Article/Xu Zhong, columnist of Sina Financial Opinion Leader Column (WeChat official account kopleader)

At present, few blockchain projects have actually landed and generated social benefits. In addition to the poor physical performance of blockchain, the weakness of blockchain economic functions is also an important reason. On the basis of continuous research and experiment, we should rationally and objectively evaluate what the blockchain can and cannot do.

Summary: This paper studies the functions of blockchain from the perspective of economics. First of all, on the basis of the economic explanation of blockchain technology, the "Token Paradigm" adopted by the current mainstream blockchain system is summarized to clarify the two basic concepts of consensus and trust related to blockchain, and to sort out the functions of smart contracts. Secondly, according to the use of tokens in the blockchain, the main application directions of the current blockchain are sorted out, and then the characteristics of tokens, the impact of tokens on blockchain platform projects, the governance function of the blockchain, and the performance and security of the blockchain system are discussed. Finally, what can and cannot be done by the blockchain are summarized and discussed.

Abstract: This article studies blockchain‘s economic functions. First, by explaining blockchain technologies from an economic perspective, it introduces the Token Paradigm to summarize mainstream blockchain systems, discusses the true meaning of consensus and trust in the blockchain field, and analyzes the functions of smart contract. Next, it categorizes major blockchain applications according to how they use tokens and discusses relevant economic problems such as tokens’ monetary features, tokens‘ impacts on platform projects, blockchain’s governance functions, and the performance and security of blockchain systems.

Keywords: blockchain token smart contract, distributed autonomous organization, encryption economics

1、 Introduction

Blockchain was first proposed by Nakamoto (2008) as the underlying technology of Bitcoin. However, the script language of Bitcoin lacks Turing completeness, and the UTXO (open transaction output) model used is difficult to support complex state operations. Therefore, Buterin (2013) proposed Ethereum. Ethereum is a blockchain system based on the account model. The script language has Turing completeness. The goal is to realize the smart contract proposed by Szabo (1994) and support distributed applications (DApp). With the founding of the American R3 company in 2014 and the launch of the Hyperledger project by the Linux Foundation in 2015, blockchain has attracted more and more attention from mainstream institutions. For example, Goldman Sachs (2016) discussed the application of blockchain in the sharing economy, smart grid, real estate insurance, stock market, repo market, leveraged loan transactions, anti money laundering (AML for short) and "know your customer" (KYC for short). The White Paper on China's Blockchain Technology and Application Development (2016) released by the China Blockchain Technology and Industry Development Forum in October 2016 discussed the application scenarios of blockchain in the fields of financial services, supply chain management, culture and entertainment, intelligent manufacturing, social welfare, education and employment.

In January 2009, the online launch of Bitcoin marked the landing of blockchain applications. But in the nearly 10 years since then, except for the issuance and trading of cryptocurrency, blockchain has not been widely used. As of October 31, 2018, CoinMarketCap website has counted 2086 cryptocurrencies and 15545 cryptocurrency exchanges worldwide. The market value of all cryptocurrencies is about $203.5 billion (of which Bitcoin market value accounts for 54%), and the transaction volume in the past 24 hours is about $10.6 billion; However, DappRadar website counted Ethereum and its 1137 distributed applications, and found that only 12521 active users in the past 24 hours, of which only 2 distributed applications had more than or close to 1000 active users in the past 24 hours, and the more active distributed applications were concentrated in games, gambling, encrypted asset transactions and other fields that had little to do with the real economy. In August 2018, PricewaterhouseCoopers' survey of 600 company executives in 15 countries found that 84% of the companies were interested in blockchain, but 52% of the companies' blockchain projects were in research and development status, 10% of the companies had blockchain pilot projects, and only 15% of the companies had blockchain projects in operation 3.

An important reason why blockchain has not been applied in a large scale is that its physical performance is not high (especially for public chains). For example, Bitcoin can support up to 6 transactions per second, while Paypal can support 193 transactions per second on average, and Visa can support 1667 transactions per second on average. Many practitioners and researchers discussed how to improve the physical performance of blockchain, including relay network, sharding, increasing block size, SegWit, directed acyclic graph structure (DAG), cross chain, side chain, state channel (represented by Bitcoin Lightning Network), and technology for compressing transaction information (such as Mimblewimble). Yuan Yuming and Liu Yang (2018) gave a comprehensive introduction to these directions. Another important direction to improve the physical performance of blockchain is to improve consensus algorithm, especially from proof of work (POW) to proof of stake (POS). Yuan Yong et al. (2018) summarized common blockchain consensus algorithms. The use of federated or private chains instead of public chains in some application scenarios is also an important aspect of bypassing blockchain physical performance bottlenecks.

This paper studies what blockchain can and cannot do from the perspective of economics. Even if the physical performance bottleneck of the blockchain can be alleviated in the future, some economic problems studied in this paper will still exist. This paper is divided into four parts. The first part is the introduction. The second part is an economic explanation of blockchain technology, which is equivalent to "translating" blockchain technology in economic language. This part summarizes the "Token Paradigm" adopted by the current mainstream blockchain system (Token has multiple Chinese translations in different contexts, such as cryptocurrency, cryptoasset, token and token, etc. In order to avoid confusion or ambiguity, this article mainly uses Token Rather than its Chinese translation), clarify the two basic concepts of consensus and trust related to blockchain, and sort out the functions of smart contracts. The third part studies the economic functions of blockchain. This part first sorts out the main application directions of the blockchain, and then discusses the characteristics of Token like currency, the impact of Token on blockchain platform projects, the governance function of blockchain, and the performance and security of blockchain system. The fourth part summarizes the full text and discusses what the blockchain can and cannot do.

2、 Economic explanation of blockchain technology

Blockchain involves computer technology and economics. This part gives an economic explanation of blockchain technology, and analyzes common misunderstandings in consensus, trust and smart contract related to blockchain, laying the foundation for the third part to study the economic function of blockchain.

