Article/Sina Financial Opinion Leader Column (WeChat official account kopleader), Peking University Guanghua School of Management

Author: Liu Qiao Dean of Guanghua School of Management, Peking University

In recent years, China's stock market has been depressed as a whole, but the reform and improvement of the system has not stopped. Some blue chip blue chip stocks with good performance have also given investors good returns. China's A-share market is becoming more and more mature. As the overall market falls sharply this year, A-share gradually shows great investment value. How will the A-share market differentiate in the future, which companies have investment value, which companies will continue to grow, and what analysis indicators are more effective?

I will tell this story more completely next. In the past 40 years, we have seen many changes, and China's economy has made rapid progress. But in fact, if we put it in a longer time dimension, the Ming Dynasty has lagged behind the Western countries. Since 1949, when we established the New China, we have begun a process of catching up, This process was accelerated after China started its reform and opening up in 1978. We have made many achievements in this process, which is a great era. Next month, the Central Committee will also commemorate this era in various ways, basically witnessing the climax and trough of this era.

There are many stories behind this. The total amount is 35 times, and the per capita amount is more than 9000 dollars. Our rise in infrastructure, and then our rise in real estate. These figures are impressive. In 1978, according to the industrial output value, China's manufacturing industry accounted for less than 1% of the world, and now it should be 27%, 28%, I think what we see behind this is that the process of industrialization has advanced rapidly, and then we almost think that the process of industrialization has been completed.

There are many reasons behind it. From the perspective of enterprises, we can see that the biggest change for us in the past 40 years is that China's enterprises in the modern sense have gone from nonexistence to greatness.

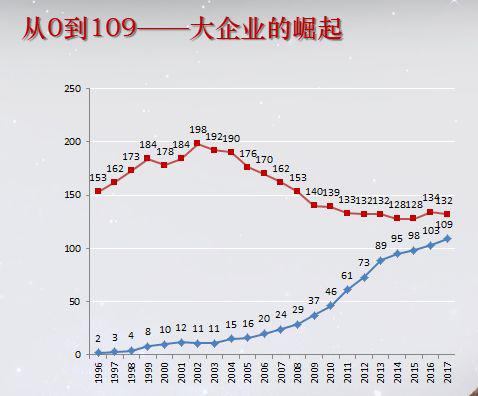

So here is a simple diagram for you. We can see that the Fortune Global 500 enterprises that Chinese people like to talk about are ranked globally by Fortune magazine in July every year according to the sales revenue of this enterprise. In 1996, there were two Chinese enterprises, 109 by 2017 last year, and 111 by this year, If we add Taiwan enterprises, we have 121 and the United States 126. According to such data, China is likely to surpass the United States in the next two years or so, and the line below will surpass the line above.

I also briefly analyze behind this. We translated the words of the Fortune Global 500, which is called Fortune Global 500 in English. I didn't point out that the Fortune Global 500 has made great progress in the past, There are many stories that can be told that 80% of them are state-owned enterprises or local state-owned enterprises.

This also reflects that we are in the capital market. As you can see, I think that the layout of large enterprises in the entire capital market is basically closely linked to our economic growth model in the past 40 years. We are investment driven. Investment driven growth model is very fast and pursues scale.

In this case, industries such as raw materials, energy and capital are particularly prone to large enterprises. This should be at the end of last year in the A-share market. We calculated that among the top 10 enterprises with the largest market capitalization, 7 financial institutions and 2 financial institutions are PetroChina and Sinopec, as well as Maotai, which is also good for production factors, This layout itself reflects the characteristics of China's economy in the past 40 years. The enterprise structure of our listed companies is highly consistent with this feature.

