Article/Li Qilin, columnist of Sina Financial Opinion Leader (WeChat official account kopleader)

When microenterprises encounter asset securitization, when two encouraged policies are combined, and when two instruments can expand credit simultaneously and can be used together, the power of this combination will be huge.

History is always in a continuous cycle, from deposit and loan to interbank and then back to deposit and loan, from debt shortage, asset shortage to asset liability shortage, and then to debt shortage, banks are in the cycle of economic cycle, as well as in the cycle of business and asset scarcity.

At present, China's economy is in a downward cycle, and the profits of enterprises are down, but credit is rigid. There is pressure to borrow new money to repay the old, and enterprises need money. On the other hand, the economic downturn and superimposition of regulatory "deleveraging" have blocked many flow channels of funds, slowed down the flow rate and slowed down the credit expansion. This is one of the reasons why the central bank continues to reduce reserve requirements and release water. We still feel that there is not much money. As the largest financier in the financial market, the bankers have no more money left, and begin to "run out of debt".

For banks, on the one hand, the slowdown of credit expansion and the marketization of interest rates have raised the cost of capital of banks. In order to attract deposits, after the financial management was standardized, the structural deposit interest rate as a supplement could once reach 5% or even higher. On the other hand, such high interest rates can no longer be outsourced to require the non bank to just cash in, nor dare to allocate high-risk "non-standard" Urban investment and low rated credit bonds, standing at the crossroads of balance sheet and income statement, are in a dilemma.

Where is the way?

At this time, some small and medium-sized banks developed a decentralized and fast turnover model of "microenterprise+asset securitization", a tool to increase liabilities and assets at the same time.

When microenterprises encounter asset securitization, when two encouraged policies are combined, and when two instruments can expand credit simultaneously and can be used together, the power of this combination will be huge.

From the perspective of liabilities, "microenterprises+asset securitization" can increase the sources of bank liabilities, vigorously develop the microenterprises and retail businesses that were less involved in the past, expand the debt boundary, and allow credit funds to be realized and returned in advance through asset securitization financing.

From the asset side, the combination of "microenterprise+asset securitization" has three main advantages. The first is that asset securitization can realize the assets lacking liquidity in advance, improve asset liquidity and divert credit lines. The second is to realize the balance sheet of assets, reduce the capital occupation and improve the capital adequacy ratio. The third is to spread risks and reduce potential non-performing rate. However, most investors are commercial banks. In fact, the credit risk is still circulating in the banking system, coupled with insufficient liquidity, and even the phenomenon that banks buy each other to make statements.

This article is mainly divided into three parts. The first part is to learn the specific model of "microenterprise+asset securitization" based on Chinese and foreign cases. The second part calculates how "microenterprise+asset securitization" realizes credit expansion and reduces loan costs. The third part describes the circulation mode and asset requirements of asset securitization in the field of small and micro businesses in China.

one 、 What does the bank do?

(1) Changed from "approval system" to "filing system", and asset securitization flew into ordinary small and medium-sized banks

In 2014, the CBRC issued the Notice on the Filing and Registration Process of Credit Asset Securitization (also known as "1092 Document"), which changed the credit asset securitization business from "approval system" to "filing system".

The process of credit asset securitization of small and medium-sized banks is to submit to the CBRC for filing, register the quota in the central bank after obtaining the approval qualification, and then issue in the inter-bank market or exchange.

(2) Decentralized and fast turnover

How to do microenterprise+asset securitization? past Cost, risk and benefit are the "impossible triangle" of inclusive finance.

If we want low cost and high yield, we may have to face a high non-performing rate in the future. To achieve low risk, we need to spend a lot of manpower and material resources to do risk control, so it is not easy to control the cost, and it is also difficult to make profits. The pattern that banks cannot make money or even lose money is not sustainable. High yield is required. If the cost cannot be reduced, high interest rate will be used, which may exceed the prescribed upper limit of interest rate, and MPA supervision and assessment will fail.

