Under the internal pressure and external volume, the domestic new energy vehicle pattern still has great changes.

Under the internal pressure and external volume, the domestic new energy vehicle pattern still has great changes. Welcome to follow the WeChat subscription account of "Sina Technology": techsina

Wen/Chu Wanbo

Source: Cybercar

The competition in the domestic new energy vehicle market is increasingly fierce. During the National Day holiday, major new energy vehicle enterprises successively released their sales reports in September:

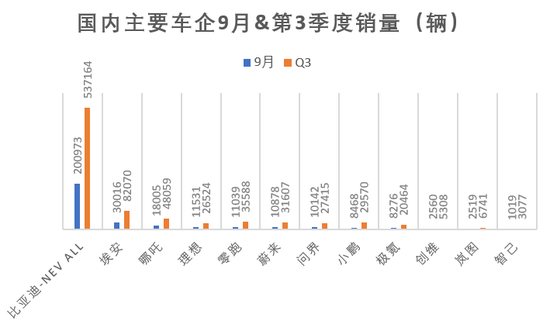

BYD took the lead with no unexpected absolute advantage. The sales volume in September was 200973, and the sales volume in a single month exceeded 200000.

Ai'an also maintained a strong growth trend, with the sales volume of 30016 vehicles in September, crossing the threshold of delivering more than 30000 vehicles in a single month for the first time.

The most miserable player of the last month, the Ideal Car, returned strongly with the support of the new car L9, and delivered 11531 vehicles in September, of which the Ideal L9 delivered 10123 vehicles in the first full delivery month.

See the detailed delivery information together.

01

BYD's monthly sales exceeded 200000 for the first time, a strong reversal of its ideal

According to the sales volume of September and the third quarter disclosed successively, the automobile enterprises are roughly ranked as follows:

As the flag bearer of the domestic new energy vehicle market, BYD still shows an absolute advantage over its friends.

According to official data, BYD's sales volume in September was 20.1 million, up 154.3% year on year and 15.5% month on month. This is also the first time that BYD's monthly sales exceeded the threshold of 200000 vehicles.

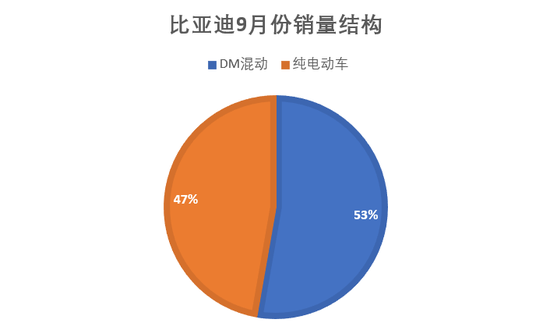

Among them, the sales volume of DM hybrid models was 106000, and that of pure electric vehicles was 95000, accounting for 53% and 47% of the total sales respectively.

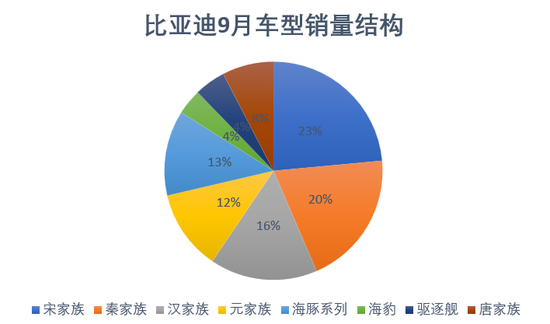

As for specific models, BYD's main sales models in September: Song, Han and Qin series sales continued to be hot. BYD Song sold 46000 vehicles in a single month, accounting for 23% of the total sales; The Qin family followed closely, selling 39500 new cars in September; Han Family is the third major model of BYD. It sold 31500 vehicles in September, which is the first time that BYD Han sold more than 30000 vehicles in a single month.

At the same time, BYD officially disclosed that the average transaction price of BYD Han has reached 250000 yuan. So far, Han series has become a high-end model with the sales volume of more than 30000 vehicles in the first month.

In addition, BYD Yuan and Dolphin series also showed a strong growth momentum with sales of more than 20000 vehicles per month.

In the whole third quarter, BYD's cumulative sales reached 537000 vehicles. From January to September this year, BYD's cumulative sales exceeded the million mark, reaching 1175300 vehicles. This data performance is not only the domestic market, but also the global new energy vehicle market.

In addition to BYD, the following auto companies also showed strong growth trends and highlights in the competition in September.

First, GAC Ai'an ranked second. The sales volume in September reached 30016, up 121% from the same period last year, and 11.1% from August this year. At the same time, this is the first time that the sales volume of Ai'an brand exceeded 30000 vehicles in a single month.

In the third quarter of this year, the cumulative sales volume of Ai'an brand reached 82070, and the sales volume from January to September this year reached 182000. Moreover, from the perspective of the general trend, after April, Ai'an has entered a relatively fast and stable growth period. Whether from the growth trend or the absolute number, Ai'an has already had a leading position in the new energy vehicle sub brands of a number of traditional vehicle enterprises.

