Summary: From upstream cost side Corn From the perspective of supply and demand, the inventory consumption ratio has further declined, the supply of corn market is expected to tighten significantly, and there is a basis for a trend increase in prices. from starch From the perspective of the spot market, it has always maintained a tense state. First, the actual effective capacity is smaller than the industry statistics, and the effective supply has always been insufficient; Second, demand should be in effective growth and exceed industry expectations. In addition, due to the increase in tax rebates, the strong trend of export will continue and is expected to reach a new high. Therefore, in the case of tight supply and demand and a sharp increase in exports, it is expected that the future price of corn starch will continue to strengthen.

1、 From the perspective of cost, raw corn is strongly supported

Corn is the upstream variety of corn starch, and the price correlation between the two is high. From the perspective of corn supply and demand, all agencies have the same expectation of supply contraction. The domestic corn balance sheet issued by various institutions in the industry is complicated, but the supply and demand trends are basically the same. According to the agency, China's corn production has been decreasing since 2016/2017, while the demand has been increasing since 2015/2016. The gap between production and demand is a scissors gap. In 2017/2018, there is a gap in supply, and the huge national reserve inventory accumulated before has been consumed. From April 2018, 2017/2018 corn dumping and storage has been completed. Up to now, 95.3 million tons of corn has been sold. According to the 70% delivery rate, the actual increase in dumping and storage is 70 million tons. At the same time, the channel inventory is expected to increase by 5 million tons to 28 million tons; The port inventory is expected to increase by 1 million tons to 5 million tons, with an actual gap of 61 million tons. This is basically consistent with the actual production and demand data. In 2017/2018, the domestic corn output is expected to decline by 15 million tons, while the demand is expected to increase by 20 million tons. Among them, the increment of feed demand is 12.5 million tons, 7.5 million tons is the substitution regression of wheat, 5 million tons is the normal increment of feed, and 7.5 million tons is the increment of deep processing (2 million tons of alcohol, 5 million tons of starch). It can be seen that the supply gap in 2017/2018 is 35 million tons larger than that in 2016/2017, reaching 59 million tons, which is also basically in line with the gap measured by dumping and storage. The national reserve stock continues to digest. By the end of 2017/2018, the remaining amount of the national reserve stock is expected to be 83.33 million tons. Add 25 million tons of channel inventory and 5 million tons of port inventory. At the end of 2017/2018, the ending inventory totaled 113 million tons, and the inventory consumption ratio dropped to 47%. In 2018/2019, the domestic corn output is expected to increase slightly, ranging from 225 million to 230 million tons, the demand is expected to be 250 million to 255 million tons, and the supply gap is expected to be 25 million tons. At the end of the year, based on the consumption of the national reserve inventory to 58.33 million tons, the channel inventory to 25 million tons, and the port inventory to maintain 5 million tons, the ending inventory was 88.33 million tons, and the inventory consumption ratio decreased to 35%. The supply of corn market is expected to tighten significantly, and there is a basis for the price to rise trend.

On the other hand, the supply side reform of the corn market is a national strategy, which aims to remove huge stocks. At present, the stagnation of maize planting area means that the output will not increase significantly, but the demand is increasing year by year. The trading volume of temporary storage in the northeast production area has reached 64 million tons. Under the expectation of high growth of corn in the new season, some processing enterprises continue to participate in the auction of temporary storage to supplement corn stocks. However, affected by the typhoon transit and continuous rainfall weather in the Huang Huai production area in North China, the arrival of processing enterprises is not high. Enterprises continue to consume inventory, and the existing inventory remains small. Some large-scale deep processing enterprises maintain inventory for 15 days. However, the start-up rate of deep processing enterprises rebounds, the purchase willingness of feed enterprises increases, the market demand increases, and the purchase price fluctuates. Stimulated by the price rise, most enterprises have no inventory and sales pressure, and follow the sales. Recently, the social inventory in North China has continued to decline, only 103000 tons so far, supporting the price rise.

