Domestic ports and large enterprises soybean The inventory is sufficient, and the buyer slows down the pace of purchase Soybean meal Soybean oil stocks climbed, and oil plants generally lacked the incentive to raise prices. However, due to the high import cost of soybeans used by oil plants, the supporting effect of costs will also increase after the crushing profits enter a loss state. As for the soybean meal market, it is currently in an awkward situation of vacillation and difficulty in operation. Participants in the soybean meal futures market can maintain the idea of shock consolidation. The domestic oil market continues to decline, the international crude oil is weak and Malaysia Palm The short pressure in the oil market has not yet been fully released, especially the overall oversupply of domestic oil and grease has long plagued the price rise. Selling short at high times is still a reasonable option for participating in oil futures trading.

1、 External bean market analysis

1. Interpretation of USDA's Monthly Soybean Supply and Demand Report

The US Department of Agriculture released a new monthly supply and demand report on November 8. This report made a major adjustment to some key data of US Bean, and caused wide market shocks. The US Department of Agriculture has reduced the unit yield of American beans from 53.1 bushels/acre last month to 52.1 bushels/acre. This time, the unit yield has been adjusted by a large margin, basically returning to the unit yield level of 2016/17, which shows that the adverse weather during the harvest stage of American beans has caused great damage to the unit yield. Affected by the decrease in unit yield of US soybeans, the total output of US soybeans fell by 2.45 million tons to 125.18 million tons compared with the previous month, still the highest output level in US soybeans history. Affected by the Sino US trade war, US bean exports to China fell sharply to 51.71 million tons compared with the previous month, a drop of 4.35 million tons. As a result, the ending carry forward inventory rose from 24.09 million tons assessed last month to 26 million tons, a year-on-year increase of 118%, the highest level of US bean's historical inventory. In addition, the U.S. Department of Agriculture increased Brazil's soybean exports by 2 million tons to 77 million tons, and reduced Argentina's soybean production by 1.5 million tons to 55.5 million tons. The US Department of Agriculture has also made major adjustments to China's soybean supply and demand data, including an increase of 1 million tons to 16 million tons in output and a decrease of 4 million tons to 90 million tons in import, which is still 6 million tons higher than the latest import data assessed by China's National Grain and Oil Information Center. On the whole, as the market pays more attention to the ending inventory data of US beans, this report has a negative impact on the market. However, whether China US trade tensions can break through next is the key to affect the trend of US beans.

Chart 1: US Department of Agriculture predicts a large increase in US soybean area

Source: USDA, Wanda Information, CIC Futures Research Institute

Chart 2: Domestic soybean imports soared in the first two months

Source: Wande Information, CIC Futures Research Institute

2. China and the United States continue to release trade reconciliation signals

The international financial market generally responded positively to this after last week's China US dollar first call confirmed that the two sides would take measures to improve the current bilateral economic and trade tensions. This week, China and the United States continued to engage in close high-level contacts, including President Xi Jinping's meeting with Kissinger, the second round of the China US Diplomatic Security Dialogue and other activities, which created a good atmosphere for the China US dollar summit at the end of this month and laid the foundation for the two sides to reach a trade agreement. Although there is still great uncertainty about whether the two sides can finally reach a satisfactory agreement to end the trade war, the positive statements of the two sides have made the CBOT soybean market bottoming out and picking up, greatly easing the Chinese market's concern about the supply gap of imported soybeans and soybean meal.