In addition to the impressive data performance, Ai'an is also focusing on adjusting the sales structure and improving the brand strength.

The sales structure of Ai'an has shown a more healthy state. Previously, the market generally believed that the online car hailing market was an important factor to stimulate the sales growth of Ai'an, but now look again, the sales of the B end market of Ai'an has accounted for very little.

GAC said to Cybercar that at present, the operating vehicles at the B end of Ai'an account for only 2%, the online car hailing purchased by individuals at the C end accounts for 10%, and the remaining 88% of sales are non operating consumption at the C end.

For the high-end market of 300000 yuan, Ai'an also officially started to work.

Not long ago, Ai'an released its high-end product series Hyper, and next year, there will be three models under this series, including coupe, SUV and MPV.

It remains to be seen whether Hyper can help Ai'an reach the high-end.

Nezha ranked third. In September, it delivered 18005 new cars, an increase of 134% over the same period last year and 12.4% over August.

In the third quarter, Nezha delivered 48059 new cars. So far, from January to September this year, Nezha has delivered 111190 new cars, an increase of 168% over the same period last year, becoming the first player among the new car makers to deliver more than 100000 cars this year.

In terms of long-term trend, Nezha has formed obvious advantages over other new car making forces in terms of sales volume. The key to success is the low-end market with long-term potential of about 100000 yuan.

The most striking thing is the ideal car. Last month, the delivery of less than 5000 cars fell by half. In September, the delivery of 11531 cars strongly reversed the decline, with an increase of 152.3% month on month and 62.5% year on year

In the third quarter of this year, the ideal has delivered 26524 new cars in total. By the end of September, the ideal has delivered 86927 new cars in total.

It should be noted that, due to the discontinuation of the production of the ideal ONE, this wave of growth is almost purely created by the ideal L9 single model. The data shows that the delivery data of the ideal L9 in September is 10123 vehicles.

You should know that September is the first full delivery month of the ideal L9. As an SUV with a price of 400000+, this delivery performance is really good.

In addition to these four players, this time there is a relatively strange brand that has entered the top ten in sales volume Skyworth Auto.

Data shows that Skyworth delivered 2560 vehicles in September, up 60% month on month from 1589 vehicles last month. So far, Skyworth has also successfully pushed its new brand Landu Automobile out of the top ten.

Compared with new mainstream players such as Weixiaoli, Skyworth has been small and transparent in the car circle for a long time. Therefore, it is also necessary to pull out this strange player to see clearly the past and present life.

According to public data, Skyworth is a new brand of Volvo Car Group entering the passenger car market, and its predecessor Tianmei Auto was founded in 2019. Until last March, Kaiwo Group and Skyworth Group reached a Skyworth trademark transfer, and Skyworth Auto brand was officially released.

Skyworth is currently selling two SUV models, Skyworth EV6, a pure electric model, and Skyworth HTi, a hybrid model. EV6 was released in July last year, and HTi was launched in September last year.

From the price point of view, the price of the two models is between 150000 yuan and 27000 yuan, focusing on the high-end market.

From this point of view, Skyworth is a younger player in the new force. Whether Skyworth can continue to grow and occupy a place in the market in the future deserves attention.

02

The market is in a critical period of reshuffle due to the scuffle of new car making forces

In addition to the current sales figures, what is more important is the new changes hidden behind the figures: the new car making forces are under internal pressure and external pressure, and the shuffle period is coming.

First of all, the listing of ZeroRun Auto in Hong Kong is a landmark event. The first to face the pressure should be Nezha Auto, which is currently in the limelight.

As a new force auto enterprise that started to produce at the same time as Zero Run, Nezha's delivery level has grown strongly since 2022. Until the last three months, it has formed a stable sales advantage for Weixiaoli.

But the question is, can this sales advantage be transformed into an advantage at the operational level? After all, for the new forces, the profit and loss balance is the ultimate measure.

As mentioned above, up to now, Nezha has two main models: the starting price of the Nezha U is 123800 yuan, and the starting price of the Nezha V is only 79900 yuan, mainly for the middle and low-end market.

It is worth noting that, according to the data of insured volume in the past, Nezha V with lower price has accounted for more than half of Nezha's sales for a long time.

The sales structure dominated by low-end models is likely to lead to a breakthrough in volume, but in terms of profitability, it is naturally lower than the high-end models with higher prices.

This problem has already been exposed in the prospectus of Zero Auto. According to the gross profit rate disclosed in the prospectus in recent three years, the zero gross profit rate from 2019 to 2021 will be - 95.7%, - 50.6% and - 44.4%, respectively. By the first quarter of this year, the gross profit rate will still be - 25.21%. Even as of the first quarter of this year, the average selling price of Zeroing cannot cover the cost of automobile materials.

