Former title: Zou Chuanwei: Special Drawing Right Innovation in the Digital Currency Era of the Central Bank

Zou Chuanwei (the author is chief economist of Wanxiang blockchain)

Zhou Xiaochuan put forward suggestions on SDR reform in 2009. At present, the development of the central bank's digital currency provides new systems and technical tools for implementing these reform suggestions.

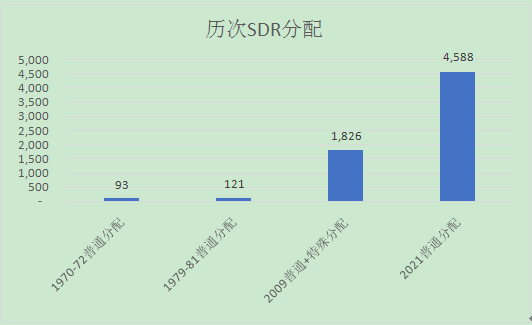

On March 23, 2021, Kristalina Georgieva, President of the International Monetary Fund (IMF), announced that he planned to add $6500 of Special Drawing Rights (SDRs) to meet the global long-term demand for reserve assets and help the global economy recover from the impact of the new pandemic. This plan will be submitted to the IMF Executive Board before June this year. After the Executive Board agrees, it will be submitted to the IMF Council, and can be passed if more than 85% of the votes support it. If approved, this will be the fourth and largest SDR allocation in IMF history, which will increase the cumulative SDR allocation from 2041 SDR to 6628 SDR, about 939 billion US dollars (Figure 1, using the exchange rate of 1 SDR=1.416620 US dollars on April 1, 2021, the same below)

Figure 1: Previous SDR allocation (unit: 100 million SDR)

1、 Background

Historically, there have been many discussions on how to improve the SDR creation and distribution mechanism, and broaden the scope of SDR use. On March 23, 2009, Zhou Xiaochuan, the then governor of the People's Bank of China, published "Reflections on the Reform of the International Monetary System", which attracted widespread attention at home and abroad. On October 1, 2016, RMB was officially included in the SDR currency basket. As of April 1, 2021, the weights of USD, EUR, RMB, GBP and JPY in SDR currency basket are 41.1%, 32.0%, 10.9%, 8.4% and 7.6% respectively. Before the middle of 2022, the IMF will conduct a routine review of SDRs (usually every five years).

In the past five years, one of the biggest changes in the international monetary system is the rise of central bank digital currency. In 2016, the Bank of England published a working paper on central bank digital currency. Since April 2020, digital RMB has been piloted in many cities in China, and will be expanded to the Winter Olympics scene early next year. The Federal Reserve Boston Branch is cooperating with MIT to study digital dollars. Jay Powell, chairman of the Federal Reserve, called it the "high priority" project of the Federal Reserve when he testified in the Senate on February 23, 2021. In October 2020, the European Central Bank released its first digital euro report. On April 5, 2021, the Bank of Japan announced that the first phase of the central bank's digital currency concept verification will be carried out in the next year.

Some scholars have noticed the relationship between central bank digital currency and SDR innovation. In May 2019, Tobias Adrian, Director of IMF's Monetary and Capital Markets Department, proposed eSDR (electronic SDR) or dSDR (digital SDR) at the IMF Swiss Central Bank meeting. In December 2019, Zhou Xiaochuan, who served as the vice president of the Boao Forum for Asia, said at the second "Asia Europe Cooperation Dialogue" of the Boao Forum for Asia that at present, the world really faces the opportunity to promote global digital currencies such as eSDR (electronic special drawing rights) and SHC (synthetic hegemonic currency), but this requires an institution similar to the global central bank. But they did not elaborate on relevant concepts.

