Author: Ai AA

Source from quadrant

No company's IPO path is as tortuous as that of Himalaya. Over and over again, from September 2021 to March 2022, each time seemed within reach, but each time failed at the last moment.

On April 12, 2024, the Himalayas launched a third impact on the Hong Kong Stock Exchange. This time, with the aura of profit, it tried to persuade the market and investors again that it had found the way to success.

However, the story behind profitability is not as simple as business growth. In addition to the "financial technology" modification, most of the profits are also from cost control, and only a small part is from business growth.

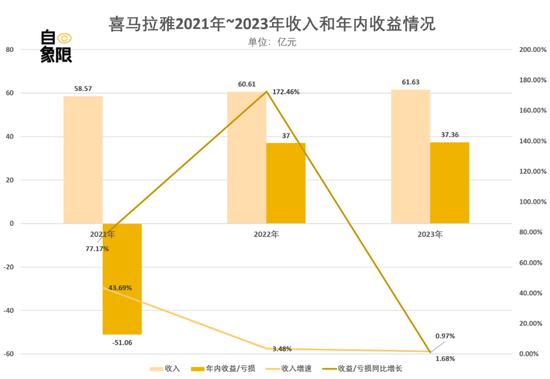

▲ Data source Prospectus self image limit chart

The deeper problem is that although Himalaya has made profits, its business model has not changed fundamentally, and the growth of paying users has begun to show signs of fatigue. For the online audio market, user growth and participation, as well as the conversion rate of paid users, are important indicators to measure the future growth potential of an enterprise.

At the same time, the competition in the online audio industry has become increasingly chaotic, ranging from audio novel platforms such as QQ reading and lazy people listening to books to Netease Cloud Music, QQ Music and even WeChat. In this situation of multi-party separatism, even if Himalayas want to achieve the positioning of "small and beautiful", they are also facing considerable challenges.

Therefore, the fierce market competition requires the Himalayas to constantly seek new ways to cope with new challenges. Even if the IPO is successful, what can be solved is only urgent. Under such a background, where is the way out for Himalayas?

Make profits, treat symptoms but not root causes

As mentioned above, the biggest confidence of the Himalayan Sanzhan Port Exchange is that it has finally achieved profitability this time.

According to the data in the prospectus, from 2021 to 2023, the Himalayas recorded annual gains/losses of - 5106 million yuan, 3.70 billion yuan and 3.736 billion yuan respectively. That is, since 2022, the Himalayas have changed from the state of continuous losses in previous years and realized profits for the first time.

One of the key problems is that in 2021, the Himalayas will still lose 5.106 billion yuan, but it will take only one year to achieve a profit of 3.70 billion yuan. It is equivalent to that Himalaya has made the net profit increase by 8.806 billion yuan in one year. This obviously does not conform to its revenue and profit growth model in previous years.

The "Self Quadrant" disassembly of the prospectus found that there were abnormalities in the distribution of share based payment fees between employees and non employees in Himalaya.

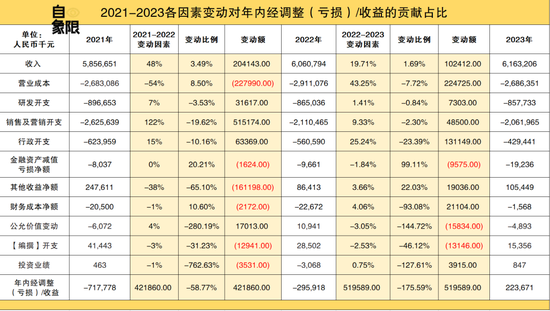

For example, the Himalayas included 790 million yuan of share based payment expenses in administrative expenses in 2021, and the administrative expenses of 545 million yuan were backflushed in 2022 due to the estimated deviation in 2021.

This totally unrelated operation is equivalent to directly moving the cost in 2022 to 2021, resulting in a difference of 1.335 billion yuan between the two years' costs.

In addition to adjusting share based payment fees, from 2021 to 2023, the impact of changes in the fair value of Himalayan convertible redeemable preferred shares on final profit and loss is also quite amazing.

