Transaction logic:

Macro: The Sino US trade dispute has taken a turn for the better, Corn The import volume of sorghum and barley, as well as its substitutes, is expected to rise, while the RMB will appreciate significantly to reduce the import cost of agricultural products.

Supply: 1. New season corn is listed in a centralized way nationwide, increasing supply pressure; 2. Corn stocks at ports in the north and south reached a five-year high.

Demand: 1. Corn deep processing enterprises have significantly replenished their stocks after the 11th Five Year Plan, and the current purchase volume has declined; 2. The spread of African swine fever caused panic, and feed demand may be affected.

Core view: corn in the new season will be listed in a centralized way, and the enthusiasm of swine fever to attack and supplement the stock market will further affect the demand for feed. The Sino US trade war will ease, the RMB exchange rate will appreciate, and sorghum will, soybean Barley and DDGS imports are expected to recover, thus squeezing the share of corn demand. Corn is facing downside risk in November December. We try to short C1901 and fall to 1800.

Trading strategy:

Transaction risk:

China US trade war negotiations failed.

Festivals demand leads to centralized replenishment in the downstream.

1、 The Sino US trade war is turning around

On November 1, Trump tweeted that the Sino US trade war was expected to ease, Soybean meal Rapeseed meal fell by the corresponding limit, and corn also opened lower after the opening of daily trading. If tariffs are cancelled, the volume of sorghum, soybeans and DDGS imported from the United States will recover, and then occupy the domestic corn market share. The real negotiations will wait until the G20 Summit in December. At present, there is more negative sentiment on domestic agricultural products.

From the perspective of historical laws, DCE corn and CBOT corn prices are positively correlated. However, this year, affected by the Sino US trade war, the trend deviates from that after April. If the Sino US trade war eases, the price difference between the two will narrow, that is, DCE corn will fall and CBOT corn will rise.

Figure 1 Trends of China US corn futures

Data source: Wind, Industrial Futures Research and Consulting Department

2、 New and used grains come into the market to increase supply pressure

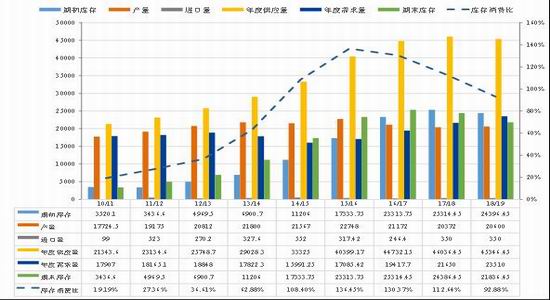

In November, new corn was harvested and listed from south to north in succession. Due to frequent disasters in Northeast China this year, the per unit yield of corn declined, maturity and harvest were delayed, and the market's available supply of goods was relatively small. In coordination with farmers' hoarding of grain, grain was stored at a high price in rotation. After the National Day, the price of corn rose steadily, and the purchase price of some enterprises in Shandong broke the 1 yuan mark. However, according to the supply-demand balance table revised in October, this year's corn production is still 2.3 million tons higher than that of last year. At the same time, at the end of the year, growers are still under pressure. Grain will be stockpiled in October or sold off in November. At that time, the supply pressure of new season corn will be highlighted.

Figure 2 China's corn supply and demand balance table (October)

Data source: National Grain and Oil Center, Industrial Futures Research and Consulting Department

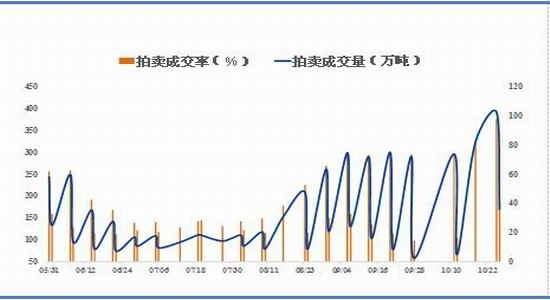

The temporary storage of corn in 2018 was officially closed on October 26. Since April, 28 rounds of auctions have been held, with 219.6 million tons put in and 100.13 million tons sold. According to the two month delivery date, there are still about 20-30 million tons of auctioned grain that have been sold yet to be delivered. It is highly likely that the old grain will be delivered in November.