(1) Token paradigm of blockchain

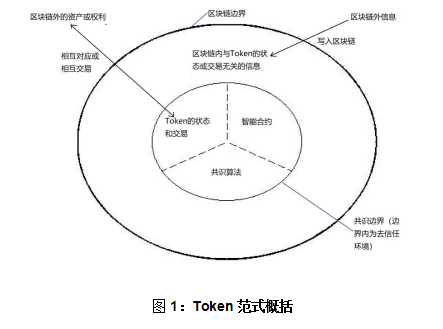

At present, the mainstream blockchain system, whether it adopts the UTXO model represented by Bitcoin, or the account model represented by Ethereum, or whether the script language has Turing completeness or supports smart contracts, has three key characteristics, which can be summarized as the "Token paradigm":

First, the consensus algorithm is aimed at the Token in the blockchain. Tokens are essentially state variables defined in the blockchain. Tokens can be transferred between different addresses in the blockchain. The total number of Tokens remains unchanged during the transfer process (that is, when the transfer out address decreases by one token, the transfer in address increases by one token). Some blockchain systems limit the total amount of tokens, which is the case with Bitcoin.

When a token is transferred between different addresses in the blockchain, the status update of the token (referring to how many tokens are in each address in the blockchain) and transaction confirmation occur synchronously. For example, Alice transferred a Bitcoin transaction to Bob. When the transaction was recorded in the blockchain (that is, the transaction was packaged into a block and connected to the blockchain), the UTXO (which can be understood as the account balance in the Bitcoin blockchain) of Alice and Bob's corresponding public key was updated at the same time. Therefore, when a token is traded, it will not form the traditional sense of settlement funds in transit or settlement risk.

Second, Token and smart contract are inextricably linked. Token itself is the embodiment of smart contract. For example, the Token Contract represented by Ethereum ERC20 stipulates a series of logics such as the total amount of tokens, issuance rules, transfer rules and destruction rules. Token contracts manage a series of statuses, recording the account book information such as which addresses have and how many tokens. On the basis of Token contracts, you can build smart contracts that perform complex operations on Tokens. The main result of the execution of these smart contracts is that the status of the token changes. The third section of this section will analyze the functions of smart contracts.

Third, according to whether it is related to the status and transaction of the token, the information in the blockchain is divided into two categories ——Relational and unrelated information have completely different status under consensus algorithm. When running the consensus algorithm, the node focuses on checking whether the first type of information conforms to the predefined algorithm rules. The second type of information is written into the blockchain as additional information of Token transactions, and the node will not check the true accuracy of this type of information. For example, the Bitcoin node will verify that the random number (nonce) is the solution to the "mining" problem, and that the transactions in the block meet predefined standards in terms of data structure, syntax normalization, input/output and digital signature. However, "The Times 03/Jan/2009 Chancellor on bring of second checkout for banks" in the creation block of Bitcoin, the node will not and has no ability to verify the true accuracy of this sentence.

Distinguishing these two types of information is the key to understanding the scope of the blockchain consensus. The blockchain consensus refers to the information related to the status and transactions of the token. For example, the Bitcoin consensus determines the number of UTXOs corresponding to each address and the record of Bitcoin transfer between addresses as of a certain block. However, the information irrelevant to the status or transaction of the token in the blockchain is basically not within the scope of consensus. In particular, the mechanism by which information outside the blockchain is written into the blockchain is generally called oracle mechanism. If the information outside the blockchain cannot be guaranteed to be true and accurate at the source and writing link, writing into the blockchain only means that the information cannot be tampered with, without improving the authenticity and accuracy of the information. However, the blockchain helps to solve the problem of data registration traceability. The data registered in the blockchain has a traceable principal identity signature and can be used for post audit. Moreover, the tamper resistance of the uplink data also helps to control operational risks.

(2) Consensus and trust within the blockchain

Consensus and trustless are two very important basic concepts of blockchain. These two concepts are born out of the computer field and are difficult to be strictly defined in economics, but they are easily misunderstood. For example, consensus is equivalent to eliminating information asymmetry or realizing common beliefs, and distrust is equivalent to no credit risk.

1. Definition of consensus

The current discussion on blockchain consensus involves three consensus concepts in different contexts - machine consensus, governance consensus and market consensus, among which governance consensus and market consensus can be called "human consensus". Many misunderstandings stem from confusing the three types of consensus, or generalizing the scope and nature of consensus.

First, machine consensus. Machine consensus is a problem in the field of distributed computing. The goal is to ensure that the backup texts of distributed ledgers on different network nodes are consistent (not semantically consistent) without central coordination in peer-to-peer networks where there are various errors, malicious attacks, and possible unsynchronization.

The nodes of the equation network (especially the nodes responsible for generating and verifying blocks) are divided into honest nodes and malicious nodes. Honest nodes follow predefined algorithm rules (mainly consensus algorithms) and can send and receive messages perfectly, but their behavior is completely mechanical. Malicious users can deviate from the algorithm rules at will. Under certain restrictions (for example, Bitcoin requires that more than 50% of the computing power be mastered by honest nodes), the algorithm rules ensure the feasibility, stability and security of machine consensus. The scope of the machine consensus is limited to the information related to the status and transactions of the Token in the blockchain.

Second, governance consensus refers to that in group governance, group members develop and agree on a decision that is most beneficial to the group. For example, the discussion of "capacity expansion" and bifurcation in the Bitcoin community can be understood in the framework of governance consensus. The elements of governance consensus include: 1. different interest groups; 2. Certain governance structure and rules of procedure; 3. Reconciliation and compromise between conflicting interests or opinions; 4. Group decision-making with general constraints on members. Yuan Yong et al. (2018) pointed out that governance consensus involves people's subjective value judgment, and deals with subjective multi value consensus. Participants in governance consensus converge to the only opinion through the process of coordination and collaboration among groups. If this process does not converge, it means the failure of governance consensus.