2、 The supply and demand pattern of the spot market has always remained tense

Corn starch is the basis of corn deep processing, and also an important link in the downstream demand of corn. In the production process of corn starch, protein powder, fiber, embryo and other by-products can be obtained. One share of corn production can obtain 0.7 shares of corn starch, 0.05 shares of protein powder, 0.14 shares of fiber, 0.08 shares of embryo. Due to different processes and equipment, the corn starch processing fees of production enterprises in different parts of China are different, about 500 yuan/ton in Northeast China and about 400 yuan/ton in North China. Since the second half of 2015, the price of corn has dropped significantly. Compared with other alternatives, corn starch has obvious price advantages. Downstream consumption has been increasing, and the overall capacity has also been expanding. Especially since 2017/18, the domestic starch output has increased by nearly 20%, and the downstream consumption is also growing at the same time. The annual consumption of corn starch is about 26 million tons, which translates into more than 37 million tons of corn. The downstream consumption of corn starch is more complex, covering food, beverage, medical treatment, chemical industry and other fields, which is similar to the living standard of residents. We believe that the growth rate of starch demand should be equal to the growth rate of GDP. From 2012 to 2017, China's GDP increased from 48.8 trillion to 78.6 trillion, an increase of about 61.1%, while the consumption of corn starch in the same period only increased by about 37.0%, significantly less than the growth rate of GDP. The main reason is that the price of corn was too high from 2011 to 2015, which inhibited the downstream demand for starch. Since 2016, the output and consumption of starch have increased significantly. In order to catch up with the growth rate of GDP, we expect that the starch production capacity will continue to expand in the next two to three years.

Since the National Day this year, the price of starch has been rising. The price of starch has risen from 2350 yuan/ton to 2450 yuan/ton in Jilin, and even more in Shandong, from 2500 yuan/ton to 2680 yuan/ton. Recently, the price of starch in Shandong was too high, which led to the obvious restriction of sales and order signing, and the actual transaction price in the market was also slightly loose, and some high price starch may be corrected in the short term. However, the early price increase in Jilin is relatively small, and it is estimated that the possibility of price reduction is small. In the future, if futures prices begin to move closer to spot prices, there may still be room for futures to rise.

On the premise that the industrial capacity has indeed increased significantly and the industrial operating rate is not low, the industrial inventory has not been effectively accumulated. The first reason is that the actual effective capacity is smaller than the industrial statistics. The price of corn starch dropped from a high of more than 3000 yuan/ton in 2015 to below 1900 yuan/ton in 2017. The dividend of low price creating demand has always been there. According to the data of the Starch Industry Association, since January 2015, the monthly demand for corn starch has maintained a positive year-on-year growth for 44 consecutive months. Since January 2018, the downstream consumption of corn starch has not only seen considerable growth in traditional starch sugar, food and other fields, but also has largely replaced cassava starch in the paper industry, and created new demand for flour blending and shaping agent in feed. Due to environmental protection and other factors, the zombie production capacity of the industry is not small, and the effective supply has been insufficient. According to industry feedback, since this year, production restrictions in Northeast China and North China have continuously affected the effective supply of the industry, and will continue in the foreseeable future. In addition, many small and medium-sized enterprises that were originally quite active have actually changed into zombie production capacity due to various factors such as poor operation. In the future, the possibility of re effective opening is not very great, that is, the actual effective capacity of the industry is less than the situation of the industry statistics. On the other hand, the demand should be in effective growth and exceed the industry expectation. The downstream food and paper industry's consumption demand is warmer, the purchase and sales activities of factories such as fans, noodles, flour addition are brisk, the traders' enthusiasm for stocking up is improved, the demand is relatively strong, and the effective supply of the industry is insufficient, which will inevitably lead to the continued upward trend of corn starch prices!

