Welcome to follow the WeChat subscription account of "Sina Technology": techsina

Wen/Li Ping

Source: Lishi Business Review

Original title: Xiaopeng Auto abandoned by investors

Lishi's introduction: After continuing to burn money and make huge losses, have Xiaopeng Motors really built a brand image and technical strength that can be called "moat" in the field of new energy vehicles?

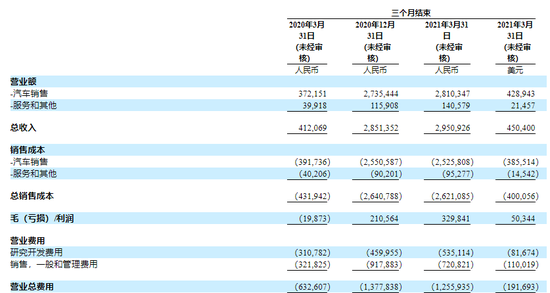

On May 13, Beijing time, Xiaopeng Auto released its financial report for the first quarter of 2021.The financial report shows that the total revenue of Xiaopeng Automobile in the first quarter was 2.951 billion yuan, an increase of 616.1% over the same period last year.Among them, thanks to the increase in the delivery of new cars, Xiaopeng's sales revenue reached 2.81 billion yuan, an increase of 655.2% over the same period last year.In addition, the company recognized the revenue of autopilot software of 80 million yuan for the first time.

However, despite the record high of revenue, vehicle delivery and other data, the "software charging" model was also highly publicized. Xiaopeng Auto closed the next day at a decline of - 4.93%, closing at $23.54, a new low for the year.Although the stock price of Xiaopeng Auto rebounded in the following days, since 2021, the biggest decline of Xiaopeng Auto's stock price has exceeded 50%.

Why didn't the secondary market applaud the multiple "good" of Xiaopeng Auto's first quarter report?

one

High expenses and increasing losses

In the first quarter, Xiaopeng Auto delivered 13340 vehicles in total, an increase of 487.4% compared with 2271 vehicles in the same period of 2020.Among them, 5366 units were delivered by Xiaopeng G3 and 7974 units were delivered by Xiaopeng P7.

It can be seen that the Xiaopeng P7 delivered in July last year contributed nearly 60% of the company's sales volume, becoming the key factor for the significant year-on-year growth of Xiaopeng's delivery in the first quarter.However, on a month on month basis, the growth rate of Xiaopeng's automobile delivery in the first quarter was only 2.9%, far lower than the average growth rate of the industry.

According to the production and marketing data released by the China Automobile Association, from January to March, the sales of new energy vehicles in China reached 515000, an increase of 23% from the fourth quarter of 2020.Among them, Tesla sold 69305 vehicles, up 20.4% month on month;The sales volume of Weilai was 20060, up 15.6% month on month.

Compared with several direct competitors in the same industry, Xiaopeng Auto's month on month growth rate is much lower, which also shows that the company's "high-speed" growth is more from a lower base.It can be predicted that with the continuous growth of the base, the decline of Xiaopeng's future revenue growth is probably inevitable.

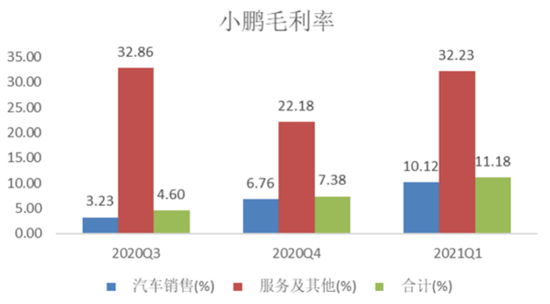

More gratifying is that the increase in delivery has indeed improved Xiaopeng's gross profit margin.The financial report shows that in the first quarter, the comprehensive gross profit rate of Xiaopeng Automobile was 11.2%, significantly higher than that in the same period of last year (- 4.8%) and the fourth quarter of 2020 (7.4%).Among them, the gross profit rate of vehicle sales business reached 10.12%, breaking double digits for the first time in history.

In addition to the scale effect brought by the improvement of new car delivery, Xiaopeng's recognition of software business income for the first time is also regarded as another key factor to improve gross profit margin.In the first quarter, Xiaopeng autopilot software recognized a revenue of 80 million yuan.It can be seen from the figure below that the gross profit rate of Xiaopeng's "service and others" business is 32.23%, which is obviously superior to the vehicle sales business (gross profit rate 10.12%).

However, the company's software revenue accounted for only 2.5% in the first quarter, and the contribution of software business to Xiaopeng's gross profit is still relatively limited.In addition, of the 80 million yuan of software revenue recognized in the first quarter, 50 million yuan came from last year's vehicle orders, and only 30 million yuan came from this year's vehicle orders.

However, Xiaopeng Automobile is still optimistic about the follow-up performance of software business.He Xiaopeng said: "In this quarter, our revenue from XPILOT software was recognized for the first time in our vehicle revenue. I believe that we are the only auto enterprise in China that has realized the independent charging of the automated driving assistance software developed by the whole stack." He Xiaopeng also believed that "Q2 software revenue will further increase after the successful expedition of NGP."

However, under the circumstance that Xiaopeng's revenue, vehicle delivery and other data all hit a new record and took the lead in opening the "software charging" mode and other multiple advantages, Xiaopeng's auto share price still fell 4.93% on the day after the quarterly report was released, with the highest drop of more than 50% in the year.

Why is the secondary market not interested in the "good" of Xiaopeng Auto's first quarter report?

Loss should be a major cause.

