Exchange Rules for Nickel Futures Trading

1、 Transaction

1. Price limit system

The Exchange implements the price limit system, and formulates the maximum daily price fluctuation range of each listed futures contract, which will be adjusted under specific circumstances according to the rules.

When a futures contract is transacted at the limit price, the principle of closing priority and time priority shall be applied to the transaction matching, but the principle of closing priority shall not be applied to the newly opened positions on the same day.

2. Limited warehouse system

The position limit refers to the maximum number of unilateral positions of a certain contract held by members or clients as specified by the Exchange. The positions of hedging transactions shall be subject to the relevant provisions of the Exchange.

The following basic systems shall be implemented for position limitation: (1) Different amount of position limitation shall be applied to contracts in a certain month at different stages of their trading process, and the amount of position limitation of contracts entering the delivery month shall be strictly controlled. (2) The market risk shall be controlled by limiting the positions of members and customers. Among them, members of futures companies are subject to proportional position limits, and members and customers of non futures companies are subject to quantitative position limits. (3) The hedging transaction position shall be subject to the approval system. The same customer has opened multiple transaction codes at different futures company members, and the total of all positions on each transaction code shall not exceed the position limit of one customer. Before the closing of the last trading day of the month before the delivery month, the speculative positions of each member and each customer in each member's nickel futures contract should be adjusted to an integral multiple of six hands (if the market cannot be adjusted on schedule under special circumstances, it can be postponed for one day); After entering the delivery month, the speculative position of nickel contract should be an integral multiple of six hands, and the newly opened and closed positions should also be an integral multiple of six hands. The limited position proportion and position limit of nickel futures contracts of members of futures companies, non members of futures companies and customers in different periods are specified as follows:

Note: The position of a certain futures contract in the above table is calculated in two directions, and the position limit of members of futures companies, non members of futures companies and customers is calculated in one direction; The position limit of members of futures companies is the base.

3. Compulsory liquidation

Compulsory position closing refers to a compulsory measure taken by the Exchange to close the positions of members and customers when they break the rules.

When a member or client has one of the following circumstances, the Exchange will forcibly close its position: (1) the balance of the member's settlement reserve is less than zero, and it fails to make up within the specified time limit; (2) The position exceeds the position limit; (3) The positions of relevant varieties are not adjusted to corresponding integral multiples within the specified time as required; (4) Being punished by the Exchange for compulsory position closing due to violation of regulations; (5) According to the emergency measures of the Exchange, the position should be closed by force.

2、 Hedging

1. Application for hedging trading position

Nickel hedging trading position is divided into general month (referring to the last trading day of the second month before the contract is listed to the delivery month) hedging trading position (hereinafter referred to as "general month hedging trading position") and the closing delivery month (referring to the first month before the delivery month and the delivery month) Hedging trading position (hereinafter referred to as "hedging trading position in the close delivery month").

Members or clients applying for general monthly hedging trading positions shall fill in the Application (Approval) Form of Shanghai Futures Exchange for General Monthly Hedging Trading Positions, submit the supporting materials required by the Exchange, and submit them before the last trading day of the second month before the contract delivery month involved in the hedging, The overdue exchange will no longer accept the application for hedging trading position in the general month of the contract. Members or clients can apply for general monthly hedging trading positions of multiple contracts at one time.

Members or clients applying for hedging trading positions in the near delivery month shall fill in the Application (Approval) Form for Hedging Trading Positions in the Near Delivery Month of Shanghai Futures Exchange and submit the supporting materials required by the Exchange, It shall be submitted between the first trading day of the third month before the delivery month of the contract involved in the hedging and the last trading day of the first month before the delivery month. The overdue exchange will no longer accept the application for hedging trading positions in the delivery month.

The cumulative hedging trading position of each contract month in the whole year near the delivery month does not exceed its production capacity in the current year, production plan in the current year, or the operating quantity of the commodity in the previous year.

2. Hedging transactions

Members or clients who are allowed to hedge trading positions shall, before the closing of the third trading day before the last trading day of the contract involved in the hedging, build positions according to the approved trading positions and positions. If a position is not established within the specified time limit, it shall be deemed that the hedging trading position is automatically abandoned.

Nickel hedging position shall not be reused since the first trading day of the month of closing.

The adjustment of integral multiples of nickel hedging positions in the near delivery period shall refer to the adjustment method of integral multiples of speculative positions.