Figure 3 Increase in auction volume of temporarily stored corn

Data source: Wind, Industrial Futures Research and Consulting Department

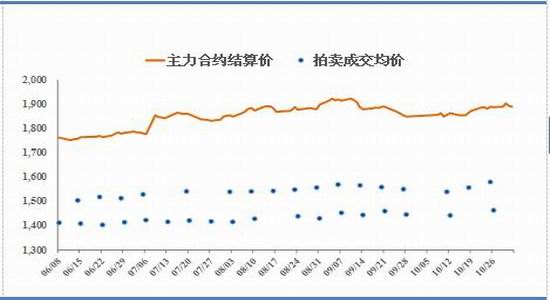

Figure 4 The average price of temporary corn reserve auction rose significantly

Data source: Wind, Industrial Futures Research and Consulting Department

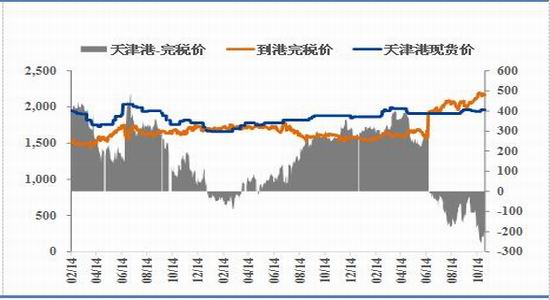

As of October 26, the total inventory of northern ports was 3.173 million tons, an increase of 72000 tons over the previous week and a decrease of 86000 tons over the same period last year. The inventory of Guangdong domestic trade ports was 745000 tons, a decrease of 50000 tons over the previous week and an increase of 412000 tons over the same period last year. The port inventory is at the highest point in nearly five years, and according to the trend over the years, the listing of corn in the new season has led to the continuous accumulation of inventory and unprecedented supply pressure.

Figure 5 Trend of corn inventory in northern ports

Data source: Tianxia Granary, Industrial Futures Research and Consulting Department

Figure 6 Trends of Domestic Trade Corn Stocks in Guangdong Ports

Data source: Tianxia Granary, Industrial Futures Research and Consulting Department

By September, the import of corn had dropped to 40000 tons. Affected by the Sino US trade war, the import volume has continued to decline in recent months. However, the cumulative import of corn this year was 2.917 million tons, still higher than last year's 641000 tons. On November 1, the Sino US trade war showed signs of easing, and the import volume will rise in the future, but the actual increase will not be realized until next year, which is more favorable at present.

Figure 7 Reduction of import volume of main grains (10000 tons)

Data source: Tianxia Granary, Industrial Futures Research and Consulting Department

Figure 8 Increased loss of corn import

Data source: Tianxia Granary, Industrial Futures Research and Consulting Department

3、 Increased demand for corn

Corn deep processing:

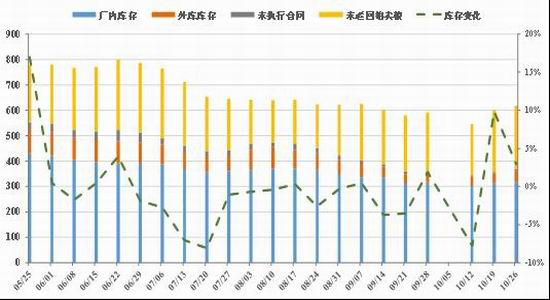

As of October 26, according to the statistics of Tianxia Granary, 114 sample corn deep-processing enterprises had 6.1729 million tons of corn stocks, an increase of 2.95% month on month, with 76 enterprises starch The corn inventory of enterprises is 315.78 million tons (+5.99%), that of 23 alcohol enterprises is 227.6 million tons (- 0.44%), and that of 15 additive enterprises is 73.91 million tons (+1.18%). Inventories have risen rapidly since the National Day, and began to fall last week. With the centralized listing of new grain, the enthusiasm of enterprises for purchasing will fall.

As of October 26, according to the statistics of Tianxia Granary, 115 sample corn deep processing enterprises had purchased 867600 (- 83500) tons of corn, and the purchase volume of enterprises fell this week after the centralized replenishment during the 11th National Day. In terms of operating rate, the alcohol industry was 62.52% (+8.86%), and the starch industry was 77.32% (+6.19%), both at a high level in recent five years.

Due to the delayed listing of new grains and tight spot supply, the purchase volume of corn deep-processing enterprises increased significantly after the National Day holiday, the inventory rose (on the high side), and the operating rate rose (at a high level in recent five years). The demand for corn deep-processing was stable.

