After getting on the horse.

After getting on the horse. Welcome to follow the WeChat subscription account of "Sina Technology": techsina

Wen/Zhangdao

Source: new knowledge of science and technology (ID: kejixinzhi)

Tencent Cloud can't sit still with naked eyes, and layoffs are only the most external performance.

Among Tencent's layoffs, CSIG (Cloud and Smart Industry Business Group) is the hardest hit area. According to multiple sources, the number of people may exceed 20%.

More importantly, the profit requirement. At the recent financial report meeting, Liu Chiping announced that cloud business should next move from increasing revenue at all costs to improving the quality of growth, so as to improve the profit margin.

Low profit is the most fatal weakness of cloud computing industry. Under the heavy pressure of profit indicators, some previous market actions of "increasing income without increasing profit" may be passively ineffective.

Especially under the current time node of Tencent - the fourth quarter of 2021, the revenue of financial technology and enterprise service business increased by 25% year-on-year to 48 billion yuan, surpassing online games for the first time and becoming the company's largest revenue source.

As Tencent's current golden bull game business, the financial report shows that in the fourth quarter of 2021, Tencent's online game revenue will be 42.8 billion yuan, and the game revenue in the local market will decline by 12% to 29.6 billion yuan.

When Tencent's ToB strategy is widely read by the outside world, layoffs and profit indicators appear to be very fragmented.

However, at the group level, this adjustment does have its due meaning. After the "930" reform in 2018, Tencent officially launched the ToB war. Now, the three-year novice period has passed. Tencent Cloud, who has been "promoted", needs to "transfusion".

Elephant turns

Previously, on May 14, 2021, CSIG announced a round of organizational adjustment. Under Tencent's official caliber, this adjustment is another major evolution of Tencent's ToB business after the "930 revolution".

It can be summarized as one sentence - "take root in the industry, cultivate the region, and improve efficiency". Taking "improving efficiency" as an example, it means that Tencent Cloud and the smart industry business group set up a business operation management department to promote the optimization of internal resource allocation.

This action can be regarded as a response of Tencent Cloud to the actions of its competitors. At that time, the personnel adjustment of Tencent Cloud was generally considered "weaker than expected" by the industry. Previously, Huawei and Alibaba Cloud had made similar adjustments.

Now, combining the action of layoffs and putting forward profit indicators, it reflects that the results of last year's adjustment are not satisfactory, which further indicates that Tencent Cloud has been aware of its own problems before.

Judging from the statements of the senior management, Tencent Cloud has been quite tangled about this in the past.

At the financial report conference in the first quarter of 2021, James Michel, the chief strategic officer, said: "If you are engaged in the cloud computing industry and rent infrastructure to a very large company, it is inevitable that large companies will use bargaining power to protect their economic interests."

The "bargaining power of large companies" mentioned here actually means that large cloud computing buyers exert pressure on IaaS pricing, which is the norm in the cloud computing industry. According to various evidences, the "big company" mentioned by Tencent is the third pole of domestic e-commerce - Pinduoduo.

In Youshu DataVision's analysis of Pinduoduo's 2021 financial report, it was mentioned that one reason why the book was profitable was that "Tencent Cloud, the server provider in the fourth quarter, sent a 'big red envelope' to Pinduoduo, a large cash returning account, and reduced some expenses."

According to Caijing, in April 2021, Pinduoduo added Baidu Cloud to its new cloud service provider in order to lower prices on the basis of Tencent Cloud.

In this regard, James Michel said: "Therefore, the way to obtain long-term economic returns in the cloud computing market is neither to seek rapid growth nor to pursue IaaS, but to cultivate PaaS and SaaS."

On Tencent's second quarter financial report conference call, James Michel did not respond positively when asked about the contribution proportion of FinTech and cloud computing business, only mentioned that currently Tencent Cloud is mainly focused on expanding customer penetration and market share, and does not aim at profitability for the time being.

In the end, Tencent Cloud chose to focus on profitability.

In the recent fourth quarter conference call, Liu Chiping mentioned Tencent's cloud business, including IaaS and PaaS, which is still in a net loss state. SaaS business has always had costs, but has not yet generated much revenue, so it is a loss making business.

This is basically in line with the agency's estimation. Previously, CITIC Securities had made a calculation in September 2020. From 2020 to 2022, Tencent Cloud's gross profit margin will still be negative, respectively - 14%, - 7% and - 7%.

In this regard, Liu Chiping proposed that Tencent Cloud migrate from IaaS to PaaS and SaaS (PaaS profit margin is higher than infrastructure service IaaS).