Third, market consensus. When Tokens participate in transactions (whether between different Tokens or between Tokens and assets or rights outside the blockchain), market consensus is involved. Market consensus is reflected in the equilibrium price formed by market transactions.

There are close and complex relationships among the three types of consensus. Machine consensus is the product of running algorithm rules on the nodes of the equation network, and governance consensus reflects the process of formulating or modifying algorithm rules by people (including the owners or controllers of network nodes). Market consensus is affected by machine consensus and governance consensus. For example, if the security of the distributed ledger is not guaranteed (that is, the machine consensus fails), the market price of Bitcoin will suffer a devastating impact. For another example, the discussion of the Bitcoin community on "SegWit2x" in 2017 (that is, introducing isolation witness and increasing the size of a single block from 1M to 2M) had a significant impact on the price trend of Bitcoin at that time, which reflected the impact of governance consensus on algorithm consensus. Unless otherwise specified below, the discussion is about machine consensus.

2. Discrimination of the meaning of distrust

The distrust originates from the arrangement that when a token is traded, the status change of the token and the transaction confirmation occur simultaneously. Imagine Alice buying a certain goods from Bob with Bitcoin. Alice's payment of Bitcoin to Bob can be carried out in a secure way within the blockchain without any understanding between the two people or trusted third-party institutions. This is the true meaning of trust. But at the other end of the transaction, how does Alice ensure that Bob will deliver qualified goods to her on time? As long as you can't hand in bitcoin and deliver goods in one hand, there will be credit risk of the counterparty that can't be ignored. Only by accurately identifying and evaluating credit risks and introducing risk prevention measures can many transactions be conducted. For example, in the dark network transaction, the transaction platform usually sets up a third-party escrow account. The buyer will first transfer Bitcoin into the third-party escrow account, and after receiving the goods and confirming them, it will notify the trading platform to transfer Bitcoin to the seller. Without the third-party trusteeship account as a means of credit enhancement, the transactions between Bitcoin loyal supporters will also be greatly reduced.

Therefore, the distrust environment within the blockchain cannot be simply extrapolated out of the blockchain. Once breaking away from the original scenarios such as Token transactions, the blockchain often needs to introduce a trusted center mechanism outside the blockchain to help solve the trust problem in reality.

(3) Functions of smart contract

Smart contracts are computer codes that run in the blockchain and mainly perform complex operations on Tokens. At present, the limited running environment in the blockchain makes this kind of code far from reaching the intelligent stage. It can even be said that the current smart contract is neither smart nor contract. This section summarizes the functions of smart contracts with respect to the basic operation of "transferring the number of Tokens from A address to B address to X under certain trigger conditions".

First, the function of property rights. A address and B address can belong to account or smart contract. Token in the address has the meaning of property right. For example, if address A belongs to the issuing address, it corresponds to the generation of a token (primary market); If address B belongs to the destruction address (that is, a special address similar to. 0000 that does not correspond to the private key), it corresponds to the destruction of the token; Token transfer between two addresses corresponds to property right change.

Second, the function of the process level. For a token transfer to be effective, the transfer initiator must have the right to operate X number of tokens in the A address, and the trigger conditions of the smart contract are met. After the initiator transmits the transfer information to the distributed network, other nodes verify whether the initiator has the operation authority of the A address, whether the trigger conditions are met, and whether the number of Tokens in the A address exceeds X The operation authority of the address is reflected in the relevant signature operation (often involving multiple signatures). The trigger condition depends on the information inside and outside the blockchain (where the information outside the blockchain needs to be written into the blockchain first). The transfer quantity X can be determined manually or by a formula to achieve contingent payment Or more complex payment structure. There are only "success" and "failure" in the execution of smart contracts, and there is no intermediate situation. In particular, if the transfer initiator cannot ensure that the number of Tokens in the A address exceeds X, the execution of the smart contract will fail.

Third, economic and social functions : 1. Voting. Transferring Tokens to an address can be understood as voting; 2. Mortgage, first transfer a certain number of tokens to a smart contract, and agree that the tokens can be returned when certain conditions are met at a future time point; 3. Freezing and unfreezing. Freezing is to lock a certain number of Tokens with a time lock, so as to temporarily give up the liquidity of Tokens and unfreeze them when they expire. Based on basic functions such as voting, mortgage, freezing and unfreezing, smart contracts can support more complex governance functions (see the second and third sections of Part III).

However, the functional weaknesses of smart contracts cannot be ignored. First, when the trigger condition of the smart contract depends on the information outside the blockchain, such information needs to be written into the blockchain first, but there is no universally applicable decentralized oracle scheme so far. At present, there are two kinds of oracle machines that have been discussed more. One is to rely on a certain centralized information source (such as Bloomberg and Reuters), which runs counter to the decentralized purpose of blockchain. The second is to discretize the information outside the blockchain and write it into the blockchain with economic incentives and votes. This kind of mechanism relies on group wisdom. Voters are rewarded and punished according to the voting results. The closer the voting is to the average, median or other sample statistics of all votes, the more likely voters are to be rewarded, and vice versa, the more likely they are to be punished, in order to encourage voters to vote seriously. The implicit assumption is that there is no systematic bias among the voting groups. However, this assumption may not be true in reality, so there is no universally applicable decentralized oracle scheme.

