Welcome to follow the WeChat subscription account of "Sina Technology": techsina

Wen/Chen Wenqi

Source: AlphaSeeker (ID: deep_insights)

The automatic driving industry is following the old path of the AI track: from easy valuation to bubble clearing, from genius worship to pragmatic progress, from superstition growth to focus on the fruits of the moment, from tall laboratories to fields, warehouses and ports.

Last week, there was a new news that WeRide, an autonomous driving company, announced that it had obtained strategic investment from Bosch, an auto parts supplier. In March, the company was rumored to have completed a new round of financing of more than 400 million dollars, with a post investment valuation of 4.4 billion dollars.

In official terms, the significance of this strategic cooperation is that "after the research and development and implementation of L4 level automatic driving technology, Wen Yuanzhixing has officially entered the development and application of L2-3 level automatic driving technology, and jointly promoted high-class intelligent driving with Bosch China, which is of vehicle scale and mass production."

The steering is obvious. The main scene of this auto pilot star company used to be L4, but now it has "reduced maintenance" to mass production of L2-L3. At the same time, the background of investors has also changed, from venture capital institutions to actively embrace strategic investors in the industry.

Wen Yuanzhi's shift to practice is a footnote to the changes in the industry.

"From the beginning, the whole industry is talking about advanced technology, grand concepts and eye-catching stories, becoming more and more focused on immediate orders and partners, with the goal of improving the degree of commercial landing more quickly." Cao Fangning, partner of Multidimensional Capital, told Zhen Tan that Multidimensional is the exclusive financial consultant for many autonomous driving projects such as Chase Technology.

"Autopilot start-ups are going to build up from a single story telling and concept telling (Established) Industry ecology, or put yourself into the whole industry ecology to think about problems. More emphasis is placed on survival and making money, not just on technical positioning. " She shared.

Due to the cold capital environment, increasingly full industry competition, accelerated industrial chain integration and other reasons, the automatic driving practitioners have changed. "Survival", "making money", and "commercialization" have replaced "technology" as the most concerned keywords.

These trend changes have already been staged on the AI track. At this time, the ups and downs of the AI track are a warning and hope.

Driverless cars in the film minority report

Driverless cars in the film minority report Capital no longer worships genius

The concept of "autonomous driving" is related to "travel", and it is one of the largest application branches of AI technology. With its own futuristic color, it has attracted technology giants and investors since its appearance.

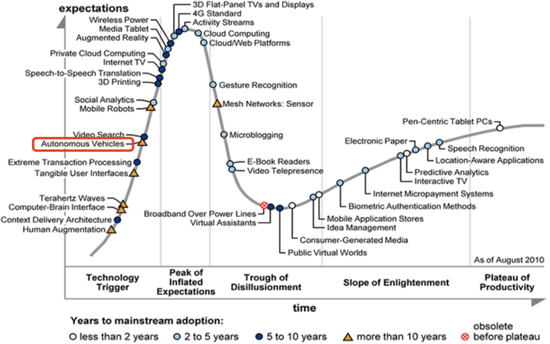

Since 1995, the consulting company Gartner has published the technology maturity curve every year. A new technology will go through five stages: technology germination, expected expansion, bubble burst trough, steady climb and production maturity. In 2010, autonomous vehicles appeared on this curve for the first time, and talent and hot money quickly flowed into the industry, entering the "expected expansion period".

In 2010, autonomous vehicles first appeared on the Gartner curve Source: Gartner

In 2010, autonomous vehicles first appeared on the Gartner curve Source: Gartner Around 2017, the automatic driving industry reached its first climax.

At that time, a large number of star start-ups had been established, including Waymo, Aurora, Argo.AI, which were separated from Alphabet. In China, there were Xiaoma Zhixing, Momenta, Tucson Future, Wenyuan Zhixing, etc. Baidu established Apollo, and Didi also began to build an automated driving team.

At this stage, the concept of automatic driving was extremely "sexy and hot". The industry was bright and full of optimism. This group of autonomous driving companies run by technology giants were ambitious, almost all of them "leapfrog" straight to L4/L5, and "replacing human drivers" seemed to be close at hand.