In 2021, a loss of 3.411 billion yuan was generated due to the decline in the fair value of convertible and redeemable preferred shares. In 2022, the increase in the fair value of convertible and redeemable preferred shares will bring about an income of 3.559 billion yuan. This alone will lead to a direct increase of 6.970 billion yuan in profits and losses in 2022 compared with 2021.

Although these adjustments are reasonable in accounting, they cannot reflect the core profitability of the company. That is to say, the profits of Himalaya in 2022 are not derived from business growth, but more from "financial technology".

Even leaving aside this part of financial means, only from the adjusted data, the profits and losses of Himalayas in 2022 and 2023 are very limited, and the benefits brought by business growth are more the result of cost reduction and efficiency increase.

From the data of the prospectus, from 2021 to 2022, the income of Himalayas increased by 3.49%, about 204 million yuan; But at the same time, operating costs also increased by 8.50%, about 228 million yuan. The two offset each other. The real reason for the sharp decline in adjusted losses in the year was the decline in sales and marketing expenses.

Compared with 2021, the sales and marketing expenses in 2022 will decrease by 19.62%, about 515 million yuan, contributing 122% to the change of final profit and loss.

From 2022 to 2023, while the revenue increased by 1.69%, the operating cost decreased by 7.72%, which together with the decline of administrative expenses constituted the main reason that affected the adjusted income in the year.

In a word, the key factor to turn loss into profit in Himalaya is not the natural growth of core business, but mainly comes from strict cost control.

However, the sustainability of this profit growth achieved by cost reduction is questionable. Once the cost is reduced to the bottom line, the company may fall back into the dilemma of growth

▲ Data source Prospectus self image limit chart

This dilemma is more caused by the peak growth of Himalayan users.

As an online audio platform, the largest revenue of Himalaya comes from user subscriptions. From 2021 to 2023, subscription revenue will account for 51.51%, 50.8% and 51.7% of Himalayan total revenue respectively.

The amount of subscription revenue depends on the size of users and the conversion rate of payment. But in both cases, the Himalayas can see the obvious ceiling.

From 2021 to 2023, the average monthly active subscribers in Himalaya will total 267.9 million, 291.2 million and 302.6 million, with growth rates of 8.70% and 3.91% respectively, and the growth trend will slow down significantly.

The situation of paying users is even worse.

From 2022 to 2023, the average monthly active users of Himalayan mobile terminals will increase by 11.3 million person times, but the number of paid users and paid members will only increase by 0.1 million person times and 0.2 million person times, respectively. The proportion of new monthly active users to paid users/members will be as low as 0.88% and 1.77%.

Compared with the payment rate in the past three years. From 2021 to 2023, the average monthly active paying subscribers of Himalayan mobile terminals will account for 12.9%, 12.9% and 11.9% respectively, while the proportion of paying members will be 12.4%, 12.6% and 11.6% respectively.

It can be said that the Himalayas did attract new users through marketing, but they were unable to successfully convert traffic into paying users, and the growth of paying users has been sluggish.

Therefore, looking back on the latest prospectus of Himalaya, profitability is indeed a bright spot, representing that Himalaya finally has the ability of self hemopoiesis. But at the same time, its performance is not as good as it seems.

In other words, although Himalaya has achieved profitability, it is still above the threshold that existed three years ago and has not yet broken through.

The cake is not big, but everyone wants to share it

In the prospectus, Himalayas positioned themselves as an online audio platform.

This is actually a very big, imaginative, but also very broad concept. It means that everything related to audio and "ears" can be summarized.

The Himalayas did the same thing, that is, they built a rich ecosystem and content system with audio as the center.

Open the home page of Himalaya, we will see the contents classified, including but not limited to music, business finance, audio books, crosstalk storytelling, radio dramas, etc.

▲ Screenshot of Himalayan official website

But the other side of pan also means that it is not good enough, and there are too many opponents and too long battle lines.

Take radio dramas as an example. Although Himalayas have the content of this category, it is not sophisticated enough.

In the same scene, there are more focused products, such as Cat's ear FM, which focuses on the secondary meta culture, and works with voice actors and production teams to create exclusive radio drama content. Its dialogue driven narrative mode can simulate a variety of scenes and sounds, giving the audience a three-dimensional auditory experience.