After entering the delivery month, the hedging seller can use the standard warehouse receipt as the performance guarantee of the futures positions in the delivery month with the same quantity as indicated by the members or customers who have obtained the hedging trading positions in the delivery month to offset the corresponding trading margin of their positions.

3. Supervision and management

The Exchange shall review the hedging position application within 5 trading days after receiving it.

When members or clients need to adjust hedging trading positions, they shall apply to the Exchange for changes in a timely manner. If the hedging position of a member or client exceeds the approved (or set quota standard) hedging transaction position, it shall be adjusted by itself before the end of the first section of the next trading day; If the adjustment is not made within the time limit or still does not meet the requirements after the adjustment, the Exchange has the right to take compulsory position closing.

In case of market risk, in order to mitigate the market risk, the Exchange shall reduce the position in the order of speculation first and then hedging according to relevant regulations.

3、 Arbitrage transaction

Arbitrage transactions and speculative transactions are consolidated into non hedging transactions. Non hedging trading positions shall be subject to the position limit ratio and position limit of each futures contract in different periods in the Risk Control Management Measures of Shanghai Futures Exchange. Members or clients of non futures companies may expand their non hedging trading positions by applying for arbitrage trading positions.

Nickel arbitrage trading positions are divided into general month (from the contract listing to the last trading day of the second month before the delivery month) arbitrage trading positions and near delivery month (the first month before the delivery month and delivery month) arbitrage trading positions.

1. Application for Arbitrage Trading Positions

Customers who need to apply for arbitrage trading positions shall declare to any member of the futures company whose account is opened, and the member of the futures company shall go through the declaration formalities with the exchange after the examination; Members of non futures companies directly go through the declaration procedures with the Exchange. To apply for general monthly arbitrage trading positions, the Application (Approval) Form of Shanghai Futures Exchange for General Monthly Arbitrage Trading Positions shall be filled in, and materials required by the trading house such as arbitrage trading strategies (including fund source and scale descriptions, intertemporal arbitrage transactions or cross species arbitrage transactions) shall be submitted. The approved general month arbitrage trading position has always been valid for the application variety. To apply for arbitrage trading positions in the near delivery month, the Shanghai Futures Exchange shall fill in the Application (Approval) Form for Arbitrage Trading Positions in the Near Delivery Month, and submit the arbitrage trading strategies (including fund source and scale descriptions, intertemporal arbitrage transactions or cross species arbitrage transactions, position building and reduction arrangements, delivery intentions, etc.) Apply for materials required by the Exchange such as analysis of contract price difference deviation. The application for arbitrage trading position in the near delivery month shall be submitted between the first trading day of the second month before the contract delivery month involved in the arbitrage and the last trading day of the month before the delivery month. The overdue exchange will no longer accept the application for arbitrage trading position in the near delivery month.

2. Arbitrage transaction

The total amount of non hedging positions of the same customer in different futures company members shall not exceed the sum of the position limit ratio of futures contracts in different periods plus the corresponding arbitrage positions in that period or the sum of the position limit provisions plus the corresponding arbitrage positions in that period.

3. Supervision and management

The Exchange shall review the position application of arbitrage trading within 5 trading days after receiving it. When the non hedging position of a member or client of a non futures company exceeds the sum of the position limit ratio of the futures contract in different periods plus the corresponding arbitrage position in that period or the sum of the position limit provisions plus the corresponding arbitrage position in that period, it shall be adjusted by itself before the end of the first section of the next trading day; If the adjustment is not made within the time limit or still does not meet the requirements after the adjustment, the Exchange has the right to forcibly close the position.

4、 Settlement

Settlement refers to the business activities of calculating and allocating the trading deposits, profits and losses, service charges, delivery loans and other relevant funds of members according to the trading results and the relevant provisions of the Exchange. The clearing of the Exchange shall implement the margin system, the day debt free clearing system and the risk reserve system. The Exchange only settles for members, and members of futures companies settle for customers.

1. Daily settlement

The Exchange shall open a special settlement account in each settlement bank for depositing members' deposits and related funds. Members shall open a special capital account in the depository bank for deposit of deposits and related funds. The exchange of funds for futures business between the Exchange and members shall be handled through the special settlement account of the Exchange and the special fund account of members.

The Exchange adopts a margin system. The margin is divided into settlement reserve and transaction margin. The settlement reserve refers to the funds that members have prepared in advance in the special settlement account of the exchange for transaction settlement, and is the margin not occupied by the contract. Trading margin refers to the funds deposited by members in the special settlement account of the Exchange to ensure the performance of the contract, which is the margin occupied by the contract.

