Fundamental analysis

1、 Macro and meso view/supply and demand

And other value-added tax and import tariff policies (the market rumor is that the value-added tax is reduced from 10% to 8%).

And other new guidelines for G20 China US relations. On the afternoon of November 8, a "misinterpretation" message from Reuters was traded in domestic double meal, which fell rapidly. The market is indeed very chaotic, and the mood has been amplified. Ordinary investors should avoid it.

In terms of domestic subsidies, continue to guide farmers to expand their planting soybean 。 Heilongjiang Province 2018 Corn And the grant of subsidies to soybean producers. In order to effectively guarantee the reasonable income of corn and soybean producers, with the consent of the provincial government, in 2018, the subsidy standard for corn producers in Heilongjiang Province is 25 yuan/mu of legal planting area, and the subsidy standard for soybean producers is 320 yuan/mu of legal planting area.

The price of domestic soybeans is firm, and soybeans with poor quality can be shipped.

Figure 5: Trend chart of US dollar against Argentine peso

Data source: Galaxy Futures

Figure 6: Trend of USD against Brazilian real

Data source: Galaxy Futures

Figure 7: Trend chart of USD against RMB

Data source: Galaxy Futures

Figure 8: VIX Panic Index

Data source: Galaxy Futures

The November supply and demand report of USDA of the United States Department of Agriculture shows that the soybean yield is basically qualitative, maintaining a volatile situation. From the perspective of the adjustment of US soybean yield per unit area, the supply and demand report in November was beneficial to the market, but it was not the focus of market transactions. In particular, the decrease in exports and the increase in carry over inventory broke this expectation. In addition, USDA did not take into account the expectation of the upcoming peace talks. This report sharply reduced the export volume of US soybeans by 160 million bushels to 1900 million bushels. The last such large reduction occurred in the report in July, when the reduction was 250 million bushels, which was the stage of deterioration of Sino US relations. The final inventory of US Bean this year was raised by 70 million bushels to a record high of 955 million bushels. USDA also further reduced China's soybean imports from 94 million tons to 90 million tons in 2018/19. And the global corn inventory has increased significantly, which of course can not be separated from the help of the China National Bureau of Statistics. On the night of the report, CBOT Meidou also had an unreasonable decline, indicating that the market did not have many topics worth trading.

Key points of the report: 88.3 million acres of American beans were harvested (8830 last month, 8950 last year), the unit yield was 52.1 bushels (53 expected, 53.1 last month, 49.3 last year), the output was 4.6 billion bushels (46.76 expected, 46.90 last month, 44.11 last year), the export was 1.9 billion bushels (20.60 last month, 21.29 last year), and the crushing was 20.80 (20.70 last month, 20.55 last year), 955 million Pu at the end of the period (expected 8.98, 8.85 last month, 4.38 last year). Although the US bean production estimate was lowered and lower than the previous market expectation, the export decline was too large, resulting in a rapid rise in the closing carry over inventory.

On Thursday, the US Department of Agriculture issued a supply and demand report, which also significantly lowered the forecast value of China's soybean imports. The US Department of Agriculture recently predicted that China will import 90 million tons of soybeans in the year from October 2018 to September 2019, lower than the 94 million tons predicted in October and 94.13 million tons predicted in 2017/18. This month, the USDA also raised the forecast value of China's soybean production in 2018/19 by 1 million tons, from 15 million tons predicted last month to 16 million tons. In addition, the initial soybean inventory was also raised to 23.54 million tons, higher than the 22.46 million tons predicted in October. The predicted value of China's soybean crushing in 2018/19 was reduced by 1 million tons, from 93.5 million tons predicted last month to 92.5 million tons, but still higher than the 90 million tons predicted last year.

2、 Weather

To put it simply, the current weather in North and South America is not the focus of market transactions. USDA's reduction in soybean yield is also due to the impact of early precipitation. However, we can see that in the report, the per unit area yield of Minnesota was flat month on month, while the per unit area yield of corn in this state was reduced by 7 bushels/acre. The direction of the adjustment of the unit yield estimate in the supply and demand report in January is uncertain compared with that in the report in November, but it has basically been determined. Considering the situation of the above corn, the unit yield of soybean may be slightly reduced in January.

As for South America, the weather is good on the whole. The author tends to think that the weather in South America and early maturing soybeans have not been fully digested on the plate.