Small and micro finance is really a dilemma, so the first problem to be solved in small and micro finance is to reduce costs while controlling risks.

two Traditional bank practices

Take Bank T as an example. As a city commercial bank, Bank T knows that it has many outlets and has no advantage in the positive competition with big banks with mature businesses. Therefore, at the beginning of its establishment, it took its own background advantage to focus on local small and medium-sized enterprises as its goal to compete differently with big banks. At the same time, Bank T is also exploring a characteristic "microenterprise+asset securitization" asset light operation road, becoming one of the earliest banks engaged in "microenterprise+asset securitization" in China.

The main pressure of Bank T is that it is difficult to absorb deposits as a small bank. In addition, under the "high price" mode of other banks to absorb funds, and then allocate "non-standard" with high returns, the cost of capital in the capital market has been raised very high. Microenterprise itself is a high cost business, in order to obtain funds and reduce costs The Bank actively seeks cooperation from other banks or financial institutions, and recycles the funds by means of securitization:

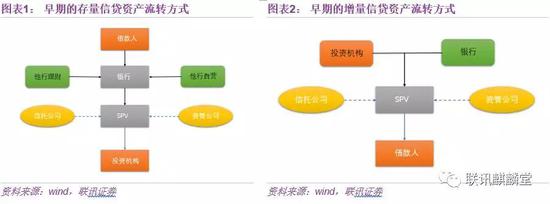

For the stock assets, the bank, together with other banks' wealth management and proprietary lending, or through trust companies and asset management companies, packs them into trust plans and asset management plans and sells them to investment institutions. Bank T needs to give out a part of the principal itself, occupy the bank's credit line, risk capital, etc., and then transfer out the statement to achieve the purpose of shifting the line and reducing capital withdrawal.

For incremental assets, the bank will introduce investment institutions to the front end, and use the funds of investment institutions to establish trust plans or asset management plans To release money directly, the bank only plays the role of loan management in this process. In essence, it is similar to collecting money from investment institutions. The bank is responsible for risk control, managing credit assets, and transferring the principal and interest paid by customers to investment institutions.

This article is mainly divided into three parts. The first part is to learn the specific model of "microenterprise+asset securitization" based on Chinese and foreign cases. The second part calculates how "microenterprise+asset securitization" realizes credit expansion and reduces loan costs. The third part describes the circulation mode and asset requirements of asset securitization in the field of small and micro businesses in China.

However, the above two models are offline private transactions, which are not standardized and transparent, and some problems have also been exposed in the process. For example, SPV is a horizontal transaction structure, and credit enhancement arrangements cannot be realized structurally. When the customer's creditor's rights are changed, the investors cannot be informed one by one, which causes difficulties in the later settlement. With the encouragement of policies and the establishment of asset circulation channels, now Bank T mainly transfers assets through asset securitization and registration with the Bank Registration Center.

The model of the Bank Registration Center is relatively simple. Bank T entrusts a trust company to set up a property rights trust plan, transfer the creditor's rights to the trust plan, and then list and transfer according to the process guidance of the Bank Registration Center, so as to delist and transfer the investment opportunities of interest.

In the asset securitization model, the bank entrusts the credit assets as trust property to a trust company to establish a special purpose trust. The issuer issues asset-backed securities with this special purpose trust, which is sold by the underwriter to investors. The credit assets in the trust property, as the underlying assets, will generate cash flow with the repayment of the borrower, It is used to repay the principal and interest of investors and pay various taxes.

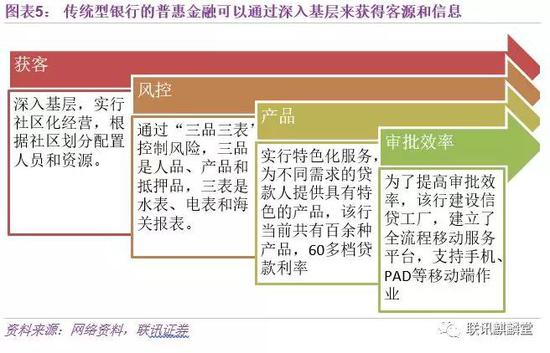

Specifically, in terms of small and micro finance, T Bank has its own unique advantages in terms of customer acquisition, risk control, products and approval.