Second, it is difficult for smart contracts to guarantee the performance of debts in the blockchain. Consider a debt contract: the number of Tokens transferred from address A to address B at a certain time point, and the number of Tokens transferred from address B to address A after a period of time (generally Y>X). At the later point, the smart contract cannot guarantee that the number of Tokens at address B exceeds Y, so the debt cannot be fulfilled. Therefore, it is impossible to eliminate credit risk only by relying on smart contracts. This is a common problem faced by building loans, bonds and derivatives within the blockchain based on smart contracts. One solution is to set an over collateralization on the repayment address, but the over collateralization will cause the idle and waste of Token resources. For derivatives, because their risk exposure may change significantly, it is more difficult to determine the scale of excess mortgage in advance.

Third, smart contracts are difficult to deal with incomplete contracts. People are limited rational, and cannot foresee all possible situations in the future. Even if they do, they cannot write them into the contract, so the contract is doomed to be incomplete. This is why there are exceptions to legal contracts in reality and judicial arbitration is needed when disputes arise. As a computer protocol, smart contracts are difficult to deal with incomplete contracts.

Figure 1 summarizes the above discussion of Token paradigm. Among them, Token、 Both the smart contract and consensus algorithm are within the consensus boundary. Token and smart contract are inextricably linked, and consensus algorithm ensures a de trust environment within the consensus boundary. Information irrelevant to the status or transaction of the Token in the blockchain is outside the consensus boundary and within the blockchain boundary. There are two types of interactions inside and outside the blockchain: first, information outside the blockchain is written into the blockchain; The second is the mutual transaction between the token and the assets or rights outside the blockchain (i.e. market consensus, see the discussion on the price characteristics of the token in the second section of Part III) or mutual correspondence (see the discussion on the second type of blockchain applications in the first section of Part III).

3、 Economic functions of blockchain

Blockchain applications are generally classified according to the industry of the application scenario, such as Goldman Sachs (2016). This paper proposes a new classification method based on the use of blockchain applications for tokens, and discusses the economic issues involved in these applications.

(1) Main application directions of blockchain

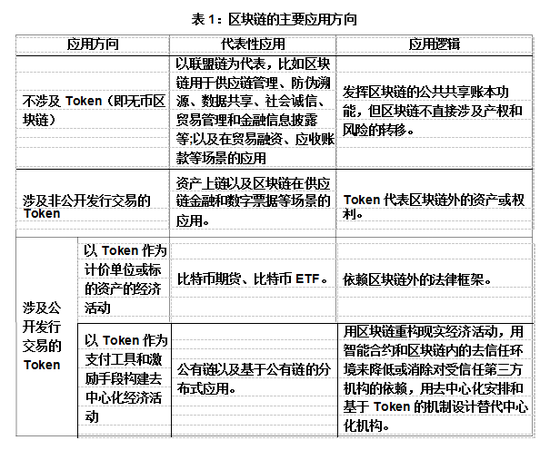

Table 1 divides blockchain applications into four categories. The first kind of application does not involve Token, but mainly uses the blockchain as a distributed database or a decentralized database. The public shared ledger function of the blockchain helps to alleviate the information asymmetry among economic activity participants and improve their efficiency of division of labor and cooperation. The main problem faced by such applications is how to ensure the authenticity and accuracy of information outside the blockchain at the source and in the blockchain link. Compared with the public chain, the alliance chain is more suitable for such applications. The alliance chain is only open to authorized nodes, and is jointly maintained by authorized nodes to achieve consensus among organizations. However, the authorized nodes know each other's identities, and doing evil will have an impact on their reputation. The cost of writing false information into the blockchain is relatively high. The link where information is written into the blockchain can also introduce a third-party identification agency to verify the authenticity and accuracy of information. However, these security mechanisms are mainly based on the constraints of the real world, rather than the characteristics of the blockchain itself. The representative cases of the first type of application are the Bay Area Trade and Finance Blockchain Platform of the Digital Currency Research Institute of the People's Bank of China and the asset securitization information disclosure platform based on blockchain technology.

The second type of application uses Token to represent assets or rights outside the blockchain to improve the registration and transaction process of these assets or rights. However, whether the token corresponds to the assets or rights outside the blockchain, and whether the status and transactions of the token have binding force or influence on the real world outside the blockchain, depends on whether the laws and systems outside the blockchain endow the token with meaning beyond the blockchain. In such applications, the application of blockchain in scenarios such as supply chain finance and digital bills deserves attention. At this time, Token represents the creditor's rights of a core institution and acts as an internal settlement tool in the supply chain. Token replaces the "triangular debt" between upstream and downstream enterprises in the supply chain with the debt of the core institutions to these enterprises after netting, which can reduce the capital occupation and improve the capital turnover efficiency. The core institution plays a similar role to that of the central counterparty and is responsible for the exchange between the token and the legal tender. The Token in these scenarios is equivalent to the concept of online community token or business circle coin proposed by Wang Yongli (2018), and the application value of Token depends on the breadth and depth of the scenarios.

The representative case of the second type of application is the design scheme of the digital bill trading platform. The platform has designed two schemes of off chain clearing and on chain direct clearing according to whether to introduce digital currency on the chain (Xu Zhong, Yao Qian, 2016). Among them, the direct clearing scheme on the chain can realize the registration, circulation and transaction and DVP (Delivery Versus Payment) settlement functions of the full life cycle of digital bills based on blockchain technology.

The third type of application uses Token as the pricing unit or underlying asset, but relies on the legal framework and mainstream economic contracts outside the blockchain. However, the high volatility of token prices limits such applications. An important direction is the so-called stable token or stable coin. Therefore, the core problem of such applications is how to understand the characteristics of Token like currency.

The fourth type of application attempts to build a distributed autonomous organization (DAO for short, see Zou Chuanwei (2018)) with the blockchain. Some practitioners propose that distributed autonomous organizations can replace the functions of real companies. There are no widely recognized successful cases in this regard so far, which are mainly subject to the following obstacles: 1. The physical performance of the public chain is not high enough to support large-scale transactions; 2. Functional weaknesses of smart contracts; 3. The high volatility of Token price limits the effectiveness of Token as a payment tool and incentive means; 4. The design of cryptoeconomics (token economics or cryptoeconomics) model is unreasonable. For the first two obstacles, the first part and the third section of the second part have been discussed respectively. The last two obstacles involve Token's currency like characteristics and the governance function of blockchain.