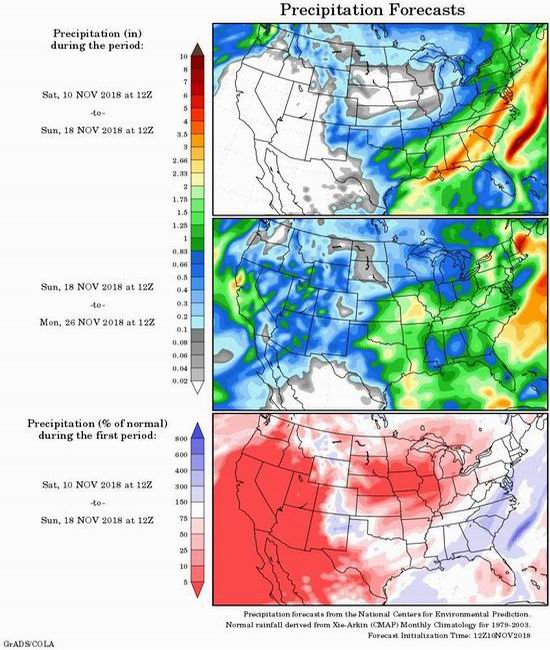

Figure 9: US Temperature Forecast

Data source: Galaxy Futures, NOAA, GrADS/COLA

Figure 10: Precipitation forecast in the United States

Data source: Galaxy Futures, NOAA, GrADS/COLA

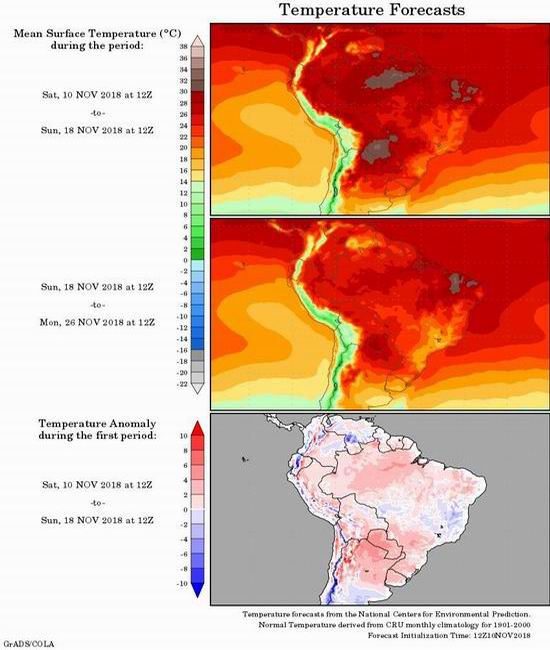

Figure 11: South American Temperature Forecast

Data source: Galaxy Futures, NOAA, GrADS/COLA

Figure 12: Precipitation Forecast in South America

Data source: Galaxy Futures, NOAA, GrADS/COLA

3、 Foreign/discount market

The discount in Brazil is still declining, and there were 290 discount deals in recent months at the beginning of this week. Even so, there is still no hedging profit on the far month shipping date. This is also the reason why many funds have tried M59 in the near future. In the return of trading profits, even considering the uncertainties of Sino US relations, the panel profit may reach about $30 before oil companies are attracted to buy.

The decline of discount in Brazil, which the author has mentioned many times, cannot be understood as the accumulation of old Brazilian works for sale. The main reason is that China and the United States are slow to buy. In addition, export traders are anxious when China's procurement slows down due to their large amount of early hoarding.

4、 Logistics and shipping schedule

General Administration of Customs: The import of soybeans in October was 6.92 million tons, down 13.6% from 8.01 million tons in September. The total import of soybeans from January to October was 76.93 million tons. The import volume of vegetable oil in October was 471000 tons, 18.8% lower than the previous month.

Judging from the current situation of soybean purchase and arrival at the port and soybean crushing, the trend of destocking in the fourth quarter and the first quarter of next year is basically determined. Few ships have been bought since January. From this point of view, it still supports the M59 positive set.

The feed group has purchased a lot of sunflower seed meal, rapeseed granule meal and peas. The benefits of "gap" are also being dispersed and digested by a small part. In the fourth quarter, the import volume of sunflower meal has purchased more than 500000 tons. However, the total amount is relatively limited, at the level of 1 million tons. The supply of peas in the fourth quarter is also expected to be more than 500000 tons (including 22% protein and 46% starch , which has the value of both protein and energy). Feed mills in East China and North China are also actively deploying procurement channels such as cotton meal. But in Soybean meal After the sharp drop in price, the value of many miscellaneous meals also fell simultaneously.