Customer acquisition The Bank went deep into the grassroots, implemented community-based management, and allocated personnel and resources according to community division.

Risk control The risk is controlled through "three grades and three meters". The three grades are moral character, products and collateral, and the three meters are water meters, electricity meters and customs statements. For small and micro enterprises with incomplete information, life oriented indicators can be used to identify their business continuity and risk level. For example, water meters, electricity meters and customs statements can be used as tools to verify production capacity.

To increase the cost of customer dishonesty, Bank T has also set up its own credit system similar to the membership system, called "product". The bank rewards customers with "product" based on their deposits in the bank. When lending, the bank will give corresponding interest rate preferences based on the product of different customers, which not only realizes cross selling, but also effectively reduces risks and increases customer viscosity.

Product , implementing characteristic services and providing characteristic products for lenders with different needs. At present, the bank has more than 100 kinds of products, more than 60 loan interest rates, and implements one price for each household and one price for each transaction. For example, the "Chuangye Tong" loan involved in the conversion to small and micro enterprises and individual businesses has two main characteristics. The first is online revolving loan. After a credit extension, the borrower can "borrow and repay" before the maturity date. The second is flexible installment. Different industries have different off peak seasons. The bank can make different repayment plans according to each customer, paying more in the peak season and less in the off season, which is very humanistic.

Approval efficiency A credit factory has been built, and a full process mobile service platform has been established to support mobile terminal operations such as mobile phones and PADs, so as to facilitate the timely reporting and rapid approval of employees, and realize the reply of whether to grant loans to new customers within three days, the reply of whether to renew loans to customers within three hours, and the loan approval within three hours.

3. Practice of technology banks

In the newly released third quarter report, the bank showed outstanding performance with low non-performing and high growth performance, adhered to the strategy of light banking, and effectively promoted the efficiency of bank capital use. However, Bank N used the formal decentralized and fast turnover "microenterprise, consumption+asset securitization" model.

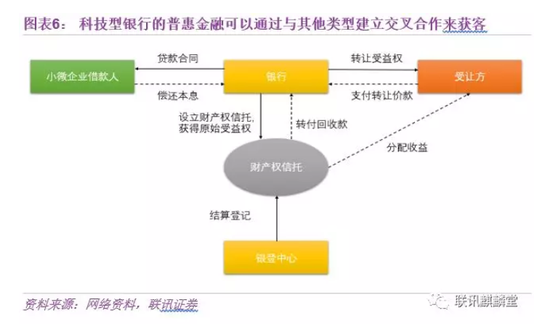

The main approach is that the bank first places a batch of microenterprise or consumer loans, and then entrusts these loans to the trust manager to establish a property rights trust to obtain the original beneficial right. Then the bank registers the transfer of the beneficial right in the bank and other centers, and the transferee pays the price to the bank after accepting the transfer. The bank transfers these credit assets to the investor, but still manages the credit in the property trust, transfers the principal and interest to the trust at the specified time, and then the trust distributes the benefit to the transferee. In this process, the funds returned by the bank are used to invest in microenterprises or consumer loans again.

In addition, in terms of microenterprises and consumption, in order to deal with the problem of high cost and high risk, the Bank used more scientific and technological means to achieve good risk control and cost reduction by increasing customer access channels and information sources.

Customer acquisition : Mining demand from internal and external multi-channel, using cross selling internally, and mining from the bank's customer base. External channels include procurement, data exchange, web crawler, credit information sharing with the National Information Center, establishing a white list database, and then distributing to local branches and sub branches for marketing according to the customer's geographical location.