(2) Token similar currency characteristics

Token has several characteristics similar to currency: 1. Token has no debt attribute; 2. Tokens defined according to the same rule are homogeneous and can be split into smaller units; 3. The transfer of Token between different addresses does not require a trusted third party; 4. Asymmetric encryption can ensure the anonymity of the token holder; 5. Blockchain consensus algorithm and tamper proof feature can ensure that Token will not be "double pending"; 6. The upper limit of the total amount of tokens and the release speed can be defined by rules. These currency like features of Token were introduced by Nakamoto (2008) and followed by other blockchain systems that meet the Token paradigm.

Tokens are directly used as payment tools to exchange goods or services inside and outside the blockchain. At this time, Tokens are generally called cryptocurrencies. In the blockchain, the use of cryptocurrency can be defined by rules. For example, in the Bitcoin system, Bitcoin is used to pay transaction fees to "miners"; In Ethereum, Ethercoin is the "gas" for running smart contracts. The payment scenario in the blockchain also involves market activities (see the discussion on the handling rate of special currency in the fifth section of this part), but because the goods or services in the blockchain cannot be purchased in legal currency, the price of cryptocurrency generally has no significant impact on this scenario. When purchasing goods or services outside the blockchain with cryptocurrency, the price of cryptocurrency is an important factor. Generally speaking, the supply of cryptocurrency is inflexible, lacks internal value support and sovereign credit guarantee, has high price volatility, and cannot effectively perform monetary functions. This is supported by many literatures.

First, the performance of cryptocurrency as a payment tool. Athey et al. (2016) found that by the middle of 2015, most of Bitcoin was held by investors and infrequent users. Bitcoin was not frequently used as a payment tool, and users who used Bitcoin for illegal activities tended to protect their financial privacy. Foley et al. (2018) studied the application of bitcoin in illegal economic activities, and found that 25% of bitcoin users and 44% of bitcoin transactions are related to illegal economic activities. As of April 2017, 40 million Bitcoin market participants mainly use Bitcoin for illegal purposes. They hold 8 billion dollars of Bitcoin in total, with about 360 million annual transactions and an annual transaction amount of about 72 billion dollars (close to the market size of illegal drugs in Europe and the United States). With the increase of interest in Bitcoin in mainstream society and the emergence of cryptocurrencies with better anonymous characteristics such as ZCash, Dash and Monero, the proportion of Bitcoin transactions to illegal economic activities has declined.

Secondly, on the price characteristics of cryptocurrency and possible price manipulation. Gandal et al. (2017) found that Mt. Gox Exchange (the largest Bitcoin Exchange at that time) had suspicious trading activities in two periods from February to mid 2013, involving 600000 bitcoins. These suspicious transactions played an important role in pushing the price of Bitcoin up from $150 to $1000 within two months. Griffin and Shams (2018) studied the impact of USDT (a stable cryptocurrency issued by Tether, which claims to be based on 100% US dollar reserves) on the cryptocurrency and other cryptocurrencies, and found that USDT was used to manipulate the price of cryptocurrencies. During the period from March 2017 to March 2018, the author identified 87 hours. In these 87 hours, a large number of USDTs were issued and used to purchase cryptocurrency. These large transactions occurred after the cryptocurrency market fell sharply. After these large transactions, the cryptocurrency market reversed sharply. The author finds that these 87 hours correspond to the 50% increase of Bitcoin in the research range (from March 2017 to March 2018), and the 64% increase of the other six major cryptocurrencies in the research range. Bianchi (2018) analyzed the transaction data of 14 major cryptocurrencies between April 2016 and September 2017, and found that there was no significant relationship between the yield of cryptocurrencies and the yield of traditional financial assets such as stocks and bonds, and there was no volatility spillover effect between cryptocurrencies and traditional financial assets, Moreover, the trading volume of cryptocurrency is mainly driven by historical yield and market uncertainty (measured by the Chicago Board Options Exchange market volatility index VIX).

The price volatility of cryptocurrency is too high, and the introduction of cryptocurrency futures is also difficult to stabilize price fluctuations. Many practitioners have tried to stabilize cryptocurrency. At present, the stable cryptocurrency scheme launched by Tether, Gemini, Circle and other companies has adopted the method of 1:1 issuance of stable cryptocurrency with legal currency as reserve, which is equivalent to the currency board system. Other schemes to stabilize cryptocurrency adopt the so-called "algorithmic central bank" model, imitate the open market operation of the central bank, and regulate the supply of cryptocurrency by issuing and recovering bonds denominated in cryptocurrency, so as to achieve the stability of cryptocurrency prices. Eichengreen (2018) pointed out that "algorithmic central bank" is difficult to resist speculative attacks. Because bonds denominated in cryptocurrency will have significant discounts when the attack occurs, and the effect of recovering cryptocurrency to support cryptocurrency prices by issuing such bonds will be significantly reduced, the "algorithmic central bank" has inherent instability. It should be noted that central bank digital currency (CBDC for short) is fundamentally different from stable cryptocurrency. The digital currency of the central bank has the attribute of liability. It is an electronic currency issued by the central bank directly to financial institutions and the public. It belongs to a form of legal tender, and does not necessarily take the form of a token in the blockchain. This article does not introduce the digital currency of the central bank in depth, and interested readers can refer to CPMI (2018).