The reason behind this is that IaaS layer functions mainly include computing, storage, networking, etc. The high homogeneity of upstream hardware resources objectively determines the high homogeneity of IaaS products.

Therefore, on the basis of similar product use functions, price becomes the main factor affecting orders, which also causes cloud manufacturers' IaaS layer products to suffer losses.

In fact, it is not surprising that Tencent Cloud chooses to migrate from IaaS to PaaS in order to improve its profits.

According to IDC statistics, in 2019, PaaS accounted for 14.9% and 15.2% of the revenue structure of Alibaba Cloud and Tencent Cloud respectively, while in 2020, it accounted for 16.1% and 16.7% respectively, which indicates that domestic cloud manufacturers have long had this migration trend.

Return to ToB logic?

As we all know, subsidy was the most effective marketing method in ToC market. In previous Internet "wars", price subsidies can often quickly bring customers to open the market.

In essence, this model is to expand the market scale first and then consider the profitability issue under the leadership of capital advantage.

Now, this reckless and tough means of market competition is facing difficulties - bike sharing, community group buying and other industries have suffered failures.

Interestingly, since price subsidies can bring the most direct market effect, the marketing methods commonly used in the ToC market are also reused in the ToB market.

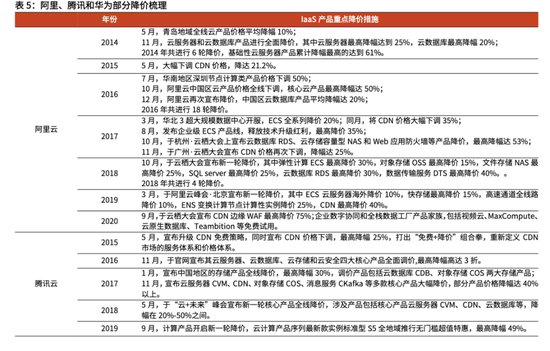

As early as 2013, the price war has been staged in the public cloud industry, and Tencent Cloud is a controversial existence.

At that time, Alibaba Cloud entered China through Amazon AWS. At first, Alibaba Cloud announced a full price reduction of its products, with a maximum reduction of 50%. It followed Tencent Cloud with a 60% discount promotion.

Later, in several price wars launched by domestic cloud manufacturers led by Alibaba Cloud and Tencent Cloud, Tencent Cloud gave Alibaba Cloud, the "leader", a headache.

Take the CDN market transformed by cloud manufacturers as an example. Before 2017, "CDN price reduction" seemed to be an essential part of every launch conference of cloud manufacturers.

In 2015, the CDN market was even more exciting. At that time, on March 26, Tencent Cloud took the lead in shooting the first shot in the market. At that time, the CDN2.0 version launched by Tencent Cloud provided customers with discounts, which could save 31% year on year.

In response, Alibaba Cloud announced a 21.2% reduction in CDN prices in May of the same year. Just a few days later, Tencent Cloud again played a combination of "free+price reduction", with a maximum reduction of 25%.

This is another heavy punch of Tencent Cloud after its price cut in March. This move will bring a great deal of free activities into the CDN service market.

With Tencent Cloud and Alibaba Cloud "falling more and more bravely" in the CDN market, traditional and small CDN manufacturers gradually left the battlefield after the frequent price war, and the former head players Netsuke Technology and Lan Xun were almost wounded.

More controversial actions are still to come. In March 2017, Tencent Cloud won the bid for the Xiamen government affairs cloud project with a budget of 4.95 million yuan at a penny.

A few days later, at the Yunqi Conference, Hu Xiaoming, president of Alibaba Cloud, said angrily, "Today, when everyone wants to promote the development of enterprises and make an industry, Ma Huateng and his team used a penny of bidding to destroy the industry."

In fact, Alibaba Cloud began to cooperate with 12306 in 2015, and also used the "no charge" cooperation method.

After Tencent Cloud, the industry has repeatedly seen "winning the bid at a penny". China Telecom, Alibaba Cloud, Inspur Information and other cloud service providers have also disclosed cases of low price bid winning.

Generally speaking, price war is often used in several games between Tencent Cloud and Alibaba Cloud.

Under this logic, the competitive strategy of Tencent Cloud is quite effective. Previously, the largest number of customers of Tencent Cloud came from the pan Internet industry, such as games, video and e-commerce. As Tencent Cloud's price cut is irresistible, Jinshan Cloud and UCloud, which have similar service groups, face market share loss.