ROIC analysis: capital use efficiency analysis

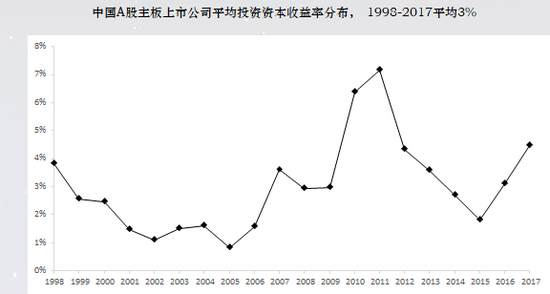

ROIC analysis: capital use efficiency analysis But this question is about what we should do in the future. If I think about it, we talked about many problems in the capital market. For a long time in the past, everyone was disappointed. I want to break the point. The main reason is that our enterprise is big, but our investment capital in all aspects is very large. This is a book, In the book, I have done an analysis called Return on Investment Capital of Chinese main board listed companies in the past 20 years, that is, ROIC analysis, that is, investment capital. The higher the efficiency of capital use, the higher the return to investors.

In China, we can see that the number has changed a lot in the past 20 years. It is very surprising that we are 3%. If we use the weighted average, it may be 4%, and the arithmetic average may be 3%. That means that our investors give a dollar to listed companies to do operations, produce products, and provide services. The tax profit is about 3 cents a year. When you think about such a problem, the way to obtain an annualized return of 10% or 20% under such circumstances is to increase leverage. That is why we say that leverage is so high, which is related to the low return on investment.

We talk about the direction of the development of the capital market, including China's macro policies. In what dimensions, we should provide a lot of inspiration for high-quality economic development.

The growth rate is basically driven by two things, one is the rate of return on investment capital, the other is the rate of investment. If my rate of return on investment is relatively low, the only way to maintain growth is the rate of investment. This story was told in the past, especially after 2010, when China responded to the financial crisis, the macro policy was basically this way of thinking. When the rate of return on investment was not high, The micro foundation is weak, and we can only rely on the investment rate to maintain GDP growth of 6.5% or more than 7%. The most important source of funds is in the financial system dominated by indirect financing, resulting in high leverage and debt. The high debt itself is also linked to the weak micro foundation and the relatively low return on investment capital of enterprises.

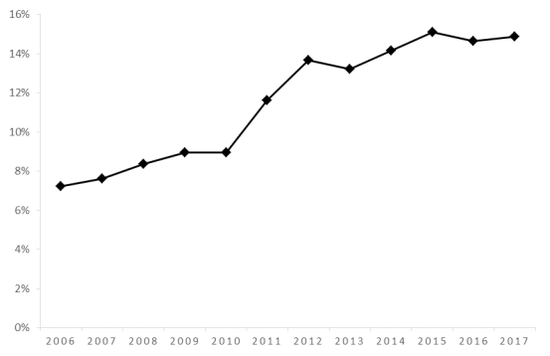

Let's go back to the listed companies. The listed companies just mentioned that the Shanghai Stock Exchange 50 is better than the S&P 500. This figure, from 2003 to 2017, the Shanghai Stock Exchange 50 year old is only 3.1%, which is very low. What I want to reflect is the quality of the investment object just mentioned.

I made another analysis, which enlightens us, especially for institutional investment, and is more sensitive to stock price discovery. Let's see the comparison between the GEM market and NASDAQ, and the analysis of the figures at the end of 2018 this year. In general, you can see that all the enterprises in the first column are included. The price earnings ratio of NASDAQ is 36 times, and we are 48 times. The bubbles in American stocks are very high. Whether there will be bubbles in China's GEM is another perspective.

We look at the removal of enterprises with a market value of more than 10 billion yuan from NASDAQ, and the removal of the GEM for more than 10 billion yuan. There are 2337 remaining enterprises in NASDAQ, with a P/E ratio of 208 times, and we have 605 remaining enterprises, with a P/E ratio of 51 times. This shows what the problem is, 208 times. However, American investors have no complaints about this bubble. They believe that enterprises have growth potential, and some enterprises will stand out, The enterprise that has brought good returns to investors, whether it is a large enterprise or a small enterprise in China's GEM, is almost the same. It is no longer between 48 and 51. In other words, there is no growth at all.