The key point of cryptocurrency supervision is the exchange between cryptocurrency and legal tender, and one of the important issues is anti money laundering. Cryptocurrency money laundering refers to the anonymity and globality of cryptocurrency application, which makes it difficult to trace the source and nature of illegal gains. Cryptocurrency money laundering is divided into three links: 1. placement, which converts illegally obtained legal tender into cryptocurrency. Some cryptocurrency exchanges have not adopted the real name system, which will bring great convenience to the placement process. 2. Layering, using technologies such as mixers, coinjoin, and tumblers, as well as the anonymity of addresses in the blockchain, transfers cryptocurrency between multiple addresses, making it difficult to trace its source. 3. Integration: integrate the "cleaned" cryptocurrency and transfer it to the "clean" address, and then convert it into legal currency or commodities. Cryptocurrency represented by ZCash, Dash and Monero uses anonymous technologies such as zero knowledge proof and ring signature, which will increase the difficulty of anti money laundering. In addition, cryptocurrencies circulate around the world, and different countries or regions have different regulatory standards for cryptocurrencies, making it difficult to share information, which will also increase the difficulty of anti money laundering.

(3) The impact of Token on blockchain platform projects

Some blockchain projects have platform economy characteristics. Token can play two roles in such platform projects: first, it is a financing tool at the start of the project, which is reflected in the initial token offering (ICO for short); The second is the payment instrument of economic activities within the platform. Tokens bring dual benefits to the holders: first, they use Tokens to buy goods or services on the platform; second, the price of Tokens rises, and the price of Tokens is driven by fundamental factors such as the number of active users of platform projects and the amount of economic activity. In addition, the Token of some blockchain platform projects has an equity attribute (see section 4 of this part).

The dual role of Token has an important impact on the launch and development of blockchain platform projects. Catalini Gans (2016) analyzed the impact of blockchain and token on two important factors in market formation - verification cost and network cost. They believe that blockchain allows market participants to verify transaction related information at a lower cost, which will promote the emergence of new market forms; Tokens can reduce network costs and start the market without the need for traditional trusted intermediaries. Cong et al. (2018) used the dynamic asset pricing model to analyze the token price and its impact on user adoption. Token transactions provide intertemporal complementarities for platform users, thus forming a feedback loop between token prices and user adoption. Token price reflects the future growth of the platform. In equilibrium, the token price will increase nonlinearly with platform productivity, user heterogeneity and network size.

The dual role of Token brings about internal instability to the price of Token. Sockin and Xiong (2018) studied Token pricing in the framework of platform economy. Users can improve their welfare by participating in transactions on the platform, and "Miner" provides transaction bookkeeping services. Tokens in the platform have two attributes: first, they are equivalent to "membership", and users need to buy a token before they can participate in transactions on the platform; The second is financing for platform construction and development, including early development costs (embodied as ICO) and rewards for "miners". The author considers two situations of platform fundamentals (mainly reflected in user endowment and "mining" costs) that can be observed publicly and cannot be observed publicly. In both cases, either there is no equilibrium or there are two equilibriums, one of which corresponds to the situation where the Token price is high and the user's enthusiasm for participation is high, and the other one corresponds to the situation where the Token price is low and the user's enthusiasm for participation is low. When the platform fundamentals are unobservable, the Token price not only gathers information about the platform fundamentals, but also plays a coordinating role between different equilibrium paths. But in general, because of the existence of multiple equilibria, the price of Token is inherently unstable.

ICO is a common strategy for launching blockchain platform projects. Li and Mann (2018) believe that ICO has solved many internal coordination failures of platforms with network effects, and can play a role of group intelligence by collecting decentralized information about platform quality. Chod and Lyandres (2018) theoretically studied the choice of entrepreneurs between the two financing methods of ICO and VC. They believe that entrepreneurs can transfer part of their entrepreneurial risks to investors without diluting their control by selling the future output of their projects through ICO, but the resulting agency problems may make entrepreneurs underinvest in projects after financing.

Some scholars have made empirical analysis on ICO. Benedetti and Kostovetsky (2018. In the first 30 days of Token trading, the buy and hold strategy can produce an average excess return of 48%. Momtaz (2018) analyzed 2131 ICO projects from August 2015 to April 2018, and found that on the first day of listing in the cryptocurrency exchange, the average return rate of Token was 8.2%, and the excess return rate relative to the overall cryptocurrency market was 6.8%. Using the first day of listing yield and ICO financing scale as indicators of the success of ICO, we found that the higher the quality of the ICO project team, the easier it is for ICO to succeed; The more ambitious the goal of ICO is, the more likely ICO will fail; Negative events in the industry (such as hacker attacks and regulatory actions) have a great impact on the ICO market.

(4) Governance function of blockchain

Blockchain can support some governance mechanisms different from traditional ones. For example, for distributed autonomous organizations, there is no balance sheet in the traditional sense, and there is no stock representing shareholders' equity. However, some Tokens can be endowed with the right of return and the right of governance through smart contracts. The right of return is realized through dividend distribution, buyback, and the right of governance is realized through participation in governance voting. This type of equity token can also have functional attributes, representing the so-called platform currency issued by some cryptocurrency exchanges. The platform currency holder can use the platform currency to pay the transaction fee to the cryptocurrency exchange, and sometimes can enjoy the discounted transaction fee. Platform currency gives its holders the right to participate in the governance of cryptocurrency exchanges by voting. The cryptocurrency exchange promises to regularly take out a certain proportion of profits, buy back the platform currency and destroy it. There is a significant difference between equity token and company stock.

However, blockchain has some governance weaknesses that cannot be ignored. First, the impact of Token price fluctuations on the incentive mechanism based on Token In the consensus algorithm of public chain (especially POS type), distributed autonomous organizations and side chain projects, many ingenious mechanism designs have emerged, and Tokens are used to encourage the behavior of relevant participants in the blockchain to tend to the expected goal. If the Token has secondary market transactions and high price volatility, even if these mechanisms are designed to be incentive compatible within the blockchain, the behavior of relevant blockchain participants may deviate from the expected goals. For example, many mechanism designs require token holders to lock their own tokens for a period of time and give token holders a certain number of token rewards. Locking a token is equivalent to giving up the right to sell a token at high prices in the secondary market (essentially, a lookback option with floating strike with floating strike). If the price volatility of the token is high, the option valuation will also be high, which means that token holders need to be given high rewards to encourage them to lock up Token9.