After the COVID-19 pandemic, major reserve currency issuing countries launched unlimited quantitative easing and large-scale fiscal stimulus plans. The defects of the international monetary system pointed out by Zhou Xiaochuan in 2009 became more prominent. With the new round of SDR allocation, the importance of SDR in the international monetary system will increase. Under these circumstances, SDR needs more innovation, and some research and practice in the field of digital currency in the past two years will help to better study this issue. First, since 2019, Libra project (now renamed Diem) has explored a basket of currency stable currencies, deepening the understanding of the design and application of super sovereign digital currencies. Second, in March 2020, with the support of the Bank for International Settlements (BIS) Hong Kong Innovation Center, the Hong Kong Monetary Authority, the Bank of Thailand, the Central Bank of the United Arab Emirates and the People's Bank of China Digital Currency Research Institute announced to jointly launch the Multi CBDC Bridge research project of multilateral central banks, in addition to improving cross-border payments, It will also promote the interconnection between digital currencies of multinational central banks.

2、 Zhou Xiaochuan's Suggestions on SDR Reform in 2009

SDR is a supplementary international reserve asset created by IMF in 1969, which, together with gold and foreign exchange, constitutes international reserves to support the growing international trade and financial activities. The background of SDR is the "Triffin dilemma" under the Bretton Woods system - the United States exports US dollars as an international settlement tool through the current account deficit, but the continued US current account deficit will shake the confidence of international investors in the US dollar.

SDR is neither a currency nor a claim to IMF, but a potential claim to a group of freely usable currencies (currently including US dollar, euro, RMB, British pound and Japanese yen). SDRs can only be held by IMF, member states and some designated institutions, not by private sector institutions or individuals. SDR is used as the unit of account by IMF, Bank for International Settlements, African Open Bank, Asian Development Bank, Islamic Development Bank and other international institutions. SDR is mainly used for transactions between IMF member countries and official institutions such as IMF and other international financial organizations, including the use of SDR in exchange for freely usable currency, the use of SDR to repay IMF, pay interest or pay share capital increase.

At present, SDR holders can exchange SDR for freely usable currency in two ways. First, through voluntary trading arrangements among IMF member countries. Second, in the case of unsuccessful voluntary exchange arrangements, the IMF designated member countries with sufficient external positions to purchase SDRs from member countries with insufficient external positions in freely usable currencies.

The value of SDR mainly comes from the commitment of IMF member countries to exchange SDR into freely usable currency. The IMF calculates and publishes the SDR exchange rate every day, which is equal to the sum of the market exchange rate of the basket currency against the US dollar and the number of basket currencies multiplied by 12 o'clock in the London market every day. The IMF calculates and publishes the SDR interest rate every Friday, which is equal to the weighted average of the representative interest rates of three-month debt instruments in the currency market of the basket currency.

After the collapse of the Bretton Woods system in 1973, the major currencies shifted to the floating exchange rate system, reducing the dependence on SDR as a global reserve asset. On the other hand, the growth of the total amount of SDR is completely determined by negotiation, and the decision-making cycle is long, which cannot keep up with the global demand for reserve assets. Therefore, the proportion of SDR in global reserve assets is declining, and the role of SDR has not been fully played. Zhou Xiaochuan's Thoughts on Reforming the International Monetary System in 2009 put forward the following important views on SDR reform:

First, the current use of sovereign credit currency as the main international reserve currency is a rare exception in history, and its disadvantages are reflected in three aspects. First, the "Triffin dilemma" still exists in theory, and reserve currency issuers cannot ensure the stability of currency value while providing liquidity to the world. Second, the monetary policy objectives of reserve currency issuers often conflict with the requirements of various countries for reserve currencies, which may be unable to fully meet the growing demand of the global economy due to the need to curb domestic inflation, or may lead to the overflow of global liquidity due to excessive stimulation of domestic demand (note: this disadvantage is more prominent after the pandemic of COVID-19). Third, when a country's currency becomes the world's primary product pricing currency, trade settlement currency and reserve currency, the country's exchange rate adjustment to economic imbalances is invalid. The overall effect is that economic globalization not only benefits from a widely accepted reserve currency, but also suffers from the institutional defects of issuing such currency. Not only do the users of reserve currencies have to pay a heavy price (for example, they are worried about the devaluation of reserve currencies), but also the issuing countries are worried about the impact of the weakening confidence of the users on their own economy and monetary policies.