In addition, it can also establish cooperation with other different types of platforms and find platforms similar to the target customers for cross cooperation, such as embedding the online tax hall of VAT taxpayers, so that tax filers can see the guidance information of the bank when handling taxes and enter the online bank to apply for loans.

Risk control After customers enter the loan application phase, they can submit personal and enterprise information online. Customers who have passed the bank card authentication can obtain online authorization and online approval in just a few seconds. Many of these elements, such as the determination of credit line and the generation of contracts, can be automatically generated through the database established by the bank, risk control model and system background, without manual intervention Reduce labor costs.

Product The bank also provides a flexible lending mode of "one-time approval and revolving lending", in which the borrower can repay and re borrow at any time within the credit line and validity period, accrue interest on a daily basis and settle interest on a monthly basis, saving financial costs for customers.

four Internet finance practices

As a bank under a technology giant, Bank W has unique data advantages and potential customers since its inception. However, as an online direct selling bank, Bank W has no physical outlets that do not obtain funds through deposit taking, so Bank W has three main ways to obtain funds. The first is to borrow money in the interbank market, such as issuing interbank deposit certificates. The second is to cooperate with other traditional banks, and the two sides issue loans in proportion. The third is to realize in advance and return funds through asset circulation.

Comparatively speaking, the circulation mode of registration and transfer of bank registration center is a relatively low-cost mode, which is also the most commonly used mode of Bank W.

The approach is similar to that of Bank N, the first step is that the bank forms credit assets after issuing loans to the borrower, and then establishes a property right trust, listing and transferring the trust beneficial rights, the investor delisted and transferred them, and paid the transfer price to the trust, and the trust transferred them to the bank. The bank is responsible for managing the borrower's funds, and transferring the principal and interest to the trust during the repayment period, The trust distributes the proceeds to investors. The financing obtained by banks in this process can be used again to make loans.

Bank W's technological means and N There are many similarities among banks, which we will not discuss in detail. However, in our research, we found that there is a supply chain type inclusive finance in Internet finance. These Internet platforms have both financial business and e-commerce business, which can realize full supply chain management from credit, purchase to sales, and can also introduce insurance institutions to further control risks.

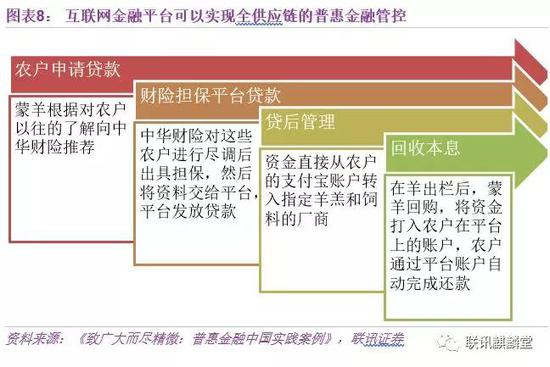

For example, Mengyang is a comprehensive farming and animal husbandry enterprise. One of its businesses is to purchase mutton sheep from farmers and then process and sell them. Farmers need to invest a lot of money to buy lambs and feed for raising sheep. Before, it was difficult for farmers to borrow money from formal channels without good collateral, which affected their productivity to a certain extent. In order to solve this problem, Mengyang has in-depth cooperation with a platform, Cooperate with China Property Insurance to provide loans and insurance for farmers.

The process is for farmers to apply for loans. Mengyang recommends to China Property&Casualty Insurance Co., Ltd. based on their previous understanding of farmers. China Property&Casualty Insurance Co., Ltd. will issue guarantees to these farmers after due diligence, and then submit the information to the platform for the platform to issue loans.

In the process of using the loan, when farmers buy lambs and feed, the funds are directly transferred from the farmers' Alipay account to the designated lambs and feed manufacturers. After the sheep are sold, Mongolian Sheep repurchases the funds into the farmers' accounts on the platform, and farmers automatically complete repayment through the platform account.