Second, the functional weaknesses of smart contracts make it difficult to transplant some commonly used governance mechanisms in the real world to blockchain scenarios. First, it is difficult to construct financial instruments such as loans, bonds and derivatives based on smart contracts in the blockchain, and these financial instruments have important governance functions. Because there is no debt, distributed autonomous organizations do not have bankruptcy problems (although their number of active users, economic activity and the price of issuing tokens can tend to zero), and their sponsors and operators will not face the constraints from creditors as the company owners and managers do. For distributed autonomous organizations, it is also impossible to introduce terms such as debt to equity swap and preferential liquidation. Secondly, the VAM clause is one of the important means to protect the rights and interests of investors, and it is an agreement between the investment and financing parties on the uncertainty of the future (mainly reflected in the performance of the financing party). However, due to the lack of a decentralized oracle, it is difficult to reliably write performance information outside the blockchain into the blockchain, and it is also difficult to use smart contracts to implement gambling terms.

Third, Token's quick liquidation mechanism has affected the interest binding of both parties of blockchain project investment and financing. In reality, the premise of many investment and financing terms is that equity cannot be transferred. The illiquidity of equity binds the interests of both investment and financing parties together, encouraging them to work together. Their equity may not be realized and withdrawn until the company is listed.

In contrast, the token of the blockchain project has a much lower standard for listing on the cryptocurrency exchange. When many blockchain projects were still in the white paper stage, the Tokens held by early investors and project teams could be realized through cryptocurrency exchanges, and their motivation to seriously do projects after the realization of Tokens might be significantly reduced. In many blockchain projects, because the position of Token holders in project governance is relatively vague, the quick liquidation mechanism of Token is more detrimental to the interests of both investment and financing parties. Benedetti and Dostoevsky (2018) measured the activity of the Twitter account of the ICO project. Only 2% of the ICO projects were active 120 days after the ICO. The quick liquidation mechanism of Token is also one of the important sources of various speculation, speculation and even fraud activities related to ICO.

Fourth, the combination of on chain governance and off chain governance. Intra chain governance is characterized by address anonymity, a de trusted environment, and automatic execution of smart contracts. Out of chain governance is characterized by real identity, integrity records, trust and reputation formed by repeated games, informal social capital and social punishment, and formal legal protection. Whether the two types of governance can be effectively combined is a complex problem that needs further study.

(5) Performance and security of blockchain system

Some scholars have made valuable research on the performance and security of the blockchain system from the perspective of economics. First, the "triple paradox" of blockchain That is, no blockchain system can simultaneously have the three characteristics of accuracy, decentralization and cost efficiency. The theoretical analysis of Abadi and Brunnermeier (2018) shows that the centralized ledger has accuracy and cost efficiency, its maintainers can obtain monopoly rents, and the franchise value encourages them to keep accurate accounts. The distributed ledger gives rewards to accounting nodes to encourage them to keep accurate accounts, but selecting accounting nodes through POW sacrifices cost efficiency. The transferability of information between blockchain forks and the competition among "miners" will lead to "forked competition". "Bifurcation competition" helps to eliminate the monopoly rent enjoyed by a single blockchain system, but it may also bring instability and disharmony.

Second, the pros and cons of POW. POW represented by Bitcoin is still the mainstream consensus algorithm in the blockchain, and the security and stability of POS have not been tested for a long time as POW. Biais et al. This will lead to an "arms race" of "mining" computing power and cause excessive investment in the field of "mining". Ma et al.

Third, the economics of POW "mining", especially the influencing factors of transaction rate. Houy (2014) theoretically studied the economic problems faced by bitcoin "miners" when packaging transactions. On the one hand, the more packaged transactions, the more likely "miners" are to receive fees. On the one hand, the more packaged transactions, the larger the blocks, and the longer it takes for blocks to spread in the distributed network and become blockchain consensus, the more likely they will become "isolated blocks". The game analysis of the two "miners" found that, under certain parameter assumptions, both miners can dig "empty blocks" (that is, do not pack any transactions), which can become a game equilibrium. The response is to increase the service charge rate. Huberman et al. (2017) studied the impact of the physical performance of the Bitcoin system on users and "miners". Users hope that their transactions can be processed as soon as possible. In the case of limited physical performance of the system, they will increase the transaction rate to attract "miners" to process their transactions first. The "miners" also have the power to maintain the infrastructure of the Bitcoin system under economic incentives. Therefore, the limited physical performance is an important guarantee for Bitcoin system to maintain operation in a decentralized environment. Easley et al. (2018)'s empirical analysis of the Bitcoin system from 2011 to 2016 found that the more congested the Bitcoin system (measured by the size of the Bitcoin memory pool and the average waiting time before transactions are written to the blockchain), the less likely the transactions with a transaction rate of 0 are to be written to the blockchain, and the higher the average rate of transactions written to the blockchain.

Fourth, on the economic security boundary of the blockchain. Budish (2018) studied the security of the POW based public chain represented by Bitcoin from the perspective of withstanding attacks, and proposed several economic incentives to improve security. The author believes that the higher the economic importance of such blockchains (for example, assuming that the market value of Bitcoin is close to gold), the higher the possibility of malicious attacks on them. Therefore, we should be suspicious and cautious about the large-scale application of the public chain. Enterprises and governments have cheaper technology in data security than the public chain.