This method of exchanging low prices for sales has obviously begun to arouse doubts in the capital market. The IPO performance of Zero Run is the best proof. The stock price has dropped to HK $24.8 per share by the end of the day, nearly half of the opening price of HK $48 per share.

Of course, Nezha is also striving for brand advancement internally. The Nezha S to be delivered in the fourth quarter is the key to the middle and high-end market.

However, from the current order volume of Nezha S, it seems not optimistic. Official data show that as of September 30, the cumulative order volume of Nezha S was only 15000+.

In contrast, the price range of C01, which is basically the same as that of Nezha S, has officially revealed that the order volume has exceeded 100000 vehicles.

In addition to Nezha, there are three other companies facing internal competitive pressure, namely Toutou Weixiaoli.

Recently, Weixiaoli has successively released new cars and started delivery. First of all, Weilai took the lead in bringing out the new SUV Weilai ES7 in the middle of June. At the level of order volume, Weilai's tradition is never disclosed, but Li Bin also disclosed at the latest quarterly financial report meeting that the orders for Weilai ES7 and ET5 are very sufficient. At the same time, when only 50000 cars were delivered in the first half of the year, we still adhere to the delivery target of 150000 to 200000 cars in the whole year.

In other words, in the last three months of this year, the average monthly delivery volume of Weilai must reach about 23000 vehicles to reach the goal.

Next is Ideals. As the most radical player of the volume, Ideals L9 was first launched at the end of June, and then unveiled a new car in the Taowa style on the eve of the National Day. Ideals L8 and L7 all appeared and released prices, and it was determined that Ideals L8 would be delivered in November this year.

Among them, on the eve of the start of delivery, the number of orders of the ideal L9 has exceeded 50000. From the performance of delivering more than 10000 in the first full delivery month, in the context of the ideal ONE production suspension, L9 has really played a strong role in the ideal delivery. After the delivery of L8 next month, it is expected to usher in another wave of delivery growth.

Finally, the late arrival of Xiaopeng Automobile. Xiaopeng G9 had previously opened blind ordering on August 11, and its order volume exceeded 20000 vehicles in 24 hours. Although there was a wave of unsubscription after the press conference, the situation has been alleviated after the rapid change of sales strategy. It was revealed that after Xiaopeng G9 changed its sales strategy, the order volume of a single store increased by at least 50%.

It can be seen that several SUVs released intensively by the three companies in Weixiaoli recently, no matter in terms of price, size or delivery time, have some overlap with each other. The pressure brought by each other has reached the level of visible to the naked eye.

In the next three months, it is likely to be the most intense period of competition between the new car building forces.

In addition to internal pressure, the new force of car manufacturing is also facing the external volume of traditional OEMs. The volume here is mainly reflected in the fact that traditional car enterprises have made up for the shortcomings of intelligence, and played the advantages of vertical integration and cost control.

Since this year, the traditional car enterprises have quickly supplemented the shortcomings of intelligence through the self research+outsourcing scheme, which has gradually weakened the leading advantages of new forces in intelligent driving and digital cockpit.

In high-end models, traditional car companies, like the new car making forces, also carry intelligent core functions such as voice interaction, pilot assistance, and auto parking.

Against this background, the new force of car building is also facing the pursuit of many independent new brands of traditional car companies. For example, Geely's Geekrypton delivered 8276 cars in September, less than 200 cars behind Xiaopeng.

As for the Siris Quest brand, which is supported by Huawei Intelligent Selection, the delivery level continued to rise in September, reaching 10142 vehicles, and the sales volume exceeded 10000 for two consecutive months. In addition, the latest model M7 of Wenjie brand has been sold in advance since its launch. Yu Chengdong previously disclosed in July that the order volume of M7 has exceeded 50000.

As a new car benchmarking with the new models launched in Weixiaoli in terms of price and size, M7 will undoubtedly exert pressure on Weixiaoli's next incremental tasks.

With the improvement of product strength, the cost control advantages of traditional automobile enterprises are gradually emerging.

Taking BYD as an example, from the three electric systems to the body parts, all have considerable vertical integration capabilities. This allows BYD to control the cost at a lower level in large-scale production and fight against new car making forces with a higher cost performance ratio.

In terms of cost control, don't forget that there is another killer, Tesla, which controls costs through a large number of automated production. At the beginning of the National Day holiday, Tesla took the lead in raising the price butcher's knife and reduced the price in a disguised way by means of an insurance subsidy of 7000 yuan.

It can be said that under internal pressure and external volume, the domestic new energy vehicle market pattern is still facing considerable variables. It can be predicted that in the last quarter, the new car building forces will face severe competitive pressure. How will the ranking of the top ten new energy vehicle enterprises change in the coming months? Let's see it again in November.

(Statement: This article only represents the author's view, not Sina.com's position.)