Second, the international reserve currency should be improved in the direction of stable currency value, orderly supply and adjustable aggregate. The super sovereign reserve currency managed by a global institution not only overcomes the inherent risks of sovereign credit currency, but also provides the possibility to regulate global liquidity, which can greatly reduce the risk of future crises and enhance the ability to deal with crises. It is the ideal goal of the reform of the international monetary system. SDR has the characteristics and potential of super sovereign reserve currency. The scope of SDR should be widened to truly meet the requirements of countries for reserve currency. The specific measures are as follows. First, establish the clearing relationship between SDR and other currencies, so that it can become a recognized means of payment for international trade and financial transactions. Second, actively promote the use of SDR pricing in international trade, commodity pricing, investment and enterprise bookkeeping. Third, actively promote the creation of SDR valued assets (note: the World Bank issued SDR valued bonds in 2016). Fourth, the basket currency range of SDR setting should be extended to major economic countries in the world, and GDP can also be considered as one of the weighting factors (note: RMB was included in the SDR basket in 2016). Fifthly, the issuance of SDR can also change from artificially calculated currency value to the way supported by real assets. It can consider absorbing the existing reserve currencies of various countries as its issuance preparation.

Third, the IMF's centralized management of part of the reserves of member countries will not only play a more effective role in deterring speculation and stabilizing the market than the decentralized use and separate operations of countries, but also promote the SDR to play a greater role as a reserve currency. The IMF can set up an open-ended fund in a market-oriented mode and issue fund units valued in SDR to member countries. Member countries can freely subscribe with existing reserve currencies and redeem the required reserve currencies when necessary. This can even serve as the basis for increasing SDR issuance and gradually replacing the existing reserve currency.

Considering that the major reserve currency issuing countries have not yet withdrawn from the quantitative easing and unconventional monetary policies after the international financial crisis, but also launched unlimited quantitative easing and large-scale fiscal stimulus due to the new coronal epidemic, President Zhou Xiaochuan's above reform proposals are more meaningful at present, and the development of the central bank's digital currency, It provides new systems and technical tools for the implementation of these reform ideas.

3、 SDR innovation based on central bank digital currency

SDR innovation is reflected in the payment and clearing infrastructure, value connotation, issuance and redemption system (primary market), trading mechanism (secondary market), SDR valuation assets, etc., but the most important is the payment and clearing infrastructure, because it is the basis for broadening the use of SDR.

(1) Payment and clearing infrastructure

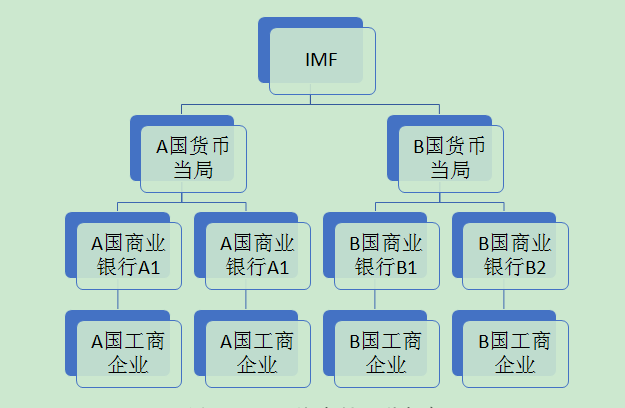

At present, the account system managed by IMF records the holding and circulation of SDRs. To expand the holding range of SDR from IMF, monetary authorities of member countries and some designated institutions to commercial banks and industrial and commercial enterprises of member countries, one method is to allow commercial banks and industrial and commercial enterprises of member countries to access SDR account system, and the other method is to use distributed ledger (DLT). This paper prefers the second method. First, the distributed ledger is more open, which helps commercial banks and industrial and commercial enterprises in member countries to hold and use SDRs. Secondly, distributed ledgers can better support the application of SDR in international trade and finance. Finally, the distributed ledger can better support the central bank's digital currency.