You can also put the finished mutton and other products on the e-commerce website of the platform for sale. Providing farmers with "one-stop" services from loans to purchases to sales can not only prevent farmers from misappropriating loans, but also control the whole process and realize capital return.

2 Why can asset circulation alleviate the problem of "difficult and expensive financing" of microenterprises?

(1) Capital cost without securitization

Capital source cost In 2017, the weighted average interest rate of interest bearing liabilities of listed banks was 2.25%. The source of funds for small and micro finance was the targeted RRR reduction by the central bank. Commercial banks put these money in the central bank with 1.62% interest. After the RRR reduction, the opportunity cost for banks to use as small and micro finance was 1.62%.

Capital provision cost Under normal circumstances, the risk of small and micro loans is higher than that of general corporate loans and retail loans. If the impairment provision of general corporate loans is 3% and that of small and micro loans is 5%, then the impairment provision of these two loans is 3 million and 5 million respectively.

As the operating cost of the bank, this provision for impairment is included in the operating expenses of the income statement, and the account is "asset impairment loss", which means that these losses have already been incurred by the bank, and we do not care whether they are reversed or written off later.

Accrued risk cost Risk capital shall also be withdrawn for the part deducting impairment provision. The withdrawal of loan risk of ordinary enterprises is 100%, and that of microenterprises and retail (personal consumption) is 75%. The cost of risk capital can be directly approximated by the cost of secondary capital bonds commonly used by small and medium-sized banks. About 6%.

The cost of venture capital is a concept of "opportunity cost". Let's compare it with 50% of housing mortgage loans. In this way, ordinary enterprise loans use 50% more capital in the provision of venture capital, and small and micro businesses use 25% (75% - 50%) more. Then the additional cost of enterprise loans and small and micro loans in the provision of venture capital is 2.91% (97% * 100% * 50% * 6%) respectively And 1.43% (95% * 25% * 6%). So the total capital cost of the bank is 8.2% and 8.15% respectively.

(2) Capital cost after securitization

The asset securitization mentioned above can reduce the capital source cost and risk accrual cost of banks.

Capital source cost : Since the money loaned in the second round was obtained from asset securitization, from the second round (the latter n-1 round), there was no source cost of the money (excluding ABS issuance costs), and it was not obtained by absorbing residents' savings or issuing certificates of deposit in the interbank market, so it was not subject to the restrictions of large deposit attraction competition and high interest rates on certificates of deposit.

Risk accrual cost : Because asset securitization can realize the statement making, once the assets are listed, risk capital will not be withdrawn, so except for the last round, the first and second rounds of lending funds have no risk cost withdrawn.

A total of 95 million yuan of small and micro loans and 95 million yuan of asset-backed securities were issued. The 95 million yuan raised from the issuance cost could be used again to issue loans. 90.25 million yuan (10000 * (1-5%) ^ 2) of loans could be issued after the second round of provision for impairment. Through the reciprocating cycle of "issuing loans - asset securitization - issuing loans", the maximum amount could be expanded to 2 billion yuan (1/5%), The largest scale that a fund can expand through asset securitization is the number of funds/provision , which is related to the provision. The less the provision, the more loans can be issued.

Asset securitization has realized credit expansion. However, the bank cannot completely use this cycle. If there are two securitizations and three rounds of loans, the total amount of loans will become 270 million. Under the two models, the cost of capital and average loan cost rate of each round are respectively:

After two rounds of asset securitization, the cost of capital has decreased from 8% to 6%, and the circulation of the balance sheet can effectively reduce the cost of bank capital.

If the reasonable profit is 2%, the market interest rate is 10.2% and 10.1% respectively, and if the loan is made according to the market interest rate, asset securitization can make the bank's profit rate jump from 2% to 11.5%.

If the banks engaged in asset securitization actively reduce interest rates, they will not only gain competitive advantages, but also significantly improve the high cost of financing for SMEs The credit expansion effect of asset securitization can alleviate the financing difficulties and expensive financing problems of SMEs at the same time.

three Does the market recognize the assets transferred by banks?