However, compared with AI, automatic driving is more expensive and difficult to land.

As a result, the phenomenon that contradicts the business logic appears: on the one hand, the capital and media are holding up various concepts and overvalues, accompanied by bubbles, For example, in 2018, Morgan Stanley once valued Waymo at $175 billion, including $80 billion for Robotaxi business, $90 billion for truck logistics business, and $7 billion for software business; On the other hand, there are all kinds of difficulties encountered by bottomless R&D investment and technology implementation, such as policies and regulations, complex road conditions, safety accidents, etc.

The automatic driving industry needs to solve two basic problems, safety and cost. The former is the lifeline, and the latter is the root of business development. But at that time, there was no suitable solution for either.

In March 2018, a Uber driverless car hit a pedestrian in a road test, killing him, which was the first driverless car fatality in the world. After the tragedy, the Uber road test was suspended for 9 months. The attribution of the incident has been controversial so far, and the bubble of the automatic driving industry has been punctured at the cost of blood and tears.

In 2019, the Morgan Stanley report reduced the valuation of Waymo by 40% to $105 billion, a direct cut of $70 billion, because "the overall commercialization of the automated driving industry is not as fast as expected". Of course, this is still an overly optimistic figure. By 2020, Waymo will obtain external financing of $2.25 billion for the first time. According to FT, the valuation of this round of financing is only $30 billion. The parent company Alphabet's 2020 financial report shows that in 2020, other investment departments (including Waymo) spent up to 4.5 billion dollars.

Seeing the collapse of the leader Waymo's 100 billion valuation story, the driverless car has been unable to get on the road. Commercialization is still far away. Capital no longer worships talents and dreams, but becomes pragmatic, focusing on landing scenarios and commercialization possibilities.

The attitude change of capital is caused by multiple factors.

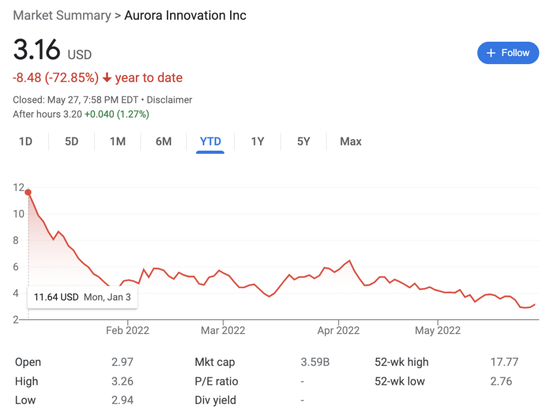

First, the serious valuation inversion in the primary and secondary markets caused reflection and adjustment on the valuation system of autonomous start-up companies. The two star autonomous driving companies listed last year have performed miserably in the secondary market, both of which have declined by more than 70% since this year. Although there is also the overall weakness of technology stocks and the impact of the Federal Reserve's tightening policy, the core reason is that the secondary market does not pay for the huge losses of autonomous driving companies.

Moreover, the automatic driving industry has basically gone through the stage of venture investment. Now, PE is more likely to see automatic driving projects, and they prefer companies with high certainty when making choices.

For start-ups themselves, being more pragmatic is also an inevitable choice. In particular, most of the companies established around 2016 that have survived have gone through multiple rounds of financing, and the pressure on commercialization has multiplied.

Aurora's share price trend since this year

Aurora's share price trend since this year At the same time, over the past decade, the entire automotive industry chain has also been reshaped in the wave of electrification and intelligence. As the most symbolic technology of intelligence, automatic driving has become the "battleground". From upstream chips and other important parts, OEM OEMs, new energy vehicle enterprises, software platform companies, and Internet giants, automatic driving companies are also cooperating with strategic investors to complete systematic cultivation.

All this is to make technology come true.