Under the distributed ledger, SDR adopts a hierarchical operation framework (Figure 2). The first level is the IMF, the second level is the monetary authorities and some designated institutions of member countries, the third level is the commercial banks of member countries, and the fourth level is the industrial and commercial enterprises of member countries. This article does not consider the situation that individuals hold SDRs, that is, SDRs do not enter the retail payment process. From the perspective of member states, each layer of "IMF monetary authority commercial banks industrial and commercial enterprises" is a "wholesale retail" relationship. In addition to direct transactions with IMF, the monetary authorities of member countries can also use SDR for direct transactions with each other. SDR can be used for direct transactions between commercial banks of member countries and industrial and commercial banks, which are not necessarily limited to the same country, but cannot be directly traded with monetary authorities or IMF of other countries. These restrictions can be implemented by smart contracts in distributed ledgers.

Figure 2: Layered operation framework of SDR

Table 1 shows the corresponding positions of different SDR use scenarios in the layered operation framework:

Table 1: SDR usage scenarios

(2) Value connotation

SDR is a claim to a set of freely usable currencies. Monetary authorities of member countries can redeem a set of freely usable currencies from IMF with their SDRs according to the composition of SDR currency basket. The IMF's ability to deal with SDR redemption comes from two aspects:

1. SDR issuance reserve;

2. Liquidity support from the monetary authority corresponding to each component currency.

Under this arrangement, SDR will no longer be an artificial calculation of currency value, but will be supported by real assets. Since the monetary authorities of member countries may not redeem SDRs from IMF at the same time, and they can also use currencies freely if they need, through voluntary exchange arrangements, SDR issuance can be based on partial reserves. This reflects the role of the law of large numbers.

As the "Liquidity Provider of Last Resort", the monetary authority corresponding to each component currency will play an important role in the stability of the SDR system to ensure that no runs against SDR will occur.

(3) Issuance and redemption mechanism

SDR is issued based on partial reserve, and the issuing reserve comes from the following two sources:

1. Initial capital injection by the monetary authority corresponding to each component currency;

2. The currency of member countries subscribes SDRs from IMF with a set of freely usable currencies, and IMF issues new SDRs and injects subscription funds into the issuance reserve.

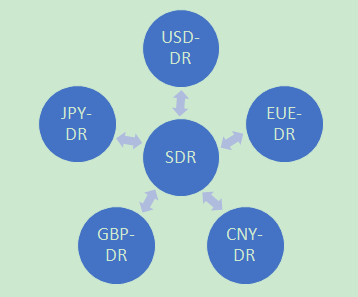

SDRs are issued and circulated on distributed ledgers. This distributed ledger is the "corridor network" in the digital currency bridge of multilateral central banks. For each component currency, the central bank digital currency system of the corresponding monetary authority (if there is no central bank digital currency, the real-time full payment system RTGS is used) is connected to the "corridor network", where there are depositary receipts of the currency. The monetary authority is responsible for 1:1 two-way exchange between the central bank's digital currency and depositary receipts on the "corridor network".

SDR is composed of smart contracts and depositary receipts on the "corridor network" according to the currency basket (Figure 3, depositary receipts are marked with DR):

Figure 3: Synthetic SDR on "Corridor Network"

SDR can be issued in two ways. First, the IMF Council and the Executive Board will negotiate to determine the timing and number of additional SDRs. This will be accompanied by the adjustment of SDR issuance reserve ratio. In other words, SDR issuance follows the "adjustable fractional reserve". Historically, SDR reissues decided by the IMF Council and the Executive Board through consultation will not be very frequent, but the number may be large each time. The additional SDRs can be allocated to the monetary authorities of member countries in proportion (i.e. the current universal distribution mechanism), or a certain proportion can be reserved for centralized use by the IMF, or the distribution proportion to key currency countries can be appropriately reduced.

The second is market-oriented issuance, in which the monetary authorities of member countries subscribe for new SDRs from IMF with a set of freely usable currencies. The time and quantity of market-oriented issuance is determined by the monetary authorities of member countries according to their own needs, which can be very flexible, and is accompanied by the withdrawal of the corresponding SDR basket currency shares by the monetary authorities of member countries. This will directly boost the demand for RMB as an international reserve currency, especially when GDP is considered as one of the weight factors of SDR currency basket. In contrast, the current ordinary SDR distribution mechanism does not play a direct role in promoting the position of RMB as an international reserve currency. Finally, market-oriented issuance will enable the IMF to centrally manage part of the reserves of member countries.