There were also new deals of Indian vegetable meal this week. According to the shipping schedule from December to January, it is an old one, but the import related procedures and documents are still in progress.

5、 Domestic press

Because of the Shanghai International Expo, the environmental protection inspection team moved to Jiangsu, and the operating rate of some large oil plants in Jiangsu declined significantly, which helped to reduce the soybean meal inventory. Nantong Cargill: started up, but not fully opened, with a production reduction of 25%, and 5000 tons of soybean processed daily. It is expected to resume full opening on November 10. Taizhou Zhenhua: double line shutdown on November 6, and it is expected to start up on November 10-11. Nanjing Bangji: It was started, but it was not fully opened. The output was reduced by 30%. The daily soybean processing capacity was 2000 tons. It is expected to be fully opened on November 10-11. Taizhou Huifu: It was shut down on the evening of November 6, and is expected to resume full operation on November 10-11. Later, it will be shut down again on November 15 for two months. Hai'an Jiahui: It was shut down on November 5 and is expected to resume on November 12. Yangzhong Zhonghai: shut down on October 30 and is expected to start on November 6. Shanghai Dongchen: Since the Expo was shut down on October 22, it is expected to start in the middle of November.

The operating rate of oil plants in East China has declined significantly, and some oil plants are short of beans or in need of maintenance. As of the week of November 9, the total crushing capacity of oil plants across the country was 1697400 tons. In the middle of the year, it is expected that the oil plant will resume production, and the squeezing volume in the next two weeks will be 180.185 million tons.

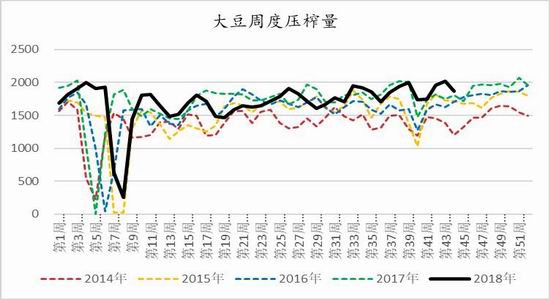

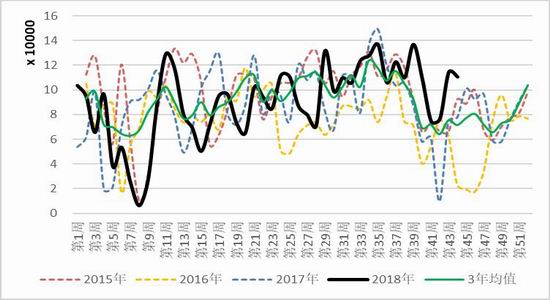

Figure 13: Weekly crushing amount of soybean

Data source: Galaxy Futures, Tianxia Granary

Figure 14: Rapeseed Perimeter Press

Data source: Galaxy Futures, Tianxia Granary

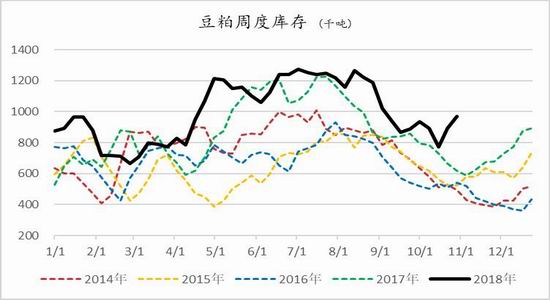

Figure 15: Weekly stock of soybean meal

Data source: Galaxy Futures, Tianxia Granary

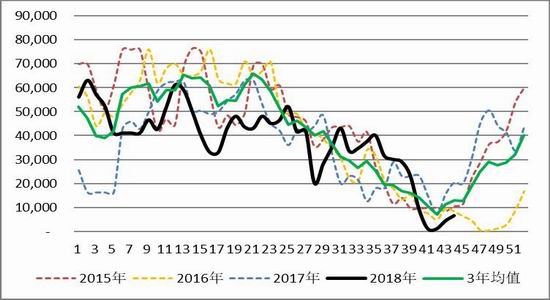

Figure 16: Weekly inventory of rapeseed meal

Data source: Galaxy Futures, Tianxia Granary

6、 Feed breeding demand

To sum up, CSF will continue to ferment, and the demand in the first quarter of next year will become more and more pessimistic, and there is basically no price in the dish. The reason is that the region will issue red headed documents restricting the supplement and breeding, which will shorten the pig cycle. Without this document, it can be predicted that there will be a big turning point in the second quarter of next year. If this phenomenon increases, it is likely that the price of pigs will take off in the next 2-3 months. In some areas, the phenomenon of delaying pregnancy of sows and slaughtering/selling piglets at a low price has also occurred. Combined with the continuous brewing of classical swine fever and the fermentation of medium and large scale (companies+farmers) epidemic, the feed demand after January 2019 is not good.