In addition, NetEase Cloud Music also launched the "Theatre of Sound" module, which launched a number of well produced radio dramas and audio novels.

In contrast, Himalayan radio dramas are more inclined to the traditional audio book mode, telling in the form of narration. In terms of creating scene atmosphere and role interaction, they are not as immersive and picturesque as cat ear FM.

In the field of podcasting, small universe, Apple's podcasting application, pirate radio, etc. can also provide the same experience. Taking Xiaouniverse as an example, as an application specially designed for podcasting, it has more advantages than Himalaya in terms of content richness, updating speed, and having a number of well-known content brands.

▲ Summary of major online audio platforms

In addition to the competition in these subdivisions, the Himalayas also face many big and comprehensive competitions.

For example, Netease Cloud Music, QQ Music and other online music streaming media platforms naturally have users and scenes listening to audio, and the user scale is far larger than that of Himalayas. These two streaming media platforms also have audio books, broadcasting, knowledge payment, podcasting and other functions.

So by contrast, although Himalaya is China's largest online audio platform [1], its location is also extremely awkward.

In addition, the market size of online audio has reached the ceiling.

The report of iResearch shows that in 2022, the market size of domestic network audio platform will be 11.58 billion yuan, with a year-on-year growth of 15.6%. It is expected that the total market volume will maintain a steady and rapid growth, and the growth rate will tend to slow down after rising. It is expected that the growth rate will fall from 19.2% in 2023 to 9.5% in 2026.

At the same time, the low barriers to entry in the market make the competition more intense. In addition to its own online audio platform, short videos, e-book reading, and even news platforms can easily and quickly enter this market.

For example, the "Listen" mode has been added to today's headlines as a news information platform, and the "Listen" tab has also appeared on the discovery page of WeChat APP. Even Bilibili, famous for comprehensive video sharing, has introduced the option of "listening to video" in "more services".

The cake of the online audio market is becoming slower and slower, but more and more people are sharing it. Many new entrants are trying to get a piece of the cake.

The Himalayas will be in an increasingly difficult situation.

Where is the way out for Himalayas?

To answer this question, the first thing to think about is - where is the core growth point of the current online audio market?

The online audio payment problem is well known.

As an important player in the industry, Himalaya initially focused on white-collar workers and elites in the first and second tier cities, with knowledge payment as its main service content.

But today, we will find that the focus of the market has changed. On the one hand, the early primary and secondary white-collar market has gradually saturated; on the other hand, users' preferences for audio content are changing.

According to the Research Report on China's Online Audio Industry in 2023 published by iResearch, the user's payment preference has gradually shifted from knowledge payment to content payment, especially audio books and radio dramas.

According to the data, 71.2% of the users prefer to buy platform members, while the content they most often listen to is audio books and radio dramas, and the paid for knowledge courses rank second. In addition, the main purpose of listening to audio is entertainment and relaxation, accounting for 70.6%, while the demand for self improvement and knowledge expansion is 37.5% and 28.6% respectively.

This shift means that the Himalayas need to re-examine their content strategy. Although Himalaya has tried audio books and radio dramas, these attempts conflict with its original knowledge payment strategy, resulting in that the business in this field does not fully meet the expectations of the market.

For the audio book and radio drama market, users obviously pay more attention to content quality and are more willing to pay for good content.

At the same time, Himalayan user portraits show that the main user groups are middle and high consumption people in the first and second tier cities. However, with the change of China's population structure, the demand for audiobooks of middle-aged and elderly people is growing day by day, and this market has huge potential.

According to the data of the National Bureau of Statistics, by the end of 2023, the proportion of the population aged 60 and above in the total population will increase to 21.10%, and the "silver economy" will become a new economic growth point.

In the face of these changes, perhaps the best solution for Himalayas is to return to the market and deeply understand the real needs of users. Look at what the market really needs, not what it wants to do.

Through in-depth strategic adjustment, Himalaya may be expected to find new growth points in the online audio market and achieve more long-term and stable development.

(Statement: This article only represents the author's view, not Sina.com's position.)