If we take a step back and make a cautious conclusion, we need to think about whether it confirms the point just made and where our quality, growth and new momentum are.

In addition, it is also the findings of our analysis. For example, the size of our enterprises, just mentioned the top 500 enterprises, is the business vision of many enterprises. The size itself, to a large extent, is connected with diversification. A simple analysis of China's A-share market, the number of business segments, and the relationship between your investment capital is basically negative, and there is absolutely no positive correlation, Basically, it is negative correlation. It means that the value creation of an enterprise is getting farther and farther when its scale is expanding and its diversification degree is constantly improving. I don't know how many of our entrepreneurs truly agree with this view.

The larger you are, the easier it is to leverage. In this case, if the rate of return on investment capital increases, your value creativity will not show, and eventually you will not be able to pay the debt interest or principal, forming a snowball of debt, like the vast number of financial institutions, For a long time in China, the story of being big and never failing also exists at the level of listed companies.

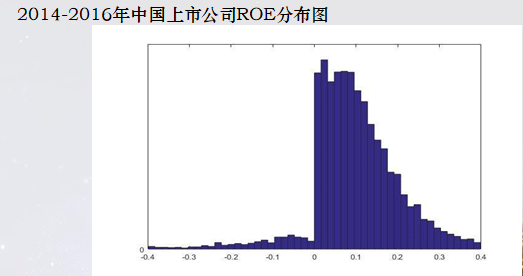

Let me give another example of the quality of our listed companies. From various perspectives, I have drawn this picture for 15 years, every year, and no change every year. This is a familiar picture of ROE of our listed companies. The histogram is obviously not normal distribution, and there is a big jump on the point of 0, which shows that Chinese listed companies are very clever in the economic level, We can always reach a high position of zero. This is the normal distribution of the United States. Whether China is a normal distribution can be concluded.

Given that the rate of return on investment capital in such capital market is only about 3%, how can investors meet their high return expectations.

Together, I want to draw a conclusion that in the future we will transform from the so-called high-speed growth stage to the high-quality development stage. I personally understand that there is only one core meaning. You need completely different enterprises, and China's micro foundation needs to be greatly reshaped and restructured.

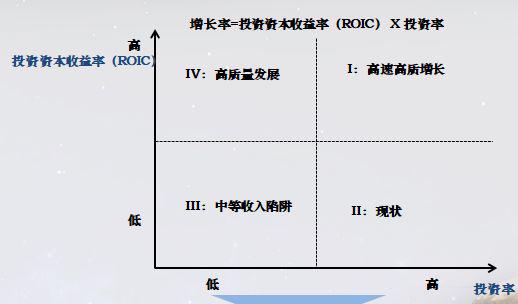

This figure is a simple two by two scenario analysis based on the growth rate equal to the return on investment capital and the investment rate I just mentioned. The horizontal axis is the investment rate, and the vertical axis is the rate of return on investment capital. The two indicators have different values.

There may be four scenarios in the future of China's economy. The first two are both high and impossible. The second is the current situation. When the economic growth is facing challenges, I will try my best to increase the investment rate. There must be room for improvement in China's investment rate. If we calculated the per capita fixed capital ratio two days ago, it is far lower than that of the United States, much lower than that of the United States when it was at $9000, This shows that there is a lot of investment space in public services and infrastructure construction. Here, our urgent requirement is to hope that if these investments are made, the investment efficiency and return on investment capital will be improved accordingly, so that the system risk is good, or the high leverage will not touch the development of China's economy.

The other is that both are low, the investment efficiency is also low, and the yield is also low. This is the middle-income trap. The high-speed and high-quality growth proposed by General Secretary Xi, the value enterprises oriented by value creation, as a whole, improve the return on investment capital of China's economy. Then we find that we can live a very ideal high-quality growth without too much investment when we combine them. How can the capital market help us in the future, How to find out the very good rate of return on investment capital. How do institutional investors participate in this process and provide assistance to it in the screening process.

Which fields of listed companies have the potential of high return on investment capital?