3、 Due to the increase of tax rebate, the export of corn starch will reach a new peak

According to customs data, in September 2018, China exported 47375 tons of corn starch, up 235% year on year and 4.84% month on month. From January to September 2018, 382000 tons of corn starch were exported, a sharp increase of 120.15% over the previous year. In fact, the export volume of corn starch from January to September this year has increased by 49.69% compared with the export volume of the whole year last year. At present, we believe that the total export volume of China's corn starch in 2018 can be calculated in the following two ways: first, the average monthly export volume in the first nine months of 2018 is 42447 tons, so that the total export volume in the 12 months of the year will be 509400 tons, a sharp increase of 99.59% over the previous year; Second, the subtotal export in the first nine months of 2018 increased by 96.5% over the same period of the previous year, so that the total export volume in 2018 will be 501400 tons. In short, China's total export of corn starch this year will far exceed the peak of 445000 tons in 2008, a new peak. In 2018, the export of corn starch increased significantly more than expected by the industry. One is the new export demand created by relatively low prices after China's cost fell; In addition, more importantly, the cassava harvest in Southeast Asia has been poor for two consecutive years, and the relatively low price corn starch imported from China is needed to fill the local gap. Therefore, the strong export trend will continue and is expected to reach a new high.

4、 Future market research and trading strategy

To sum up, first of all, from the perspective of upstream cost side corn supply and demand, China's corn production has been decreasing since 2016/2017, while the demand has been increasing since 2015/2016, showing a scissors gap between production and demand. In 2017/2018, there was a gap in supply, and the huge national reserve inventory accumulated before was beginning to be consumed. At the end of 2017/2018, the inventory consumption ratio dropped to 47%. In 2018/2019, the inventory consumption ratio decreased to 35%. The supply of corn market is expected to tighten significantly, and there is a basis for the price to rise trend. Moreover, from the perspective of starch spot market, it has always maintained a tense state. Since 2016, the output and consumption of starch have increased significantly. In order to catch up with the growth rate of GDP, we expect that the starch production capacity will continue to expand in the next two to three years. In addition, under the premise that the industrial capacity has indeed increased significantly and the industrial operating rate is not low, the industrial inventory has not been effectively accumulated. The first reason is that the actual effective capacity is smaller than the industrial statistics, and the effective supply has been insufficient. Second, demand should be in effective growth and exceed industry expectations. Third, in 2018, the export of corn starch increased significantly more than expected by the industry. First, the new export demand created by relatively low prices after China's costs fell; In addition, the cassava harvest in Southeast Asia has been poor for two consecutive years, and it needs to import relatively low price corn starch from China to fill the local gap. Therefore, the strong export trend will continue and is expected to reach a new high. Therefore, in the case of tight supply and demand and a sharp increase in exports, it is expected that the future price of corn starch will continue to strengthen.

Based on the above judgment, we chose the trading strategy of long corn starch futures:

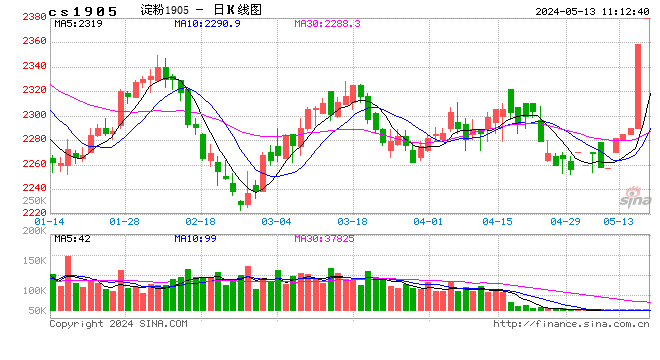

(1) Transaction contract: cs1905,

Trading direction: buy

Entry point: 2460-2475

Target price: 2480-2600

Stop loss position: 2300 -- 2430

It is planned to occupy 38% of the total capital and buy 800 hands.

Hehe Futures Team 1

Sina statement: The purpose of posting this article on Sina.com is to convey more information, which does not mean to agree with its views or confirm its description. The content of this article is for reference only and does not constitute investment advice. Investors operate accordingly at their own risk.

Editor in charge: Song Peng