It should be noted that some scholars proposed that SDR should have an endogenous expansion or contraction mechanism of credit currency in quantity, which means that SDR has the characteristics of "loan accompanied by deposit currency creation". Because this plan will give the IMF too much discretion, this article has reservations. SDR issuance, on the one hand, should meet the demand of member countries' monetary authorities for reserve assets; on the other hand, it should follow perfect governance rules, and the core is the balance between member countries' monetary authorities and IMF.

When the monetary authorities of member countries redeem their SDRs from the IMF, they will obtain a set of depositary receipts of freely usable currencies on the "corridor network". They can adjust the position of depositary receipts through the trading mechanism described below (such as selling EUR-DR and buying CNY-DR), and then obtain the desired freely usable currency through the corresponding monetary authority. When dealing with SDR redemption, the IMF first uses SDR issuance reserves, and if there is a shortage, it uses the liquidity support of the monetary authority corresponding to each component currency.

Under this new issuance and redemption mechanism, the IMF can continue to calculate and publish the SDR exchange rate every day. This exchange rate mainly serves as a reference (referred to as the "reference exchange rate"). The SDR exchange rate will be determined by the market (referred to as the "market exchange rate"). However, driven by arbitrage activities, the market exchange rate will converge to the reference exchange rate. The logic is as follows. If the market exchange rate exceeds the reference exchange rate, the monetary authorities of member countries will subscribe for the newly issued SDR from the IMF with a set of freely usable currencies. The cost of this strategy is linked to the reference exchange rate, and the income is linked to the market exchange rate, so as to obtain excess returns. However, other conditions are the same, the increase of SDR supply will drive the market exchange rate down. Conversely, if the reference exchange rate exceeds the market exchange rate, the monetary authorities of member countries will use SDR to redeem a group of freely usable currencies from IMF. The cost of this strategy is linked to the market exchange rate, and the income is linked to the reference exchange rate, which can also obtain excess returns. However, other conditions are the same, the decrease of SDR supply will drive the market exchange rate to rise. The overall effect is that the SDR market exchange rate will fluctuate around the reference exchange rate, still showing a low volatility, so as to mitigate the asset price fluctuations and related risks caused by the use of sovereign credit currency pricing, especially for primary products around the world.

(4) Transaction mechanism

The transactions between SDR and various constituent currencies (actually depositary receipts) take place on the "corridor network", and can support payment versus payment through smart contracts. The transaction efficiency is very high. Corresponding to the hierarchical operation framework of SDR, the transaction mechanism is also hierarchical:

1. The monetary authorities of member countries and IMF conduct SDR transactions on a set of freely usable currencies. This corresponds to the market-oriented issuance and redemption of SDR, which will make the SDR market exchange rate converge to the reference exchange rate.

2. Transactions between monetary authorities of member states on various currencies and SDRs. This will help the monetary authorities of member countries adjust their currency positions and form the exchange rate of SDR against each component currency.

3. In each member country, transactions between monetary authorities and commercial banks, as well as between commercial banks and industrial and commercial enterprises, on domestic currency and SDR. This corresponds to the SDR distribution mechanism in member countries.

The overall effect is that based on the "corridor network", an active foreign exchange market will be formed around SDR and currencies of all components.

(5) SDR Valuation Assets

With the expansion of the use of SDR, the number of SDRs held by monetary authorities, commercial banks and industrial and commercial enterprises in member countries will often be mismatched with the demand for SDR, so they need to constantly allocate SDR resources in both time and space dimensions, which is the internal driving force behind the emergence of SDR denominated assets. This also shows that the core reason for the slow development of SDR denominated assets is that SDR is not widely used and the demand for allocating SDR resources through the market is not strong.

In the long run, the market will develop a yield curve that can reflect the supply and demand of SDR. SDR itself does not pay interest, but the bonds and loans priced by SDR will pay interest, and the SDR interest rate will be determined by the market rather than artificial calculation. At present, the SDR interest rate is mainly self financing - first allocate fees to SDR, and then use the fees obtained to pay the interest on holding SDR.

Massive information, accurate interpretation, all in Sina Finance APP

Editor in charge: Fan Di