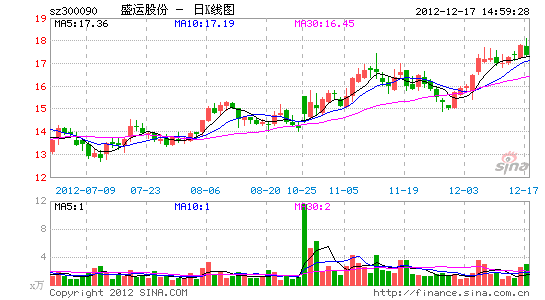

Shengyun Co., Ltd.: strategic focus turns to environmental protection project EPC

Guess you like it

-

Record every bit of life: Sina Weibo -

Voice weather forecast: Weather Pass -

The hottest photo sharing application: pushpin -

Daily focus: Sina in the palm -

Unique parkour: monster mobilization -

Beautiful and gorgeous picture: dark travel -

The game requires fire: the flying king -

Pure cuteness: fantasy aurora -

Exquisite and fashionable: fashionable flashlight -

Let the photo speak: Pappa -

Change makes beauty: beauty -

Mobile beauty artifact: Meitu Xiuxiu -

Extremely challenging: crossing boundaries -

Fighting for Mao: Little Sheep Mobilization -

Super cute cartoon screen: looking for cheese -

Cute and interesting: jelly dream factory

-

How to Avoid the Tragedy of Left behind Girls -

Difficulties of "Election" Poor Students -

Environmental pollution caused by mineral exploitation -

China will raise the threshold of blue sky -

Resource tax reform should not impact people's livelihood -

Jiyi Ecological Park Tibetan Refinery -

The old town of Beichuan is fully open -

Let the system help the elderly who fall -

Public toilets and private toilets are not allowed -

Urea in 10% swimming pools nationwide exceeds the standard -

Luxury stores suspected of abusing employees -

The rescue of a traveler who falls from a cliff is refused -

The hollow home behind the labor force -

RMB 20000 for 14 years -

Braille Library Waiting for Readers -

2012 Guangzhou Auto Show opened in November

-

Oriental Story Sina Privilege Card -

Exclusive gift package of Sina for "Seeking defeat alone" -

Dawn Light Magic Angel Card -

"Nine Yin Scripture" Huashan Sword Argument Card -

Test code of "Huang Yi's Heroes 2" without deleting files -

"Ask" Tianwai Feixian Card -

Valley of Dragons Gift Bag for Good Friends -

Powerful Dance Hall Superstar Gift Bag -

"Sword Laughs" Internal Taiji Card -

Sina Exclusive Gift Bag for "The Legend of the Great Wilderness" -

"Xuanwu - Blood Drop" exclusive gift package for Sina -

Legends of Gods and Ghosts Privilege Treasure Chest of Gods -

Role play novice card -

Shooting game novice card -

Action game novice card -

Strategy game novice card

-

Love transmission, warm leukemia girl @ Lu Ruoqing -

In the microblog era, if you don't play with sharp tools, you will be out -

Friend interaction, file transfer, and quick use of Weibo desktop! -

The list of WeChat Charity Group was announced! -

Registered enterprise Weibo fast channel: three steps to face target users -

Sign in to 2012 Boarding Gathering Point 100 day countdown starts

-

[Finance] Stock market inquiry -

[Finance] Financial calculator -

[Technology] Digital product library -

[Video] The hottest movie -

[Tourism] Inquiry of domestic and foreign scenic spots -

[Child care] Child care utility library -

[Car] Model query -

[Women] cosmetics product library -

[Constellation] Constellation fortune query -

[Entertainment] Video query -

[Entertainment] TV program list -

[Education] University and college inquiry