2、 Analysis of Domestic Oil Meal Market

1. The bullish sentiment of soybean meal market has cooled due to the multi pronged regulation measures

Chart 3: Domestic soybean meal inventory climbed

Source: Wande Information, CIC Futures Research Institute

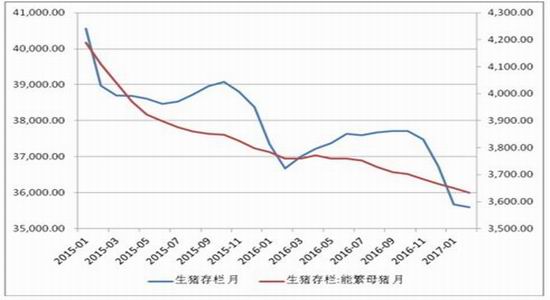

Table 4: Domestic pig stock continues to decline

Source: Wande Information, CIC Futures Research Institute

At the end of last month, the General Administration of Customs issued the Inspection and Quarantine Requirements for Import of Indian Rapeseed Meal, indicating that Indian Rapeseed Meal meeting the requirements would be allowed to be imported. This indicates that the ban on the export of Indian rapeseed meal to China, which has lasted for several years, has been lifted, which is of great significance for increasing domestic rapeseed meal supply. Since then, after the Ministry of Finance announced the cancellation of the soybean meal export tax rebate policy, it has reduced the competitiveness of domestic soybean meal exports, focusing on meeting domestic demand. In addition, the Feed Industry Association also approved a new standard for pig and chicken feed. The standard reduces the protein content of pig feed by 1.5 percentage points and that of chicken feed by 1 percentage point. Although the new standard is not mandatory, it has guiding significance for the industry. It is estimated that 14 million tons of soybean demand can be reduced one year by correcting the protein cost in domestic feed. If the standard is successfully promoted, it will certainly have a long-term and far-reaching impact on the domestic feed industry and the demand for protein meal in the future. In addition, the domestic swine plague in Africa is still spreading, and the outbreak is expanding. Since the beginning of August, more than 50 epidemic cases have been reported accumulatively. The number of farmers selling has increased, and the enthusiasm to supplement has declined, which is not conducive to long-term soybean meal consumption. On the whole, the domestic multi-channel increase of protein meal supply and the active and passive reduction of demand overlap, and all parties' concerns about the insufficient supply of soybean meal market have been significantly alleviated.

2. Soybean imports in October increased significantly year on year, easing the expectation of tight domestic supply

According to the latest data released by the General Administration of Customs, China imported 6.92 million tons of soybeans in October, an increase of 18% year on year. From January to October, China imported 76.93 million tons of soybeans, a decrease of 0.5% year on year in the cumulative quantity, and the decline continues to narrow. The soybean import data in October increased significantly, mainly because the market was worried that the international soybean supply would become more tight after the end of the Brazilian soybean supply season and increased purchases. According to the tracking of the current shipping schedule, it is expected that the arrival of imported soybeans in November will be about 7 million tons, in December it will be about 6.5 million tons, and in January it may drop to 5.4 million tons. At present, the soybean stock in domestic ports is about 7.06 million tons, which is at a normal high level. The soybean supply of large domestic oil plants is sufficient, which can basically meet the demand for soybean meal pressing before January next year. According to the soybean export sales report released by the U.S. Department of Agriculture, as of the week of November 1, China had purchased 977000 tons of American beans (including 407000 tons shipped), compared with 17.1262 million tons in the same period last year. If the trade war between China and the United States can be ended by the end of this month, the US soybean exports to China will surge, significantly improving the domestic supply pressure at the beginning of next year.

3、 Suggestions on operation of oil market

The monthly supply and demand report of the US Department of Agriculture has been finalized, which has limited substantive guidance for US beans. The pattern of bumper harvest of US beans has been set. The blocked export to China has led to high inventory and heavy resistance to price rise. The key to solving the "difficulty in selling beans" of American soybean farmers lies in the improvement of Sino US trade relations. In the near future, CBOT beans will continue to be affected by Sino US trade negotiations.

The Sino US trade issue is also a key factor affecting the trend of the domestic bean market. Before the Sino US dollar summit at the end of this month, the bullish sentiment of the domestic bean market will continue to be suppressed due to the negotiation between the Sino US trade team. Domestic ports and large enterprises have sufficient soybean stocks, and the demand side slows down the pace of procurement, leading to a rise in soybean meal and soybean oil stocks. Oil plants generally lack the incentive to raise prices. However, due to the high import cost of soybeans used by oil plants, the supporting effect of costs will also increase after the crushing profits enter a loss state. For the soybean meal market, it is currently in an awkward situation of swing, and the operation is difficult. It is suggested that feed enterprises and traders can appropriately reduce the procurement cycle, and try to purchase as soon as possible. Participants in the soybean meal futures market can maintain the idea of shock consolidation. In case of a sharp drop in 1901 soybean meal futures, they can buy a moderate amount of it, otherwise they should try to look more at it than move it. The domestic oil and fat market continues to decline. The weakness of international crude oil and the short pressure of Malaysian palm oil market have not been fully released, especially the overall oversupply of domestic oil and fat has long plagued the price rise. Selling short when the trend is high is still a reasonable option to participate in oil and fat futures trading. The demand side of the domestic soybean market is unable to boost the price, including the news that a large number of targeted sales may occur at the beginning of next year, which is still not conducive to the soybean price going out of the weak position. It is not recommended to buy at the bottom too early, but can continue to wait and see.

Risk point: uncertainty in Sino US trade negotiations.

CIC Futures Team 1

Sina statement: The purpose of posting this article on Sina.com is to convey more information, which does not mean to agree with its views or confirm its description. The content of this article is for reference only and does not constitute investment advice. Investors operate accordingly at their own risk.

Editor in charge: Song Peng