In IDC rankings, in the first half of 2017 and the second half of 2018, Jinshan Cloud and UCloud disappeared from the top five of the public cloud IaaS market, while Tencent Cloud's market share rose from 9.6% to 11.8%.

Now, after several price wars, Tencent Cloud wants to pick up profits again. The first thing it faces is, can the previously spoiled customers pay?

This time is another time

On March 28, Huawei released last year's annual report at its headquarters in Shenzhen. At this financial report meeting, Meng Wanzhou introduced that Huawei Cloud will achieve sales revenue of 20.1 billion yuan in 2021, an increase of 34% year on year.

It can be calculated that the revenue of Huawei Cloud in 2020 is 15 billion yuan.

Summarize the cloud business revenue of last year disclosed by domestic mainstream cloud manufacturers: AliCloud 72.4 billion yuan, Huawei Cloud 20.1 billion yuan, Baidu Intelligent Cloud 15.1 billion yuan, and Jinshan Cloud 9.1 billion yuan.

Tencent Cloud is not one of them. The reason is that Tencent will not disclose its cloud revenue and growth rate after 2020. According to previous financial reports, Tencent Cloud's revenue in 2018 was 9.1 billion yuan, with a growth rate of more than 100%; In 2019, the revenue exceeded 17 billion yuan, up 87% year on year.

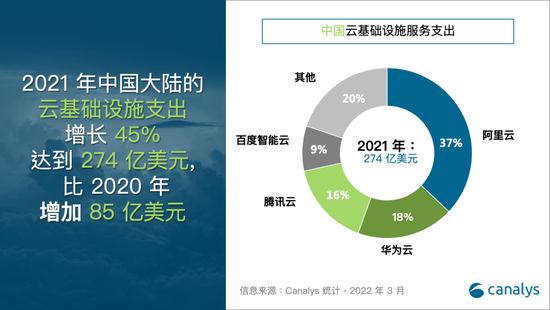

According to the data released by Canalys, a research company, the scale of China's cloud infrastructure service market will reach US $27.4 billion in 2021, of which Alibaba Cloud will account for 37%, Huawei Cloud 18% and Tencent Cloud 16%.

If so, Tencent Cloud's revenue in 2021 is at least on the same scale as Huawei Cloud. According to Dolphin Investment Research, Tencent Cloud's revenue in 2020 and 2021 is 21.06 billion yuan and 30.7 billion yuan, respectively, with a slowdown in growth, but it is still the second cloud manufacturer in China.

It should be noted that this time, Huawei disclosed the revenue scale of Huawei Cloud for the first time, which undoubtedly shows the ambition of cloud computing.

Today, under the power outage in the United States, developing cloud computing and creating an ecosystem with software as the port has become a way out for Huawei operators and consumers under the sluggish business growth.

Previously, under the IDC data caliber, in the third quarter of 2021, the market share difference between Tencent Cloud and Huawei Cloud's public cloud IaaS+PaaS is only 0.18%, and the difference in H1 is also only 0.3%, which is very weak.

It is conceivable that if Tencent Cloud wants to increase its profits as expected, it is bound to face the "wolf nature" of Huawei Cloud.

In addition, as a latecomer in the market, the addition of byte hopping will also intensify the fierce competition in China's cloud computing market. What's more, the primary service concept of volcanic engine cloud products is "pursuit of extreme cost performance", which will also intensify the price war to some extent.

In addition to competitors, we should also see that today, the cloud computing industry is "multi cloud" rampant.

RightScale's survey of global enterprise cloud strategy in 2019 showed that among large enterprises with more than 1000 people, 84% chose multi cloud deployment, of which 58% chose hybrid cloud.

For cloud customers, selecting "multi cloud" can spread risks. However, for cloud manufacturers, key customers often use the "multi cloud" strategy to avoid bundling while lowering prices, which is bound to increase the "price comparison" competition of cloud manufacturers. The Pinduoduo case above has verified this trend.

Previously, after 11 years of blood transfusion by the group, Alibaba Cloud, which had the advantage of first mover, finally became a regular EBITA in the fourth quarter of 2020 for the first time with a profit of 24 million yuan, and has been profitable ever since.

Similar to Alibaba Cloud, in the medium and long term, Tencent Cloud will be a growth point with high certainty for Tencent in the next decade, which is also the starting point for Tencent to increase profits.

But now, Tencent Cloud is bound to face multiple obstacles if it wants to become the next "Alibaba Cloud".

reference material:

Caixin Tencent Slimming

Caixin China Cloud Total War

(Statement: This article only represents the author's view, not Sina.com's position.)