On the poultry feed side, the current growth of chicken demand in the terminal market is limited, and the willingness to receive products from gaojia is weak. Slaughterhouses, driven by costs, have a strong willingness to support prices. The demand for chicken seedlings is good, the supply has not recovered, and the quotation has fluctuated at a high level, continuing to hit a new high since 2011. It is expected that the price of feather chicken will continue to fluctuate at a high level in the next few weeks.

7、 Capital

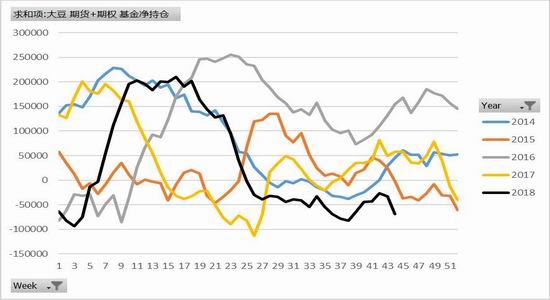

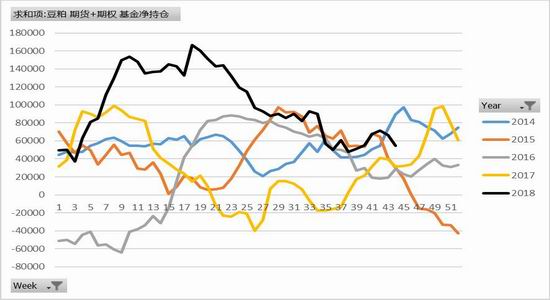

Figure 17: CFTC's net position of American soybean futures+options

Data source: Galaxy Futures, CFTC

Figure 18: Net position of CFTC US soybean meal futures+option fund

Data source: Galaxy Futures, CFTC

On the night of the USDA's November supply and demand report, CBOT Meidou also had an unreasonable decline, indicating that the market did not have many topics worth trading. The yield of soybeans is basically qualitative, and the situation is volatile. From the perspective of the adjustment of US soybean yield per unit area, the supply and demand report in November was beneficial to the market, but it was not the focus of market transactions. In particular, the decrease in exports and the increase in carry over inventory broke this expectation. In addition, USDA did not consider the expectation of the upcoming peace talks.

In terms of domestic capital sentiment, it is disorderly fluctuations, waiting for policy guidance. Considering that the bulls are on the verge of being scared, the positions have not been given confidence for a long time, and the market's news about the expected increase in the peace talks+the reduction of VAT has not landed, it is difficult for prices to rise in the short term.

According to the weekly position report, Yong'an increased the number of orders, increased the price difference between beans and vegetables to expand, and M59 was set. More seats in Morgan and other industries will move from empty positions in January to empty positions in May. There is no special sign. On Friday, November 9, except that COFCO moved some empty orders of protein from January to May, the rest seemed more quiet.