The difficulties encountered by automatic driving companies in the primary and secondary markets and industries are quite similar to those of AI companies: the company's high investment, high loss and high valuation coexist, and the valuation of the primary and secondary markets is inverted; In the industry, AI has become the bottom technology, the competitive advantage of start-ups has weakened, and there are many obstacles to commercialization and scale. AI has entered a steady growth period after experiencing cold winter and foam collapse, which is naturally a positive enlightenment for the automatic driving industry.

See the inflection point again?

In recent years, the popularity of automatic driving has obviously returned, and the commercialization path of each company has become clearer. Since this year, there has been a lot of good news in China.

In terms of financing, the popularity of 2021 has continued. In the case of poor capital environment, financing is frequent. Since this year, more than 20 companies have received new financing. Among them, in April, the A round of Ruqi Travel, a subsidiary of GAC, financed 1 billion yuan, indicating that it would accelerate the promotion of Robotaxi; The number of "Zhixing" round A exceeds 1 billion; ADAS (Advanced Driving Assistance System) has started to expand its technology to more than 1 billion E-wheels; Wen Yuanzhixing's D-round investment of 400 million US dollars has seen a lot of money.

Policy support and the landing of driverless vehicles. In April, Beijing released the Implementation Rules for the Management of Unmanned Road Test and Demonstration Application of Passenger Vehicles in the Beijing Intelligent Connected Vehicle Policy Pilot Area, and Baidu's "unmanned behind the steering wheel" team went on the road. Xiaoma Zhixing announced that it won the bid for the taxi capacity index of Nansha District in Guangzhou in 2022, which is the first taxi business license issued to an autonomous driving enterprise in China.

Assisted driving on the vehicle is also in progress. According to IDC's China Auto Driving Passenger Vehicle Market Data Tracking Report, the penetration rate of domestic L2 level auto driving in passenger vehicle market in Q1 will reach 23.2% in 2022.

With a thriving scene, the "inflection point theory" appeared again.

Zhang Kai, Chairman of Nawei Zhixing, said in a public speech: "2022 will be the most critical year for the development of the automatic driving industry. The competition in the field of passenger vehicle assisted driving will officially enter the second half, and automatic driving in other scenes will also officially enter the first year of commercialization."

Coincidentally, in April, Peng Jun, CEO of Xiaoma Zhixing, also proposed that "the turning point of automatic driving is coming". Yu Qian, founder and CEO of Qingzhou Zhihang, said at the brand conference in May: "The automatic driving industry is ushering in a golden turning point of development. Policies and regulations are becoming more friendly, technical algorithms are becoming more powerful, sensors and computing are moving closer to the vehicle specification level, and industry advocates are growing."

Has the turning point really come?

In terms of objective conditions, all important links of automatic driving technology are improving, such as chip computing power, 5G Internet connection, data volume, high-precision maps, radar, etc., and the cost is also decreasing. For example, the price of laser radars has now reached 1000 dollars from tens of thousands of dollars. According to ICVTank's prediction, the price of laser radars will drop to 500 dollars in 2025, a drop of 97.5% compared with 2018.

On the policy side, the laws and regulations of various countries have gradually improved and played a leading role. For example, Germany passed the L4 Automatic Driving Act last year, allowing L4 level completely driverless cars to appear on public roads in 2022.

Industry integration and elimination accelerated, and the market also made a choice to keep companies with technical, engineering and commercial strength in the industry.

"The so-called inflection point is actually a so-called knockout game, a shuffling stage of ranking." Cao Fangning said that she believed that this year and next, 5-10 autonomous driving start-ups will successively enter the secondary market, and each segment will form a clearer echelon camp.

Few companies can finally enter the narrow door, and commercialization is their necessary weapon.