In the first quarter, affected by the sharp increase in operating expenses, Xiaopeng Auto suffered a net loss of 787 million yuan, which was higher than 650 million yuan in the same period last year.Although the revenue scale has increased by more than 6 times, the loss of Xiaopeng Automobile is still increasing, which also aggravates investors' concern that the company is still unlikely to reach the break even point in the short term.

In order to support vehicle sales, Xiaopeng needs to spend a lot of money on marketing and advertising expenses.Financial report data shows that the sales and management expenses of Xiaopeng Auto in the first quarter reached 721 million yuan, up 124% year on year.

By the end of March, the company had 178 sales outlets and 61 service outlets nationwide, covering 70 cities.In addition, in order to achieve more sales of new cars, Xiaopeng plans to increase the number of sales outlets to about 300 by the end of 2021, covering 110 cities.

R&D investment is another major expense.With the growth of R&D personnel and the increase of P5 new model related development costs, the R&D expenditure of Xiaopeng Automobile in the first quarter reached 535 million yuan, up 72.2% year on year.

Among the "three fools of car building", the operating expenses of Xiaopeng Automobile have always been the highest.In 2020, the operating expense rate of Xiaopeng Auto will reach 79.5%.By contrast, this figure of Weilai is 39.9%, and the ideal figure is only 23.5%.

The difference in operating expense rate comes from the different revenue scale and model planning of the three companies.Relatively speaking, Weilai Auto delivered the largest number of new cars, and its revenue scale dominated;Ideally, it has only one model and relatively low R&D expenditure;In addition to the P5 just launched, Xiaopeng has three models, and the related marketing and promotion costs and new car research and development costs are naturally high.In addition, Xiaopeng has the highest esteem for automatic driving technology, and should also pay a high R&D cost for software.

However, Xiaopeng's R&D investment has not yet been converted into income. The gross profit rate of the company in 2020 is only 4.6%, which is significantly lower than Weilai (11.5%) and Ideal (16.4%).The high operating expenses and low gross profit rate make Xiaopeng one of the new forces with the worst profitability and the highest single car operating loss.

two

Role changes, new forces are challenged

It should be said that from "PPT car building" to "selling one car and losing one car" to the gross profit rate becoming positive, the improvement of the operating performance of the new car building forces is obvious to all.However, with the continuous entry of Baidu, Xiaomi, Huawei and other technology giants, the market is increasingly worried about the intensification of competition in the new energy vehicle track.As a result, the bubble problem of new energy automobile stocks was re examined, which became the deep reason for the continuous decline of the share prices of new forces such as Xiaopeng Automobile.

What is more serious is that when traditional fuel vehicle enterprises turn to ally with the Internet car building corps, new car building forces are facing new challenges from both sides.

In April, when Xiaopeng P5 was promoting the slogan of "the world's first mass production lidar smart car", it was successfully won the limelight by the co branded model "Jihu Alpha S" jointly launched by Huawei and BAIC.From the AI computing power of Huawei HI, the density of millimeter wave imaging radar point cloud, the number of laser lines of laser radar, the detection distance of camera and other indicators, Xiao Peng can not gain any advantage against Huawei in terms of unmanned driving technology.

The original plan of the new force of car building was to use electrification and intelligence to overtake on the curve, but the traditional fuel vehicle enterprises completed the "anti overtaking" with the help of the empowerment and cooperation of technology giants.

The capital market also gave a clear view on this.Since 2021, the continuous rise of BAIC Bluevale and Xiaokang shares has formed a sharp contrast with the continuous decline of New Power shares, which shows that the market is more optimistic about the future development of Huawei's intelligent driving system.BAIC Bluevale and Xiaokang, once not direct competitors, have become the new competitors of Xiaopeng.

The competitive pressure is not only from the Internet car building corps and its allies.The new energy vehicle sales list in April showed that the BMW iX3 ranked 15th with 3552 vehicles, Xiaopeng P7 and Weilai EC6 ranked 16th and 18th with 2995 and 2779 vehicles respectively.

It is quite surprising that BMW has caught up with the flagship EC6 and P7 models of Weilai and Xiaopeng with an immature iX3 before it has officially launched its power. This shows the resilience of traditional automobile giants.In the future, once the Volkswagen ID series is on the right track, the new domestic car making forces will probably face greater impact.

It is worth noting that the sales volume of Xiaopeng cars in April was 5147, with a month on month growth of only 0.9%.Weilai Automobile fell 2.1% year on year.Obviously, with the intensification of competition and the increase of the base, the myth of high growth of new forces has disappeared.

For a long time, Weilai, Ideals, Xiaopeng and other new car building forces have always been the challengers of fuel vehicles, and the market has also given the greatest tolerance to their operating performance losses.In November of last year, the stock price of Xiaopeng Auto rose by more than 200% in a month, and its total market value exceeded 50 billion US dollars, forcing Honda to become the world's tenth largest auto company.

However, the bubble under the sun will eventually burst.

Obviously, compared with the third-party car building corps composed of technology Internet companies, the concept, technology and first mover advantages of new car building forces are no longer obvious.When new forces such as Weilai, Ideals and Xiaopeng have changed from the challenger of traditional fuel vehicles to the challenger in the current pattern of new energy vehicles, the change of roles has also accelerated the collapse of the valuation of new forces.

This also made many investors start to reflect: after continuing to burn money and make huge losses, have Xiaopeng Motors really built a brand image and technical strength that can be called "moat" in the field of new energy vehicles?

(Statement: This article only represents the author's view, not Sina.com's position.)

Lishi Business Review focuses on global business and management, and is committed to becoming a professional and insightful world-class business knowledge media, providing the Chinese business community with the world's best business ideas and management practices.