Key data

Figure 19: Price difference of soybean meal 01

Data source: Galaxy Futures, Wind

Figure 20: Price difference of soybean meal 05

Data source: Galaxy Futures, Wind

Figure 21: Price difference of soybean meal 1-5

Data source: Galaxy Futures, Wind

Figure 22: Price difference of rapeseed meal 1-5

Data source: Galaxy Futures, Wind

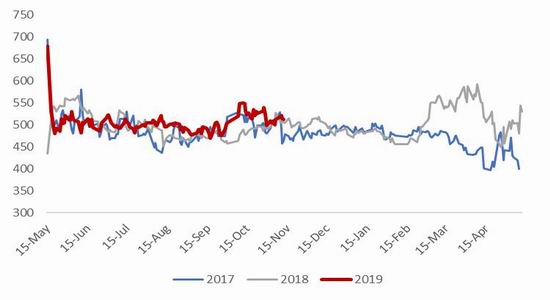

Figure 23: Soybean meal basis

Data source: Galaxy Futures, Wind

Figure 24: Rapeseed meal basis

Data source: Galaxy Futures, Wind

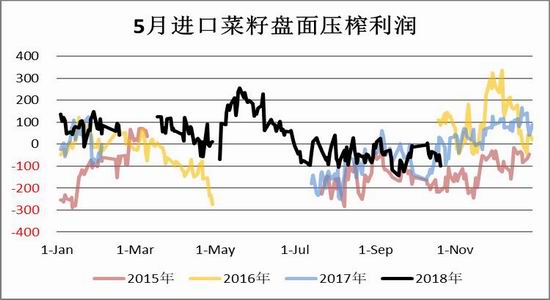

Figure 25: Soybean plate pressing profit

Data source: Galaxy Futures, Wind

Figure 26: Rapeseed plate pressing profit

Data source: Galaxy Futures, Wind

logic analysis

In the short term, the futures prices at home and abroad are fluctuating in disorder, and the fundamentals are lacking. We have to wait for the guidance of Sino US relations.

Abroad - On the night of the November supply and demand report of USDA of the U.S. Department of Agriculture, CBOT Meidou also had an unreasonable decline, which showed that the market did not have many topics worth trading. The yield of soybeans is basically qualitative, and the situation is volatile. From the perspective of the adjustment of US soybean yield per unit area, the supply and demand report in November was beneficial to the market, but it was not the focus of market transactions. In particular, the decrease in exports and the increase in carry over inventory broke this expectation. In addition, USDA did not consider the expectation of the upcoming peace talks.

Domestic - In terms of fund sentiment, it is disorderly fluctuation, waiting for policy guidance. Considering that the bulls are on the verge of being scared, the positions have not been given confidence for a long time, and the market's news about the expected increase in the peace talks+the reduction of VAT has not landed, it is difficult for prices to rise in the short term. Most of the seats in the organization are also conservative operations such as moving positions.

It is worth mentioning that Yong'an and the industry have respectively made some unilateral multiple orders of protein, expanded the price difference between beans and vegetables, and M59 positive and M59 negative. Yong'an's position has a large part of the pre judgment component of policy interpretation, among which the expansion of the price difference between beans and vegetables also has the consideration of greater pressure on Indian rapeseed meal to trade miscellaneous meal.

The focus is mainly on the interpretation of the meal type far month cross month arbitrage contract, which is a relatively safe position keeping a certain distance from the topic of Sino US trade war. For example, the biggest driver of M59 Zhengtao comes from the fact that the profit is still negative when the discount in South America continues to decline. After January, China's purchase of soybeans sharply reduced, so the profit needs to be repaired, and even in the case of sudden changes in Sino US relations, additional risk premium should be given. What the author considers is that the topic of South American soybeans that has not yet been digested and the demand for the first quarter of next year that there are basically no too many transactions on the market. If you open the position at the current price, the downward space is small, and the macro variables are also large. Therefore, the final suggestion is to wait for the contract in May to rise, and then try to reverse arbitrage. For the aggressive type, try to take advantage of the M59 position, and then take 20-30 profits.

Since November, the performance of the spot market has been very weak (the basis of East China soybean meal has dropped below 100, and South China 130 has not been visited), which has also put pressure on the weak market. The market transaction is extremely light and pessimistic. Many traders have turned from bulls to bears (especially from February to April). They are not optimistic about the second half of the month, December and January. The reasons why they are not optimistic are as follows: first, the demand is not good, and the stock of broilers and pigs has declined; second, too many miscellaneous meals have arrived in Hong Kong, affecting the demand for soybean meal.

However, according to the recent market understanding, the recent weak demand/delivery is more due to the feed price rise in October, overdraft, demand in November, and the decline of raw material prices, driving the downstream inventory reduction. The reason is that the overall inventory status has not changed except for the early listing of pigs in some areas. The weak sales of poultry materials in the first ten days of November also confirmed that the demand for overdraft of stock in the early stage had a greater impact. Therefore, it is reasonable that the demand was poor in the first ten days of November, but at this time point, traders and oil plants no longer pay high prices.

We pay attention to the potential large-scale early listing probability in December. Just based on the current situation, the market is pessimistic about the demand in the fourth quarter.

Trading strategy

Transaction plan

Operation contract: M1901 soybean meal

Direction: short

Entrance interval: 3000-3100

Stop loss range: 3150

Stop interference target: 2900

Number of operators: 350 (20% capital)

Galaxy Futures Team 2

Sina statement: The purpose of posting this article on Sina.com is to convey more information, which does not mean to agree with its views or confirm its description. The content of this article is for reference only and does not constitute investment advice. Investors operate accordingly at their own risk.

Editor in charge: Song Peng