Which fields of listed companies have the potential of high return on investment capital? Let me briefly mention some areas that can be focused in the future. If China's economy finds new momentum, it will eventually return to entrepreneurship and research and development.

I think R&D and entrepreneurship are indeed the key for us to reshape the micro foundation of China's economy in the future. In addition to R&D, that is to say, if I want to choose from more specific indicators, I really want to emphasize this indicator of ROIC.

Let's take some examples. For example, Chinese enterprises with high valuation now, whether in A-share or overseas markets, have a high return on investment. For example, in the past five years, Alibaba simply calculated that the ROIC before tax last year was 41%, and after tax 30%. You gave Ma Yun 1 yuan and he gave you 30 cents in profits. This enterprise earned a valuation of more than 500 billion dollars, This valuation, which is equivalent to more than three trillion yuan, shows a very high rate of return on investment and a very fast growth rate. It can be imagined that investors' love for such enterprises can be reflected.

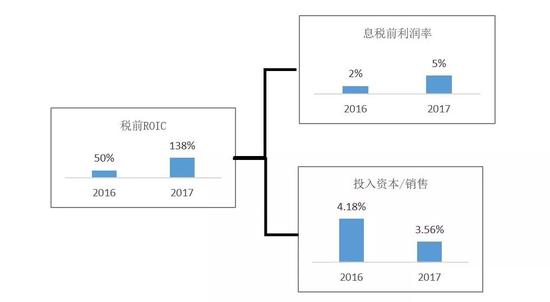

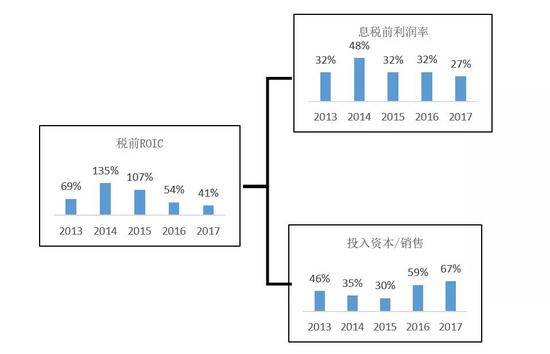

I won't comment on Xiaomi's words, but I will tell you one thing: a manufacturing enterprise, no matter what brand it plays, has done well in this ROIC. Let's take a look at the information in this prospectus, and simply calculate the ROIC in 2017, which is 138%, multiplied by 0.75, which is also an unusually high figure. Can Xiaomi continue to have a high return on capital investment in the future, It depends on whether it can maintain a high valuation premise.

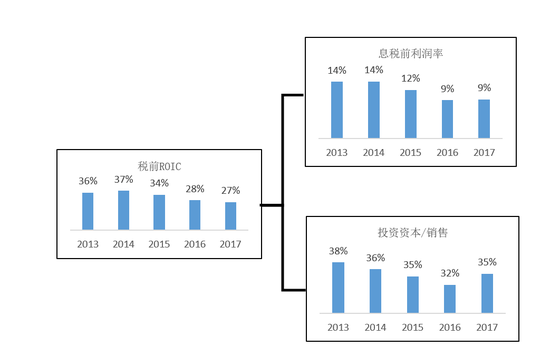

Not commenting from the perspective of operation, it also reminds us what kind of enterprises we need in the future, which must be enterprises with high return on investment capital. Huawei is not listed, but he saw that as an enterprise in a capital intensive industry, in 2017, it was 27% of the ROIC before tax, and nearly 20% after tax. If such an enterprise is a listed company, you can think about what returns it will bring to investors.

Behind Huawei's success is R&D, which is a game against China. If you compare R&D to sales by more than 15%, R&D is the numerator, and sales revenue is the denominator. Last year, Huawei's revenue was 600 billion yuan, 15% multiplied by 600 billion yuan, and nearly 100 billion yuan of R&D, the value of this market yield to investors is worth looking forward to.