Figure 9 Inventory of 114 corn deep processing enterprises (10000 tons)

Data source: Tianxia Granary, Industrial Futures Research and Consulting Department

Figure 10 Purchase volume of corn deep processing sample enterprises (10000 tons)

Data source: Tianxia Granary, Industrial Futures Research and Consulting Department

Figure 11 The operating rate of corn alcohol industry dropped slightly

Data source: Tianxia Granary, Industrial Futures Research and Consulting Department

Figure 12 Five year high operating rate of corn starch industry

Data source: Tianxia Granary, Industrial Futures Research and Consulting Department

Feed:

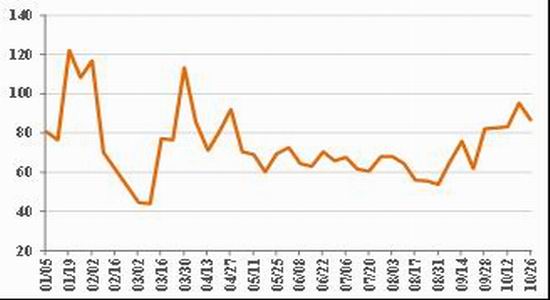

The feed industry has significant seasonality, and the annual peak of price and output often occurs from September to November. However, this year, the feed industry suffered from environmental protection and macro negative effects, resulting in a sharp decline in output.

Figure 13 The price of formula feed has risen steadily

Data source: Tianxia Granary, Industrial Futures Research and Consulting Department

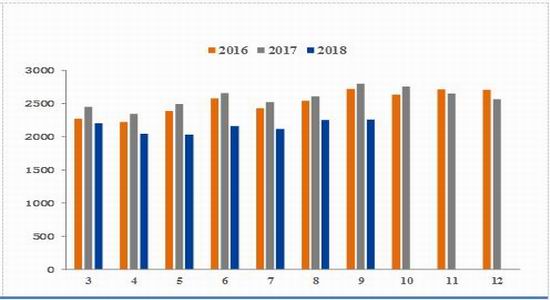

Figure 14 Feed output (10000 tons)

Data source: Tianxia Granary, Industrial Futures Research and Consulting Department

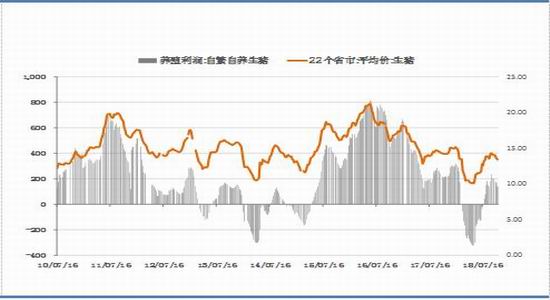

According to the statistics of the Ministry of Agriculture, in September, the number of live pigs on hand increased by 0.8% month on month, with a year-on-year decrease of 1.8%. The number of fertile sows decreased by 0.3% month on month, with a year-on-year decrease of 4.8%. With the continuous improvement of pig breeding profits, the number of live pigs on hand stopped falling and recovered. However, African swine fever is still spreading. As of November 2, there were 54 cases of epidemic throughout the country and 200000 pigs had been culled. At present, 24 provinces and 4 municipalities directly under the Central Government have stopped trans provincial transfer of pigs. Farmers are generally pessimistic, and their enthusiasm for making up for slaughter is poor, or it may affect feed demand.

Figure 15 Growth rate of pig price leads the growth rate of pig stock

Data source: Tianxia Granary, Industrial Futures Research and Consulting Department

Figure 16 Pig breeding profit decline

Data source: Tianxia Granary, Industrial Futures Research and Consulting Department

4、 Summary

Based on the above analysis, corn in the new season is concentrated on the market, and the enthusiasm of classical swine fever to attack and supplement stocks has further affected the feed demand. The Sino US trade war has eased, and the imports of sorghum and DDGS are expected to recover, thus squeezing the share of corn demand. In November and December, corn is facing the risk of decline. We try to short C1901 and see it fall to 1800 points.

Industrial Futures Team 2

Sina statement: The purpose of posting this article on Sina.com is to convey more information, which does not mean to agree with its views or confirm its description. The content of this article is for reference only and does not constitute investment advice. Investors operate accordingly at their own risk.

Editor in charge: Song Peng