, they lowered the threshold for card application. They did not review the qualification and repayment ability of customers. They could apply for cards as long as they had ID cards or other bank credit cards. The loan limit often exceeds the repayment capacity of the cardholder.

There is no condition for a large-scale outbreak of non-performing loans

Financial regulatory environment: Finance is in the regulatory cycle, not the innovation cycle. The general direction of deleveraging and breaking the rigid conversion is relatively certain, and the risk appetite of financial institutions is in a downward channel. Although consumer finance is encouraged by policies, there is no excessive policy.

Credit business data: There is no continuous high growth rate of card issuance and loan balance, and the growth rate of credit balance is slower than that of card issuance. There is no widespread over consumption. The rise of non-performing ratio is mainly caused by cash loan supervision. At present, the impact has been gradually eliminated, and the non-performing ratio is low.

Penetration rate of consumer finance: In countries or regions where the credit card crisis broke out, the number of credit card holders per capita often exceeded two, and the proportion of excessive credit card holders was high. China has a large population base. At present, the per capita number of credit cards is 0.46, and the leverage ratio of residents is relatively low.

Existing problems and improvement measures

The current problem: the debt sharing ratio. The failure to grasp the overall debt situation of borrowers is a major problem faced by consumer finance business. The credit data of financial institutions are included in the credit investigation of the Central Bank, while the lending data of a large number of P2P platforms and Internet consumer finance platforms cannot be obtained directly, so the relevant institutions can only indirectly speculate on the borrower's debt sharing situation. On the one hand, this increases the credit investigation cost of consumer financial institutions, which requires access to multiple credit investigation data for cross validation. On the other hand, it also reduces the accuracy of the pricing model, which makes it impossible to price individuals differently.

Improvement measures: (1) Accelerate the construction of credit infrastructure, conduct license management for companies engaged in lending business, and then incorporate their credit data into a unified system. At present, the judgment of the debt sharing ratio is mainly obtained through indirect means, including calling third-party data or extrapolating through call records. However, the quality of third-party data is uneven, and the feasibility is low. Lending institutions often need to call multiple data sources for cross verification, leading to increased credit reporting costs, but the effect is still not guaranteed. (2) Establish a reasonable and effective regulatory framework for consumer finance business, provide appropriate guidance for loan interest rates and loan lines, make clear requirements for collection behavior, and establish a punishment mechanism for dishonest people. Create a market-oriented development environment for the consumer finance industry under the general framework.

Risk warning

Macroeconomic downturn, credit data integration was less than expected, and the leverage ratio of residents continued to rise

(The author of this article introduces: Chief of the banking industry of Zhongtai Securities, head of the financial team, and a special researcher of the National Finance and Development Laboratory.)