I am relatively optimistic. We have many potential areas that can generate growth and value. I have a few figures here to report briefly, and can also provide a larger vision.

The total amount, if we maintain 5.5%, and then maintain it until 2030, then the total amount will reach 157 to 160 trillion yuan. At this price, I think the speed is still relatively large. Last year, 87.2 trillion yuan, and the next 12 years will be equivalent to a relatively moderate growth rate. We still have a growth space of twice the size.

What does this mean to us? I want to tell you something. For our financial system, the financial system, everyone says that this indicator is the ratio of financial assets to GDP. China is now 3.7 times, the United States is between 4.6 and 5 times, deleveraging has been in progress, and the structure is changing consistently, between 4.6 and 4.5 times, China is 3.7 times, and we will reach 4 times by 2030, According to this price, the GDP may be 160 trillion yuan. If you provide four times, the most conservative estimate is 640 trillion yuan.

At today's price, Industrial and Commercial Bank of China About 26 trillion yuan last year, the largest financial system in the world last year. In China, the financial volume may be about 640 trillion yuan. Speaking of the stock market, the U.S. accounts for 40% of the assets of scale, but China may not be as high as 30%. Maybe 180 trillion yuan is reflected in the form of stocks among the 60 billion yuan.

So at this time in the future, I think the opportunity is absolute and very real. We need to make the quality of the capital market real, and we need to find out a group of good enterprises that have a very high rate of return on investment capital to meet the people's aspirations for a better life.

Finally, I would like to make a summary. In my own opinion, what kind of industries will be concerned about in the future? I believe the concept put forward by Goldman Sachs. What other industries in China may have the possibility of 4 or 4 times of GDP growth in the next 10 years? Emerging industries, new consumption, the Internet, health industries and other industries will come out, It will grow at a high speed in the future, accompanied by changes in consumption levels, changes in demand, and adjustment of industrial structure.

In the future, these industries will rise, so there will be some enterprises that do not really have too much historical burden, have clear ideas, reasonable strategies, and can really create value and improve the return on capital. This is the main reason why we have some confidence in China's capital market in the future, whether it is China's economy.

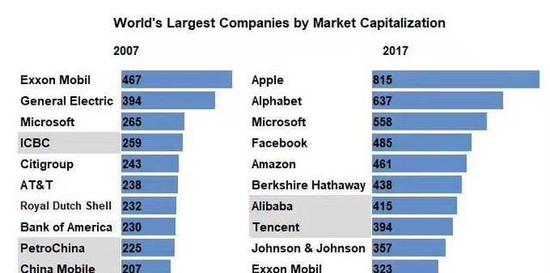

If I think about it, the last picture will show you how the pace and rhythm of this era of change has changed our future expectations. Here, 80% of the world's top 10 digital enterprises in 2007 and 2017 have changed. I looked at it at that time, that is, Alphabet is still there, and Microsoft is still there, In 2017, only 2 were on the list.

Looking at China from 1997 to 2017, we made such an analysis every ten years. The largest market capitalization enterprise in 1997 was Sichuan Changhong , changed in 2007, PetroChina In November 2007, its market value reached 1 trillion US dollars, but it was not too long ago. By 2017, you will see that the ranking of this digital enterprise has changed a lot. The first and second ranked enterprise has not been born in the beginning year of this ranking. Twenty years later, it is the largest market value enterprise in China, although listed overseas, When we look at this picture again in 2028, I believe we will see many completely different enterprises, probably from different industries, and you can imagine it.

But in what way will these enterprises change the micro foundation of China's economy, change the pattern of China's economy, and ultimately bring real vitality and returns to investors and the capital market? I think this is a decade worth looking forward to.

In the end, everything comes down to how to do and work hard. One sentence is for everyone. The answer to the future is hidden in the present. Thank you.

This article is the author's speech at the China Institutional Investors Summit.

(The author of this article introduces that as the main body of business management education in Peking University, Guanghua School of Management of Peking University is one of the best business schools in the Asia Pacific region.)