The combination mode of "microenterprise+asset securitization" has obvious advantages. What about the market situation of asset circulation?

Over the past 17 years, asset securitization of small and micro businesses and personal consumption loans in China has gradually increased. According to wind data, as of October 18, China had issued 227 ABS corporate loans, with a total amount of 950 billion yuan. In 2017, banks began to issue special asset-backed securities for loans to small and micro businesses. So far, three cases have been issued (actually more than this, but these three cases are specifically noted for small and micro businesses).

Among the three asset securitization projects, the smallest is 700 million, and most of the assets in the pool are hundreds of thousands, which is relatively dispersed. The priority interest rate is positively related to the weighted average interest rate of the underlying assets, which is 3% - 6% higher than the priority interest rate.

The asset securitization of microenterprises has gradually developed since 2015. In addition to banks increasing the issuance scale and increasing supply, investors are also more active on the demand side.

From the perspective of investors, in addition to the high interest rate, asset diversification and low risk mentioned above, investing in ABS has three advantages:

First, low occupation of venture capital Priority A is 20%, which is lower than 75% of microenterprises and personal consumption loans.

Second, liquidity is improving At present, the liquidity of asset securitization is not high, but fortunately, the term of microenterprises and personal consumer loans is not long, and the term of ABS with them as underlying assets is generally short. And with the policy encouragement, the liquidity of the secondary market is gradually strengthening, which is expected to be further improved in the future.

Third, asset securitization generally uses excess interest rate to prepay, and mezzanine is often upgraded to bring capital gains 。 According to wind data, of the 522 credit asset securitizations that have been downgraded in China since 2007, except for one that has been downgraded, the rest 521 have been upgraded, most of which are priority B for mezzanine files.

This is mainly because of the excess interest margin The excess interest margin is a credit enhancement measure, that is, the interest rate of the underlying asset is higher than the priority issuance interest rate and the tax sum of the trust. In order to ensure the loss of the underlying asset, the excess interest margin is first partially absorbed.

Taking the above * and the first phase of 2017 as examples, the weighted average interest rate of the underlying assets is 10.22%, which is 5.3% higher than the interest rate of priority A. After the payment of priority A interest and various taxes, the excess interest margin will first repay the principal of priority A. After being repaid in advance, priority B (AA+, interest rate 5.4%) will become essentially priority A (AAA, interest rate 5.3%) of the project, and then be upgraded.

The market price of Priority B of RMB 79 million increased to 79.075 million (7900 * (1+5.4%)/(1+5.3%)), and the capital gains increased by 75000 immediately.

Asset securitization is not the only way of asset transfer. All forms of transfer that can achieve the above advantages have the above advantages. Another way of asset transfer is the registration transfer of the Bank Registration Center.

Like asset securitization, the registration transfer of the Bank Registration Center can increase the liquidity of assets, reduce the capital occupation, and realize the double statement of accounting and supervision. Moreover, the registration transfer is shorter and cheaper than asset securitization.

There are five main steps for banks to participate in the transfer of bank registered assets: the first step is to open credit asset accounts and network access, the second step is to submit filing materials, the third step is to register the assets to be transferred, the fourth step is to handle the circulation of credit assets, and the fifth step is to settle credit assets.

At the end, we would like to remind that any model is not perfect, and any business that has been advocated for explosive growth may have unexpected drawbacks. We think that small and micro finance has several risks that need to be reminded: first, pay attention to risk control. According to the "impossible triangle" of inclusive finance that we mentioned, while vigorously supporting policies, human resources If technology fails to keep pace, the rapid growth of Pratt&Whitney may be at the cost of certain risks. Second, pay attention to the pledge rate and risk of the collateral. If the pledge rate is too high, the collateral will be easily exposed to risk. The collateral accepted by banks on a large scale should be low-risk, so as to avoid large-scale position closing stampede due to future value changes.

(About the author: Chief Economist of Lianxun Securities)