4、 Summary

This paper analyzes the functions of blockchain from the perspective of economics, summarizes the "Token paradigm" adopted by the current mainstream blockchain system from the perspectives of Token, smart contract and consensus algorithm, and gives an economic explanation. 1. Token is a state variable defined in the blockchain and has several characteristics similar to currency. Token transactions within the blockchain do not need to rely on trusted third-party institutions, but this trust free environment within the blockchain cannot extend beyond the blockchain. Once breaking away from the original scenarios such as Token transactions, the blockchain often needs to introduce a trusted center mechanism outside the blockchain to help solve the trust problem in reality.

2. Smart contracts run in the blockchain The computer code that mainly performs complex operations on the Token can realize the functions of the definition, issuance, destruction, transfer, mortgage, freezing and unfreezing of the Token, but it cannot ensure the performance of the debts in the blockchain, and it is also difficult to deal with incomplete contracts. At present, the limited running environment in the blockchain makes this kind of code far from reaching the intelligent stage.

3. The consensus algorithm aims at the information related to the status and transaction of the token, and ensures the authenticity and accuracy of such information. However, the information irrelevant to the status or transaction of the token in the blockchain is basically not within the scope of consensus. In particular, the writing of information outside the blockchain into the blockchain only means that the information is open on the whole network and cannot be tampered with, which cannot improve the authenticity and accuracy of the information at the source. At present, there is no decentralized prediction function that can truly and accurately write information outside the blockchain into the blockchain.

Based on the "Token" paradigm, this paper analyzes four main application directions of blockchain: 1. Currency free blockchain. Such applications play the public sharing ledger function of the blockchain to improve the efficiency of division of labor and collaboration, and do not directly involve the transfer of property rights and risks. The main problem is how to ensure the authenticity and accuracy of information outside the blockchain at the source and in the blockchain link. The alliance chain is more suitable for such applications than the public chain because it is only open to authorized nodes and relies on the constraints of the real world.

2. Tokens traded in non-public offerings represent assets or rights outside the blockchain to improve the registration and transaction process of these assets or rights. However, a token is only a piece of code in physics. Whether a token corresponds to an asset or right outside the blockchain, and whether the status and transaction of a token have binding force or influence on the real world outside the blockchain, depends on whether the laws and systems outside the blockchain endow a token with meaning beyond the blockchain.

3. Economic activities based on the legal framework outside the blockchain, with the token of public offering transaction as the pricing unit or underlying asset. Because it is difficult to accurately evaluate the intrinsic value of Token based on fundamentals, such applications can only refer to the price of Token in the secondary market, but the price of Token often shows high volatility, which limits the development of such applications.

4. Build distributed autonomous organizations with blockchain. There are no widely recognized successful cases in this regard so far, which are mainly subject to the following obstacles: the physical performance of the public chain is not high enough to support large-scale transactions; Functional weaknesses of smart contracts; The high volatility of Token price limits the effectiveness of Token as a payment tool and incentive means; The design of encryption economics model is unreasonable.

When analyzing these main application directions of the blockchain, this paper also discusses the economic issues involved and summarizes the relevant research: 1. Token's characteristics of similar currencies, including the performance of cryptocurrency as a payment tool, the price characteristics of the secondary market, the test of stabilizing cryptocurrency, and anti money laundering issues related to cryptocurrency; 2. The impact of Token on the financing and development of blockchain platform projects, and the dual role of Token cause the intrinsic instability of the price of Token; 3. The governance functions of the blockchain, including the design of equity based token, the impact of token price fluctuations on the incentive mechanism based on token, the impact of the functional weakness of smart contracts on the migration of governance mechanisms in the real world to the blockchain scenario, and the impact of the quick liquidation mechanism of token on the interest binding of both parties in blockchain project investment and financing; 4. The performance and security of the blockchain system, including the blockchain's "ternary paradox", the pros and cons of POW, the economic problems of POW's "mining", and the economic security boundary of the blockchain.

In general, there are few blockchain projects that have actually landed and generated social benefits. In addition to the low physical performance of blockchain, the weakness of blockchain economic functions is also an important reason. On the basis of continuous research and experiment, we should rationally and objectively evaluate what the blockchain can and cannot do.

First, do not exaggerate or superstition the functions of blockchain. The industry practice over the years has proved that some blockchain application directions are infeasible. In particular, the modern financial system has constantly absorbed various technological innovations in the process of development. Technological innovation will be integrated into the financial system as long as it helps to improve the efficiency of financial resource allocation and the security and convenience of financial transactions. So far, no technological innovation has had a disruptive impact on the financial system, and blockchain is no exception. The supply of cryptocurrency is inflexible, lacking internal value support and sovereign credit guarantee, unable to effectively perform monetary functions, and impossible to subvert or replace legal tender. The anonymity of blockchain will increase the difficulty of implementing anti money laundering (AML) and "Know Your Customer" (KYC) in financial transactions. However, it should also be noted that some of China's national conditions provide opportunities to practice blockchain, such as the digital bill trading platform, which helps to alleviate the problem of decentralization of China's bill market.

Second, blockchain applications should be based on the actual situation and not be restricted to some overly idealistic purposes. For example, it is very difficult to replace system and trust with technology, which is even utopia in many scenarios. For another example, decentralization and centralization have their own applicable scenarios, and there is no difference between advantages and disadvantages. In reality, complete decentralization and complete centralization are rare. Many blockchain projects start from the purpose of decentralization, but later they more or less introduce the element of centralization, otherwise they cannot be implemented. For example, writing information outside the blockchain into the blockchain often requires a trusted centralized organization, and complete decentralization is impossible.

Third, the current blockchain investment and financing field has obvious bubbles, and speculation, market manipulation and even illegal activities are common, especially for Token projects involving public offerings. Relevant government departments should strengthen supervision and prevent financial risks.

This article comes from the Working Paper of the People's Bank of China

(About the author: Xu Zhong, Director of the Research Bureau of the People's Bank of China)