The Exchange shall implement a liability free settlement system on the same day. The day to day liability free settlement system (also known as mark to market) refers to that after the end of each day's trading, the Exchange settles all contract profits and losses, trading margins, service fees, taxes and other fees at the settlement price of the day, transfers the net amount of accounts receivable and payable at one time, and increases or decreases the settlement reserves of members accordingly.

2. Key points of margin system

The Exchange implements the trading margin system. The minimum trading margin for nickel futures contracts is 5% of the contract value.

In the trading process of a futures contract, when the following situations occur, the Exchange can adjust the level of its trading margin according to the market risk: (1) when the position reaches a certain level; (2) Near the delivery period; (3) When the cumulative rise and fall of several consecutive trading days reaches a certain level; (4) When there is a continuous up and down limit; (5) In case of national statutory long holidays; (6) When the Exchange believes that the market risk is significantly increased; (7) Other circumstances deemed necessary by the Exchange. The Exchange formulates different standards for the collection of trading margins according to the different stages of the listing operation of a futures contract and the different number of positions.

The collection standard of trading margin when the position of nickel futures changes:

Note: X represents the total bilateral positions of contracts in a certain month, unit: hand.

During the trading process, when the position of a certain futures contract reaches the total position of a certain level, the Exchange will not adjust the margin collection standard of the Exchange temporarily. At the settlement of the day, if the position of a certain futures contract reaches the total position of a certain level, the exchange will charge the trading margin corresponding to the total position of all positions of the contract. If the margin is insufficient, it shall be added in place before the opening of the next trading day.

The Exchange shall adjust the collection standard of trading deposits according to the different stages of the listing operation of futures contracts (near the delivery period).

The standards for collecting trading margins at different stages of the listing and operation of nickel futures contracts are as follows:

The cumulative increase and decrease of nickel futures contracts reached 10% for three consecutive trading days; Or the cumulative increase or decrease for four consecutive trading days reached 12%; Or when the cumulative increase or decrease for five consecutive trading days has reached 14%, the Exchange may, according to the market situation, unilaterally or bilaterally, with the same or different proportion, increase the trading margin of some members or all members, restrict some or all members to make cash payments, suspend some or all members to open new positions, adjust the limit of increase or decrease, and close positions within a time limit, One or more of the measures such as compulsory position closing, but the adjusted range of the limit of rise and fall shall not exceed 20%.

Nickel futures reached the limit of rise and fall in the same direction for three consecutive days and the adjustment method of margin:

Note: X% represents the limit range of nickel varieties at D1

Note: Y% represents the corresponding trading margin level of nickel varieties at D1

5、 Closing

Physical delivery refers to the process that when a futures contract expires, the trading parties settle the outstanding position contract by transferring the ownership of the commodity contained in the futures contract.

After the last trading day of the contract, the holders of all open positions shall perform the contract by physical delivery.

The physical delivery of clients shall be handled by the members, and shall be carried out in the name of the members at the Exchange.

Customers who cannot deliver or receive special VAT invoices are not allowed to deliver.

After the closing of the third trading day before the last trading day of a futures contract, the position of a natural person customer in the futures contract shall be zero. From the second trading day before the last trading day, the positions of natural person customers in the delivery month shall be closed by the Exchange directly. The physical delivery shall be completed within the delivery period specified in the contract. The delivery period refers to five consecutive working days after the last trading day of the contract. These five delivery dates are called the first, second, third, fourth and fifth delivery dates respectively, and the fifth delivery date is the final delivery date.

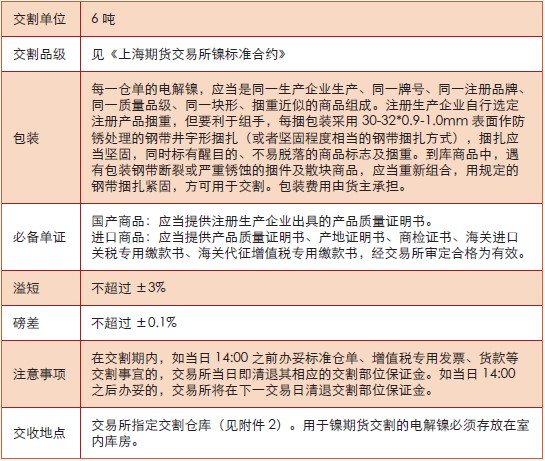

Delivery process:

Nickel delivery: