Article/Xue Hongyan, columnist of Sina Financial Opinion Leader (WeChat public account kopleader)

The spirit of openness should be advocated, but openness itself is not exciting. If the business itself is not competitive, it will still not be competitive after opening the API interface. Openness is just the beginning, and it is not success itself, which needs us to remember.

Following the opening steps of financial technology giants, recently, many banks have begun to build open platforms to open their own products and technological capabilities, enabling scenarios and peers. When openness becomes a trend at the industry level, follow the trend at the institutional level. The question is, is openness really a panacea?

How to open? Three open modes!

In the current industry context, the so-called openness of commercial banks can be roughly divided into three modes:

First, build a one-stop open platform. The open target is the same industry, and the high concept is called technology empowerment, covering customer acquisition, risk control, post loan and other aspects. Among them, the typical example is the joint loan promoted by various giants, which essentially opens up the asset capacity, opens up new growth space under the existing capital constraints, and successfully realizes the transition to the asset light model.

For example, the "Star Project" of online merchant bank, which opens its capabilities and technologies to the industry, plans to work with 1000 various financial institutions in the next three years to jointly provide financial services for 30 million microenterprise operators.

The second is to open financial service capacity. The open object is the traffic scenario, and the product is embedded in each scenario in the form of API (application development interface), which is essentially a new customer acquisition and diversion mode.

as Shanghai Pudong Development Bank The launch of API Bank (Boundless Open Bank), which encapsulates financial products such as "payment, equity preference and points" and service capabilities such as "market forecasting, risk assessment and data analysis", is open to various APP scenarios. In addition, the secure lending platform similar to the headline today is connected with the credit products of licensed institutions. From the perspective of licensed institutions, it is an opening of loan products.

On the whole, these two types focus on the ability to open assets, solve the problem of partial capital (such as joint loans), and focus on the ability to open financial products, solve the problem of partial assets (flow and customer acquisition). Capital and assets are two sides of the same coin. In a sense, these two kinds of openness are also two sides of the same ecology, just from different perspectives.

Traffic tycoons tend to open up their ability to attract customers to attract funds. For such institutions, the so-called opening is to build an open platform, while financial institutions that do not master the scene tend to access assets by docking with the scene. The opening is manifested in the opening of financial service capabilities, namely the so-called API bank.

The third is matchmaking mode. For many banks, they lack their own scenarios and are not typical funders. At this time, they can take another open road, that is, combine the two models mentioned above. The consumer finance opening strategy of Nu Skin Bank promotes joint loan products to financial peers to solve the capital problem, while penetrating into various scenarios to solve the flow problem.

This mode is essentially a matchmaking mode based on science and technology, and many entrepreneurial mutual fund platforms are also adopting it. For example, the consumer finance solution of Pinti Technology, based on its own big data risk control capability, receives scene traffic on one hand and institutional funds on the other; Another example is Jianpu Technology (Rong360), which is positioned as an intelligent selection platform for financial products. Based on long-term scientific and technological accumulation, it accumulates traffic and users while connecting with the products of various financial institutions.

Open what? Four products&capabilities!

Regardless of the B-end business, as far as the C-end business is concerned, the ability that banks can open up is no more than four categories: payment (account system), wealth management products, personal loans (including credit cards), and financial technology capabilities. The following analysis is made respectively:

(1) Payment (account system) capacity is open. The opening of payment capacity can be divided into two categories: one is the open account system, which is the bottom bank account of the scenario party's specific financial products. The most typical is the virtual account opened for lenders and borrowers in the P2P custody process; The second is to open payment capability and load standardized payment, transfer and other product functions for scenario parties.

In terms of the former, banks have achieved a large-scale growth in the number of virtual accounts opened, and also precipitated deposits. However, as the underlying account, it is usually insensitive at the user level, with obvious limitations, and it is difficult to carry the sales of other financial products. As for the latter, under the current payment market pattern, banks open their payment capacity, which is generally to open aggregate payment capacity, and package their accounts with third-party payments such as Alipay, WeChat payment, Suning payment, etc.

From the perspective of the scenario side, the open products of bank payment (account system) capacity are highly homogeneous and highly replaceable, which inevitably lack stickiness and loyalty to cooperative banks.

(2) Financial products are open. According to the Measures for the Supervision and Administration of Financial Services of Commercial Banks issued in September 2018, "commercial banks can only sell financial products through their own channels (including business outlets and electronic channels), or through other commercial banks, rural cooperative banks, village banks, rural credit cooperatives and other banking financial institutions that absorb public deposits." It can be seen that, Only banks can sell bank financial products, so the ability of bank financial products is open, which is not feasible at this stage.

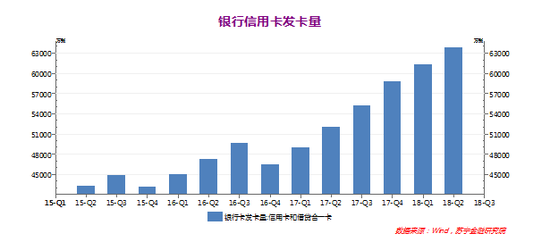

(3) Personal loan (including credit card) products are open. Essentially, it is to increase the channels for loan products to attract customers, which is the most mainstream open mode at present. The opening strategy of personal loan products is successful in terms of results, which is also an important incentive for more and more banks to embrace the opening strategy.

Taking credit cards as an example, in 2017, 123 million new credit cards were issued in the banking industry, an increase of 90 million over the same period last year, opening the way for explosive growth; In the first half of 2018, 50 million new cards were issued, maintaining a high growth. According to Rong360's estimation, more than 60% of the new cards are issued through online channels, that is, cooperation with various online players.

In the field of personal loans, the cost of capital of banks is low enough that there are almost no competitors. The only bottleneck is the bank's own risk control. In theory, as long as the risk control threshold is lowered again and again (or the risk control capability is continuously improved), the business scale will become larger and larger.

(4) Financial technology capability is open. In this wave of bank financial technology transformation, the leading banks have chosen to open their own IT and technology capabilities. as Industrial Bank 、 Ping An Bank and bank for economic construction , have established independent subsidiaries to provide financial institutions with all-round capabilities from IT system building, platform operation to intelligent risk control, business cooperation, etc. Other banks open specific modules such as authentication and authorization, fraud management and alarm, and data risk control. For example, the blacklist sharing platform based on blockchain independently developed by Suning Bank has shared nearly 3 million data.

Example: core business matrix of Industrial Digital

Open challenge: can we be a universal connector?

Opening the interface and connecting everything seems to be a great idea, which seems to open endless space. The question is, although you can connect "everything", why is "everything" willing to connect you? Just like a well-known road to becoming rich, "1.4 billion people in the country will give me a dime each, and I will become a billionaire immediately". The real challenge is how to make people in the country give me a dime each?

From a commercial point of view, it is not easy to be a linker.

From the perspective of product functions, "connection" is a tool attribute, and the key is to see what business benefits can be brought to partners. For example, WeChat, Alipay, Baidu and Toutiao have successively released small programs. They want to be the connectors and responders in the Internet field. What people look at is not the small programs themselves, but the high-quality scenes and attractive traffic behind the small programs.

As far as banks are concerned, it is not difficult to open the API interface, but it is difficult to attract partners.

In terms of typical consumer financial products, assets (customers&flows&scenarios), funds (financial products), and risk control (technology) are three core resources. In order of scarcity, assets (customers&flows&scenarios)>risk control (technology)>funds (financial products). Therefore, the ability to acquire assets is the premise of being the "universal connector" of the industry. For most banks, the ability to acquire assets is just a weak point. They want to build an open platform with homogenized funds (financial products) to find high-quality assets for "redundant" funds. With the low cost of capital, we can certainly gain the growth of scale, but with the homogeneous resources, we are doomed to not be the leader of the platform.

Therefore, the spirit of openness should be advocated, but openness itself is not exciting. If the business itself is not competitive, it will still not be competitive after opening the API interface. Openness is just the beginning, and it is not success itself, which needs us to remember.

(The author of this article introduces: Director and Senior Researcher of Internet Finance Center of Suning Financial Research Institute.)