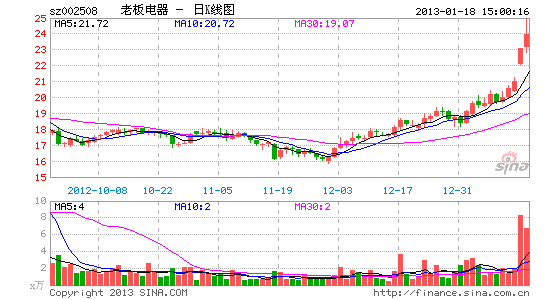

Boss Electric: performance exceeds expectations, and long-term growth continues to be optimistic

Guess you like it

Those who have read this article have also read

-

Ticket grabbing artifact: 12306 ticket booking -

View the world from the perspective of graph: graph bar -

The trend follows: YOHO! E -

Social entertainment alarm: Pepsi Bell -

Rubble Cute Beast: Small fur ball monster -

Justice of Meow Star People: Captain Meow Star -

Play Lonely: Gene Effect -

Funny, humorous and dangerous: come and save me -

Love Dream Travel: Taobao Travel -

Autobots' little secretary: Xiaomi driver -

Good time in the grid: course grid -

Book tickets at any time: Guevara movies -

Funny and unambiguous: Pixel Horror -

Funny: Garfield Escapes -

Fashionable, dynamic and cool: street skateboard -

Simple and durable: Feitian Zhengtai

-

How to Avoid the Tragedy of Left behind Girls -

Difficulties of "Election" Poor Students -

Environmental pollution caused by mineral exploitation -

China will raise the threshold of blue sky -

Resource tax reform should not impact people's livelihood -

Jiyi Ecological Park Tibetan Refinery -

The old town of Beichuan is fully open -

Let the system help the elderly who fall -

Public toilets and private toilets are not allowed -

Urea in 10% swimming pools nationwide exceeds the standard -

Luxury stores suspected of abusing employees -

The rescue of a traveler who falls from a cliff is refused -

Hollow home behind the labor force -

RMB 20000 for 14 years -

Braille Library Waiting for Readers -

2012 Guangzhou Auto Show opened in November

-

Dream Journey to the West, a speed dating red envelope for Spring Festival -

"Sword of Guardianship" Sina Privilege Card -

Devil Kingdom Warm Winter Love Privilege Card -

The Dream of Three Kingdoms exclusive card of Sina -

Journey to the West 3 Sina Privilege Card -

"Ask" Golden Snake Dance Gift Bag -

Valley of Dragons Salon Disaster Gift Bag -

The Demon Subduing Sina Chunlika -

"Zhu Xian 2" Sina Lucky Card -

Painted Skin II Sina Shenlu Card -

"Xuanwu - Blood Drop" exclusive gift package for Sina -

"Condor Heroes" New Year Edition Privilege Card -

Role play novice card -

Shooting game novice card -

Action game novice card -

Strategy game novice card

-

Love transmission, warm leukemia girl @ Lu Ruoqing -

In the microblog era, if you don't play with sharp tools, you will be out -

Friend interaction, file transfer, and quick use of Weibo desktop! -

The list of WeChat Charity Group was announced! -

Registered enterprise Weibo fast channel: three steps to face target users -

Sign in to 2012 Boarding Gathering Point 100 day countdown starts

-

[Finance] Stock market inquiry -

[Finance] Financial calculator -

[Technology] Digital product library -

[Video] The hottest movie -

[Tourism] Inquiry of domestic and foreign scenic spots -

[Child care] Child care utility library -

[Car] Model query -

[Women] cosmetics product library -

[Constellation] Constellation fortune query -

[Entertainment] Video query -

[Entertainment] TV program list -

[Education] University and college inquiry