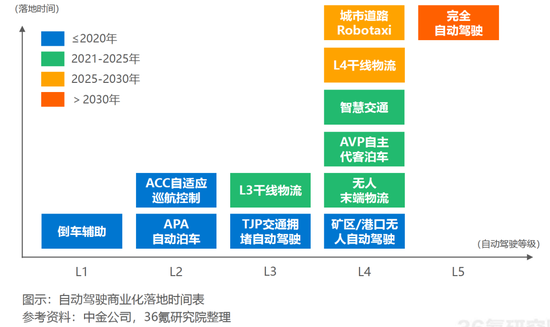

Now the landing direction of automatic driving has shown a clear map. Compared with the "Unmanned Vehicle" that initially went straight to L4, it is obviously more expensive and practical. According to the application scenarios, the automatic driving track is divided into two major markets: commercial vehicles and passenger vehicles; The latter is a manned application for C-end consumers. Due to the difficulty of technology application and legal restrictions, the commercial application of automatic driving usually follows the principle of carrying things first, then carrying people, and closing first, then opening up, and gradually launches.

Source of landing map of automatic driving commercialization: Research Report on China's Automatic Driving Industry from 2021-2022 by 36 Krypton Research Institute

Source of landing map of automatic driving commercialization: Research Report on China's Automatic Driving Industry from 2021-2022 by 36 Krypton Research Institute In the fields of commercial vehicles and logistics, specifically, in the closed low-speed scenarios such as trunk lines (long-distance truck transportation on trunk roads), end lines (short distance distribution connecting end users) and ports, mining areas, and warehouses, automatic driving is landing quickly. For example, in the port transportation scenario, according to the data of the Ministry of Industry and Information Technology, as of September 2021, the proportion of automatic driving applications of large port freight vehicles in China has reached 50%.

In terms of Robotaxi landing, this is one of the largest autonomous driving scenarios in the market. Now, new licenses are issued every year, and the scope of road testing and trial operation is expanding. Its driving environment is complex, with high technical requirements, and it is more difficult to achieve commercial landing. The precondition is the improvement of technology and policy, and the decrease of safety officer and hardware cost. Robin Li gave Baidu Robotaxibusiness a profit time point of 2025. According to public data, the cost of a single car of the Apollo Moon, which was released in June 2021, has dropped to 480000 yuan.

Robotaxi, made by technology companies, sells services, while auto companies sell cars for automatic driving. The former has less pressure on mass production and delivery, and chooses a leap forward development path. The latter has obvious advantages in manufacturing and commercial closed-loop.

Tesla, Weixiaoli and other new energy vehicle enterprises have a more aggressive respect for automatic driving, and have carried driving assistance systems that can be upgraded through OTA on their vehicles. However, many accidents have occurred due to excessive marketing packaging, confusion of concepts and immature technology.

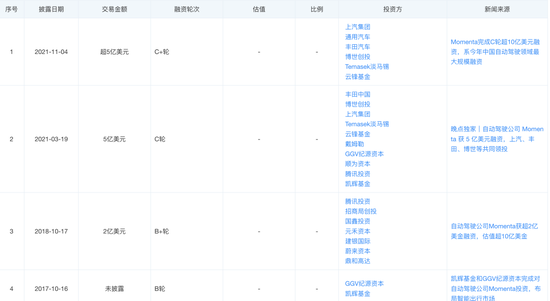

Compared with traditional automobile enterprises, they are not so "aggressive" in the field of automatic driving due to multiple self factors such as size, price system and internal system, but they are also entering the market through self research and investment. The object of its investment is mostly the autonomous driving unicorn, which is based on technology. For example, the autonomous driving startup Momenta, which raised $1 billion last year, has received a high degree of attention, and its investors are obviously more traditional car companies and other industrial institutions. GM even acquired Cruise in 2016, and continued blood transfusion to ensure its sufficient funds.

Momenta financing history source: Tianyancha

Momenta financing history source: Tianyancha Traditional car companies and autonomous unicorns take their own needs and complement each other. On the one hand, car companies need core technologies and Internet genes to speed up more advanced auxiliary driving functions; On the other hand, automatic driving companies just need landing scenarios and large-scale commercial cooperation. If technology is not integrated with industry, it is just a castle in the air.

Automatic driving, after all, is not a cool story of a company changing the world. Technical talents also have to go out of the laboratory to wrestle with complex road conditions, engineering forces, mass production, and the business world. In the next decade of automatic driving, the key word is pragmatism.

(Statement: This article only represents the author's view, not Sina.com's position.)